Executive Summary

The fundamental purpose of financial planning is to help clients make better financial decisions to achieve their financial goals – and hopefully to feel happy or empowered along the way by having made those decisions. Yet as most financial advisors know from experience, getting clients to make better decisions (and ones that they feel happy about) is not so easy in practice.

Clients do not always listen. Clients don’t always follow through on the advice they are given. And sometimes clients even do things that truly worry us, and actually endanger their financial health in the process. And unfortunately, there is remarkably little training on what financial advisors should actually do in such instances!

In this guest post, Meghaan Lurtz, our Senior Research Associate at Kitces.com, explores how the tools and techniques of Financial Therapy could be that research-based solution that financial planners may want to give some serious consideration to for training on how to deliver better advice that actually sticks, and to learn to better help clients actually help themselves. Perhaps even more so than the recently in-vogue Behavioral Finance research, which in practice is more focused on categorizing the problem behaviors that clients tend to express, than what financial advisors can and should actually do about it.

For instance, Financial Therapy utilizes techniques like Solution-Focused Therapy (SFT) to help clients figure out what skills they may already possess to overcome their own (financial) challenges. Financial Genograms provide a means to unearth clients’ financial family history and how the relationships around them may be influencing their money behaviors. And exercises like “What Do You Believe” help to unearth and explore money scripts that may cause clients to get stuck in a financial rut, as their sometimes subconscious limiting beliefs sabotage their ability to make good financial decisions.

Of course, the reality is that at some point, problematic financial behaviors cross the line from something that a financial planner can help with (even one trained in financial therapy techniques), into a bona fide psychological disorder that merits a referral to a qualified mental health professional. Nonetheless, a wide range of financial therapy tools and techniques can be applied by financial planners in their routine work with clients, in an effort to help ensure clients actually follow-through on the advisor’s recommendations, and the client’s own financial decisions and commitments.

And fortunately, with the rise of organizations like the Financial Therapy Association, and new educational programs like the Certified Financial Therapist (CFT) designation, there are more opportunities than ever for financial planners to explore the tools and techniques of financial therapy and how they can be applied in a financial planning context with clients!

Why Consider Financial Therapy?

Research in financial planning has demonstrated that advisors spend approximately 25% of their time dealing with non-financial issues, and perhaps more shockingly, 74.4% of advisors have had a client cry, sob, tremble, or become violent. So if you are a financial advisor you have probably experienced (or will experience) one of the following issues surrounding interactions with clients: crying, arguing, immense fear, immense anger, extreme risk-aversion or risk-seeking, death of a family member or spouse, and/or one spouse or both spouses financially enabling an adult child.

The question now is: what do you do in those moments? How do you handle the crying? Do you or do you not comfort the grieving widow(er), and if so, does a tissue suffice? Is it okay to say “things will get better”? Is there something you should say when couples fight in front of you? Can you stop clients from their own self-sabotage without losing them as a client? Have you ever even been trained on best practices for even handling "less extreme" issues, like a client not following through (maybe for the third time) on a recommendation you have agreed upon?

If you are feeling like your answer would probably be, “I just get through the moment as best I can,” or “I have no idea,” or “I don’t know,” or “Wait, are there best practices?” you are not alone. The training advisors receive as part of CFP curriculum is great at the technical issues of financial planning, but does not necessarily prepare advisors to handle any of the emotional and relationship-driven scenarios listed above.

Compounding the intensity of these moments is that, as the financial advisor, you are often the first professional your client may reach out to in a time of financial and/or emotional need, and you are likely the first person that would notice financial behaviors and financial beliefs/fears that may be causing the client harm.

Simply put, you as the financial advisor are often the first line of defense. But without any armaments.

What is Financial Therapy?

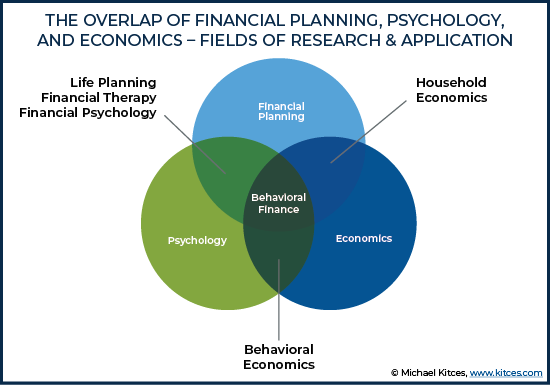

Along with the aforementioned list of common financially-related emotional issues with clients, you have probably (hopefully) also heard of some of the following in response to them: behavioral economics, behavioral finance, evolutionary psychology, financial psychology, and life planning. And now… financial therapy.

Each of these “responses” is slightly different from the others, but each of them is making some connection between our psychology and our money, and in their own ways attempt to provide some of or at least one of the emotional/relational/behavioral tools you may use to help see a client through.

Behavioral Economics: This has become a broad field of study, originating from Kahneman and Tversky’s famous studies, findings, and theory in 1969, and then continually expanding with other great researchers and authors such as Richard Thaler and Hersh Shefrin in the 1980s and 1990s. Behavioral economics looks at economic behavior (e.g., risk/reward trade-offs, and general decision-making under risk) utilizing a behavioral rather than an economically-traditional rational approach. It answers the question: “In what ways are humans continually and predictively going down an 'irrational' path?”

Behavioral Finance: Born out of behavioral economics, but narrower in scope, behavioral finance is focused more directly on irrational behavior in personal finance – asking and answering questions about how individuals “irrationally” react to markets, market behavior, portfolios, and investing. Authors H. Kent Baker and Victor Ricciardi provide an excellent overview of behavioral finance in their book entitled: Investor Behavior The Psychology of Financial Planning and Investing, where they cover many of the cognitive issues brought to light by behavioral economics, but with the specific focus on personal finance and investing.

Evolutionary Psychology: Another field of study dating back to Darwin, but more recently re-popularized by David Friedman. Evolutionary Psychology is no longer concerned with labeling behavior as rational versus irrational, but actually understanding the “why” behind the behavior itself. For instance, humans will in some instances act impatiently (e.g., engaging in hyperbolic discounting) while in other situations be remarkably patient, but instead of just labeling this behavior as irrational, evolutionary psychology tries to understand such behaviors within a new (evolutionary) frame: in what way might this behavior actually have been rational in the context of evolutionary natural selection?

Life Planning: In line with the belief that clients are “rational” and that a particular behavior typically has a (not necessarily apparently but) valid and important reason behind it, life planning programs (e.g., from the Kinder Institute of Life Planning) have been designed such that financial planners, without ever becoming full-blown mental health practitioners, can work with clients towards these healthy money behaviors and ask the big “why” questions. For instance, life planning pioneer George Kinder has discussed how powerful and important it is to explore and understand “freedom” for each client, in addition to (and potentially more so than) the numbers behind client plans. Further, George Kinder points out that if a financial advisor can get to know their client and develop deep trust between him/herself and the client, where the client feels safe enough to reveal very personal information and insight about themselves and feel safe enough share private information, then the financial plan can become transformative and inspirational with respect to a client’s financial decisions and behaviors. Getting in touch with the client’s deepest freedoms excites the client and drives the client to carry out the plan (and change their financial behaviors for the better).

Financial Psychology: In line with the goals from life planning – i.e. happier, healthier clients that feel empowered in relation to their money – financial psychology offers another perspective and approach to working with clients and their money. In fact, in much the same way behavioral finance is effectively focused on behavioral economics, financial psychology in some ways may be the (financial) focusing of evolutionary psychology. For instance, individuals often exhibit a tribe mentality, and a financial comfort zone, when it comes to their money. And given that perspective, it would make sense that the study of financial psychology is also finding that our upbringing, socioeconomic status, gender, and other multi-generational beliefs and family behavior patterns also matter to our money. Moreover, financial psychology homes in on the individual, recognizing many considerations in line with evolutionary psychology, and at the same time, has also begun to consider questions about what might “cure” a client of their maladaptive behaviors (likely rooted in their past money disorders).

Financial Therapy: At around the same time financial psychology entered the world of personal finance, so did Financial Therapy, but they are not exactly the same. Financial therapy, as we know and understand it today, was developed through the collaborations of academics and practitioners from both financial fields and mental health fields. Particular influences were marriage and family therapists, who saw the value of systems theory in better understanding money issues within individuals, couples, and families. As such, financial therapy does work on issues similar to financial psychology with respect to a client’s past and present but does not necessarily use a “medical” model (that all clients need to be “cured”). Thus, while financial psychology focuses on diagnosing, identifying, and curing financial maladies that can have strong connections to diagnosable psychological disorders (such as gambling addiction or hoarding, which in turn necessitate a referral to a licensed mental health practitioner), financial therapy places a greater emphasis on empowering individuals to understand themselves and their relationship with money at a deeper level. Financial therapy also relies on the individual, not necessarily the overarching skills of the therapist, to identify and solve financial issues in their life.

In other words, financial therapists set themselves apart through their deeper understanding of the relational aspects of money, by seeking a more holistic and systemic view of the client and their money struggles (e.g., their family of origin, current intimate relationship dynamics, workplace environment & career, socioeconomic context, social and cultural influences, etc.).

What Are The Tools of Financial Therapy?

The tools of financial therapy are built around “intervention models” (i.e., approaches to "intervening" in a client’s situation), which have been developed using evidence-based approaches - e.g., tested for both practical application (can the financial therapist effectively use the tool/process?) as well as their outcomes (was the client’s financial behavior actually changed for the better after the intervention?). Essentially, a practitioner can trust that, when using an evidenced-based intervention from financial therapy, the “intervention” (e.g., a practice or process, style of question) has been tested in a client-advisor/client-therapist relationship, and it works.

For instance, Solution Focused Therapy is a process-oriented intervention that identifies important financial goals and focuses on helping the client to recognize their own talents in the present moment to move them forward toward those goals (rather than looking at the past or focusing on failures to fix, and rather than having the advisor or therapist try to tell them what should be done).

As an illustrative example, perhaps you and your client have identified that s/he would like to save more money each month. Yet, you and your client have been meeting and discussing this need already, and a strategy for saving more… yet there hasn’t been any change to their savings rate. Instead of just reminding them, pressuring them, or being frustrated with them – you might consider using the process outlined by SFT to get to the heart of the issue, and at the same time build up greater confidence in your client to make the change. …

Research has demonstrated that SFT can be an effective tool as part of a financial goals meeting. An example SFT exchange to address a client with problematic (non-)savings behavior can be seen below.

Advisor: Tell me how your savings efforts are going. (Note the advisor is using an open-ended statement and NOT using a short-answer question like “Have you made changes to your savings rate?”)

Client: My savings haven’t really gone anywhere. I haven’t signed up as I said I would.

Advisor: Tell me what you think is holding you back.

Client: I just don’t have a lot of time. I always think the ideas/plans we have are great, but when I get home I have no energy and do not make the time to make the changes.

Advisor: So I hear you saying you don’t have the time, and life gets busy for you again the minute you leave this office. (Note the advisor is re-affirming what s/he has just heard, to encourage clarity, and a sense of being heard/understood in the client).

Client: That is right, I just get home and life takes over.

Advisor: I understand. Are there other examples, maybe outside of money, that you can think of when you set a goal and yet you made sure that life did not take over? Please take a moment and think of an example, no rush. (Note: Silence is hard, but as the saying goes…it is golden. Especially when you use it to give space to the client for reflection. The advisor is not just listing stuff or coming up with examples for the client, the client needs to find the answer in him or herself.)

Client: Yes, actually, last year I had said that I wanted to start taking walks in the middle of the day to relieve stress. I ended up marking time on my calendar to remind me, and ensure I did not schedule meetings over that time.

Advisor: Great example! If I am hearing you correctly, marking off your calendar was good for you.

Client: Correct! I do best when it is on my calendar and I know there is special, set-aside time already built into my day, so as not to mess up other important things I need to do that day.

Advisor: Perhaps then we have a possible solution, you are already going a great job of identifying what you need for success. Would you be open to making a calendar appointment for yourself now while we are here together today, for some time between now and our next meeting, to log-in and make your savings allocation adjustments? (Note the advisor’s use of compliments, and reinforcing the ability the client sees in him or herself.)

Client: Yes, that sounds like a great idea. I will do that now.

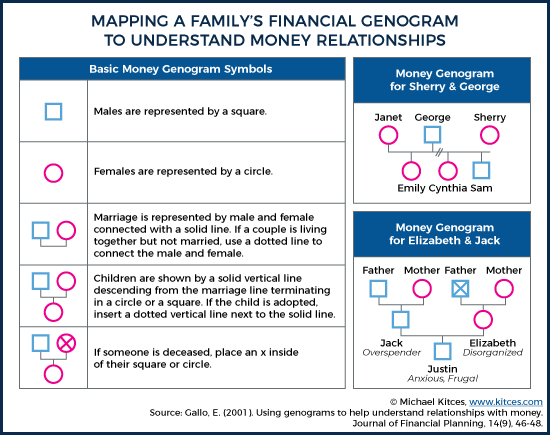

Another great tool coming out of financial therapy is the Financial Genogram. In the therapy world, genograms were developed first by Murray Bowen, and are used to explore a variety of family structures and relationship dynamics, helping clients to recognize familial patterns and their impacts across generations.

A financial genogram is essentially a family tree. Once completed, they often resemble a pedigree chart; where the different lines (dashed, dotted, double, thick, thin, etc.) and the different shapes (squares, triangles, etc.) demonstrate information about the relationships between individuals. In essence, a financial genogram is a historical mapping of family members, and the relationships between the members, which can create insights about the family context of money.

Financial Genograms could be used as part of any intake process with a new client to learn more about how the family and its money are currently structured (and have been structured over the past few generations). Dr. Eileen Gallo with her husband, Jon Gallo, financial planners/estate planners in Los Angeles, actually contributed their findings to the Journal of Financial Planning on how they use Financial Genograms in their work with clients.

Above is an image of a Financial Genogram from Dr. Gallo’s work in the Journal of Financial Planning. The way it works, or the way it can be used, is simply to ask the client to draw out their family tree. Men are boxes, women are triangles, and how the client chooses to draw the relationship (indicated by the line connecting them, which may be squiggled, dashed, broken, straight, or a double-line) tells you about the family dynamics. After the tree is completed (or even while the tree is being completed), the advisor may ask questions about any lessons from the relationships, as they relate to money. For example: “I see you have a close relationship with your parents, that is great. Tell me what they taught you about money?”

In short, the training and the tools of financial therapy offer huge benefits for financial advisors, who are not already mental health practitioners (nor want to be!), because it provides and enhances communication skills and knowledge to move “stuck” clients forward… without worrying about analyzing or diagnosing clients in a medical (e.g., financial psychology) context. It also allows advisors to ask those “why” questions and understand their clients, as well as the world the client sees around them, which provides a more nuanced and interesting picture.

Moreover, just like the practice of massage therapy isn’t mental health therapy, nor is practice of financial therapy techniques exactly the same as mental health therapy – being an attentive listener, a more effective communicator, and possessing a more comprehensive understanding of the complexities within clients’ financial lives certainly does not equate to being (or taking on the burden of) a mental health therapist. Financial planners who receive training in this area simply possess special knowledge and skills which help them to assists their clients make changes as well as provide unique tools and training to help financial advisors address some of the client struggles mentioned above with more finesse and confidence.

How is the Practice of Financial Therapy Different from the Practice of Financial Planning?

Given the overlap between financial therapy and the conversations at least some financial planners already try to have with their clients, a common question that arises is, “what is the difference between a full-blown financial therapist and a financial planner?” (Or at least, “how is or can financial therapy be applied to financial planning to bring about ‘financial planning done well’” for those who want to delve into the deeper issues of the client?)

The main difference between financial planning and financial therapy lies in what would be done, and what would not be done, in the client relationship, as well as the "focus" of the work with clients. In fact, the Financial Therapy Association has designed a new CFT (Certified Financial Therapist) designation, specifically to accommodate both those who want to learn financial therapy and those who are financial planners and don’t want to “do” financial therapy but do want to bolster their financial planning skills.

Thus, the Certified Financial Therapist certification has three levels. The first level is for everyone. CFT-I focuses on basics in therapy, personal finance, ethics, and financial therapy. In many ways, it can be thought of as a refresher to your home discipline (financial planning), and an introduction to therapeutic techniques and practices, as well as ethical considerations that arise in a therapeutic context, and a review of the current research in financial therapy (e.g., taking a deeper dive into areas like Solution Focused Therapy, Systems Theory, and Genograms, as they have been used in client-planner/client-financial therapy meetings).

The second level of the CFT-II has not yet been released, but it will place a greater emphasis on the "doing" of financial therapy techniques. It is also for everyone (i.e., not specific to the practice of financial therapy as a licensed mental health professional). Think of the 2,000 hours you may have had to complete for the CFP. CFT-II won’t require 2,000 hours, but it will be monitoring hours and be completed in a “mentorship” arrangement where you can receive more personalized instruction, feedback, and practice with some of the therapeutic techniques or processes. At CFT-I you read about others’ research on the use and practice of, for example, solution-focused therapy. You may even get some basic instruction through continuing education, webinars, or a conference. but at CFT-II, you are going to personally do, be monitored, and received feedback on your use of Solution Focused Therapy with clients.

The last level, CFT-III, has also yet to be released but is designed for those who will be dually-certified (i.e., a CFP professional and licensed mental health practitioner). In other words, this person will be working as a “full-blown financial therapist” with CFT-III training, which means he/she will be certified by his or her state to practice therapy (in the true mental health sense). Accordingly, the CFT-III student will be spending all of his/her time focused on the emotional aspects of money, and resolving any emotionally-related financial issues that may be present. In addition, because the CFT-III working with clients through the emotional aspects of money, he/she will most often rely on health insurance to bill clients for their work, and typically would not (at the same time) be managing that client’s portfolio.

Notably, though, this does not mean that financial advisors (who are likely not dually certified as licensed mental professional professionals) are banned in any way from using the knowledge and skills gleaned from financial therapy training in their client meetings while continuing financial planning business as normal. In fact, this is why CFT-I and CFT-II exist – so that financial planning professionals can learn and use these skills, without leaving their discipline (financial planning) to engage in the new (and separately licensed) profession of financial therapy. As such, if you are a financial advisor who is interested in and intending to understand your client at a deeper level and wish to become aware of limiting beliefs or difficult relationships in order to assist your financial planning client in connecting with and supporting their own behavior change, you may choose to use financial therapy tools, but you are still doing financial planning – you are not doing “full-blown financial therapy."

In fact, Dr. Kristy Archuleta (a founding member of the Financial Therapy Association) specifically comments on why and how adopting financial therapy practices and skills should be encouraged in financial planning. For instance, in financial planning, we create plans and then deliver to clients what can feel (and often is) a long to-do list. Follow-through on these action item lists is often difficult for clients at best, and abysmal at worst. But good news: the reason is often psychological, and training in financial therapy can help advisors to help their clients to have better follow-through!

Arguably, the only time financial planning and financial therapy skills should truly be separated is when or if the client is genuinely in need of mental health services to truly confront, cure, and heal trauma or another diagnosable mental health issue (e.g., depression, anxiety, hoarding, gambling, grief, etc.). Financial advisors are not therapists any more than a massage therapist is a therapist – to get to know your clients, build deep relationships with your clients, and when or if you need to give them a referral for help that only a licensed mental health practitioner can provide, they will hopefully take and trust your advice.

Practical Applications for Financial Advisors

As previously stated, Genograms and/or Solution Focused Therapy are just two of the many tools financial planners can use with clients without being in fear of crossing over ethical or practice lines. A list of additional webinars on tools and practices of financial therapy and how it can be applied in financial planning can be found on the Financial Therapy website along with other resources for financial planners.

Another great and practical tool, entitled “What Do You Believe”, comes from the book “Facilitating Financial Health: Tools for Financial Planners, Coaches, and Therapists” by Klontz, Kahler, and Klontz, and addresses clients’ financial beliefs. The “What Do You Believe” exercise involves simply making a list of the “beliefs” clients hold about money. For instance, “there will never be enough money,” or “money is evil,” or “it is unsafe/improper to discuss money.” Once the list has been made, the advisor and the client can walk through each of the beliefs, and discuss in what instances those beliefs hold true, when they may be false, and how they may be otherwise impacting the client’s financial situation and progress towards goals.

The virtue of the “What Do You Believe” exercise is that, as mentioned earlier, what we learn from our family and the world around us often matters to our relationship with money. However, it is not very often that we actually take the time to stop, think, and consider what these messages are and/or how useful or not useful they are in our everyday lives. Going through this exercise, even for myself, was transformative. I uncovered things about my own money beliefs and their origins that profoundly changed the way I view my money today – and it is a different perspective from the one I held before when I had never taken the time to consider what the message was, where it came from, and then ultimately ask myself – is this even true, and/or is the belief still useful or relevant in my life today?

A common example when working with clients is the belief that there will never be enough money. This could stem from the experience of witnessing money struggles in the family while growing up. Or it could come from a money message passed down to your client that was told to them over and over again (e.g., the parents who earned raises and promotions but always upgraded their lifestyle and continue to live paycheck-to-paycheck under financial stress). Regardless of its origin though, such beliefs almost inevitably manifest in the way the client handles or thinks about their money today. In some instances, this may just look like stress toward money and overanxious calls and fear about their money running out (even if you know they have more money than they will ever need!). In more extreme situations, such problematic money scarcity beliefs can lead to hoarding or "excessive" frugality and an inability of the client to enjoy the money and resources they have.

(Meghaan’s Note: Hoarding or excess frugality from having grown up watching money struggles are negative examples. However, there are lots of positive examples too. Financial Therapy does not have to mean you are only going to talk about all of the bad stuff – in my own life and with my own clients, this is often a very positive, uplifting, funny, and enlightening exercise of exploring where good money habits and beliefs came from, too. Such as the person who has achieved financial success early and can attribute the success to lessons about money and financial responsibility instilled in them at a young age through receiving an allowance and opening a first bank account.)

As a financial advisor, you should not, and likely do not even want to, help a client through handling a bona fide hoarding problem. This is a clinically diagnosable mental disorder (in the extreme version), and I myself with Master’s in Psychology and two different certifications in financial therapy would not attempt to take this on. I am not a licensed mental health professional – I’m closer to a massage therapist than a mental health therapist – and in this situation, I would give the client a referral to a mental health professional… and you can (and should), too.

The key point, though, is that you can, as a financial advisor, learn about your clients’ money beliefs, discuss these beliefs, and even give your clients the opportunity to become enlightened of their own beliefs, while reminding your client that their belief may be valid in some instances but problematic in others. Essentially, such financial therapy tools give you the ability to better understand your client and their background at a different level, that will help you respond to their needs and fears in a more powerful way. At a minimum, the conversations can help to normalize the fact that money is a strange, uncomfortable, awkward, and an emotionally charged topic for nearly everyone.

On the other hand, it is worth at least mentioning that there are financial planning firms out there that have a financial therapist in house. As stated before, the dually-licensed financial therapist likely won’t be managing the money of the same client they work with on emotional issues. Yet, having him or her on hand to work alongside the financial planner (who is managing the money) in a collaborative meeting can become a natural, normal extension of your financial planning office, and a wonderful addition to your offering for clients (and in the more extreme cases would make an external referral to a mental health professional pretty simple).

Cautions and Caveats of Financial Planners Doing Financial Therapy

Financial therapy is exciting and interesting, and if you decide to go down the education path of financial therapy, you will likely experience your own personal epiphanies and realizations about your own money story, emotions, and behaviors… that you will likely be dying to share and want to encourage others to do or experience as well!

However, there are a few cautions or caveats to be aware of as you begin the journey.

First, once you start taking classes, reading books, and exploring the new tools of financial therapy, you will also likely feel motivated to try it. But it is, I can report from first-hand experience, harder than it looks or sounds! Something as simple as listening intently and effectively repeating back to clients what they have told you takes a lot of practice. As such, remember that practice makes perfect. Don’t be frustrated with yourself or clients – think of how many hours you have spent honing your skills as a financial advisor. It is the same when learning and using financial therapy skills.

Second, not every client will want financial therapy (or be open to engaging in financial therapy conversations). My own father is a great example; as much as he believes in therapy, and thinks what I do and what I study is interesting, he does not want it “done to” him. Be sensitive and in tune with what your client is asking of the process with you – not everyone is going to want to “be on the couch” or discuss their beliefs and related emotions, so do not try to make them if they don’t want to go there.

Third and final; know your own limits. As mentioned throughout this blog, there will be issues – technically diagnosable as a mental health concern or not – that you may not feel comfortable working through with your client. This is 100% okay, and says a lot about you, in a good way, when and if you recognize and acknowledge these areas and limitations for yourself. Knowing your thresholds, and which issues are beyond your scope of service, is good for you and the client. You can always provide a referral to a full-time financial therapist or mental health professional if it truly becomes necessary – in the same way you might suggest a CPA or an estate planner when the work with the client goes beyond your scope or capabilities.

In fact, financial therapy has a “Do No Harm” promise that is nearly synonymous with “fiduciary” promise for financial planners, and comes down to the same simple concepts: only do what you have been trained to do, and if you feel uncomfortable, stop. Working within your scope of practice, and knowing when to ask for help, will avoid nearly all potential ethical and practice limitations.

Next Steps To Exploring Financial Therapy Further

There are many ways to learn more and become involved with financial therapy for financial advisors who want to delve deeper. In fact, as the current President of the Financial Therapy Association, I can confidently say – we like you. We want to talk to you. We want to share our research with you. And we want you to be a part of our community because we think what you do as a financial planner is incredibly important work. Our work would arguably not exist or be as powerful without your work!

As a starting point for those financial planners who want to explore further:

- Attend an FTA Webinar: The Financial Therapy Association provides a webinar on the first Friday of each month. These webinars are focused on financial therapy topics, tools, and practices. Many of the webinars provide continuing education credit, and will certainly enhance the way you work with clients.

- Meet a Financial Therapist or a Licensed Mental Health Practitioner: There are websites to find a Financial Therapist in your area, and there are similar ones for finding a licensed mental health practitioner as well. Give a local financial therapist a call, meet up, and get to know them. You might even decide to put yourself through their process to experience it directly. It never hurts to learn more about yourself and money, let alone start to build a relationship with a person who could become a trusted referral source or collaborator with clients.

- Become More Educated on Financial Therapy Techniques: There are two great programs currently available where you can actually take classes on financial therapy, or do some self-study and begin to expand your knowledge base into tools that you can one day use in your own financial planning practice.

- Kansas State University: An academic, Masters level certificate.

- CFT-I(TM) Certification: A professional credential

- Join FTA: The Financial Therapy Association is a growing and exciting new industry association. By joining, you can meet many other financial practitioners, but also therapists, psychologists, academics, and students that all care about the same thing – money and our relationship with it.

- Register for the May 2019 FTA Conference (co-located with NAPFA National): Attending a Financial Therapy conference is certainly a great way to learn more, but it can be much more than that depending on your level of interest and time. For instance, the upcoming conference in Austin, TX on May 11th-13th will be done in collaboration with NAPFA. FTA will be providing many of NAPFA’s pre-conference sessions, so come early to FTA and attend NAPFA National as well, where you can not only learn about research and develop your skills, but get further involved. And the FTA conference is filled with mental health practitioners, students, pure academics, and financial practitioners from every walk of life: coaches, debt counselors, and behavioral economists. So you’ll have a lot of new networking opportunities!

- Get involved with research: Financial Therapy offers perhaps the best platform for financial advisors and researchers to come together to do more, helpful work as it pertains to the actual financial advisor-client relationship.

- As a member of the Financial Therapy Association, you will receive a copy of each issue of the Journal of Financial Therapy sent directly to your email!

- Meet and work with researchers by contacting the Financial Therapy Association directly ([email protected]), or plan to meet some financial therapy researchers in person at an upcoming conference.

In my work as a financial planning consultant, it is pretty common for me to receive somewhat distressing phone calls about how advisors want to be able to help clients that won’t help themselves and are asking, “what more can I do?” Financial advisors want to help, they want to be great mentors, confidants, and guides for their clients, but what to do and how to do it – to get clients to actually make changes and implement the advice – has not always been so clear.

But the world of Financial Therapy explores what it does take to get clients to better implement a financial planner’s advice, what the common blocking points are, and how to overcome them in working with clients. Great research already exists on the value of these collaborations, tools, and techniques in financial planning settings, and the training is now emerging for financial planners to learn them directly, for the betterment of themselves and their clients!

Leave a Reply