Executive Summary

Using an S corporation to reduce self-employment taxes – by splitting the income into a “reasonable compensation” salary and S corp dividends – is a popular strategy that financial advisors recommend to clients in a wide range of businesses. And in point of fact, it’s actually a viable strategy for financial advisors to use for their own advisory firms.

However, the recent Tax Court case of Fleischer v. Commissioner (TC Memo 2016-238) serves as a reminder that while advisory fees can be paid to an S corporation and partially passed through as a dividend to reduce taxation, the strategy does not work for insurance and investment commissions. In Fleischer’s case, the Tax Court invalidated his efforts to assign and transfer both his LPL investment commissions and MassMutual insurance commissions into his S corporation, finding instead that he should have claimed them as personal income on his Schedule C (and paid self-employment taxes on all of it).

The fundamental challenge is that, in order for a corporation to legitimately claim income, it has to actually control the contractual engagement to earn in the income. Which in the case of insurance and investment commissions, is generally impossible, because securities and state insurance laws require that commissions be paid directly to the individual. The only way an entity can legitimately receive the income is if the entity itself is registered as a broker-dealer or an insurance agency (and then contracts directly for the commission income), which alas may be common for an RIA but is usually not feasible for a broker-dealer or insurance agency due to regulatory and compliance costs.

Nonetheless, as the Fleischer case indicates, the fact that establishing a bona fide broker-dealer or insurance agency isn’t economically feasible in most cases doesn’t change the underlying requirement of the tax law – which is that if an individual earns income personally (including investment or insurance/annuity commissions), that person must report the income for tax purposes, and can’t simply transfer it into a business account and issue a 1099-MISC to the S corporation and expect it to be honored by the IRS!

Requirements For Securities And Insurance Commission Payments

It is a fundamental requirement that for an individual to receive a commission for the sale of a securities product, he/she must actually be registered as a representative of a broker-dealer. And to ensure that this rule is honored, FINRA Rule 2040 states that no payment of compensation may be made to an entity at all, unless the entity itself is registered as a broker-dealer as well.

Similarly, most states also limit the payment of insurance commissions to either individuals licensed as an insurance agent, or entities that are properly registered as an insurance agency or insurance brokerage firm. Splitting insurance commissions to/with non-licensed entities is generally forbidden as well.

The ultimate purpose of these rules is to prevent individuals from circumventing registration rules by trying to route their (securities or insurance) commissions through non-registered entities. Instead, commissions must be paid directly to (registered/licensed) individuals, and the only entities that can be registered must honor the compliance requirements that apply to those types of (broker-dealer or insurance agency/broker) entities. Thus, non-licensed individuals have no path, directly or indirectly via an entity, to get paid commissions they shouldn’t be entitled to as non-registered persons.

The caveat, however, is that always receiving payments individually is not always ideal from a tax planning perspective. Because income that is paid directly to an independent broker or insurance/annuity agent will have to be fully reported as self-employment income (net of any expenses) for tax purposes. Whereas if the income was paid to an entity – in particular, an S corporation – it would potentially be possible to pay a portion of the income out as S corp dividends, not subject to self-employment taxes.

But as a recent Tax Court case illustrates, the fact that commission income must be payable to an individual also means it must be reported by that individual for income tax purposes; as desirable as it may be, it’s not permissible for brokers or insurance agents to try to “reassign” commission income to an S corporation, just to avoid or minimize self-employment taxes!

The Tax Court Case Of LPL Broker Fleischer v. Commissioner (TC Memo 2016-238)

In the recent case of Fleischer v. Commissioner, TC Memo 2016-238, Ryan Fleischer was a Series-licensed independent broker with LPL (structured as an independent contractor), and also an insurance agent with MassMutual for fixed insurance contracts (again as an independent agent).

In addition to being individually licensed as a broker and agent, Fleischer also had an S corporation, called Fleischer Wealth Plan (FWP), for which Fleischer was the sole shareholder and officer, and with which he had an “employment agreement” to perform duties as a financial advisor.

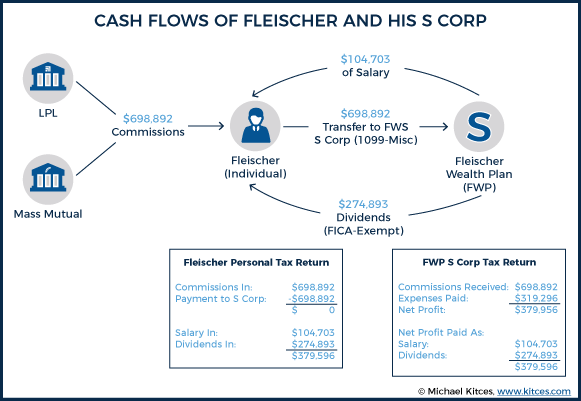

In 2009, Fleischer received a total of $147,617 of commissions from LPL and MassMutual, which he reported as income for his S corporation. The business netted $46,775 after expenses that year, of which Fleischer then paid himself $34,851 as salary, and took $11,924 as a dividend not subject to self-employment tax. None of his $147,617 of income was reported on his personal Schedule C.

In 2010, Fleischer received $284,963 of insurance and brokerage commissions. He claimed all $284,963 as an “expense” on his Schedule C – netting out to zero – and that even though they’d originally been paid to him, the commissions were all income of FWP, his S corporation. Overall that year, FWP generated $289,201 of total revenue, the business netted $182,498 after expenses, and Fleischer then paid himself another $34,856 as salary, taking the remaining $147,642 as a not-employment-taxed dividend.

In 2011, the process repeated. Fleischer received another $266,292 of combined LPL and MassMutual commissions, and again claimed a matching $266,292 of “expenses” for a net profit of $0 on his Schedule C. The commissions (of $266,292) were again reported as gross revenue to the S corporation, from which then paid Fleischer $34,996 of salary, and $115,327 of pass-through dividends, after deducting his (valid) business expenses.

Across all three years, Fleischer showed a net Schedule C income of $0, while the S corporation’s net profits (after Fleischer’s salary) were reported on a Form K-1 as pass-through income and claimed on Schedule E of Fleischer’s personal tax return instead. Cumulatively, Fleischer took $104,703 of salary (subject to payroll taxes), and $274,893 of pass-through dividends not subject to employment taxes.

Unfortunately, though, the IRS caught wind of the situation – ostensibly through a random audit – and upon evaluating the situation, noted that since all the commissions were paid to Fleischer directly (and not the S corporation) that the income should have all be reported directly by Fleischer (on his Schedule C) and not via the S corporation and its pass-through to Schedule E.

The key difference – if the income had been (properly) reported on Schedule C, all the income would have been subject to self-employment taxes. By contrast, with the S corp structure, there was $274,893 of (pass-through dividend) income never subject to payroll/self-employment taxes. Accordingly, IRS issued a deficiency notice that Fleischer owed $41,563 of self-employment taxes across all three years.

Limitations On Shifting Personal Commissions To A Related S Corporation

The key issue in the Fleischer case is that, under long-standing principles of taxation, income is taxed to the person who earned it. This rule avoids people simply shifting and ‘assigning’ income at will, which could otherwise be used for substantial tax avoidance, particularly in our current world of progressive tax rates. For instance, if income could be shifted so easily, those in high tax brackets could just distribute income across multiple family members in lower tax brackets to reduce their tax bill, or even just create a series of corporations and split the income evenly across as many entities are necessary to keep them all within the bottom (corporate) tax bracket.

Notably, determining who “earned” the income can be more complex in situations where there’s a corporation and an employee who does the “work” that generates the income. In the logical extreme, income could never be taxed to a corporation, because it’s always the human being employed by the corporation that is actually doing the work to “earn” the income.

To distinguish when an individual earns money in his/her personal capacity instead of merely as the employee of a business, the tax code looks to who controls the earning of the income. Thus, in a standard corporation-employee scenario, the employee may do the work, but the corporation has the contractual agreement with the client and ultimately controls whether the contract will be fulfilled and controls how services will be rendered. Which means the income would be taxed to the corporation (even though the employee “did the work”).

Specifically, under existing case law and Treasury Regulation 31.3121(d)-1(c)(2), to claim that the corporation is the controller of the income, “the individual providing the services must be an employee of the corporation whom the corporation can direct and control in a meaningful sense”, and “there must exist between the corporation and the person or entity using the services a contract or similar indicium recognizing the corporation’s controlling position”.

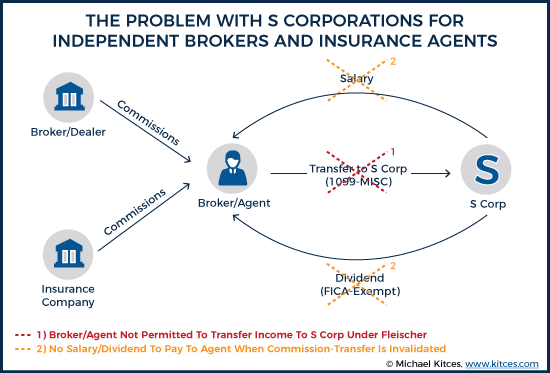

Except the problem in the case of Fleischer – or any independent B/D or insurance/annuity agent – is that there is no contract between the corporation and the person paying for the services (in this case, the B/D or insurance company for whom the broker/agent is a representative), because the actual engagement is between the broker-dealer (or insurance company) and the individual broker/agent who is (individually) licensed to do the work as a registered representative or insurance agent. The broker’s S corporation is not a party to the engagement with the insurance company or broker-dealer (much less a controlling one!).

In other words, if Fleischer’s S corporation was contracted directly with LPL or MassMutual, such that the S corporation was going to be the insurance agent or registered representative (and Fleischer himself was merely an employee), it might have been permissible for the S corporation to claim the income. A similar 1991 Tax Court case – Sargent v. Commissioner – was decided this way, where two hockey players formed an S corporation that established player contracts directly with the hockey team, and the team then paid income directly to the S corporation (which in turn remitted salaries to the hockey players as employees).

Unfortunately, though, given the licensing requirements applicable to broker-dealers (and their registered representatives) or for insurance agencies (and their insurance agents), for LPL and MassMutual to have paid Fleischer’s S corporation FWP directly (rather than Fleischer himself), Fleischer would have had to form a broker-dealer entity (and/or insurance agency), with all the costs, capital requirements, and compliance obligations that go along with it. Which Fleischer himself noted wasn’t very feasible.

Nonetheless, the conclusion of the Tax Court was straightforward: if FWP wasn’t directly a party to the commission agreements with LPL and MassMutual, it couldn’t claim the commission income. Instead, Fleischer was the licensed broker and agent, and thus should have claimed the income directly. And as a result, he was found liable for the $41,563 of unpaid self-employment taxes as calculated by the IRS.

Are Brokers And Insurance Agents Running Afoul Of The Fleischer Case Now?

Notwithstanding the Tax Court’s very straightforward conclusion that an S corporation shouldn’t claim investment or insurance commissions as income if that income isn’t actually paid to the S corp in the first place, the Fleischer strategy appears to be engaged in frequently amongst many independent brokers and insurance agents.

The standard scenario, akin to Fleischer, is that the individual broker/agent receives commissions directly, and then immediately moves those dollars into the S corporation’s bank account, claiming a deduction (and likely issuing a 1099-MISC) for all the money transferred to the S corp, for which the S corporation subsequently splits the net profit payments back to the advisor as part salary, and part dividend. And the broker/agent saves tax dollars to the extent of the self-employment taxes not due on the dividend portion of the income.

Except the case of Fleischer v. Commissioner makes it clear that this is not permitted! Again, if the S corp isn’t contractually engaged with the broker-dealer or insurance company to receive the securities or insurance commissions directly, it cannot claim them as income. The mere fact that the advisor may be transferring the money to the corporate account, issuing a 1099-MISC to the S corporation, and claiming a deduction, doesn’t make it legitimate or binding, when there’s no actual legal basis for transferring the income in the first place. In the Fleischer case, it wasn’t a matter of whether Fleischer “properly” transferred the income or properly reported it; the conclusion of the court was that the income should have all been on his personal Schedule C. Period.

Practical Implications Of The Fleischer Case

Unfortunately, the outcome of the Fleischer case may be bad news to a lot of independent brokers and insurance agents, currently engaged in a similar strategy using an S corporation to reduce their self-employment taxes!

Of course, the reality is that the Fleischer case didn’t actually cause a change in the tax rules; instead, it merely reiterated existing laws as they stand. But it does reaffirm that brokers and insurance agents transferring commissions to their S corporation (to shift the income for tax purposes) is not permitted. And the fact that the IRS caught Fleischer in the act, and defended it all the way to Tax Court, suggests that the IRS now has the issue more squarely on their radar screen and is ready to pursue it.

Notably, the challenge for advisors shifting compensation to an S corporation is unique to those working under a broker-dealer or insurance agency, but not those who own an independent RIA. Because in the case of an RIA, it really is possible to register the S corporation entity directly as a Registered Investment Adviser (at a drastically lower cost than what it takes to establish a broker-dealer). And once the RIA is registered, clients can engage the firm directly and pay fees directly to the RIA, which in turn can pay a salary to the advisor/owner (who ideally should have a formal employment agreement in place to substantiate the arrangement as an IAR of the RIA), and then pass through the remaining income as a (not-self-employment-taxed) dividend. Notably, it’s still necessary for the advisor to be paid “reasonable compensation” salary.

The Fleischer scenario is also a moot point for brokers who operate under an employee model and are treated as wage employees of the broker-dealer (or insurance company). Because in that case, the broker-dealer itself is already paying FICA payroll taxes as a part of the W-2 wages to the broker, and there is no self-employment tax obligation (nor any role for an external S corporation in the first place).

But in the case of those working for an independent broker-dealer (or as independent insurance or annuity agents), the challenge remains that commissions can only be paid directly to an individual, unless the S corp entity itself is established as a broker-dealer or insurance agency, which alas usually just isn’t economically feasible.

It’s important to recognize, though, that the Fleischer case doesn’t necessarily mean no dollars could ever be legitimately paid to a related S corp. For instance, in a situation where the S corp actually has other staff employees, the employees could be employed by the S corp, and the advisor could pay the S corp for those support staff services. Of course, that doesn’t necessarily generate any employment tax savings, since that staff compensation would have been deductible anyway. But it might be appealing for some partial liability protection purposes, and avoids what would otherwise be a problematic scenario where the S corporation has all the (employee) expenses but no income, producing not-currently-deductible “business” losses that couldn’t be netted against Schedule C income. And in some cases, there might at least be indirect tax savings, such as in a situation where the advisor lives in a higher-tax state while the S corp is in a lower tax state (that doesn’t have a special gross receipts tax on S corps).

Example 1. Jeremy generates $450,000 of gross commissions, and has three support staff members to which he pays a total of $200,000 of salary and related employee benefits. While Jeremy is directly licensed with his broker-dealer, his employees are all employed by his related advisory firm S corporation. On his personal tax return, Jeremy claims a $200,000 business expense for “Advisor Support Services” to his related S corporation, which then uses the $200,000 of “income” to pay the employees. The end result is that Jeremy’s Schedule C shows $450,000 of gross income and $250,000 of net income (after the expenses paid to the S corporation), and the S corporation shows $200,000 of gross revenue and $200,000 of expenses for net income of $0.

Notably, the end result of this example is not any improvement in Jeremy’s personal tax situation – as he could have paid the employees directly and deducted the $200,000 of staff expenses on his Schedule C for the same net income. But if he wants an S corporation in place – perhaps because it generates other income that can be paid to the S corporation, and he wants to group it all together – the $200,000 should be recognized, because he’s not merely “transferring” income, but actually paying for bona fide services (albeit to a related business he owns).

In point of fact, it’s also fair to recognize that if a third-party S corp “service” business were working with the advisor, it might charge a reasonable markup to generate a profit as well. After all, if the broker had to hire a third-party outsourcing solution, it could reasonably charge a markup to actually make a profit over its staff costs, not merely price them as a pass-through. Which means it may be possible to at least slightly shift some additional amount of income to the S corporation (and reduce self-employment taxes).

Example 2. Continuing the prior example, Jeremy might recognize that if he had to hire a third-party outsourcing firm on the open market, it would reasonably have charged $230,000 for his “service contract”, allowing for a 15% profit margin on the engagement. Accordingly, Jeremy agrees to pay (his related business) $230,000 for his “advisor support services”. This reduces his Schedule C income to just $220,000, and creates a $30,000 profit for the S corporation (since it is “paid” $230,000 but only has $200,000 of actual employee expenses).

In this case, Jeremy’s total income is still $220,000 + $30,000 = $250,000 (the same as an Example 1), but the $30,000 of S corp profits could be taken as a pass-through dividend, which means the $30,000 is still taxed as ordinary income but not subject to self-employment taxes. Given Jeremy’s income (and that he’s above the Social Security wage base), this would produce a moderate $30,000 x 2.9% = $870 of self-employment tax savings.

The fundamental point remains, though, that paying a portion of a broker’s (or insurance agent’s) income to an S corporation for services (even if it’s a related S corp he/she owns) is one thing, but simply transferring/assigning income from yourself to your S corporation is another. Because even if you take back what would have otherwise been a “reasonable compensation” salary for your work under the S corp, it doesn’t matter, because the S corp wasn’t contracted and engaged to earn the income in the first place.

Given the popularity of this strategy in recent years, brokers and insurance/annuity agents who have been engaging in it anyway, and may have been running afoul of this issue in the exact manner that Fleischer did, may want to contact their accountants to consider whether/how to rectify the situation (potentially retroactively, as well as going forward). Especially since, as the Fleischer case notes, this is an issue that appears to now be on the IRS’ radar screen!

So what do you think? Does the Fleischer ruling impact you? Do you have any clients with S corps that may be similarly impacted due to licensing within their industry? Do you think it's still worth using S corps for other reasons? Please share your thoughts in the comments below!

Sadly, we have one extremely convoluted tax system. Scenarios like those you’ve presented here are common among those I know in the industry. Even more sadly, I know many accountants that routinely recommend this to their clients.

Practically speaking though, let’s look at a scenario where an independent insurance agent generates $200k of gross commissions in a year. In your scenario, you mentioned the agent actually paying his S corp for advisor support services. Couldn’t one of those services also be “lead generation” and/or “marketing”? This would be an activity done by the agent as an employee of the corporation. If it’s an activity that doesn’t require a license, the corp can do it, and it can pay the agent as an employee, right? I can think of many things that would fit this criteria. Certainly enough to likely wash all of the $200k in commissions against.

At larger numbers, this may not be practical, but then again, maybe it could be.

I’m not sure how you’d substantiate that “the S Corp” did the marketing and lead generation, when it’s still the actual broker/insurance agent physically doing the marketing and lead generation, meeting with clients, etc.

You raise an interesting theory to this, but I’m just not sure how you substantiate the activity, ESPECIALLY if the only employee of the S corp IS the advisor (so clearly he/she was still actually DOING all the lead-gen and marketing).

The “advisor support services” angle works specifically because IT’S NOT THE ADVISOR DOING IT. It’s other employees. So if you had a full-time marketing person, could you hire them through the S corp and make an allocation of their salary off the commissions and over to the S corp? Perhaps. But I don’t know many advisors with $200k in gross commissions who have full time (or any) marketing staff…

– Michael

“I’m not sure how you’d substantiate that “the S Corp” did the marketing and lead generation, when it’s still the actual broker/insurance agent physically doing the marketing and lead generation, meeting with clients, etc.”

So, this is interesting. I guess I’d argue that it wasn’t the “actual broker/insurance agent” physically doing the marketing and lead generation, as no license is required for that activity. It was the owner of the corp, who, acting not in the capacity of a licensed broker/agent, generated leads. In other words, what hat am I wearing at any given time?

I can certainly hire a non-licensed business to generate leads for me (call center, internet-based leads, seminar marketing companies, etc.) But what you seem to be saying is that if I own the S corp that is in the “marketing business”, and in my role as an employee of said corp I generate leads, which the corp sells back to me as an individual, the controlling factor is that because I am licensed I can’t do this. What if the corp sold the leads to another licensed agent/broker? What if that other agent/broker “gave up” on those leads and gave them to me as a licensed agent/broker?

What you describe is possible and we’ve done it for clients, but Michael is correct that it may look a bit suspect for a business doing $200k in revenue. But, still technically possible – setting up a company where you wear one “hat” and per the terms of a very clearly laid out employment arrangement perform duties on behalf of the company that is unrelated to the activities you do as an advisors, then pay the company for said services. It gets a little complicated from a succession planning perspective, but it is an effective strategy we’ve used to help an advisor provide a legitimate reason for getting their personal production into the entity so you can then run the business there.

Michael lays out a good example towards the end of the article as a possible solution. There are ways to get this done, it is complicated and simple all at the same time. There is a long checklist of things to do that we advise every advisor’s CPA on when helping setup this structure up. The issue in this case, and others like it, is that money was moved into the s-corp so he could pay less in taxes…Kitces does a good job of laying out how that was designed to happen in this case and why this was obviously an issue for the IRS.

Fateful timing of this post for me; I’m currently in the process of setting up a structure which hopefully avoids running afoul of this bad fact pattern case. My CPA was aware of this case as we began our strategy.

I am an independent insurance agent and have recently joined an RIA in 2016. I’ve created an LLC, taxed as an S-Corp, and am licensing that LLC as an insurance agency in the states where I do business. I am redoing contracting with individual insurance companies to pay commissions directly to the now-licensed LLC; my RIA is already paying advisory fees to the LLC. New commissions generated will be paid directly to the business account of the LLC and distributed to me via payroll & distributions.

Anything that continues to pay in to my personal accounts I will be reporting on my Sch C (not going to move it over as in the Fleischer case), but the idea is to get that down to a level where its composed solely of renewal commissions from old insurance contracts which cannot be moved to the LLC. My “reasonable” salary will be approximately $125,000 per year and distributions will run another $100k or so, with another $150-200k reported on my Sch C for 2017. I have one administrative assistant who is on payroll in the LLC as well.

Thoughts anyone?

If the appointments with the insurance company are to your LLC agency entity directly and not to you personally, this seems reasonable. The challenge in the Fleischer case was that it’s FAR more challenging to set up your own broker-dealer than your own insurance agency, so he didn’t set one up at all. If your agency is contracted and commissions are truly paid directly to the agency as contracted in the first place, you would seem to be in the clear of the facts in the Fleischer case. (Though as you note, old trails payable to you would still need to go to you.)

– Michael

All this, good stuff. Thanks!

I think the key with “reasonable salary” is getting your CPA to agree. After all, during the audit you don’t want her saying “I told you to take a higher salary…” Personally I set my salary such that it lets me max out retirement plan (SEP) contributions.

Michael Kitces’ article is a GREAT summary of the case, but just restates the problem and misses all the small nuances that tax court provided (and has provided before) regarding major steps that Ryan should have taken that he didn’t. There ARE strategies to using company as an advisor that have passed an IRS audit. Will you ever be “bullet proof” with the IRS? No. But don’t take this article at face value and think there is no way to accomplish this. It can be done, and has been done MANY times correctly by your peers. Talk to an accountant and consultant that knows how independent reps like Ryan could have put themselves in a defensible position with their s-corp/LLC – you’ll find like we have, it IS possible, just not the way it was done in this case.

The question becomes (and for me, remains), how do we find a tax professional who knows the right way to do this? Looks like Ryan got the wrong advice. Any suggestions, please share.

We can happily assist you with this. We have defined processes/strategies and the necessary form agreements all built to make this turnkey for you. Once we have it all setup for you, we will coordinate with your CPA so they understand the what/why before they have to file your taxes for all this! We do this a lot for advisors, and have helped a lot more recently “tune up” their structures given the publicity that Mr. Fleischer’s case received. If you’d like to schedule a time to chat, here is the link to my calendar so we can find a convenient time: http://bit.ly/davidgrau

The court mentioned something on page 5 of the decision and it sticks with me. Fleischer never contracted with his own firm (FWP) a requirement that he was to pay over his industry related earnings as a condition of employment. I know a large portion of your piece here is dedicated to the idea that income can’t simply be “reassigned” but I do find it interesting that the lack of this contractual stipulation was even mentioned in the decision.

I think there are two things Fleischer could have done that may have created a different result. 1.) the employment contract stipulation discussed above. 2.) provide evidence that he asked LPL and Mass to pay his earnings directly to his S-Corp – ie. a written refusal to pay his S-Corp directly. This too was mentioned in the decision as something to the effect that LPL didn’t know his S-Corp even existed.

If I’m a one-man-band graphic designer and I get W9d by a client, I put my S-Corp down and the client 1099s my S-Corp. However, if I’m a one-man-band RR / IAR and I get W9d by my affiliate BD / RIA, I put my S-Corp down and they say “sorry, no,” forcing me to list myself on the W9. In the latter, I attempted to put my S-Corp in control of the income but was prevented from doing so by no fault of my or the S-Corp’s own. I think the intent, and the ways that it can be proven, are important here. Even more so if the S-Corp in question is the DBA through which services are marketed.

The contractual agreements are binding, not just the intent. Otherwise, I could shift all my income to my kids by just telling the company “contract with my kids” and when they say “no, we don’t do business with 5-year-olds” I’d say “well, my INTENT was to pay my kids, the company refused!”

The tax law looks to the actual substance of the contract. If the person you’re trying to shift the income to doesn’t have a contract/agreement because he/she CAN’T, the outcome is still the same: there’s no contract/agreement to that person.

Fleischer tried to defend himself by saying that the cost to make his business contracted directly – forming his own broker-dealer – would have been cost prohibitive. He is correct in that regard. But it doesn’t change the outcome, which is that his entity wasn’t contracted directly, regardless of his intent/desire to do so. :/

– Michael

Hyperbole aside, you’re describing a sub-contractor situation. In that instance you would contract with the client and then contract the “5-year-old” to do the work the client needs done. Client pays you, you pay the “5-year-old.” So…

In the context of Fleischer’s employment contract with his S-Corp, the court said: “The agreement does not include a provision requiring petitioner to remit any commissions or fees from LPL or any other third party to FWP.”

For what reason would the court mention this in its decision? As you say “the contractual agreements are binding.” The court seems to indicate that if such a contract provision existed it might have mattered. I also don’t believe we can conclusively say that such a provision would lack substance simply because it was between an S-Corp and its owner/employee.

The court noted TWO requirements. ONE is that the corporation has to have control of the income-earning relationship. The SECOND is that there needs to be an employment agreement.

Having the latter in the absence of the former still fails the test. It’s completely irrelevant whether Fleischer had an employment agreement with FWP, when FWP wasn’t contracted to receive the commissions in the first place. It still fails the first part of the test.

– Michael

Thanks, Michael.

Couple of ways I have seen this dealt with. The strategy of Ryan contracting with his company to perform certain services for him is a great idea that Kitces highlights. I have also seen situations where the advisor signs an employment agreement with his/her company, then the company can at least show that the advisor/employee was simply acting on its behalf when performing all functions of his job (as outlined in the employment agreement), and the company is therefore entitled to all revenue earned (the requirement to pay such money to the company is also in the agreement, which Ryan did not have).

I think the advisor “tempted fate” a little too much with his allocation of income. “Fleischer then paid himself another $34,856 as salary, taking the remaining $147,642 as a not-employment-taxed dividend”. $35,000 of salary when you are generating $200,000+ of income seems really hard to justify and has been on the IRS’s list for a long time.

Jeff,

Ultimately, Fleischer didn’t lose on the basis of reasonable comp. He lost because the S corp wasn’t entitled to ANY of the income at all. Technically, he could have paid himself 95% as salary and 5% as a dividend, and have had “reasonable” comp, and it still would have been invalidated.

That being said, the size of the FICA tax savings he had by ALSO not paying himself reasonable comp may well have been what put him on the IRS’ radar screen in the first place. In other words, it’s not the issue he ultimately lost on, but it may well be what got him pulled over in the first place. :/

– Michael

I think Jeff’s point is a sound one. That is likely part of what got him audited in the first place.

But Kitces seems to be correct in his statement, even IF he was paying 95% of the revenue back to himself as a salary, it would still have been invalidated because he didn’t have his agreements in order for paying the revenue to the entity in the first place…

No doubt this was likely the cause of his getting audited. I find it interesting that the “reasonable compensation question” is flipped upside down when dealing with C corps. I’ve been on both sides of this in my life, and it further speaks to how messy (and arbitrary) our tax system can be.

Agreed, that definitely did not help him. The point of using the corporation shouldn’t just be to save money on taxes…done more conservatively, he might have saved a little in taxes, but you would use an entity for a host of other reasons. Ryan should also have had very specific duties prescribed in his employment agreement, which the IRS Court filing indicated he did not, and that he should have had some kind of contractual requirement between himself and his company requiring that some/all of his personal production to be paid to the company.

The RIA I work for 1099s advisors their advisory fees. Can I start an S-corp and have the RIA I work for pay by advisory fees to it?

I second this question. If the RIA I am a 1099 of is willing to pay an LLC/ S-Corp I create AND issue 1099s to that LLC/S-Corp, does it become valid? Does the LLC/S-corp that I create also need to be registered in anyway?

Complicated set of questions, but I’ll give you our perspective at Succession Resource Group having worked with advisors in similar situations – if you are operating under a corporate RIA and paid on a 1099 as the IAR of said RIA, we have had advisors we’ve help setup their own entity that you then run your revenue through – we just need to make sure there is a contract in place that documents why the revenue is being paid from you to the company, and it can’t just be assigning the income as was highlighted in the Fleischer case. But doable.

So, a few questions:

1. Regarding RIAs, does this mean that the rules/laws subjecting a registered representative/independent advisor to personal liability go away when the RIA uses a corporation for various purposes including being sheltered from personal liability?

2. I have heard of broker dealer advisors being able to shift income to corporations for these purposes. Is there an approach to this that is acceptedable? My guess is no, given the great lengths Michael said no wa in the article. But so many advisors have worked with so many of their CPAs on this type of approach, that I have to ask the question.

3. Did the IRS find anything else out of sorts with Fleischer’s taxes, ex. inappropriate deductions or missed income?

1. You should consult your attorney on questions of liability, but from those I’ve spoken to, the answer has been yes. In an RIA, where the client signs a contract with your corporation (for example) you should in theory reduce personal liability.

2. Independent advisors under a BD have been able to shift there income to the corporation, but there are a number of steps to make sure you do this correctly. And when done right, you won’t have a huge tax savings…that isn’t the point. There are a LOT of other benefits to having an entity structure.

3. If your accountant read over the IRS Tax Court documents for Mr. Fleischer, they would tell you the same thing we would – there are a number of things he should have been doing that he wasn’t.

Thanks for writing this article Michael! Great summary. There are some clear nuances that the IRS Tax Court identifies that we’ve seen be issues before. You have to read between the lines, but they are pretty clear on things he could/should have done differently. The trouble with this case is that advisors will read it and think they can’t use a corporation or LLC. There are ways to accomplish this, he just didn’t do it right. I would also say that if you are just looking to setup a company, so you can move money into it and back out and pay less taxes, you might as well setup a desk in your office for the IRS auditor, cause they will come knocking….

David, thanks for the additional insight. You are right … I read from the article “no way, Jose.” But maybe there is another article that outlines the process for this, and the people needed on the team.

I find the idea of going through all these motions to save a few bucks in taxes as irritating. But, I do find real value in asset protection. For someone with significant assets outside their advisory business and they are broker-dealer based, the question is … is there a way to create a structure to protect other assets from being subject to claim by an unreasonable client and unfavorable regulatory environment?

For additional commentary on this issue and explanation of solutions Succession Resource Group has been employing with advisors and their accountants, you can also read our recent article: http://www.successionresource.com/first-dol-now-irs-gunning-advisors/

What is the best tax deferred savings Plan for an S-Corp with employees? Seems like a Simple IRA is most flexible and has the lowest cost for the owner(s) but the IRS limit is low. SEP IRA has a much higher limit but only the owner(s) fund contributions.

Michael, thank you for the article! How does an advisor under a corporate RIA fit in this scenario? I am under a corporate RIA with an Independent BD and I am compensated with 95% AUM based fee revenue and 5% trails from old A Share business I inherited. The BD lumps everything together for each compensation cycle and will only send the compensation to the individual. I can generate a report that breaks down the commission vs fee revenue for the year but the paycheck will not separate it. I just want to clarify because the article mentions investment commissions, insurance commissions, or being an independent RIA but nothing about being under a corporate RIA.

Great question and a common arrangement for many of our advisor clients. The short answer is, whether its broker-dealer, insurance, or corporate RIA/advisory revenue – you are paid directly and begin down the path of figuring out how you can then run your business and limit personal liability (i.e., using a corp or LLC). Simply assigning your production (or nominating your income to the entity as the accountants refer to it) to the entity doesn’t work obviously, but as a business owner you should still have an entity to handle your operations, which means you will incur expenses in the entity (lease, administrative staff, software, server, phone system, etc.). We have had a lot of success with our client’s CPAs around the country helping develop a contractual relationship between you as the producer and the entity as the service provider (much like if you bought a building and then signed a lease with yourself) which then gets the majority of your revenue into the entity – but it ends up there through a legitimate business arrangement. Hopefully that helps a little. Happy to talk about more specifics if you’d like.

This article was from a while ago, but what about hybrid advisors? Consider this scenerio:

-An advisor comes on board with a large RIA that uses a broker/dealer like LPL as its custodian.

-This advisor does fee business but also does insurance and commission products through LPL.

-LPL pays the RIA all of the advisor’s commissions through an override.

-The RIA takes their cut and then pays the advisor’s S-corp directly.

In this a scenario, can the advisor accomplish what Fleischer had hoped to?

came across this very useful and informative article.

I work from home, no employees, minimal corporate expense, have a s-corp but is paid on a 1099 on SSN

So far, assigned 1099 revenue to S-corp, paid myself a good salary, have a 401k plan set up from s-corp and s-corp provides max profit sharing based on salary.

Now it seems that this is no longer feasible/advisable.

Not sure if even David can find an agreement that will assist in assigning 1099 revenue to s-corp in this case, lol

In my opinion the point would be, if you are paying all your self-employment taxes, whether it is through an LLC or an S Corporation it does not matter. The IRS allows either model to deduct business

expenses. If you are paying rent, have employees, and other typical business expenses you are a

business and should be taking the deductions.

Fleisher was trying to game the system. The 2022 Cap for Federal taxes excluding Medicare is $147,000, so whether you are paying your taxes through payroll or monthly SE the amount of employment taxes would be the same.

Broker Dealer typically Commission the agent’s social security number, because they are holding their licenses as an individual. The agent list an OBI for the entity they have created with the Broker

Dealer.

Verbiage From FINRA website.

“Associated Persons” of a Broker-Dealer

We call individuals who work for a registered broker-dealer “associated persons.” This is the case whether such individuals are employees, independent contractors, or are otherwise working

with a broker-dealer.

The point would be moot if salary from S-corp is 147K but since most people take a lower salary and get distributions as well many times it’s 50-50, that makes it a gray area.