Executive Summary

Financial advisor standards of care has become the "hot topic" of 2016, driven by everything from recent controversies about the CFP Board's enforcement of its compensation definitions, to the looming Department of Labor fiduciary rule. Yet despite rising scrutiny over fiduciary standards of care, the FPA took the somewhat controversial action last week of dropping its requirement for financial planning professional members to adhere to its own FPA Standard of Care and Code of Ethics.

In this week’s #OfficeHours with @MichaelKitces, my Tuesday 1PM EST broadcast via Periscope, we explore the FPA decision to eliminate its Standard of Care, and look at how it was actually a good decision of the organization - because the reality is that the FPA has no means to enforce a standard of care anyway, and claiming to have a standard of care without enforcing it just creates more problems than it solves by attracting low-quality "professionals" who wish to don the mantle of a professional association.

In fact, arguably the biggest problem with FPA's decision to drop its own Standard of Care was that it didn't go far enough. While the organization said members will still be required to follow the Standards of Care that apply from other credentialing bodies and regulators - from the CFP Board to the SEC and FINRA and state regulators - which means CFPs doing financial planning will be fiduciaries, as will financial planners working within an RIA, the reality is that the FPA still permits "financial planning professional members" to include non-CFP product salespeople who are not subject to a clients'-best-interests standard at all. Which means, ironically, that the FPA just lowered the required standard of care for its non-CFP members!

Ultimately, the FPA does continue to acknowledge that it sees the CFP marks as the best certification around which to build the financial planning profession... yet the question arises of how the FPA can say it embraces CFP certification as the basis for the financial planning profession, yet continue to invite "financial planning professionals" who are not CFP certificants and now, under FPA's revised rules, aren't even required to give financial planning advice in the best interests of their clients (as FINRA and state insurance regulators don't required them to) - which, notably, is a violation of the original Memorandum of Intent upon which the FPA was founded!

(Michael’s Note: The video below was recorded using Periscope, and announced via Twitter. If you want to participate in the next #OfficeHours live, please download the Periscope app on your mobile device, and follow @MichaelKitces on Twitter so you get the announcement when the broadcast is starting, at/around 1PM EST every Tuesday! You can also submit your question in advance through our Contact page!)

#OfficeHours with @MichaelKitces Video Transcript

Good afternoon, everyone. Michael Kitces here talking to you for our weekly Office Hours with Michael Kitces segment. This week I decided to tackle a frankly not-very-well-covered announcement in the industry news last week. FPA sent out a rather interesting email to members, announcing that they were basically eliminating the requirement to follow the FPA Standard of Care and Code of Ethics. So as members, we will no longer be required to actually honor the Code of Ethics and Standard of Care that's written into FPA membership requirements. Or I guess, now no longer requirements!

[Email from FPA National, sent Monday, January 18th at 11:46PM]

Dear Michael,

I want to inform you that the FPA Board of Directors voted unanimously in November 2015, to transition our Standard of Care and Code of Ethics from a requirement of FPA membership to an official, organizational policy. This shift is effective Jan. 1st.

Why did we make this change?

FPA is not a regulatory or certifying body, but rather a voluntary professional membership organization and as a consequence of legal and resource issues inherent in developing and enforcing standards effectively, it is not in the best interests of our association and the profession to set standards that other bodies use to measure the ability to hold a license or certification. The Certified Financial Planner Board of Standards, the SEC and FINRA all set standards to ensure that those affiliated or bearing their marks are abiding by those standards. Most importantly, as a policy matter, FPA will take on the appropriate monitoring role to ensure that standard setting bodies are meeting their responsibility to advance the financial planning profession.

What does this mean to me?

While FPA will continue to hold our Code of Ethics and Standard of Care policies in the highest regard as a means to elevate the profession by influencing policymakers, regulators and legislators, it is simply no longer a requirement of membership. By clarifying the role of those policies in our association, we are cementing the role of FPA in the profession as the organization that grows and nurtures highly competent financial planners rather than one that certifies and regulates. FPA supports the CFP® marks as the best certification to build the financial planning profession around and as such, we will continue to be staunch advocates on behalf of CFP® professionals for the appropriate policies and rules that standard setting and regulatory bodies implement. We will also continue to support that our CFP® professional members uphold their fiduciary duty when providing financial planning to the public. FPA will use the disciplinary decisions from certification and regulatory bodies to determine continued membership in FPA and/or participation of members in certain programs and services.

How can members who want to leverage the FPA Standard of Care and Code of Ethics policies in their marketing do that moving forward?

Members are encouraged to demonstrate their voluntary support of the FPA Standard of Care and Code of Ethics policies. Since following the Standard and Code policies is now voluntary, members cannot state that they are required or mandated to do so. For example, it is perfectly acceptable to say that you “proudly adhere to the FPA Standard of Care and Code of Ethics policies.” It is not acceptable to say “Membership in FPA requires compliance with the FPA Standard of Care and Code of Ethics.”

If you have any questions, you can refer to the FAQs posted to OneFPA.org or you can reach out to the following FPA staff:

Karen Nystrom (Advocacy Team Leader) at [email removed]

Ben Lewis (Public Relations Team Leader) at [email removed]Thank you for your continued support of FPA.

Sincerely,

Pamela Sandy, CFP®

2016 FPA President

FPA Standards Of Care And Code Of Ethics

So this is kind of a funky thing. As I'm going to explain to you in a moment, I think it's actually a good thing in the long run and something I've been calling on the FPA to do for a couple years.

But let me start with this little thought experiment. So how many of you are... well hopefully most of your members of FPA. You should be members of FPA, or AICPA, or NAPFA. So give me a little tap, tap here [on the Periscope app] if you're members of at least one of the major membership associations.

But how many of you had this experience? You've gone to an FPA chapter meeting, you're doing the whole networking thing, you're introducing yourself, you're meeting some of your peers at FPA. And you meet a couple of great people, there's a lot of good planners and FPA, and then you meet a couple of people where you're going, "I'm sort of embarrassed this person is my peer in a professional membership association."

Anybody ever had that feeling before? I'm seeing some hearts, you can chime in and type here if you've experienced this once. I know I've gone through it, right? I go to an FPA meeting, and say, "Hi, good to meet you. Tell me a little bit about your business, your practice." And then you start talking to them, and it's like, "Wow, you actually don't care about financial planning at all. It's just a product sales pitch thing for you. In fact, you're pitching me, and I'm your fellow peer, and you're pitching me to sell something to me at the meeting!" Right? I'm seeing the [Periscope] hearts. Some of you have actually had this experience. They're so wired into being salespeople that they can't even not try to sell you at the meeting. Wow, look at all those hearts. I'm really hitting someone's nerve here!

So, we've had this problem I think with FPA for a long time, and probably more so than NAPFA and AICPA PFP. There's some really good people in the crowd, and frankly, there are some people that I'm a little embarrassed to call my financial planning professional peers in this professional membership association.

Lack Of Enforcement For FPA Standard Of Care

Now in theory, FPA had an answer for this. It was called the FPA Standard of Care, it was pretty straightforward, all the normal things you would expect a professional Standard of Care to have. You have to put your client's interests first, and you had to act with due care and almost good faith, and you couldn't mislead clients, and you had to disclose all the material facts, and disclose and manage your conflicts of interest. We had all these line items written out.

But there was a fatal flaw in FPA's Standard of Care, which anybody who's been to a chapter meeting and talked to some of their peers has kind of noticed. There's no enforcement. There's no enforcement. Right? You show up at an FPA meeting, you meet someone doing all sorts of stuff that he/she really shouldn't be doing or is demonstrating at the meeting that he/she clearly does some things with clients that are probably not putting client's interests first, and mismanaging conflicts of interest, and so forth. And you're sitting right there at the meeting, and you're sitting as FPA member at the meeting saying, "I can't believe this person's my peer. It's kind of embarrassing to be a professional member, or member of this professional association, when these are the people that are around me."

I know this hits some chapters more than others, so depending on what chapter you're in, you either fortunately see this rarely, or sometimes you see it unfortunately all the time.

But FPA had this fundamental flaw with its Standard of Care, which is that it put out there this grandiose statement, "All of our members adhere to this highest standard. We put our client's interests first." They never use the F word, fiduciary word, but basically it was a fiduciary standard, "Put your client's interests first. Act with due care. Don't mislead. Manage conflicts of interest. Disclose all material facts." And then there was no enforcement. To my knowledge, I'm not aware in the history of FPA and its 24,000 members or whatever it is now, and 16 years now that it's been in existence, that it has ever eliminated a member for failing to adhere to its Standard of Care!

Which is what I was illustrating with the article I wrote a couple of years ago: What's the point of a standard of care if you can't enforce it? If you're not enforcing the standard of care, at best it's meaningless, at worst, it actually attracts in bad people who want to be recognized for being a member of your great organization with its great standard of care and then just not do it, and have zero repercussions for that. And I think that frankly was a challenge that FPA has had. It was living out in real time. This is the problem when you create a standard of care and don't enforce it. So I had actually been advocating for years that FPA needed to dump this ridiculous standard of care. Not because financial planning professionals shouldn't have a standard of care, but because it doesn't belong in a membership association that has no means to enforce it.

One Profession, One CFP Designation Standard

And particularly in a world where FPA increasingly has said that they're focusing on the CFP marks at the center of the financial planning profession. CFP has a standard of care. It has one that the CFP Board actually enforces. Granted, I've been a critic occasionally of some of the CFP board's enforcement policies. We can get a little better there, and I'll be writing more about that in the coming weeks. But they have a standard of care, it's clearly articulated, it's radically better defined. It goes into serious detail about what the standards of professional conduct are, not just FPA's like five bullet points and that's it. And the CFP board has an enforcement mechanism. They enforce, they investigate matters, and they discipline CFPs publicly, and they even kick some of them out for failing to adhere to the professional standards.

This is what a professional standard really shows look like, a standard of conduct where you actually lose something for not following through on it. So FPA has basically said, "You know what? We're a member association." They basically acknowledge this kind of criticism I've put forth for years. They're a membership association. They have no enforcement means. They don't really have the resources to like build out an enforcement division, nor does it really make sense for them to do so. So they said, "We're letting it go. We're not going to enforce the Standards of Care." It's going to be kind of optional. I guess they'll leave it there for some reason, even though it's basically... well, it's even more meaningless now. Not only is it there and not enforced, but it's not even required. So you just kind of say it and it maybe sort of means something? I'll come back to that at the end. I think even that's ironically a problem now.

But what FPA instead has said, "We're going to look for our members to be in good standing with their other regulators." So with the CFP Board, with state securities regulators, with federal securities regulators, so the SEC and FINRA presumably, state insurance departments as well. And members who run afoul of other regulatory organizations that have what eventually become public disciplinary matters if you're found guilty, will be addressed within FPA as well. FPA didn't go so far as to actually say, "We will kick out members who are found guilty of at least severe regulatory infractions," but presumably that's what they mean. Frankly, in a positive way, I'm going to be waiting for the first announcement of the first ten members that FPA kicks out because they've got a giant list of regulatory infractions already against them. Right?

In fact, I would bet all my life savings that if I did a FINRA search on all 24,000 FPA members, I'll bet you I can find at least ten of them right now that have so many regulatory infractions it would make your skin crawl. Unfortunately, they're out there. FINRA has been long criticized for allowing rogue brokers to keep coming back into the industry. So I'm hoping this means that FPA is actually going to look at some of these regulatory records, look at new regulatory infractions that come in, and actually start kicking some people out who are at least the worst of the worst. It's hard to clean everyone. There's a lot of financial advisors out there, but we can at least start with the lowest of the low, knock them out, and lift the bar over time.

So overall, I actually think this is a good change. FPA was only kidding itself having a standard of care that had no actual means to enforce. I think they were attracting in bad actors who thought it sounded great to be part of the Financial Planning Association, even though they had no interest in actually doing financial planning, following financial planning, adhering to financial planning standards, or acting in their client's interests. They were there to sell a product and that was it. Which frankly, I think there's a role for in this world. But you don't call yourself a financial planner when you're there to sell product, and your sole role is a salesperson. So FPA getting rid of this standard and not fooling itself, I think is a plus.

CFP-Centric In Name Only?

Now here, unfortunately, is kind of the caveat for it. Ironically I think while FPA took a good step on this, I'm not sure that they went far enough in some ways. Because when you read the detail of what FPA wrote, and I'll make sure we get this published up to the blog [see above], they sent out as a member email. Presumably if you're all members, you should have gotten it last week. But they sent this out, and what they said is basically, "We're not going to require the Standard of Care anymore. We're going to allow other regulators that already do regulation to do the regulatory action, and we'll look to them for enforcement to figure out who's adhering to the appropriate standards."

And then the FPA made this comment, "The FPA supports the CFP marks..." I'm reading it right off the letter, "The FPA supports the CFP marks as the best certification to build the financial planning profession around. And as such, we will continue to be staunch advocates on behalf of CFP professionals for the appropriate policies and rules for standards setting and regulatory bodies." So, "We continue to support the CFP marks."

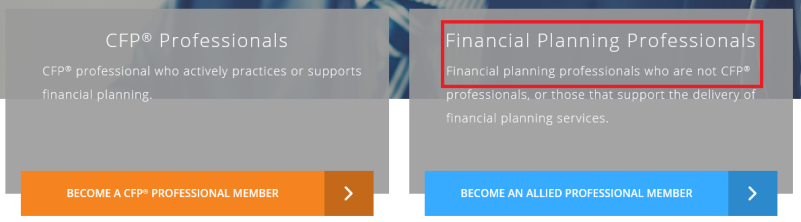

But here's the weird thing. You still don't actually have to be a CFP to be a [financial planning professional] member of the FPA. They have this category that's called Allied Professionals. And while I think originally the point of Allied Professionals was like attorneys, accountants, people that are proud of the financial planning product ecosystem, that genuinely work with and support financial planners as allied professionals, which I'm all for having. We need those people to serve our clients well. We should have relationships with them if they believe in financial planning wellness, support it, they should be welcome in the Financial Planning Association. But FPA's Allied Professionals is kind of a fuzzy catch-all category, and it basically says it right on their website, "This is for people who support the financial planning process, or people who provide personal financial planning services to the public without a CFP certification."

In other words, if you want to be a financial planner and do financial planning for the public and just not have CFP marks, hey, that's apparently still cool with the FPA. And I don't really get that. If they're serious about standards of care, why do we continue to welcome in people who are doing financial planning but not serious about a standard of care? And I'm sorry if I'm offending a couple people out there who are doing financial planning but don't have CFP marks and don't plan to get them. There was a point 10, 20, 30 years ago where that was okay. That's not going to be okay going forward. That's not where the profession is going. That's not where we are going in emerging this as a profession. All professions have a minimum competency standard.

Doctors have got to go to medical school, accountants have to get their CPA, lawyers have to get their JD, and financial planners are going to have to get their CFP certification. So if you've been lagging with the times, I'm sorry, it's going to be time to come forward.

But as FPA, I don't understand how they can still say, "We support the CFP marks as the center of building a financial planning profession, but we welcome all people to do financial planning [as 'professionals'] for the public even if they don't have CFP marks."

And it's not even just about the CFP marks per se. This world where FPA is now delegating its enforcement and its standards of care to other organizations, here's what this means, if you're an FPA member who has a CFP certificate, you're subject to a fiduciary standard under CFP Board guidelines when you deliver material elements of financial planning to the public. That's CFP Board rules. If you want to just be a non-CFP that does financial planning for the public that proudly says you're an FPA member of the Financial Planning Association, the leading organization for the financial planning profession and not have your CFP marks, and therefore, not be held to any kind of fiduciary standard of care, that apparently is okay. Right? Because when FPA gets rid of its own standard of care and just says, "We'll use whatever regulatory body you're subject to," that means if you're a CFP subject to a fiduciary standard, you're a fiduciary. If you're an RIA subject to fiduciary standards, you're a fiduciary. And if you're just a product sales person subject to solely FINRA or insurance regulator suitability product guidelines, FPA is still welcoming you as a member of the financial planning professionals. And I don't get that.

If the goal is to advance a financial planning profession, and FPA really believes that advancing the financial planning profession means building around the CFP marks, when are we going to get to the point where we're actually willing to say, "We're going to put a stake in the ground for building a profession, you've got to get your CFP marks"? Now you can be working on it, right? We don't have to give everyone a boot all at once. We can have a transition plan, if you don't have your marks, we can give everyone a three-year window or something to go get them. Ironically when you look back at the founding documents for the FPA, it was supposed to be CFP centric right now, and everyone had a ten-year transition opportunity to get their CFP marks before FPA was going to become purely CFP centric.

That was written into the founding documents [and the FPA merger Memorandum Of Intent And Commitment]. I think it was a ten-year window. It's a ridiculously long window when FPA was founded in 2000, yet here we are in 2015 still welcoming non-CFP, non-fiduciary people who go out and proudly say, "I deliver financial planning to the public as a member of the Financial Planning Association." [In fact, the founding FPA Memorandum of Intent stipulated that "all individual members engaged in financial planning, including those who are not CFP licensees, will agree to adhere to the CFP Board's Practice Standards", a requirement the FPA is now ignoring and violating.]

And to me, it's just incongruous. It's inconsistent, it lacks really following through on this vision that FPA claims that they're pursuing but they're really not. So kudos to the FPA for at least eliminating their own weird, duplicative standard of care. If you're supporting the CFP marks, you needed to support the CFP Board's professional standards, and I'm glad that FPA has finally made that transition because there was no way the FPA was going to enforce it. I had said it for years. It was an untenable problem at the organization, and fortunately they finally moved past that step.

But for all of us as members that show up at local membership meetings, and want to shake hands with fellow financial planners and be proud of the people that are in that organization with us, we all need to be held to the same high quality standard. That's what makes a quality membership association where you're actually proud to be part of the organization and be involved with your peers at that organization, not just voluntary standards. You've got to draw a line and require it. And FPA seems to still drag its feet on that by welcoming people who are not CFPs, not fiduciaries, not obligated to act in the interest in their client, to call themselves financial planners and to be financial planning members of the association.

Can The FPA Advance To The Next Level?

So, FPA, good job on the first step, but it's still time to go to the next level. It's still time to really say you're serious about fiduciary financial planning and building a profession around the CFP marks, which means not welcoming "financial planners" until they get their CFP marks or they're genuinely pursuing it.

So you guys tell me, do you agree with this? Am I nuts? Am I just ranting off into space here, or do you agree with this idea that financial planners, if they're really going to hold out to the public, should have appropriate minimum standards that go along with this. It's something I believe in very strongly. I think I'm seeing from the tapped up hearts on Periscope here that at least a number of you agree with that as well!

So give that as feedback for your FPA leadership, push that message forward.

[Question: Is there an org that is doing what you want?]

Is there an organization that's doing what I want, what I vision this category? Yeah, I honestly, I think the AICPA is with their personal financial planning section. Now, that's not really a fit for non-CPA financial planners, but the AICPA actually took this one step further, and I wrote this up on the blog last year. The AICPA because it's both function as membership organization and it provides guidance on the standards that state regulators actually use to enforce against CPAs, the AICPA's personal financial planning section actually set forth standards on personal financial planning conduct that require essentially a fiduciary-esque standard. They didn't literally use the F word [fiduciary], but it's basically embodied in the code that they wrote.

And that can actually be enforced against CPA financial planners not being fiduciaries and not acting in their client's interests. So AICPA I think almost went one step further, that they're really driving this as an enforceable action pushing down from the AICPA. I think NAPFA takes a step towards this as well by requiring other, I think now CFP or PFS marks, maybe they're down to just CFP, and requiring fee-only, and requiring fiduciary.

FPA has lagged behind on this. Frankly, I think they've always lagged behind on this. And while at least acknowledging that their regulatory standard was duplicative and that they needed to get rid of their standard of care, which kudos, they've done, they're still not actually lifting the bar and saying, "Oh, and now you've got to be a higher standard."

Strictly speaking, FPA just actually lowered the standard now for all their non-CFP members, because you're still only subject to state insurance regulators or FINRA. You're not subject to CFP board's fiduciary requirements, you're not subject to state fiduciary requirements, and you're not subject to the FPA's, granted unenforced, but still, you're not even subject to the FPA's standard of care. So we actually let non-CFP members take another step down on quality standards without any backing, without any enforcing, while they still deliver personal financial planning services to the public and proudly say they're members of FPA.

Department Of Labor Fiduciary Vs CFP Fiduciary Standards

[Question: Should FPA distinguish between the CFP fiduciaries vs the soon-to-be "DOL fiduciaries"?]

"Should FPA distinguish between CFP fiduciaries and the soon to be DOL fiduciaries?" Yeah, absolutely. I think this is part of why, if FPA really wants to move forward and remain relevant... they say they support building a financial planning profession around CFP marks... if they're really serious about that, if anything, now is the time to finally make this transition. Again, the founding documents of the FPA said this was supposed to have been done years and years ago. And the FPA board has just basically not followed through on the legal guidance that was written into the founding documents.

But absolutely, we're going to have a massive crisis of differentiation coming. I've written about this already. I think frankly we're already in the midst of crisis of differentiation as advisors. It's about to get a whole lot worse when we bring in a fiduciary standard from DOL [and "everyone" is a fiduciary], which realistically is probably going to turn into an even broader fiduciary standard in the next couple of years. The SEC is very likely to take this up in 2017. FINRA is going to try to glom onto it. I really think this is actually the beginning of a broader based fiduciary standard.

But here's the thing, even for a fiduciary standard, there's technically two duties of care under a fiduciary standard that matter, two core duties for advisors. Number one is the duty of loyalty, that's the one we all talk about. You've got to act in your client's interest, do the right thing. Number two is what's called the duty of care. The duty of care... so the technical definition is you should only give advice in areas in which you're competent, or as I like to put it a more basic level, if you're going to get paid for advice, you should know what the heck you're talking about in the first place. So you should actually have some training and education about how to give advice.

Ironically the problem with DoL fiduciary, while it will lift up the duty of loyalty, it's doing nothing for the duty of care, right? There are going to be people out there who are legally obligated to act in their client's best interests, and their only training in finance is a series 65 and a high school diploma, and the high school diploma was optional. So I don't know how those folks even know what's necessarily in the best interest of their clients when they're that undertrained in the delivery of advice and the evaluation of solutions. So I actually think the next battleground that you're going to see in all these fiduciary discussions once we lift up the duty of loyalty, is going to be the duty of care. It's not just about acting in your client's interests, competency matters too.

And the DoL fiduciary standard has no competency requirement attached to it. Something like what the CFP marks do. And I think that's a huge opportunity for the FPA to distinguish real fiduciaries from DoL fiduciaries. Real fiduciaries act in their client's interests and have the training, and education, and experience to know what they're talking about. DoL fiduciaries just have to act in their client's interest even if they have no idea how to actually fulfill that obligation.

So this becomes the next battleground issue, and again is a chance for FPA to take leadership for once, like driving the vision forward the way they did 10 years ago when they sued the SEC over these rules. It's time to say, "Look, if we're going to have a fiduciary standard going forward, it's not just about duty of loyalty. Duty of care matters too. Competency matters too. We believe that the CFP marks are the best line we can draw in the sand about what real competency means."

Frankly, as many of you know, I advocate that you should go beyond the CFP. The CFP is not like an endpoint to your education, it's a starting point. It's a minimum professional standard, not the end and pinnacle of your career. But if anybody's going to take up that mantle and push it, it's FPA, it's the Financial Planning Coalition working jointly with NAPFA and the CFP Board. They can actually all get on the same page about this, but it's FPA that lags, right? NAPFA requires everybody to have a CFP marks to be a financial planning professional. Obviously CFP board is built around that. It's the FPA who still says, "We welcome you as a financial planner that works with the public without being a fiduciary, without being obligated to a standard of care, without getting your CFP marks, and without having getting your training, education, or experience, or any expectation that you're going to get it."

So it's FPA's chance to step up. Getting rid of their own standard of care was the right first step, but really taking the next step to embracing the CFP marks is ultimately how we move the profession forward, and again, as you said [in your question] Hannah, this is a huge opportunity for differentiation as a whole slew of DoL fiduciaries are going to come in, who have the duty of loyalty, and FPA members can differentiate on duty of care, on competency and expertise.

I hope that's helpful as food for thought around this whole dynamic. This story has been really, really quiet. Financial Advisor Magazine wrote something about it last week, but only because I tipped off one of their reporters about this news when I was at the AICPA conference. Frankly, I don't think it's got the discussion that it deserved, which is why I wanted to elevate it with the discussion here.

But again, hope this has been helpful food for thought for you. I guess if there are just one or two things you could take away from this, first, recognize it is a plus. It was actually something that needed to be done. FPA was not going to enforce its own standards of care. It needed to work with CFP Board and regulators. But a big number two is technically, this has just lessened the standards for non-CFP financial planners in the FPA.

And if FPA is really serious about moving the financial planning profession forward, and as it says, "Using the CFP marks is the best certification to build the financial planning profession," it's time for the FPA to be willing to actually say, "If you are delivering financial planning to the public, you need to be a CFP certificant, or get one, or you don't belong as a financial planning member of this organization. We welcome other allied professionals who support, but don't be saying your financial planner who's a member of the Financial Planning Association if you're not a CFP certificant of the Financial Planning Association."

Thanks again for joining in Office Hours. Next Tuesday, 1 p.m. East Coast time, we'll be continuing. In the meantime, if you've got questions you want me to field an answer, you can put them in through the blog as well, kitces.com/contact, that's the stuff that comes to me. I really do read all those emails. I cannot reply to all of them because there are a lot of you now that send me emails, but I really am reading them. I will respond to as much as possible.

So thanks again, everyone, and have a good day.

So what do you think? Was it a good decision for the FPA to eliminate its own separate Standard of Care and Code of Ethics? Is the FPA still not focusing enough on the CFP marks and advancing the profession? Is it appropriate to allow non-CFP financial planning "professional" members in the FPA? Please share your thoughts in the comments below!

Re: The CFP Mark and Fiduciary Status

Admittedly, I am going off-track, but only somewhat. As a licensed attorney, securities representative and insurance agent with considerable experience in trust operations and OCC Regulations, I have always been intrigued by the standards of care adopted by the CFP Board and affiliates.

As I understand it, which could be incorrect, a CFP designated individual is held accountable to the adopted “fiduciary standards” as applied to each of the educational components or disciplines that comprise the CFP designation curriculum.

Speaking candidly, I have yet to meet a CFP who is qualified to serve his or her client’s best interests in all aspects that comprise a “financial planning” engagement. To do so effectively would require a client engagement document that would fill volumes with various disclaimers and exceptions regarding the CFP’s actual skill competencies and areas of demonstrable expertise.

Am I missing something here?

Thank you.

David F. Sterling, Esq., Consultant

David,

You have a fair point here. Strictly speaking, an “unlimited scope” engagement of “we help you with everything financial planning” is almost certainly going to fail some aspect of a strictly enforced fiduciary standard in the long run. Virtually all other professions are very active about properly limiting the scope of an engagement. Arguably that’s overdue in financial planning, but an area I suspect we’ll see refinement in the coming decade as financial planning continues its rise (or the issue will get forced with consumer complaints of planners who didn’t talk about such-and-such and the planner claiming it was outside their undocumented scope…).

– Michael

You raise two separate issues in your comments. On the first, Standard of Care, your argument echoes the DOL Fiduciary position in part and with all due respect — adopts the same premise by ignoring that if you are a Series 65 license holder, you are a fiduciary whether or not you have your CFP. Some make the mistake that the fiduciary aspect only applies to AUM. As you know, it does not! As an aside, if the DOL/SEC/Financial Planning Coalition really wanted to move everyone to a financial fiduciary standard, they could have simply have reworked the licensing (which they really shouldo anyway) and adopted a combo 6/65 & 7/65. In fact, NASAA polled on the issue of reforming licenses in early 2015 but never really went anywhere with it. But for the DOL, is was implementing FinCare (sort of an ObamaCare for our industry) by using ERISA and 401k’s to fly under the radar to reform the industry to force fee only and eliminate commissions, except if you are insurance licensed only, meaning you will get a pass, once again, for selling securities in the guise of Equity Indexed Annuities, which is the premise of Sen Warren’s push for the DOL rule, and her report – trashing the industry for trips and awards when it really relates to….wait for it….Equity Indexed Annuities.

As to the second issue, that’s a little sticky. As you are no doubt aware, FPA has gone back and forth as to whether or not to be inclusive or exclusive to just CFP’s over the last two decades. The stickiness comes in several aspects. a) Not all CFP’s practice financial planning as a whole but many focus in on just AUM adding to a misunderstanding by the public as to fully defining financial planning, b) state chapters of professional associations such AMA, Bar and Accounting providing “financial planning” through retirement accounts (see “a”) adding to the confusion, c) the designation ChFC, d) confusion heaped upon the industry and public by allowing JD’s and CPA’s to test out, and e) confusion in the past by CFP practioners (I refuse to use the ridiculous term “certificant”) over how to actually perform financial planning prior to the capstone course, f) Ongoing confusion by practitioners that financial planning encompasses a projection of growth by assets, and a regurgitation of facts from a software printout and then grab AUM.

Complicating the equation further, in the past, 2/3 of FPA’s membership has been BD affiliated with the remaining 1/3 RIA only. Not all CFP’s sign up for the FPA, and less than 15% (probably increased since CFP test change, this is an older number) of the financial services industry is even a member. In my opinion, if CFP is to be the de facto standard — regardless of a practitioner’s focus — then we need to be inclusive.

As a former two term non-CFP Chapter President, who was elected by Board acclamation comprised of CFP’s, I promoted the CFP standard before, while President, and since, and have seen the effect of inclusiveness lead to more CFP’s while exclusivity pushes people away and hurts promoting the standard.

Finally, thanks for tackling this issue. I always enjoy your comments, wit and wisdom! Regards….

By the way, if we are to truly revolutionize the industry — the first step has taken place. CFP as a course of study at universities across the United States. The second step is in process, a model rule from NAIC causing a loss of insurance license to those who lose their securities license. Three, overhaul securities licenses – combining the aspects of 62/6/65 and then, 7 with 65. Four, overturn that portion of the Dodd/Frank that allows insurance license only to sell Equity Indexed annuities. And finally, move to one combined license of insurance and securities with 65, or 65 only.

The FPA, in trying to fuse sales people and professionals into one organization (Merger of ICFP and IAFP) has come to represent neither. I think we should give it to the salespeople and all head to NAPFA.

Well, while NAPFA is a much smaller organization overall, it is worth noting that NAPFA has nearly doubled its registered advisor account since the FPA merger, while FPA itself has membership down ~20% from the merger days (and despite the fact we’ve added 10s of thousands of CFP certificants along the way)…

Though ultimately, I have to admit that multiple membership associations, all representing “financial planning”, is duplicative and probably untenable in the long run… one, or the other, will be forced to reinvent to differentiate.

– Michael

Michael, as much as I respect you, I could not possibly disagree more. Granted that the FPA lacked an enforcement mechanism, but the FPA has never been nor has it ever presented itself as a regulatory organization. It still remains, though, the principal professional organization for financial planners. Thus, it’s lack of enforcement is no more relevant than saying that a fish cannot fly.

Whenever I met with regulators and legislators on behalf of FPA and the Chapter I would always introduce us by saying that there were only two things you had to do to join and they were to pay the dues and to agree to abide by our Standard of Care. Now we are down to pay the dues.

The CFP Board will be the first to tell you (when it’s convenient) that they are not a membership organization. They are a certifying body. The FPA is, and has been since its inception the principal professional organization for financial planners. Granted that the Standard of Care was aspirational, but it was far stronger than the CFP Board’s or anyone else’s. It had no exceptions, no equivocations. Aspirations are not irrelevant, though. They help to define who we are. This is yet another sad step in the self inflicted decline of the FPA into becoming nothing more than the mere booster club for the CFP Board.

David,

Requiring financial planning members to have CFP certification and be in good standing with the CFP Board is not a step down for the FPA’s Standard of Care.

It’s a step UP. It goes from being an empty aspirational standard, to one that has an actual oversight and enforcement process. “Pay the dues and abide by our unenforced standard of care” was/is inferior to “Pay the dues and be a CFP certificant in good standing with the CFP Board.”

And now as the CFP Board’s enforcement process continues to improve, SO TOO WILL THE FPA’S in the process.

At least, once the FPA finally is willing to say that a financial planning professional should actually have the CFP marks to be a professional, which remains a significant gap for their proclaimed vision of building a profession…

– Michael

Michael,

But the FPA does not require members to have CFP certification, not that I would agree that such a requirement would be a good thing. We can support it, endorse it as the highest standard, but why would we want to require it as a condition of membership?

Moreover, the CFP Board’s Standard of Care is far weaker than the former FPA Standard of Care since it is far more equivocal. Yes it has its enforcement process, problematic as it may be, but there is nothing “empty” about an aspirational standard. It defines who we are. Nor is there any need to choose. Why not let the CFP Board have it’s regulatory minimum Standard of Care and the FPA have a higher aspirational Standard of Care?

Even if lacks the pretense of a regulatory structure, how is it a step up to forgo a broad based aspriational standard that defines who we are, to nothing more than a statement that we expect you to be in compliance with any and all applicable regulatory entities? That is simply dropping from a higher statement of who we are to the minimalist requirement of minimum compliance with all applicable regulations.

Finally, why are we assuming, as you seem to, that the FPA should develop an enforcement process. Why on earth would we want to become a regulatory organization? Shouldn’t we be aiming higher than that?

David,

If the FPA did a brilliant job with its aspirational standard, such that it became known across the country as THE LEADING place for financial planners… and then attracted 20,000 low-quality annuity salesmen who used and promoted their FPA membership as the means to sell 20%-commission annuities… what is the FPA supposed to do when it has no means to enforce membership standards or remove members for failing to enforce them?

Claiming a high standard and failing to enforce it is an inevitably self-destructive path. It either fails outright, or it succeeds to the point that it attracts low-quality players who subsequently destroy the brand the organization may have spent years trying to build. :/

Simply put, it’s an unsustainable path. It might work in the short run, but it’s simply not feasible in the long run. Which I’d argue has ALREADY been the case for FPA, and helps to explain how in the past 15 years, the number of CFP certificants has gone from 35,000 to over 70,000, yet the number of FPA members has DECLINED from 28,000 to 24,000. It’s already failing.

– Michael

Michael,

The FPA never undertook that kind of a campaign, but if it had then I would agree that would be a serious mistake. But it is not the FPA that launched a public branding campaign and then followed up with a deeply flawed enforcement program. That distinction fell on the CFP Board. It is the entity whose brand is at risk with a Standard of Care so filled with equivocation and a deeply flawed enforcement program that come far closer to the scenario you outlined

Don’t get me wrong, my commitment to the CFP mark is demonstrated by 15 years of teaching the program, but commitment to the mark does not require that we disregard the failings of the CFP Board.

The FPA has never presented itself as a regulatory entity and so it’s failure to apply an enforcement program it never claimed to have doesn’t seem to pose a serious threat. Nor has it engaged in the kind of marketing program toward the public that would generate the kinds of negative branding consequences you mention.

But requiring each member to certify that, without equivocation or exception, they will always put their best interests ahead of their own, that they will always act in utmost good faith, that they will fully and fairly disclose all conflicts of interest, is valuable in that it tells that member what it means to be a financial planning professional and a member of the principal professional organization of financial planners and what his/her fellow members are entitled to expect of her/him.

David,

If the FPA believes that the CFP marks are the basis upon which the profession should be built (which they’ve publicly stated), and that the CFP Board’s enforcement has been problematic (as many have noted), then the conclusion is not for the FPA to dump the CFP marks.

The conclusion is for the FPA to ADVOCATE ON BEHALF OF CFP CERTIFICANTS to get the rules fixed. Exactly the way they would if the SEC or FINRA passed a problematic rule that impacts financial planning professionals.

The FPA is not a regulatory body. It’s an advocacy organization. It advocates to many regulators, including suing them (the SEC).

Why can’t the FPA advocacy on behalf of CFP certificants to push for improvements at the CFP Board? How is that anything less than fundamental to their mission?

Or viewed another way – if you believe that FPA’s standard of care was the “right” standard of care, then why isn’t the NUMBER ONE OVERRIDING ADVOCACY GOAL OF THE FPA to have that standard of care enshrined into the CFP Board’s Standards of Professional Conduct and be enforced as such?

– Michael

My only exception with what you have said here is that I, for one, have never advocated for dumping the CFP mark. As I mentioned above, I have spent 15 years teaching students so they could become CFPs.

But yes, a true professional organization should be advocating for a broad, principles based standard of care that does not equivocate and does not provide for “hat switching” — a standard of care exactly like the one the FPA has now abandoned.

Since the FPA has never presented itself as a regulatory organization, it’s lack of a regulatory mechanism is not material. The fact, though, that it, as the professional organization, required each member as a condition of membership to acknowledge that this is the appropriate Standard of Care for all financial planners at all times had put the FPA in a position to advocate to the CFP Board as well as any state or federal regulatory agencies for it to be the appropriate standard of care for ALL Financial Planning Professionals.

Wouldn’t that be better than taking the position that “we really don’t think our members should be in violation of anybody else’s requirements.”?

David,

You realize the CFP Board’s standard for CFP certificants doesn’t allow this kind of hat-switching either? Once a CFP “does” financial planning, they’re bound to a fiduciary standard, with all the elements that the FPA’s standard had.

Functionally, the only difference between the standards was that FPA’s applied upon joining, while the CFP Board’s only applied once you actually DID financial planning.

But both applied a comparable level of fiduciary standard for anyone actually delivering financial planning services to the public (with the caveat that the CFP Board actually has at least some means to enforce it).

That aside, I still think you’re missing the fundamental problem with FPA’s standard. Someone could join the FPA, sell a 91-year-old grandmother an annuity with a 20% commission and a 20-year surrender charge, while advertising that they were a member of the Financial Planning Association and its high consumer-centric standards. That’s a blatant violation, but without any means of enforcement, there was nothing to stop salespeople from blatantly abusing the FPA’s standard until its brand was destroyed. (Which is exactly what the board realized and acknowledged in eliminating the standard – it’s a public relations disaster waiting to happen.)

– Michael

Michael,

And yet the difference between the CFP Board’s standard an the FPAs is that the former get’s into the weeds of whether or not one is doing financial planning while the latter applies to the individual member. I understand that the CFP Board has commercial reasons for imposing its limitations, but that does not mean that the FPA should abandon it’s higher standard.

As for the the public relations disaster, I guess I just don’t see it. Anything can be abused so the fact that someone could abuse their membership in FPA shouldn’t shock anyone. You and I both know that every day there are CFPs, FPA members, NAPFA members, who are abusing their memberships. Does that mean that we should abandon our standards just because we cannot force everyone to comply with them? I see that as a larger problem for entities that claim an enforcement mechanism. than for ones that don’t.

David

This is an interesting and important topic. Thanks for bringing this to our attention. By the way, this kind of discussion is one of the reasons I follow your blog. Awesome content! Regarding FPA, when I was going into private practice 1.5 years ago (leaving the brokerage industry) I new I wanted to join NAPFA because I was starting a fee-only practice. I looked at FPA hard and opted to just join NAPFA because FPA seemed, well, different from NAPFA. I want to support the FPA and am going to their conference in SF this year because I cannot attend NAPFA’s due to a schedule conflict. But I don’t understand, as you say, how FPA could admit non-CFPs to it’s ranks at all. I mean, if we’re trying to legitimize the profession of financial planning we need very clear guidelines about who is, and who is not, a financial planner. Personally I don’t think someone can hold themselves out as a “planner”, or even “advisor”, unless they act in their client’s best interest, and are legally held to such a standard (not able to disclaim it away on page 79 of a 121 page disclosure doc). We should come up with another name. Maybe “financial consultant” if “securities salesperson” seems too harsh. So a question: Does this mean you’re not presenting at FPA Norcal this year? : )

Tahoediver,

Yes, I will still be presenting at FPA NorCal. And I am still a due-paying FPA member.

I don’t raise issues with the FPA as a non-member to throw stones at them. I advocate for the FPA to adhere to a higher standard because I am an FPA member, and want to be proud of the membership association to which I belong!

– Michael

That makes sense to me. Happy to hear it. Maybe I’ll join as well.