Executive Summary

Over the past year, the Financial Planning Association (FPA) has been no stranger to controversy. After years of declining revenues and membership levels and ongoing organizational struggles, the FPA rolled out its OneFPA Network initiative last November, which in effect would have nationalized its existing chapter system, centralizing all decision-making and budgetary control at the National level. Not surprisingly, given the FPA's history of chapter autonomy and a long-standing concern that the National organization is out of touch with its chapters, the OneFPA Network rollout met with a significant backlash from members and chapter leaders, forcing the FPA just a few months later to roll back most of its planned changes.

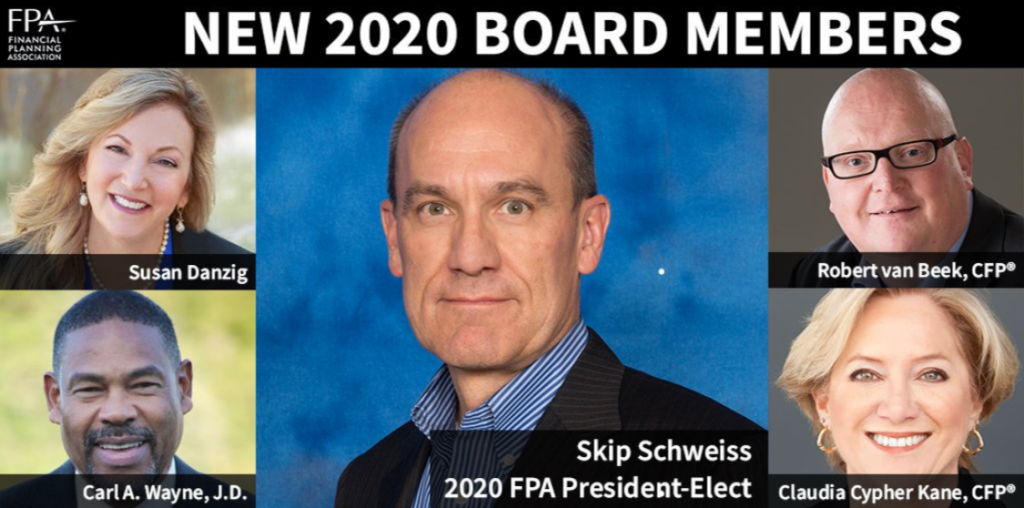

Yet even as the FPA National organization tries to smooth over its increasingly tense relationship with its chapters, this week as the FPA Annual Conference gets underway the organization dropped the bombshell announcement that its new and incoming President-Elect and future Chair will be Skip Schweiss of TD Ameritrade, who serves as Managing Director of TDA's Trust Company and its Retirement Plan Solutions platform for advisors. Which is significant because it means Skip Schweiss is not only not a financial planner himself (or from an advisory firm or organization that teaches financial planning, as every prior FPA president has been in the past), he will be the first-ever FPA Chair that doesn't actually hold the CFP marks (even as FPA promotes itself as the principal membership association of CFP professionals), and the first-ever FPA Chair who represents a vendor whose business is selling solutions to FPA members.

However, even more concerning is the fact that TD Ameritrade itself has been the FPA’s leading top-tier sponsor nearly every year for more than a decade, which means that, with its current "Cornerstone Partner" $200k annual sponsorship commitment, TD Ameritrade has cumulatively written upwards of $1 – 2 million in sponsorship checks over the past decade! And while it’s not necessarily a bad thing for the Board to have representation from vendors (since vendors that serve financial planners are themselves stakeholders in the FPA and the broader financial planning community), there’s a difference between having representation on the FPA board and having a non-CFP representative of a vendor (which is ‘coincidentally’ the FPA’s largest sponsor) be the President of the entire organization (that can influence, amongst other things, its policies with vendors that FPA relies upon for its financial viability).

And if that apparent conflict of interest weren’t enough, perhaps most problematic is the reality that TD Ameritrade has a history of lobbying on regulatory issues in a manner that directly opposes the FPA’s own advocacy for a uniform fiduciary standard for all investment advisers and broker-dealers providing financial advice. In fact, earlier this year, TD Ameritrade went so far as to threaten to discontinue offering services in the entire state of Nevada if the state imposed a uniform fiduciary duty on its brokers... a uniform fiduciary duty that the FPA directly supported along with the rest of the Financial Planning Coalition in its own public comment letter. Which means that, after spending a cool $1 to $2 million in FPA sponsorships over the past decade, TD Ameritrade now has one of its executives in a position to strongly influence the direction of FPA's advocacy efforts that have a history of conflicting with TD Ameritrade’s own business interests! If the future CEO of TD Ameritrade someday calls Skip Schweiss and asks him to dissuade FPA from advocacy for a fiduciary standard that harms TD Ameritrade's retail business interests, how exactly is Schweiss supposed to handle that conflict if his job is on the line?

Putting aside these deeply concerning conflicts of interest between FPA's board leadership and TD Ameritrade's executive representation, it's also notable that the FPA’s decision means, for the first time ever, the majority of its Executive Committee will consist of non-practitioners with no leadership experience within the FPA’s local chapter system. Just as the FPA National organization struggles in its chapter relations in the wake of the failed OneFPA Network rollout. And more broadly, of the newly elected slate of Board candidates, only two members even have CFP certification, one of whom is an international representative whose CFP marks are based in the Netherlands (and may not be valid here in the United States, which would actually mean the FPA no longer has sufficient representation of CFP professionals on its Board of Directors to meet its own Bylaws requirements!).

Perhaps the upcoming restructuring of the Nominating Committee, of which half will be comprised of FPA chapter leaders going forward, will provide a good first step towards unwinding some of the FPA’s recent missteps... except given that the FPA National Board has still retained the right to veto chapter leaders from the nominating committee, to veto nominees that chapter leaders select for the board, to substitute its own candidates and override the nominating committee anyway, while stacking the nominating committee with the President-Elect and President in all the meetings and the National Chair presiding over the nominating committee and casting its tiebreaker vote over chapter leaders... it's still not clear that the FPA is even serious yet about really adopting a more "participatory governance" structure in the future?

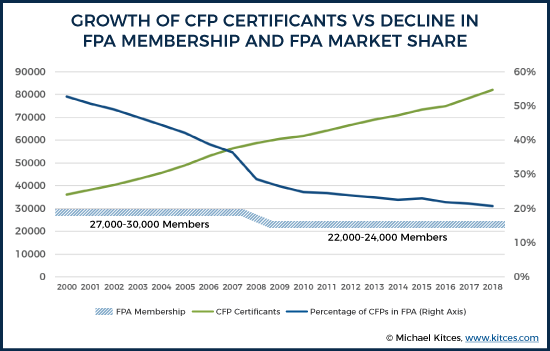

Ultimately, though, the key point is simply that if the FPA is going to get back on track and growing again - recognizing that if the FPA merely maintain its market share of CFP certifications since it was first formed, it should have over 50,000 members today, instead of barely 23,000 - it desperately needs to focus on the real needs of its chapters and the 60,000+ CFP professionals who are not currently members... and it's hard to see how that goal will be achieved by reducing chapter leadership experience on its Executive Committee, and reducing CFP representation amongst its entire Board, even as the FPA continues to try to grow an 86-chapter system while holding itself out as the principal membership association for CFP professionals.

(Michael’s Note: The video below was recorded using Periscope, and announced via Twitter. If you want to participate in the next #OfficeHours live, please download the Periscope app on your mobile device, and follow @MichaelKitces on Twitter, so you get the announcement when a new broadcast is starting! You can also submit your question in advance through our Contact page!)

#OfficeHours with @MichaelKitces

Welcome everyone! Welcome to Office Hours with Michael Kitces!

For today’s Office Hours, I want to talk about the big news that just came out yesterday from the national conference of the Financial Planning Association, which is underway this week.

The big news is that the FPA just announced its new slate of National Board members, including its new incoming President-Elect and future Chair… which will be Skip Schweiss of TD Ameritrade, who leads their Trust Company and their Retirement Plan Solutions business for advisors. Which is significant because it’s not only the first time in its 20-year history that the FPA ever elected someone who does NOT hold the CFP marks to be the leader of the organization that holds itself out as the principal membership association for CFP professionals… but it’s also the first time the FPA has ever elected someone who is not a practitioner, or from an advisory firm, or someone who teaches financial planning, but a vendor that sells to financial advisors… and who writes very large sponsorship checks to the Financial Planning Association itself.

The big news is that the FPA just announced its new slate of National Board members, including its new incoming President-Elect and future Chair… which will be Skip Schweiss of TD Ameritrade, who leads their Trust Company and their Retirement Plan Solutions business for advisors. Which is significant because it’s not only the first time in its 20-year history that the FPA ever elected someone who does NOT hold the CFP marks to be the leader of the organization that holds itself out as the principal membership association for CFP professionals… but it’s also the first time the FPA has ever elected someone who is not a practitioner, or from an advisory firm, or someone who teaches financial planning, but a vendor that sells to financial advisors… and who writes very large sponsorship checks to the Financial Planning Association itself.

In fact, even as the FPA announced at its Annual Conference that Schweiss from TD Ameritrade will be the FPA’s new incoming President-Elect and future Chair, it is also highlighting TD Ameritrade as one of just two “Cornerstone Partners” of the Annual Conference. Which is FPA’s top sponsorship tier for the entire organization.

For those who aren’t familiar, Cornerstone Partnership with the FPA is a $200,000 sponsorship package according to the FPA’s own Sponsorship Kit. That’s the biggest sponsorship check that any organization can write to the FPA. And TD Ameritrade actually has a more-than-10-year history of being FPA’s lead top-tier national sponsor almost every year since the mid-2000s. Which means cumulatively, I believe that TD Ameritrade is at least one of, if not the single largest cumulative sponsor that the FPA has had for the past decade – spending upwards of one or even two million dollars on FPA sponsorships.

And now, suddenly, ‘coincidentally’, for the first time in the FPA’s history… TD Ameritrade gets the first ever non-CFP vendor representative to be selected to be the future Chair of the organization.

TD Ameritrade’s Advocacy Agenda Conflicts With The FPA On Fiduciary Interests [00:02:16]

Now I think it’s important to point out that I’m not necessarily opposed to having representatives from industry vendors be involved in the Financial Planning Association, including at the Board level. The reality is that as financial advisors, we DO need vendors that provide us with the products, platforms, and services that we use to run our businesses and serve our clients.

And vendors that support financial planning ARE stakeholders of the Financial Planning Association. That’s WHY the FPA’s Bylaws specifically state that a minimum of 75% – but a minimum of only 75% – of its Board members must be CFP professionals. However, there’s a difference between having a vendor representative be a member of the board, and a non-CFP vendor representative becoming the future President of the entire organization. Especially when that vendor also happens to be the FPA’s biggest financial sponsor. And ESPECIALLY when that vendor lobbies for advocacy positions that directly conflict with the FPA’s fiduciary advocacy efforts, as TD Ameritrade has done!

A case in point example is just earlier this year, when Nevada issued the draft regulations for its new state fiduciary rule, and invited public comments. For those who aren’t familiar, the basic gist of the Nevada rule is that it would apply a uniform fiduciary standard to both RIAs, AND to representatives of broker-dealers who provide investment advice to clients. This is the exact uniform fiduciary standard that the FPA and the Financial Planning Coalition have advocated for, for more than a decade now.

In fact, the FPA has spent several years gearing up state-wide chapters in large states like Florida and California, specifically to get involved in state advocacy efforts to advance a uniform fiduciary duty at the state level, and the FPA’s website in its advocacy priorities explicitly states that “FPA supports the adoption of appropriate uniform regulation of financial planners that includes a mandatory fiduciary standard of care for ALL professionals providing personal financial planning advice.” Accordingly, when the Nevada rule came out, the FPA along with the rest of the Financial Planning Coalition submitted a public comment letter supporting Nevada’s fiduciary rule as being consistent with the Coalition’s longstanding advocacy for a uniform fiduciary standard for investment advisers AND broker-dealers.

By contrast, when the Nevada fiduciary regulations were announced, TD Ameritrade not only opposed them in their public comment letter, but specifically stated that they thought it was important to maintain “two distinct business models” to serve investors – i.e., NOT a uniform fiduciary standard for all advisors – and even went so far as to threaten to discontinue offering services in the entire state of Nevada if the state went through imposing a uniform fiduciary duty on its brokers. Furthermore, TD Ameritrade explicitly emphasized its support for the Wall Street lobbying organization SIFMA, which itself suggested that Nevada should put aside its rule and defer to the SEC’s Regulation Best Interest… that also did NOT impose a uniform fiduciary rule on RIAs and broker-dealers that FPA advocates for and instead as we now know, is allowing broker-dealers to largely continue its conflict-laden business model as usual.

In other words, the FPA has been a strong supporter of a uniform fiduciary duty for investment advisers and broker-dealers. In 2004, it spun off its entire broker-dealer division to become what is now the Financial Services Institute just so it could take a focused lobbying position on uniform fiduciary standards for advisors and sue the SEC back at the time. TD Ameritrade, as a retail broker-dealer that runs alongside its RIA custody business, has actively opposed a uniform fiduciary duty for investment advisers and broker-dealers and instead has lobbied for separate standards for each to maintain the lower standard that currently applies to broker-dealers. And now TD Ameritrade, having spent a decade being FPA’s largest sponsor writing the biggest checks, now has one of its company representatives as the future President of the FPA in a position to directly influence FPA’s advocacy efforts that have been opposing TD Ameritrade business interests.

Now to be fair, TD Ameritrade’s INSTITUTIONAL business for advisors – its RIA custody unit – has generally been supportive of the advisor community, and Skip Schweiss himself is known as a fiduciary advocate, and his work in TD Ameritrade’s Retirement Plan Solutions business is largely aligned to a fiduciary duty already, albeit under ERISA. TD Ameritrade is a large company, and it’s fair to recognize that it may support advisors in its institutional division, even as it competes against advisors with the advice provided by TD Ameritrade’s retail brokers.

HOWEVER, at the end of the day… the FPA from the 2000s sued the SEC when it issued a rule that undermined uniform fiduciary advice, while the FPA of today mysteriously punted on Regulation Best Interest and failed to challenge the SEC this year in the biggest fiduciary advocacy opportunity of the decade just as TD Ameritrade’s representative was being evaluated by the nominating committee for Board leadership.

And while the FPA has been active at the state level… well, what happens if next year there’s another state fiduciary proposal that would impose a uniform fiduciary duty on investment advisers and broker-dealers, and the FPA wants to support, and TD Ameritrade’s retail division wants to oppose it? And the CEO of TD Ameritrade calls Skip Schweiss and says “Hey, I know you’re responsible for advisor advocacy around here, but our retail brokerage business is going to take a $100M hit by that state fiduciary rule the FPA is supporting. The FPA’s advocacy is costing us a lot of money. You need to get them to back off as the President of the FPA!”?

Is Skip Schweiss really ready to get fired from TD Ameritrade if their next CEO decides to prioritize its retail division over its institutional division and advocates against a fiduciary rule that the FPA is trying to support, and pushes Skip to get FPA to change its tune? How exactly is Skip – or ANYONE – supposed to maintain their objectivity in a position of FPA leadership with that kind of conflict of interest looming over their head, with their job on the line? And if Skip and TD Ameritrade push the issue, can the FPA even afford to say “No” to the organization that’s become their biggest national sponsor in addition to being the President of the National Board?

Can FPA’s Executive Committee Execute The OneFPA Network With A Majority Of Non-Practitioners Without Any Chapter Experience? [00:08:33]

Beyond the deeply concerning conflict of interest that the FPA’s national board now faces with a future President from a vendor organization that has actively opposed the FPA’s own advocacy agenda, the second concern about the FPA’s newly announced leadership is that it means, for the first time ever, the majority of its Executive Committee will be comprised of non-practitioners who also have no leadership experience with the FPA’s lifeblood – its local chapter system.

As the FPA’s rising President who will precede Skip Schweiss in leadership is Martin Seay, a professor and the Program Chair for the Kansas State University Financial Planning program. Who has a strong reputation for being a sharp and level-headed guy… but is someone who, like Skip Schweiss, and UNLIKE almost every other FPA president that has ever preceded them, has no history of being a chapter President before becoming the National President of the Board.

Now again to be fair, I don’t really think that EVERY leader of the FPA has to be a chapter leader before becoming a national leader – although that has been, by far, the most common track to national leadership. But these are uniquely difficult times for the FPA. As it was less than a year ago that the FPA first announced its ill-fated OneFPA Network initiative that would have unilaterally taken over and dissolved all 86 of its chapters and forcibly nationalized them.

Except the initiative was SO out of tune with the actual needs and desires of the membership and the chapters, that the FPA National leadership faced an immense backlash, such that despite announcing the OneFPA Network as an already done deal at its Chapter Leadership conference last November, just a few months later the FPA had to retract the entire initiative and instead walk it all the way back to a “beta” test where they’ll try just some of the things proposed in the OneFPA Network, and then maybe sorta might end out bringing the OneFPA Network back to the table around 2022 or so.

And so even as the FPA is reeling from the National leadership putting YEARS of energy into its OneFPA Network proposal, only to have it struck down by chapter leaders who said FPA National was out of touch with their needs… FPA National now responds with a second year in a row of electing a President that has NO CHAPTER EXPERIENCE?

How is this POSSIBLY going to help the FPA National leadership get better in touch with what the chapters want and need, when the Executive Committee just has less and less representation from anyone who actually has chapter leadership experience and can connect with the membership? Especially since the FPA not only expanded its Executive Committee to include its first non-CFP vendor and become 2/3rds leaders of an 86-chapter organization despite having no chapter experience themselves, but it’s also notable that the newest slate of National Board members includes several more non-CFPs that further move the FPA away from its stated purpose of being the principal membership association for CFP professionals.

As a result, the FPA National Board retired out 4 CFP professionals, and replaced them with two non-CFPs and only two CFPs. And one of the two CFPs is an international representative, whose CFP certification is actually from the Netherlands and isn’t valid in the US.

Which is notable not only because it means the FPA added only one CFP practitioner to its slate of four new Board members this year, but also because if its international member’s CFP marks aren’t valid here in the US, the FPA’s National Board is no longer at least 75% CFP, and the FPA may actually be in violation of its own Bylaws for failing to maintain the required representation of CFP professionals.

And this even as the FPA’s representation of CFP professionals across the country falls to an all-time low. When the FPA was formed 20 years ago, its membership included more than 50% of all CFP professionals. By 10 years ago, it was down to only about 30% of CFP professionals who were FPA members. Now the FPA is about to fall below 20% of CFP certificants who are FPA members.

In response to the reality that the FPA is so out of touch with its chapters that they repudiated its OneFPA Network initiative, and is so out of touch with the needs of CFP professionals that its market share had dropped by more than half… its solution is to REDUCE chapter leader representation on its Executive Committee, and to REDUCE representation of CFP professionals on its National Board?

Maybe FPA has a ‘master plan’ about how a broader diversity of views from non-chapter leaders and non-CFP professionals will suddenly give it insight in how to better connect with its chapters and the more-than-60,000 CFP professionals who aren’t members… but, well, call me skeptical.

Is FPA’s New Nominating Committee Structure Too Little Too Late? [00:13:05]

Now perhaps the greatest irony of all these concerns about the FPA’s latest slate of National Board members and leadership is that the organization IS in the midst of changing its Nominating Committee structure, an aspect of the original OneFPA Network proposal that IS still on the table to be implemented this year.

Under the OneFPA Network proposal, the National Board’s nominating committee would shift from its current structure, where the National Board can populate the entire committee with its own National Board members – which some have already criticized as a very insular and self-perpetuating group – to a structure where half the Nominating Committee will be comprised of FPA chapter leaders from the FPA’s new OneFPA Council, and only the other half will be designated directly by the National Board. And I can’t help but wonder if THIS is still the Board slate, of non-CFP Board members and non-chapter-experienced leadership, that would have been chosen if the chapter leaders had more of a hand in the nominating process for National Board leadership.

Unfortunately, though, the chapter leaders never got a chance to contribute this year, as even though the OneFPA Council is being formed and is supposed to convene for the first time next month at the Chapter Leaders conference, in August, two months ago, the FPA modified its own Bylaws to require that its Nominating Committee must have been appointed at least 180 days prior to the Board elections… which by the stroke of a pen made it impossible to actually include the new OneFPA Council’s feedback in this year’s Board nominees because 6 months prior would be back in February, and back then the FPA was still in its “deciding” phase of whether it was going to move forward with the OneFPA Network initiative or not, due to the huge backlash at the time.

And at the same time in August, the FPA also modified its Bylaws to permit the current President to become a non-voting member of the Nominating committee when previously the President was excluded, which limited undue influence by current leadership on future leadership choices. And that’s on top of the Bylaws stipulating that the FPA Chair will be the Chair of the nominating committee AND its tiebreaker vote, and maintaining a rule that the FPA President-Elect gets to be a voting member of the committee as well. Furthermore, with the new Bylaws, the National Board still explicitly reserves its right to approve – or disapprove, and effectively veto – whoever the chapters select as their chapter leader representatives to the nominating committee, AND reserves the right to approve or veto any candidate the nominating committee selects, AND reserves the right to just go off script and choose its own candidate that wasn’t proposed by the Nominating Committee in the first place.

Which means even as the FPA has publicly emphasized that it is changing its Nominating committee to better incorporate the feedback of chapter leaders in a “participatory governance” structure… it’s actually been engineered to have veto rights to any nominating committee member the chapters select that the National Board doesn’t want, veto rights to any candidate the chapter leaders DO select on the nominating committee, and the ability to choose entirely new candidates outside of who the Nominating committee selects, all while stacking the ENTIRE existing Executive Committee in the room with the Nominating Committee, including the Board Chair as the Chair of the committee with the tie-breaking vote… so, frankly, it’s still not really clear to me whether anything is actually going to be different with the FPA’s leadership selection process in the future.

And of course, with the FPA’s latest set of changes to the Bylaws, there was nothing about a conflict of interest policy in selecting a representative from your largest sponsor who also happens to be actively opposing your own organization’s advocacy positions from then being selected as the incoming President-Elect and future Chair of the organization.

To be fair, the FPA does have an existing Conflict of Interest policy, which states that FPA leaders shall “avoid placing, and avoid the appearance of placing, one’s own self-interest OR any third-party interest above that of the FPA” and that Board leaders should NOT be engaged in “any outside business that would directly or indirectly materially adversely affect the FPA”. But I guess a requirement that FPA Leaders avoid even the appearance of placing a third-party interest above that of the FPA doesn’t apply to the FPA’s own National Board and its Nominating Committee.

Maybe that’s something we can consider changing in the future when we finally get through this OneFPA Network “Beta Test” and can refocus on what the FPA actually needs to do to get growing again under new leadership?

Now I would note through all of this that I’m not raising this concern here because I have anything against the FPA. I’m a 17-year dues-paying member of the FPA, a former chapter President, I’ve been on too many National committees to count over the years, and I’ve been a Chair for one of its national conferences. And as I’ve advocated for years, I believe that a strong FPA is absolutely essential to the financial planning profession itself. Every profession NEEDS a professional membership association, and the FPA is and has always been best positioned to take that mantle of leadership as the principal membership association for CFP professionals.

Heck, if the FPA could have just maintained the market share of CFP professionals it had when it was formed 20 years ago, the FPA would literally be more than DOUBLE its current size, would be nearly 50,000 members instead of barely 23,000, with drastically more resources to support all financial planners, and better capabilities to engage in the exact kind of regulatory advocacy for financial planners that the FPA claims to prioritize.

But if the FPA is finally going to get back on track again, and get its chapters growing with CFP professionals, a good STARING POINT would be to keep the board actually focused on CFP professionals – not reduce their representation – and to select leadership that is really in touch with the needs of the chapters and their financial advisor members – not appoint an Executive Committee that for the first time ever is 2/3rds non-practitioner and non-chapter leader, to be led by a representative from a multi-million dollar corporate sponsor that espouses opposing advocacy views.

Perhaps in the coming year the new Nominating Committee structure with the OneFPA Council, even still largely controlled by the National Board, will be enough to finally help nudge the FPA in a new and better direction with new leadership that can get the FPA growing again the way it SHOULD be growing. Or at least, for the sake of the financial planning profession, and the FPA itself, I truly hope so.

This is Office Hours with Michael Kitces. Thanks for joining us, and have a great day.

Michael,

I feel the need to speak up, because I’m not surprised by recent decisions of the FPA. I left the FPA a few years ago. I had volunteered for several committees, and I got along with everyone in my Philly chapter. The best thing we did was have you speak at our chapter meetings and spring symposiums. Unfortunately, the association felt hallow to me. I’m a small independent advisor who grew from the tax/accounting side. I did not feel home networking at seminars because they were attended by mostly large firm advisors, brokers, or wholesalers. I never found much of a fit among the membership. By the time they started their next generation out reach, I had already aged out.

Sponsorship Capture?

Michael,

After reading all the comments to date, I have to say I agree with you that is is a BIG mistake to make a non-CFP the head of the Board of the FPA. Keep the discussion focused on the conflicts of interest instead of on the exact person that was chosen. I agree with you….there must be some one with a high level of needed skills that IS a CFP. The fact that they chose a non-CFP is, in the mind or this 15 year FPA member, a huge red flag.

Kay C.

Kay,

Indeed, the point of the article is the decision that the FPA made to select a non-CFP from a highly conflicted vendor. It’s not literally about the particular person (who I noted is actually known as a fiduciary advocate).

– Michael

Hi Michael.

I am absolutely baffled by your continuous public assault on the FPA while you simultaneously proselytize on behalf of the CFP Board. How can you criticize the FPA’s enlistment of Skip Schweiss as a non-CFP? The last time I checked, the CEO of the CFP Board, Kevin Keller, is not a CFP either. In fact, his background is as a lobbyist!!! (yeah, that’s great for consumers). My understanding is that Skip is very much an industry insider and I would be willing to wager that he is being paid considerably less than the $1 million salary + hundreds of thousands of dollars in perks that Kevin Keller receives.

You also are critical of Skip’s perspective on the fiduciary standard, yet you turn a blind eye to the CFP Board’s shameless promotion of a faux fiduciary standard that does not require CFPs to disclose the amount of compensation they may receive from the sale of products with opaque commissions. The CFP Board’s new self-defined, self-serving fiduciary standard does not even require its members to provide advance written client disclosure of conflicts of interest. As you surely know, the CFP Board’s new fiduciary standard is not only vastly weaker than the standard the SEC applies to financial planners, it is actually weaker than the FINRA B.I. standard that you and other CFP Board acolytes continue to disparage.

How can you continue to promote the CFP Board when you know perfectly well from Jason Zweig’s and Andrea Fuller’s July 30th Wall Street Journal article that the board actively promoted the CFP mark as a higher standard than the regulatory agencies while simultaneously promoting more than 6,000 CFPs with significant FINRA and SEC disclosure events as being clean? You are also completely well aware that this pattern of deceiving consumers is not new to the CFP Board. In your podcast with original CFP designee Ben Coombs,you openly discussed and acknowledged how the CFP designation was created to help life insurance salesmen appear credible so that they could sell high commission products to consumers. This is your moral high ground relative to the FPA? Really???

It is also worth mentioning that you frequently tout the CFP mark on grounds that CFPs are held to a higher ethical standard and are better educated than non-CFP financial planners. While the Zweig/Fuller article brings that into question, it is my understanding that a peer-reviewed journal article is soon to be published that provides empirical data showing that CFPs tend to have more disclosure events than non-CFP registered reps! I am also gathering data for a paper that I believe will show that CFPs actually tend to have less academic experience in finance and economics than non-CFP financial planners. There is already plenty of anecdotal evidence to support this conclusion. Infamous Ponzi-schemer Bradford Bleidt openly admitted that he used the marks to gain credibility. It is generally known in that many people in our profession attain the marks in order to gain marketing credibility. In your own bio, you describe how you graduated from Bates College with a degree in theater and psychology, and that you felt compelled to attain the marks because you had no prior academic experience in finance. In contrast, financial planners who actually have real, quantitative academic experience don’t necessarily feel as insecure about our knowledge base or qualifications, so it seems intuitive that financial planners who are not CFPs would tend to be more academically qualified.

When highly regarded ethics and fiduciary advocates, such as Don Trone, comment that the CFP Board has done more harm to consumers than any other organization and that its corporate governance is akin to North Korea, doesn’t it give you pause? You are an extremely intelligent man and a great thought leader for our profession. How is it that you cannot see that you are essentially playing the role of Darth Vader in promoting the Evil Empire that is the CFP Board?

I mean no offense by this, but, given your unflappable support for the CFP Board in the wake of scandal after scandal, a question that begs asking is: Do you receive any direct or indirect benefit from the CFP Board or the American College or similar affiliated organization that might be perceived as a conflict of interest? Do any such organizations help fund or promote XYPN or Advice Pay or any other affiliated businesses? I only ask because I just can’t understand the moral or ethical defensibility of your perpetual endorsement of the CFP Board.

Respectfully,

J.R. Robinson

Owner/Founder Financial Planning Hawaii

Wow…this comment is just sooooo wrong on so many levels!

Hi Kay.

Hello Kay.

Here are some of things that I believe are wrong on “so-many levels”

– The CFP Board of Standards has spent tens of millions of dollars each year for more than decade telling consumers that its members are “thoroughly vetted and held to the highest standard.” At the same time, it willfully and knowingly endorsed to the public more than 6,000 CFPs who had major disclosure events including felony convictions as being clean on the CFP Verification website.

– The CFP Board and Michael are outspoken in their criticism of the SEC and FINRA for lax enforcement. None of the 6,000+ CFPs with disclosure events were caught by the CFP Board. At the same time, the CFP Board produced consumer a video featuring the Board’s Corporate Counsel explaining how the CFP Board represents a higher authority than the regulatory agencies.

– The CFP Board and Michael are also outspoken in their criticism of the SEC for enacting Reg BI. However, a side-by-side comparison of the CFP Board’s new self-defined, self-serving “fiduciary standard” finds that it is actually a weaker standard that Reg BI!

– The CFP Board for years ran a multi-million dollar ad campaign stating that “Anyone can call themselves a financial planner. If their not a CFP, you just don’t know.” This statement was actually a complete lie. The SEC regulates all advisers who offer investment guidance and hold themselves out as financial planners. The fiduciary standard of conduct to which financial planners are held by the SEC is far stronger than the faux “fiduciary standard” the CFP Board is now trumpeting.

– Michael regularly states that the CFP marks represent a higher standard of competency and ethics than that of non-CFP financial planners. There is zero empirical evidence to support this claim. In fact, there is some evidence that CFPs tend to have more ethical lapses than non-cfp financial planners. With respect to competency, there is also evidence to suggest that non-CFP financial planners are more likely to have actual quantitative academic backgrounds in finance and econ whereas many CFPs who did not have such backgrounds sought to attain the CFP designation to gain credibility. Prior to 2009, a college degree was not needed to obtain the CFP mark. Even today, no prior academic background in finance or econ is needed.

– As recounted in Michael’s podcast with original CFP graduating class member Ben Coombs, the CFP designation arose out of a desire for insurance salesman to gain credibility in order to sell high commission products to consumers. Today, the CFP Board’s new Standards of Conduct still do not require its members to disclose to their clients the amount of revenue they may receive from the sale of products with opaque commissions. They don’t even require you CFPs to disclose such conflicts of interest in writing.

If my commentary is “wrong on so many levels,” please feel free to call me out, if you believe anything I have written here is factually incorrect. #growaconscience

-JR

J.R.,

I promote the CFP marks, not the CFP Board. I’ve posted many long criticisms of the CFP Board over the years, and actively advocate for and promote change when it comes to various CFP Board policies, both publicly and privately. In fact, we’ve written far more over the years criticizing the CFP Board on this blog than the FPA. Just a handful of examples include:

– https://www.kitces.com/blog/cfp-board-of-directors-public-comments-accountability-and-carver-governance/

– https://www.kitces.com/blog/cfp-board-softens-experience-requirements-for-new-cfp-certificants-reduces-capstone-requirement-for-challenge-status/

– https://www.kitces.com/blog/should-the-cfp-board-really-risk-losing-the-camarda-case-or-is-it-time-to-settle/

– https://www.kitces.com/blog/the-goldfarb-tip-of-the-camarda-iceberg-cfp-boards-ongoing-fee-only-compensation-disclosure-debacle/

We were also the first to point out and criticize the CFP Board for permitting wirehouse brokers to be listing themselves as “fee-only” on the CFP Board’s website in 2014 (a story that ultimately escalated to the Wall Street Journal later that year).

Regarding Skip versus Kevin Keller, there’s a difference between the Board of Directors (where Skip will serve), and being the CEO of the organization (Kevin Keller’s role). In point of fact, none of the CEOs of the major associations have CFP marks – Kevin Keller doesn’t, nor does Lauren Schadle, Geof Brown, or Sean Walters – which I don’t view as a concern. Their role is to run and execute the organization. It’s the Board that sets the strategic vision, where alignment between the board and its stakeholders matters most (and thus why it’s so problematic for the FPA, which holds itself out as the principal membership association for CFP professionals, to have a non-CFP Board Chair).

In terms of your final question, it is fair to recognize that a portion of our educational business on this platform is to serve as a Continuing Education Sponsor, of which CFP CE credits are part of what we offer. But that is compensated by our readers, not by the CFP Board. I do not and have never received any financial benefits from the CFP Board. I have occasionally in the past been engaged as a speaker by the American College, but not for more than a year, and not in any manner more or differently than any of the other organizations that I speak and teach for. In practice speaking revenue from the American College has never even reached 1% of our revenues. And neither the CFP Board nor the American College provide any payments to any of my other businesses in any manner.

But again, simply put, I advocate for the CFP marks, and for reform regarding many policies of the CFP Board itself as an entity. Just as I advocate for the FPA, but also raise issues as a concerned stakeholder when I see concerns.

– Michael

Hi Michael.

Thank you for taking time to respond. As a long-time subscriber to your truly wonderful blog, I have read all of the articles you cited as examples of you criticism of the CFP Board. To paraphrase a famous line from Hamlet, “Methinks you doth protest too much.”

The tepid criticism of the Board you serve up regarding peripheral issues certainly creates the appearance of objectivity, but when it comes to acknowledging the immeasurable harm the CFP Board has done to consumers through its false narratives, deceptive advertising campaigns, and endorsement of thousands of CFPs with major disclosure events and criminal backgrounds, you are all about moving forward with the profession. No outrage, no calls for real accountability. To my moral compass, the Board’s conduct borders on criminal and is unforgivable.

With respect to Skip vs. Kevin Keller, you must also be aware that that the FPA’s membership is not limited to CFPs, so why must all of its directors be CFPs? I am not (and will NEVER be) a CFP, but I am a financial planner and I have been an FPA member for many years. Given the well-documented and now well-publicized ethical and moral lapses at the CFP Board, I am lobbying hard for the FPA to distance itself from the CFP Board and to terminate its membership in the “Financial Planning Coalition” PAC.

Given that the CFP Board seems to be actively trying to undermine the FPA (by launching its own Journals, holding its own conferences, etc.) and that Board supporters like you are regularly publishing articles aimed at tarnishing the FPA’s integrity, I am hopeful that the FPA’s leadership will finally wake up to realize that the financial planning profession’s interests are better served by focusing on consumer advocacy and a true fiduciary standard for its membership base rather than the false, self-defined, self-serving standard that you and the Board are promoting.

Another counter point worth mentioning is that the CFP Board of Directors also has members who are not CFPs and who work for firms that could potentially benefit from their positions. For example, Natalie Wolfsen of Asset Mark is a Director. I will hazard a guess that Asset Mark is a sponsor at the CFP conference, yes? More broadly speaking it seems disingenuous for you to call out the FPA for questionable governance when the CFP Board has been accused of operating under authoritarian rule and secrecy in a manner akin to North Korea. That’s without mentioning the tales of lavish executive junkets and a CEO pay package that would have made William Aramony blush.

Further, if you are so up in arms about Skip Schweiss’ potential conflict of interest, why does it not bother you that your CFP ceritifcate alma mater, the American College (formerly known as the American College of Life Underwriters) has a board of trustees that is comprised almost entirely of representatives from major insurance companies? For the record, it bothers me, that this institution presents itself as a “college” and references its “undergraduate tuition” but has no academic accreditation and confers no undergraduate degrees.

While I respect you for answering my pointed question about your potential conflicts of interest and I accept you at your word that you receive no unreasonable benefit from the CFP Board or the American College that might influence your views, your response leaves me all the more befuddled. Honestly, your comment that you advocate for the marks and for reform at the CFP Board just doesn’t fly.

As you know the CFP Board owns the CFP mark and if you and the CFP Board get your wish of making the CFP mark a required standard for the financial planning profession, then the CFP Board will have monopolistic control over the profession. Time and time again over its 50 year history – and perhaps now more than ever – the CFP Board has willfully abused the public trust and denigrated the financial planning profession. How could you ever in good conscience put the CFP Board wolves in charge of the proverbial henhouse? Why would you do that to the public? I just don’t get it.

Sincerely,

JR

Michael,

I find most of your work enlightening, but you did not do your homework in your criticism of Skip Schweiss. Skip was not involved in the Nevada rule. This objection was driven by the retail side of TD Ameritrade. Skip has been very active for a very long time defending the fiduciary standard on behalf of the RIAs who use TD Ameritrade Institutional. There is no one better equipped than Skip to help the industry move to a uniform fiduciary standard.

Dave Umstead, PhD, CFA

Founder

Cape Ann Capital, Inc.

David,

I’m well aware that Skip works on the Institutional side of TD Ameritrade, and that it was the TD Ameritrade retail side that issued a public comment letter opposing the Nevada rule.

Nonetheless, the concern I’ve raised still stands. What happens when the next CEO faces a situation where a fiduciary rule that Retail opposes is one that Institutional supports? Which line of business is bigger for TD Ameritrade if/when the two come into direct conflict with each other? What if the CEO decides to prioritize the retail business over the institutional business, and finds out that a key Institutional executive is in a position to influence the biggest association that is pushing for a fiduciary rule that harms TD Ameritrade’s retail business?

If you don’t think that’s possible, just look at what happened 2 years ago when TD Ameritrade was acquiring Scottrade and decided to revamp its entire No Transaction Fee ETF platform to better monetize their retail business? The entire Institutional business was deemed ‘collateral damage’ and forced to tow the line.

Conflicts between the Institutional and Retail channels happen at all the multi-channel custodians. In and of itself, that’s fine, the marketplace can sort itself out, and unhappy advisors can vote with their feet.

But that doesn’t mean it’s a good idea to put a highly conflicted vendor executive into the highest position of influence in an association that lobbies against his parent company’s corporate interests. It has nothing to do with Skip personally. That’s an untenable position for ANYONE.

FPA has a Conflict of Interest policy for a reason. That they unfortunately chose to ignore. And there’s no “exception for nice guys” exclusion. I checked.

– Michael

Bear in mind as well that the FPA of 2004 spun off its entire broker-dealer division (to what is now the Financial Services Institute) to eliminate the Board’s conflicts of interest so it could challenge the SEC on a major fiduciary rule (in which the FPA ultimately prevailed in 2007 and had the rule vacated).

By contrast, the FPA of today retains a more conflicted board, and “coincidentally” decided not to challenge the SEC over the biggest fiduciary advocacy opportunity of the decade (Reg BI).

I don’t know whether that’s a coincidence, or TD Ameritrade’s influence over the FPA Board. The problem with the FPA opening itself up to such conflicts of interest is that there’s no way FOR us to know now, especially since the Board no longer releases its Board Minutes to members. It just looks bad. 🙁

– Michael

It all comes down to putting our money where our mouth is. We wouldn’t need corporate sponsors if we, as CFP’s were willing to pay 2,3,4K per year instead of 4 or 500 per year in dues. We all want to join a group with no conflicts but very few are willing to fund its operations. We’ll just opt for the cheap option with conflicts and then complain about it later.

This is the nail in the coffin, the FPA should have sued over Reg BI and the fact they abdicated their duties speak volumes.

Michael,

I think you are wrong on 1 point and that is that the CFP mark of the new International board member is not valid in the US. The CFP mark is the same in all the Countries where CFP’s are active. The only difference is local knowledge. I think it is great that we now finally have an International Board member because he can bring in some more International perspective.

Henk,

I’m all for the international sharing of information.

But legally, the CFP Board owns the CFP trademark in the US, and the FPSB owns the CFP trademark outside the US (which it then sublicenses to other countries for their local CFP organizations).

Which means someone who earns CFP certification from the FPSB doesn’t have the legal right to use the trademark in the US. Because the FPSB doesn’t own the trademark in the US. The CFP Board does. And the CFP Board only grants the right to use the CFP marks in the US to those who meet the CFP Board’s US requirements. Which weren’t met here.

– Michael

Great post Mike!

FWIW, I sat in that seat at a time when FPA was undergoing great change and dealing with controversial issues. I have some understanding of what it takes to affect change at that level of the organization. When Mr. Schweiss was announced at the conference, I was very happy and actually made a fist pump. He is an experienced and seasoned executive and Michael, if you want some of the things you are critical about to get addressed, a leader like Skip strikes me as exactly what is needed. Skip Schweiss has my full and unqualified support.

Dan,

I appreciate the comments, and do understand that at a personal level Skip brings some valuable corporate leadership experience that FPA lacks and needs.

But if Skip as a non-CFP vendor representative from a company that actively opposes the FPA’s advocacy agenda was the “only” good choice that FPA had – such that it felt it had to choose such a conflicted President to break precedent – then I have some very serious concerns about what FPA has done to its leadership development pipeline over the past 7 years since Lauren took over.

What’s happened to an entire decade of NexGen leaders who were incredibly active in NexGen under Marv Tuttle, yet not a single one has reached National Leadership, or even joined the National Board, since Lauren took over as CEO? (As the latest/closest was Mike Branham, but he joined the Board and was elected while Marv was still CEO.)

Where have all the future leaders gone?

– Michael

I understand the concerns about the conflict. He understands fiduciary issues better than 99% of CFP licensees and if anyone can manage the conflicts, he can. We won’t know for sure until we see it unfold, of course so I am not arguing that there is no conflict or that the conflict doesn’t matter. In fact, I agree with many of your concerns about FPA. My concerns are precisely why I was happy to hear Skip’s name called. I think his considerable skill set may be exactly what is needed to help fix things. Changes must come and that means some tough decisions need to be made. He is more than capable of making those calls. He has my full and unqualified support.

Dan,

I can appreciate that Skip has a personal skillset to help FPA with some of its woes.

But I would also expect Skip, as a fiduciary advocate, to understand more than most that fiduciaries are expected to avoid material conflicts of interest, not just disclose them. Because material conflicts of interest can undermine even good well-intentioned people. That’s why there’s no “but he’s a nice guy” exception to the fiduciary rule.

The truly hard thing about being a fiduciary advocate is that it means we can’t just advocate that “THEY” have to be fiduciaries that avoid material conflicts of interest. It means WE have to advocate for OURSELVES to avoid material conflicts of interest in our OWN fiduciary roles as well, and lead by example.

Simply put, if the FPA is not willing to apply the requirements of a fiduciary obligation to itself (even and especially when it’s hard), how can the FPA ever maintain the credibility to advocate that a fiduciary duty be imposed on others?

– Michael

Only the White House is more corrupt.

Make it democratic! Create 11 geographical voting districts each with about the same amount of FPA members. FPA members in each district could vote for their own board member. (Also make being a CPF certificant as a requirement to hold office.)

Any adviser can vote with their dollars. They can quit FPA, and join other organizations like NAPFA. Then the FPA will have the choice of changing their ways or fade into obsolescence. Looks like that’s what’s happening.

I just discovered a new way some CFP certificants are ignoring their fiduciary duty.

A service I heard about is the Schwab Intelligent Portfolios Premium for $300 upfront + $30/month for unlimited talk with a financial planner. I was thinking how could they offer this so inexpensively?

They make a profit with 2 hidden fees.

First they switch all the clients funds to Schwab funds, where they make money with the fund management fees.

Secondly, they keep at least 8% of client’s portfolios in cash and paying them a low interest rate. For example, Fidelity sweeps unused cash into rates that are about 1.5% higher. For a $500,000 account, $40,000 would be in cash and would lose about $750 compared to Fidelity. (Also that money isn’t given the option of being in stocks, and a 7% difference between stock market securities vs. Schwab’s low interest difference would be a $2,800 difference.)

A true fiduciary would consider investments from more than one fund company, and wouldn’t keep all that cash at near bottom interest rates. I hope the CFP Board disallows CFP’s from working in this conflict of interest situation, before they start losing their reputation like the FPA is.

Apparently the transition to ‘industry organization’ is complete.

We should face up to the fact that large organizations never care about quality of service or care at the client level, revenue concerns always win. With industry groups controlling the FPA the focus will be on what maximizes revenue for the industry, not any standard of client care. Quality work is expensive and often not as profitable, and the ‘industry’ doesn’t care: “Just sell’m that propitiatory variable annuity with the 8 year CDSC, and stamp it “fiduciary quality work” and move on the next sucker, …err ..we mean prospect because you need revenue in your grid this month or we will laugh at you in the next sales meeting…err…we mean compliance training event …and every one knows you can’t get to Hawaii on Vanguard Airlines.”

The CFP board is almost as bad as the FPA. Just imagine how they let CFPs work at Edward Jones and still use the marks…

I am considering starting a new organization to carry the true mantle of the fiduciary standard, I just need a name and I am considering these: (let me know which you prefer)

The Highest Order of Real Serious Fiduciaries (HORSF) or

The Association of Fiduciary Education (TAFE- pronounced TAFFY) or my favorite:

Standards Association Promoting Professional Services (SAPPS).

Com’on and join me, lets all be SAPPS!

Or:

Fiduciary Association of The States (FATS) or,

Kind Neighbors Instituting Fiduciary Education (KNIFE) Or :

Center of America Retirement Education Systems (CARES), or

Woman fiduciaries Have Organized (WHO)

Perhaps several organization might start up and then latter merge. The new organization would be called: KNIFE FAT SAPPS WHO CARES

Imagine the Chair of the American Medical Association being not an MD and president of Tylenol! Could not happen.