Executive Summary

From the rapid growth of goals-based financial planning software like MoneyGuidePro, to the recent announcement that even legendary wirehouse Merrill Lynch will be focusing on a goals-based planning approach, financial planning is on the rise, and is increasingly focusing around an approach of identifying and understanding client goals, and then crafting a plan to help the client succeed in achieving them.

Yet at the same time, the reality is that in practice the goals-based approach doesn't always go as smoothly as hoped. Some clients haven't crafted their goals yet in the first place, while others have goals that are wildly unrealistic and force planners to be the bearers of bad news. Often the goals-based planning process can get mired down in countless iterations of alternative "what if" plans, culminating in a giant physical tome that clients aren't committed to and is never read again after being presented away.

But perhaps the fundamental problem with goals-based planning is simply that it puts the cart before the horse; clients shouldn't be selecting the goals to pursue until they understand what the possibilities are in the first place! Which means in turn, perhaps the best thing that can be done with financial planning software is not use it as an analytical tool to craft a plan to achieve hypothetical goals that may or may not even be realistic, but instead to use the software interactive with clients to explore the possibilities of multiple scenarios and understand the trade-offs just to arrive at what the goals should be in the first place. Once the possibilities have been selected, realistic goals can be chosen, and then a more productive series of financial planning recommendations can be delivered for implementation!

The inspiration for today’s blog post are some additional thoughts I've been having regarding a recent book I read, entitled “Scenario Selling: Technology and the Future of Professional Selling” by former advisor and entrepreneur Patrick Sullivan and psychologist Dr. David Lazenby. As I've written in the past, don't be fooled by the books "selling" title; it presents some powerful ideas about how to better deliver financial planning advice to clients. In particular, the book highlights that despite its increasing popularity, the goals-based planning approach may actually be fundamentally flawed.

The inspiration for today’s blog post are some additional thoughts I've been having regarding a recent book I read, entitled “Scenario Selling: Technology and the Future of Professional Selling” by former advisor and entrepreneur Patrick Sullivan and psychologist Dr. David Lazenby. As I've written in the past, don't be fooled by the books "selling" title; it presents some powerful ideas about how to better deliver financial planning advice to clients. In particular, the book highlights that despite its increasing popularity, the goals-based planning approach may actually be fundamentally flawed.

The Problem With Goals(-Based Planning) – Not Knowing How Big To Dream

For some clients, a goals-based planning process is relatively easy; the clients come in with the details of what they have, where they want to go, and it’s pretty clear how to craft a plan to get them from here to there. They know when they want to retire, where they will live, what they will spend, and their current assets and savings are on track enough that there aren’t any hard conversations and trade-offs necessary, just a series of tactics to implement to get to the goal.

For other clients, though, the process gets bogged down quickly. When asked “what are your goals” the answer is “well, we don’t really know.” They’ve never really thought about it before. Or worse, there are some goals, but the goals are so wildly inappropriate for the resources (assets, income, and ongoing savings) they actually have, that they’re totally unrealistic. At best, crafting a plan is just going to project a catastrophic failure and require a sit-down with the client to come up with a second plan instead that has new, more realistic and feasible goals.

This situation – where some clients have realistic goals and easy plans to craft, while others have unrealistic goals that can’t be achieved with any feasible plan – is perhaps not entirely surprising, though. By analogy, imagine trying to take a long trip in an airplane. It’s not enough to just say “where in the world would you like to go?” Because there’s only so much fuel in the plane, and even with the tank topped up there’s only so far the plane can possibly go given its weight, and there may only be a little bit of wiggle room in the amount of weight that can be shed. In addition, there could be storms somewhere between “here” and “there”, which means the trip will be bumpy at best, or at worst require a workaround (or rather, a fly-around-the-storm), which in turn will just burn more fuel and reduce the range even further.

As Sullivan and Lazenby point out, what this means is that in the end, it doesn’t really make sense to ask “where in the world would you like to go” until you survey the situation, figure out “where in the world can we go, given the plane/fuel and current weather conditions” first, understand the possibilities, and only then decide where to go once it’s understood what is feasible. And in a similar manner, arguably it really doesn’t make sense to just ask clients what their goals are, until they first understand what possibilities are feasible to begin with. In other words, whether it’s flying a plane or charting a path towards retirement (or some other goal), a client can’t decide where they’d like to go until they first know where it’s possible to go first. We just don’t know how big to dream.

Turning Around The Financial Planning Process And Putting Possibilities Before Goals

From the financial planning perspective, this challenge to goals-based planning raises an interesting question: what would it look like if we explored the possibilities first as Sullivan and Lazenby suggest, and selected the goals second (and then crafting the plan comes third thereafter!).

Fortunately, possibilities are something we can evaluate. We have the data to know where the client is today (current assets), and to understand their current trajectory (current income and savings). We can discuss and explore what kinds of adjustments can realistically be made to the path they’re on; how much more could they really save (or not) by changing spending, would it be possible to put in more hours at work and get a raise, how flexible is the retirement date, would it be acceptable if the kids took on student loans for not all but at least some of their college expenses?

With this initial framework, clients can explore the possible scenarios. What would happen if they just stayed on their current path? What if they really did trim current spending a bit to save a little more? How would the projections change if the retirement date is moved, or the allocations are shifted further towards or away from the college goal instead? Does a higher growth rate assumption actually help, or does the additional risk do more harm than good? By looking at the various scenarios, the client can evaluate what is realistically possible and not, as well as understanding which assumptions are really driving the plan and which changes have the most leverage to impact the outcome.

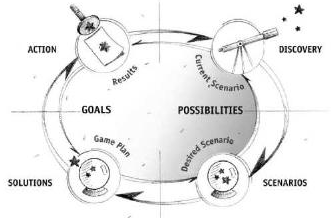

Examining the various scenarios to look at the realistic possibilities – just like assessing the fuel, weight, potential range, and looming weather for our prospective flight – gives the client an understand of what are FEASIBLE, REALISTIC goals in the first place. And THEN the client is better equipped to choose from amongst the goals, prioritize which are most important, evaluate the alternatives to get there, and make choices about which to pursue and which trade-offs are acceptable, and in the process crafting a real, actionable plan with the advisor to get there. Or as Sullivan and Lazenby envision it in their book:

Source: Scenario Selling: Technology and the Future of Professional Selling by Sullivan & Lazenby

Financial Planning Software As A Scenario Learning Tool

So as financial planners, how do we facilitate the Sullivan and Lazenby approach of visioning of possibilities with a client? By using financial planning software not for goals-based planning, but to collaboratively explore possibilities-first scenarios and learn from them.

Ideally, then, financial planning software should allow for clients to quickly change amongst and adjust scenarios, to find where the leverage points are, and see what works and what doesn’t. In this environment, the role of the planner is as collaborator, to help explain/interpret possibilities, the trade-offs they entail, and put context to what’s feasible and what’s not.

Notably, though, this isn’t just about crafting a plan with several “what-if” scenarios. For many (most?) clients, real world financial planning is too complex; when clients don’t know what the possibilities are in the first place, you’d be stuck making 47 different plans just to show them the range of potential outcomes. Consequently, it’s far easier to just use the software interactively, and let them see how the scenarios change with adjustments on the spot. What might have been pages and pages worth of printed plan alternatives can be evaluated with a few tweaks to a slider, and the client can quick evaluate which possibilities are relevant and which are not, and make a real commitment to which they wish to pursue.

Unfortunately, not all financial planning software is capable of doing this effectively; the tools themselves can be so complex that many planners would be afraid to use the software live and interactively with clients for fear of making a software mistake (though in recent years, a number of software packages have become somewhat better!). Nonetheless, along with writing their book back in 2006, Sullivan and Lazenby ultimately created their own years ago, called ScenarioNow, specifically to help facilitate the process of clients evaluating multiple scenarios. And fortunately, in recent years big screen televisions had gotten so much less expensive it really is feasible to put them into every conference room (as this process wouldn’t be nearly so appealing if everyone was crowding around an old 15” monitor!).

The bottom line, though, is simply this: the traditional goals-based planning approach can actually be very problematic when clients don’t understand what goals are possible in the first place, leading to a slow arduous process with lots of questions and lots of alternative plans and what-if scenarios, that are just slowed even further if the planner has to go back to their computer and run new analyses and schedule new meetings with the client just to talk through the “new” results. In other words, it’s hard to analyze goals and craft a plan when clients aren’t certain they’ve selected the “right” goals in the first place! By contrast, when the planning process starts by helping clients to just explore the possibilities – using financial planning software as a collaborative tool to test multiple scenarios and evaluate the trade-offs – and then select the goals with an understand of which are realistic and feasible in the first place, it’s far more practical to move on to the next step where the planner can figure out the best path to help clients achieve what they wish and then implement what’s necessary to get there!

And in the meantime, for those who want a deeper understanding of what possibilities-first scenario learning is all about, I do highly recommend getting a copy of Sullivan and Lazenby's book!

So what do you think? Viewed in this manner, are there “problems” with traditional goals-based planning? Is a possibilities-first scenario approach a better way to help clients figure out their own path to success?