Executive Summary

Trusts have been used in estate planning for decades as a way for individuals to ensure that their assets are distributed according to their wishes after death. Not only do trusts give owners more flexibility to specify how their assets are distributed upon their death (relative to a simple Will, for example), but strategies using trusts can also reduce the potential income, gift, and estate taxes associated with those assets (thereby allowing heirs to benefit more from the assets left to them). And while numerous trust strategies exist for individuals, many of the most popular strategies have historically revolved around the use of Grantor Trusts.

However, the recently proposed “Build Back Better” reconciliation bill currently under debate in Congress has targeted the use of Grantor Trusts, particularly because of how they are used by wealthy individuals to transfer assets – free of estate taxes! – to their heirs. The bill’s text, released by the House Ways and Means Committee on September 13, 2021, proposes major changes to how assets in Grantor Trusts are treated for gift and estate tax purposes, such as making all Grantor Trust assets includable in the Grantor’s estate, treating transfers between a Grantor and their trust as a gift or sale rather than a disregarded transaction, and treating transfers from the trust to anyone other than the Grantor during their lifetime as a gift. As a result, Grantor Trusts that are frequently used in many estate planning strategies – including Grantor Retained Annuity Trusts (GRATs), Intentionally Defective Grantor Trusts (IDGTs), and Spousal Lifetime Access Trusts (SLATs) – could be seriously impacted or eliminated altogether!

Importantly, for individuals and families who can benefit from these strategies, the proposed bill would only apply to new trusts created after its enactment. Which means that there is still a (very limited!) window of opportunity between now and the bill’s enactment (which can happen anytime in the coming weeks or months) to implement Grantor Trust strategies. Additionally, the Build Back Better legislation would also reduce the taxable estate exemption by 50% (to $5.85 million for individuals, and $11.7 million for couples), meaning that strategies such as Grantor Trusts that currently remove assets from one’s taxable estates could be newly relevant for individuals and families whose assets fall between the old exemption amount and the new, lower one… but because of the proposed changes to Grantor Trust laws, those who can benefit from such strategies only have between now and the date of the bill’s enactment to decide on a strategy and to create and fund a trust!

Ultimately, while the proposed bill would not impact Grantor Trusts already in place, it would place significant limitations on implementing new strategies and leave existing ones with less flexibility to change course. And even though the bill has several steps to take before becoming law, the potential significance of its impact combined with the limited amount of time before its provisions take effect means that the time to plan (and act on!) any Grantor Trust strategy is now… because letting more time elapse between now and the bill’s passage risks running out of time and needing to start from scratch with fewer options!

On Monday, September 13, 2021, the U.S. House of Representatives Ways and Means Committee released its markup of the proposed revenue raisers (i.e., tax increases) to fund President Biden’s broader “Build Back Better” initiative. While much of the focus since then has been on the proposed legislation’s impact on income taxes, the draft legislation also contains a number of provisions that, collectively, would create a seismic change in the estate planning world.

With respect to estate planning, the headline provision in the proposed legislation is an acceleration of the sunset of the Tax Cuts and Jobs Act’s doubling of the estate and gift tax exemption. Currently, the exemption is an inflation-adjusted $10 million ($11.7 million in 2021) through 2025, at which time it is scheduled to revert to its pre-Tax Cuts and Jobs Act level of an inflation-adjusted $5 million. The House bill would accelerate that change from 2025 to 2022, leaving individuals with ‘only’ a (roughly, after inflation-adjustments) $6 million exemption amount, and married couples with about $12 million in total exemptions.

Such a change would subject far more households – including those who are more likely to work with a financial advisor – to a potential estate tax liability (even though the percentage of total U.S. households that would owe such a tax would continue to be relatively low). For instance, in a study released earlier this year, the Spectrum Group found that while in 2020 there were ‘just’ 214,000 U.S. households with total wealth (excluding their primary residence) of more than $25 million, there were roughly 1.8 million households with wealth between $5 million and $25 million!

But that’s not all. To make matters worse for potential households caught in the proposed lower exemption amount’s ‘crosshairs’, many of the strategies that such families could otherwise use to reduce the value of their taxable estate are also under fire. Such proposed changes include substantial revisions to the Grantor Trust rules that would reduce, or eliminate entirely, the benefits of many trust-driven estate tax planning strategies.

The Current Role Of Grantor Trusts In Estate And Income Tax Planning

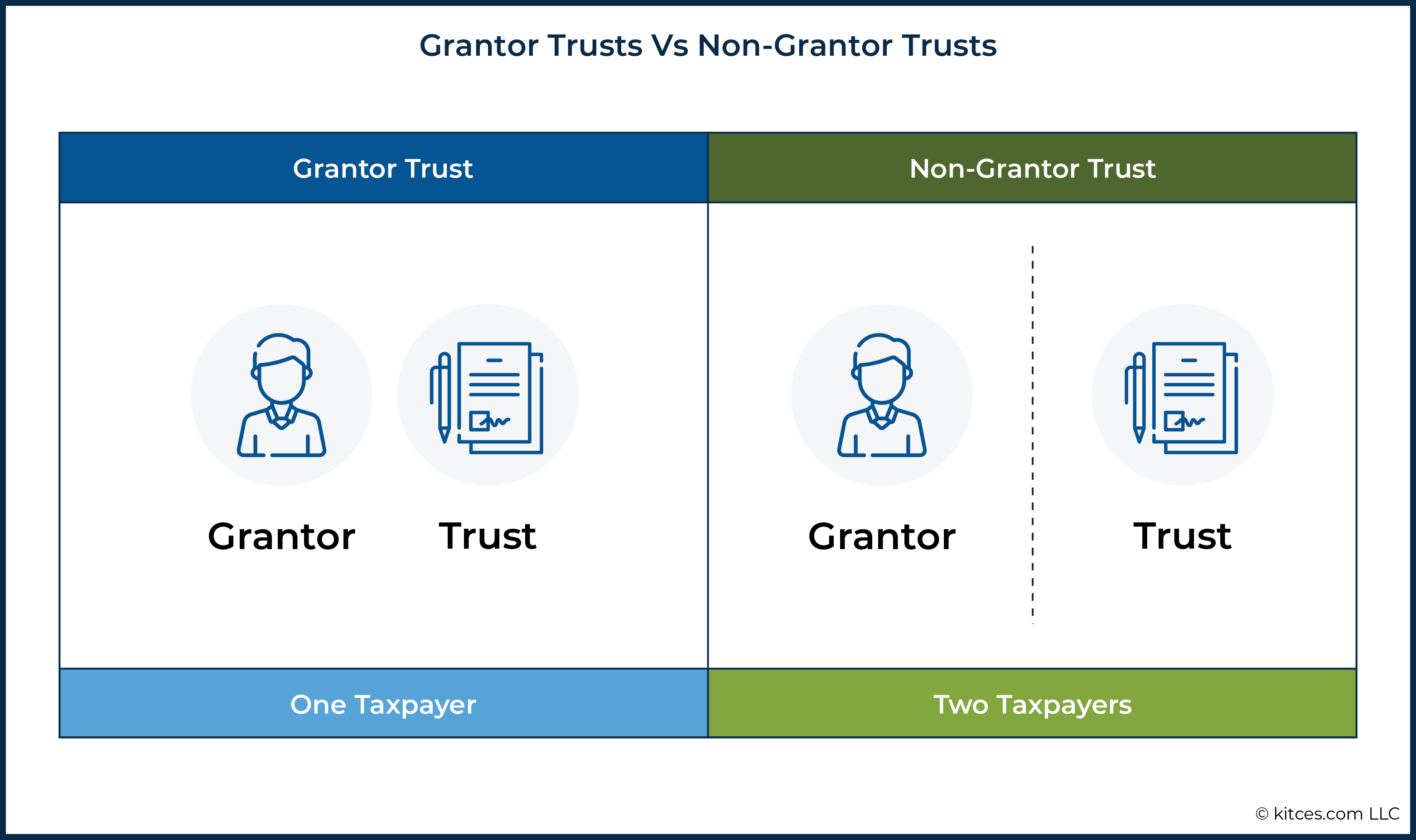

For decades, Grantor Trusts have been a vital part of many estate plans. At a high level, the defining feature of a Grantor Trust is that, for income tax purposes, the trust and the Grantor (the creator of a trust) are viewed as one and the same. Essentially, the income of a Grantor Trust, along with any deductions or credits, flows up to the Grantor and is reported on the Grantor’s personal income tax return.

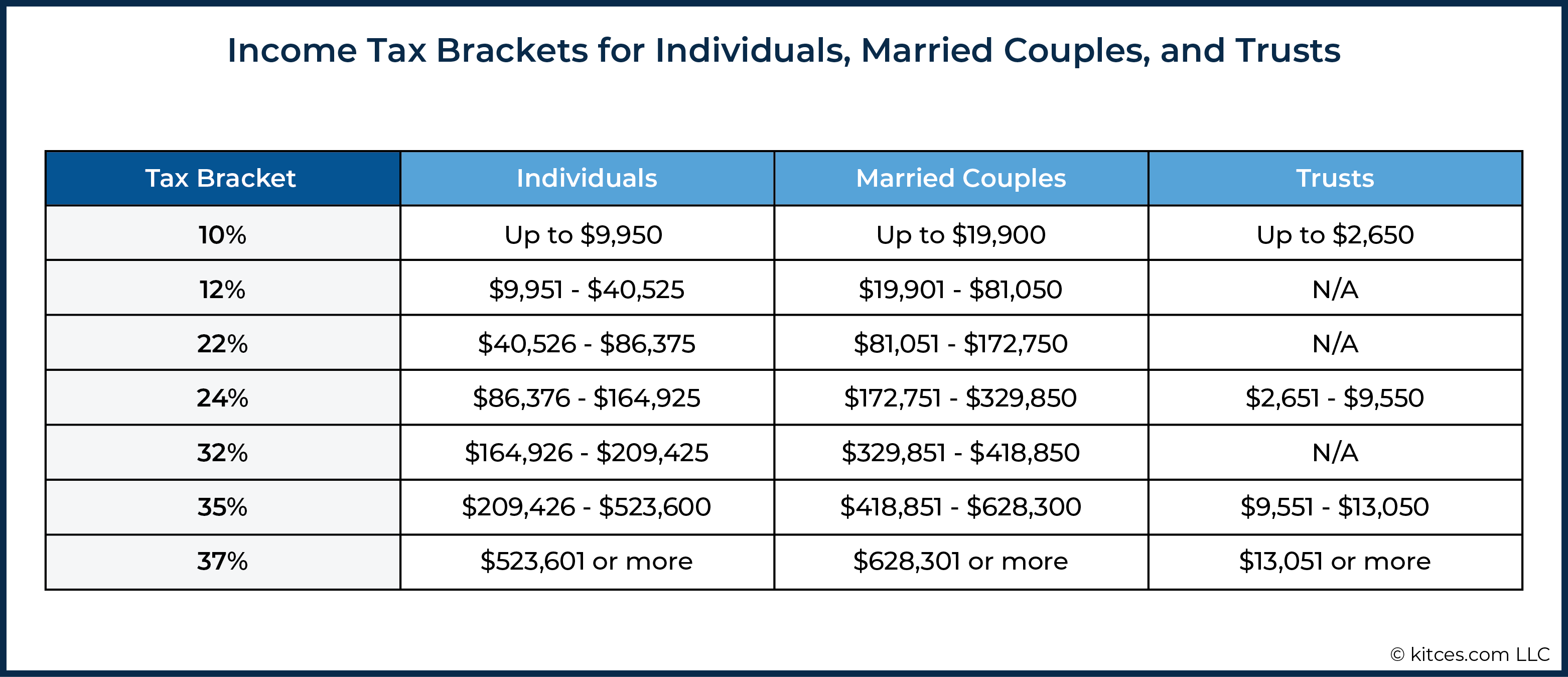

This treatment can provide a number of potential benefits. One benefit is that, compared to the income tax brackets for individuals (e.g., single filers, joint filers, etc.), the income tax brackets for trusts are substantially compressed. For instance, in 2021, the top ordinary income tax bracket of 37% kicks in for trusts once they have more than $13,050 of taxable income. By contrast, the 37% top rate doesn’t apply to single filers until taxable income exceeds $523,600, and to joint filers until taxable income exceeds $628,300.

Another potential benefit of Grantor Trusts is that since the Grantor Trust and the Grantor are considered one and the same for income tax purposes, many transactions between the two that would otherwise be subject to income tax do not create a taxable event. For example, under current law, a “sale” of an appreciated asset from a Grantor to a Grantor Trust does not generate any capital gains, as for income tax purposes, there has been no change in ownership.

Finally, a Grantor Trust can be drafted such that even though the income of the trust is still taxable to the Grantor, the assets within the trust are removed from the Grantor’s taxable estate for estate tax purposes. All fully revocable trusts are, by their very nature, Grantor Trusts. But under the current tax regime, certain Irrevocable Trusts can also be structured as Grantor Trusts.

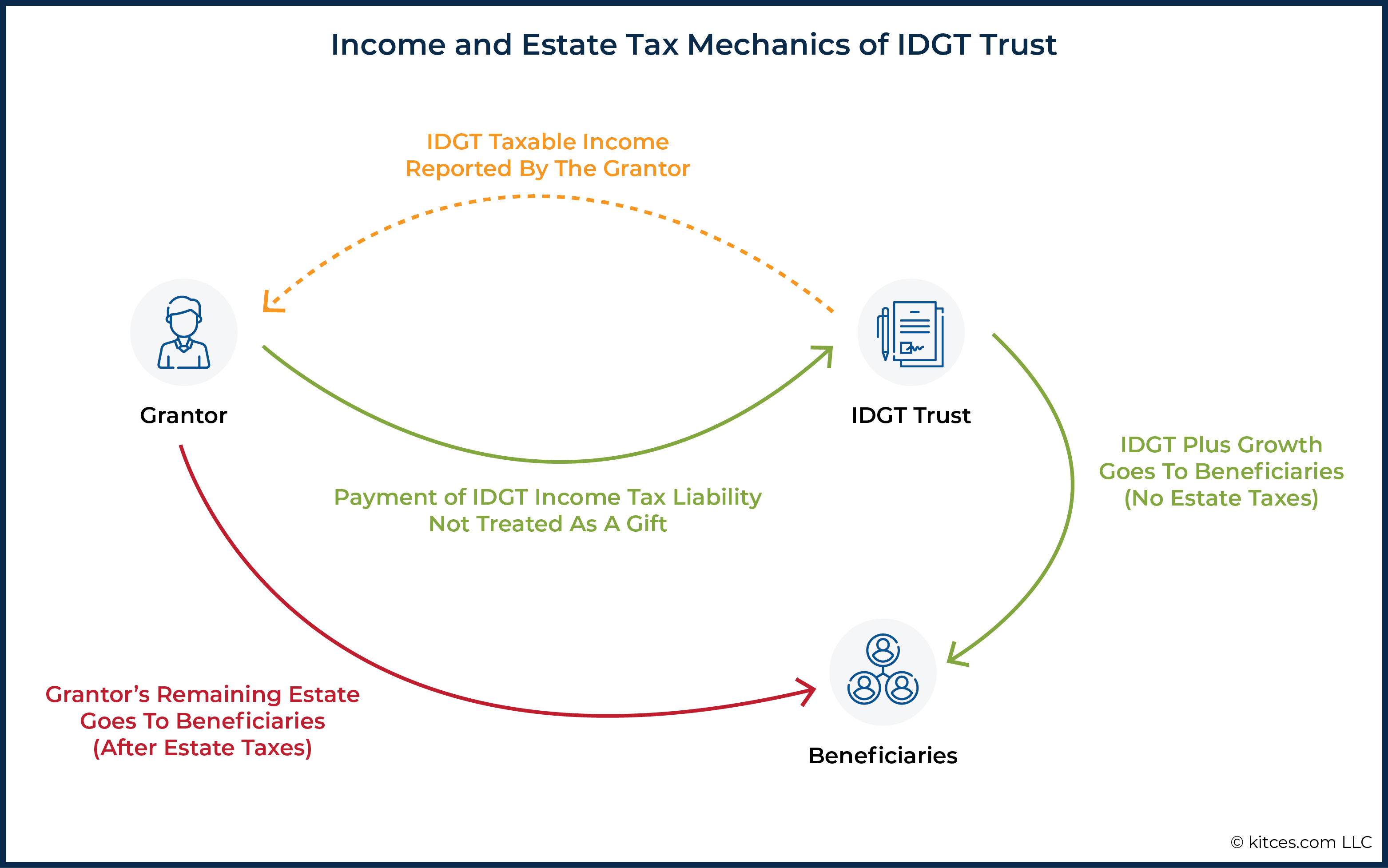

More specifically, through creative planning and careful drafting, planners can thread the proverbial needle and create Grantor Trusts that receive both favorable estate tax treatment (because trust assets have been removed from the Grantor’s Estate) and favorable income tax treatment (because the income generated by the trust is still taxable to the Grantor). Such trusts are commonly known as Intentionally Defective Grantor Trusts (IDGTs) because they are intentionally drafted to run afoul of the rules that transfer the income tax liability generated from gifted assets to the recipient of those assets.

By continuing to personally pay for the income tax liability of trust earnings, a Grantor is able to benefit from both using the individual income tax bracket (as opposed to the much more compressed trust tax brackets) and allow the out-of-the-taxable-estate-already trust assets to grow unencumbered by any income tax liability. At the same time, the tax liability created by the trust’s income is paid for by assets in the Grantor’s estate that may have otherwise been subject to estate tax upon their death!

The hybrid treatment of IDGTs (excluding trust assets from the grantor’s estate and including trust income in the grantor’s income) is made possible because, under current law, the rules for making a Completed Gift (which removes an asset from one’s estate) for estate and gift tax purposes do not precisely align with the rules for transferring the tax liability associated with the income generated by such transferred assets.

Thus, it is possible to create a trust that receives an irrevocable gift, removing the gifted asset from the Grantor’s estate for estate tax purposes, but where some sort of retained power, as outlined in IRC Sections 673 – 677 and/or IRC Section 679 cause the income of the trust to be taxable to the Grantor.

Popular so-called ‘triggers’ to keep Grantor Trust status include retaining the power of substitution, the ability to borrow trust assets without sufficient security, allowing income to be distributed to the Grantor’s spouse without the consent of an adverse party, the ability to add beneficiaries to the trust, and the ability to use the income of the trust to pay life insurance premiums of a policy for which the Grantor or their spouse are the insureds.

Proposed Changes To The Grantor Trust Rules

For years, many in Washington (and beyond) have looked at the potential benefits of Grantor Trusts described above as loopholes that have allowed the wealthy to avoid paying their fair share. And so, in an effort to limit, if not outright eliminate, these loopholes, the Ways and Means Committee’s proposed legislation includes a number of provisions that take direct aim at a variety of commonly employed Grantor Trust planning strategies.

Specifically, Section 138209 of the Ways and Means Committee’s proposal would amend “Subtitle B - Estate and Gift Taxes” of the Internal Revenue Code by creating a new Chapter, “Chapter 16 – Special Rules For Grantor Trusts.” Changes to the Grantor Trust rules made by that Chapter would include the following:

- Grantor Trust assets would be included in the value of the Grantor’s gross estate [Proposed new IRC Section 2901(a)(1)];

- Distributions would be treated as gifts when made during the Grantor’s lifetime from a Grantor Trust to individuals other than the Grantor and/or the Grantor’s spouse [Proposed new IRC Section 2901(a)(2)];

- If a Grantor Trust becomes a Non-Grantor Trust during the lifetime of the Grantor, the assets of the trust shall be considered gifted by the Grantor to the Non-Grantor Trust at that time [Proposed new IRC Section 2901(a)(3)]; and

- The Grantor and the Grantor Trust would be treated as separate taxpayers with respect to “any transfer of property” between them [Proposed new IRC Section 1062 (old IRC Section 1062 would become IRC Section 1063)].

Collectively, these changes spell varying levels of doom or disruption to a host of different Grantor Trust planning strategies. Just as critical, Doomsday could be soon. Very soon.

Section 138209(c) of the draft legislation would set the effective date of these changes as of the date of enactment, which could be as early as a few days (unlikely), weeks (more likely), or even (a few) months from now. Which means that any trust created on or after the date of enactment would be subject to the new, much more restrictive Grantor Trust rules. Additionally, any portion of an existing trust (in existence before the date of enactment) that is attributable to contributions made on or after the effective date would also be subject to the new rules.

So, simply put, there may be an extremely limited window of time in which individuals can create, execute, and fund various kinds of Grantor Trusts that could help reduce a future estate tax liability under the current rules, but would be impacted by the proposed changes.

Grantor Trust strategies that would be impacted include Grantor Retained Annuity Trusts (GRATs), the aforementioned Intentionally Defective Grantor Trusts (IDGTs), and Spousal Lifetime Access Trusts (SLATs).

And critically, if any final legislation does cut the estate and gift tax exemption in half beginning next year, as is currently being proposed, a lot more taxpayers would be in need of looking beyond just their estate tax exemption amount to try and minimize and/or eliminate such tax liabilities for their heirs.

Grantor Retained Annuity Trusts (GRATs) Would Be Rendered Essentially Useless By Proposed Changes

For roughly three decades, Grantor Retained Annuity Trusts (GRATs) have been a powerful tool in the estate planner’s arsenal and a preferred method for many ultra-high-net-worth taxpayers trying to shrink their estate tax liability. In fact, a recent ProPublica article suggests that more than half of the 100 wealthiest Americans have used GRATs or similar trusts as part of their planning strategy. Given the relative ease with which they can be created and implemented, coupled with their potential benefits, it’s not hard to see why.

Grantor Retained Annuity Trust (GRAT) Overview

The basic Grantor Retained Annuity Trust (GRAT) structure entails a Grantor contributing assets to a trust in exchange for fixed annuity payments over a period of at least 2 years. The fixed annuity payments are designed to be as small as possible, using the IRC Section 7520 rate to calculate the minimum allowable interest rate.

At the same time, the contributions made to the GRAT are invested (or remain invested) in assets that are expected to have high growth during the term of the GRAT. Ultimately, if the Grantor of the trust outlives the term of the GRAT, any growth of the GRAT assets (during the GRAT’s term) that exceeds the minimum interest payments associated with the GRATs annuity payments is shifted out of the Grantor’s estate without estate or gift tax consequences.

It should be noted that one of the most powerful aspects of GRAT planning is that they can be (and often are) structured so that the annuity payments received in exchange for the GRAT are (actuarily) equal in value to the original contribution. These GRATs, referred to as “Zeroed-Out GRATs” (because they use almost zero dollars of the Grantor’s gift tax exemption), can allow even those who have already used up their entire exemption amount to shift massive amounts of wealth (future growth) out of their estate without the impact of transfer taxes.

Example #1: Adam is an ultra-high-net-worth real estate developer. In order to minimize the future impact of estate taxes for his heirs, he has already used the full value of his exemption to gift assets out of his estate. Nevertheless, Adam continues to have significant wealth in his estate and has a new project that he expects will produce substantial returns.

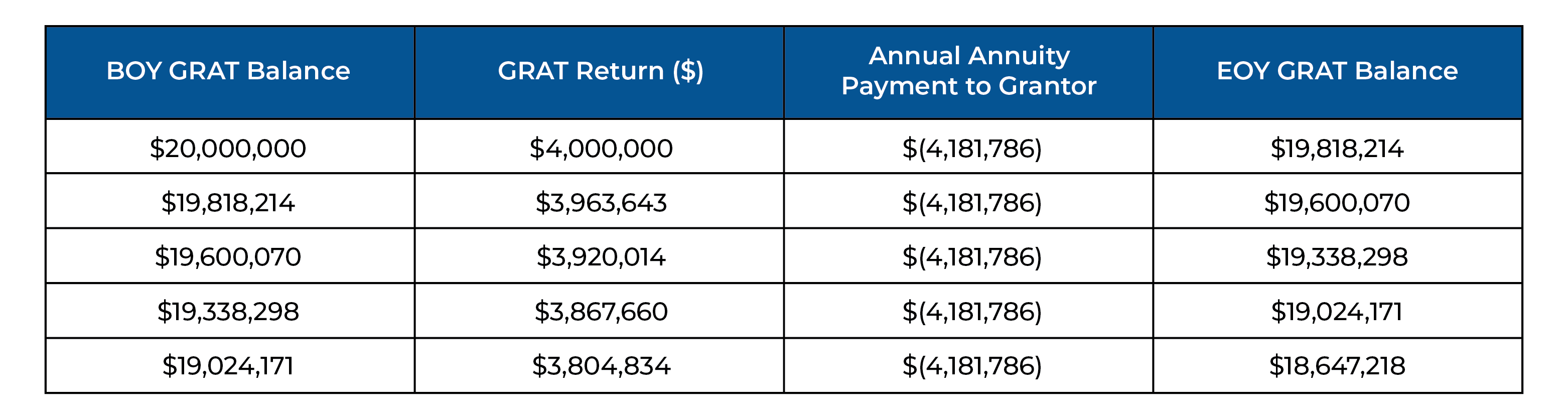

In an effort to further reduce future estate tax liability, Adam makes a contribution of $20 million to a 5-year GRAT, structured as a Zeroed-Out GRAT, and that the $20 million is invested into Adam’s new high-expected-growth project. Based on a hypothetical 1.5% IRC Section 7520 rate, the GRAT would have to pay Adam about $4.2MM annually.

Suppose that Adam was right about his new project and that it turned out to be a huge success, generating a 20% annual GRAT return over the five-year trust term.

In such a circumstance, even after paying Adam his annual payments, the GRAT would be left with well more than $18.5 million! And that $18.5 million would now be outside of Adam’s estate… at a total transfer tax cost of… $0!

Nerd Note:

The calculation of the GRAT’s remaining value is essentially a future value calculation, where the present value is the initial contribution, the growth of the GRAT funds annually (their return) is the interest rate, and the annual required annuity payments are the payments.

Impact Of Proposed Changes On Current GRAT Planning

The newly proposed IRC Section 2901 would render new GRATs utterly useless. In short, at the end of the GRAT’s term, there would be one of two equally useless choices.

On the one hand, the GRAT could be structured so that the remainder beneficiary (the person or entity to receive the remaining GRAT value after all annuity payments have been made) is a Grantor Trust (but one which is out of the taxable estate of the Grantor). However, because the new proposed IRC Section 2901(a)(1) would include all GRAT assets in the value of the Grantor’s gross estate, using a Grantor trust as a remainder beneficiary for a GRAT would not result in any assets being removed from the Grantor’s estate!

On the other hand, the GRAT could be structured so that the remainder beneficiary is the Grantor’s children, a non-Grantor trust, or other persons. In that case, because the proposed new IRC Section 2901(a)(3) would treat those distributions as gifts made by the Grantor, such gifts would either reduce the Grantor’s remaining exemption amount or, if already exhausted, would create a current gift tax liability. In either case, the Grantor would have been better served to simply make an outright gift.

What To Do Now – GRATs

Given that the proposed changes would be effective as of the date of enactment (likely to be in the coming weeks or months), there still remains a limited window of time in which individuals who can benefit from the use of a GRAT can implement such a strategy.

In this context, it’s important for individuals to consider not just the value of their taxable estate today but rather, what it will, or could be, in the future at the time of their death. That requires thinking about both the potential future growth of their gross estate, as well as the possible (likely?) shrinking down of the estate tax exemption.

Whereas today, many ‘merely’ very wealthy households may have a large enough estate tax exemption to cover their entire net worth (as opposed to those with even more wealth who would be subject to an estate tax even with today’s high exemption amount), the reduction of the estate tax exemption could create future concerns. To date, some individuals who could benefit from the GRAT may have held off on using such an approach with a “maybe-next-year” type of mindset. Unfortunately for them, it now looks like their hand may be forced.

In short, as the great Yoda once said, it’s now “Do, or do not. There is no try.” Individuals who could benefit from a GRAT need to act NOW, to have even a chance at getting such a trust implemented prior to the enactment of any new law. Because even if they’re now on board with the approach and willing to move forward at breakneck speed, there’s no guarantee that they’ll be able to find an estate planning attorney who can move forward at a similar pace!

The Value Of Sales To Intentionally Defective Grantor Trusts (IDGTs) Would Be Annihilated As A Result Of Proposed Changes

Sales to Intentionally Defective Grantor Trusts (IDGTs) in exchange for an installment note are another popular estate planning technique that is used to shift the future growth of highly appreciating assets out of one’s estate. While similar to GRATs in some ways, such installment sales can be preferable for some individuals due to their flexible design (e.g., IDGT installment notes can be set up using balloon payments, whereas GRAT payments must be equal) and their lower interest rates (GRATs use the IRC Section 7520 rate, whereas IDGTs use the Applicable Federal Rate). That said, if the current proposed legislation is enacted, the two strategies would essentially be rendered equally useless.

Sales To Intentionally Defective Grantor Trusts (IDGTs) Overview

As noted earlier, the current rules that govern when an asset has been moved out of an individual’s estate and the rules that govern when the income tax liability created by those assets has been shifted from a Grantor to a Grantor Trust don’t perfectly align. Thus, it is possible to create a trust that is separate and distinct from the Grantor for estate tax purposes, but that is considered one and the same for income tax purposes. The Intentionally Defective Grantor Trust (IDGT) is designed to do just that, allowing the Grantor to exploit that divide.

As mentioned earlier, IDGTs are drafted as irrevocable trusts, which allow the Grantor to remove any assets of the trust from their estate. But at the same time, the trust is drafted to intentionally run afoul of the rules for shifting the income tax liability of the trust assets to the Grantor. By retaining certain powers, such as the power to swap assets with the trust, the Grantor of the trust forces the trust to retain Grantor status.

An individual can then sell an asset they currently own to the IDGT via installment sale in exchange for a promissory note. Similar to the annuity payments of a GRAT, the promissory note payments of the IDGT are structured to be as low as possible (using the Applicable Federal Mid-term Rates). And also similar to GRAT planning, the best assets to sell to the IDGT in this manner are those that have high future expected returns.

Oftentimes, the same assets have already experienced substantial returns (possibly leading to the need for such planning in the first place!). And whereas selling those assets to a third party would create an income tax liability, the sale to the IDGT does not. Since the Grantor and the IDGT are considered the same taxpayer for income tax purposes, the transaction is essentially ignored.

Even better? Since the promissory note received by the Grantor of the trust is considered full value in exchange for the asset that has been sold, the shifting of the sold asset to the trust does not require the use of any of the Grantor’s exemption (though to facilitate the sale, the Grantor generally needs to have first gifted the trust about 10% [or more] of the purchase price of the assets, requiring the use of at least some exemption amount, or the payment of some gift taxes where the exemption has already been used up).

The end result of such a transaction, not all that dissimilar from that of the GRAT, is that the Grantor is able to trade a highly appreciating asset (i.e., the asset sold to the trust via installment sale) within their estate for one with a lower expected return (i.e., the promissory note), with minimal gift and estate implications.

Impact Of Proposed Changes On Current IDGT Planning

The proposed changes to the Internal Revenue Code would eviscerate the sale-to-an-IDGT strategy. Notably, in a provision that directly targets such strategies, the newly proposed IRC Section 1062 would treat the Grantor and the IDGT as separate taxpayers for income tax purposes upon any transfer of property.

Such transfers would, naturally, include installment sales. Accordingly, whereas today such sales can be made free of any income tax liability, the proposed changes, if enacted, would trigger capital gains taxes for the Grantor as if they had sold the appreciated property to a third party.

Even at today’s capital gains rates, that would likely be enough to make a Grantor think twice about (if not outright avoid!) such an approach. If that rate increases, as is also contemplated by the proposed legislation, the desire to avoid such taxes is likely only to grow.

And of course, that’s to say nothing of the fact that the Intentionally Defective Grantor Trust is a Grantor Trust! Thus, the assets of the trust would still be considered part of one’s estate under the proposed new IRC Section 2901(a)(1).

In effect, if an individual made a sale of an appreciated asset to a GRAT under the new rules, they would trigger recognition of the asset’s gain, potentially resulting in a substantial income tax liability, in exchange for absolutely no benefit with regard to the estate tax front. Ouch!

What To Do Now – IDGTs

For individuals who want to make use of the sale-to-IDGT strategy, this is an “all-hands-on-deck” situation. There is, quite literally, no time to waste.

Either take action (now!) to reach out to a qualified attorney to begin drafting the necessary documents and make the preparations needed to seed the trust with the required capital (generally about 10% of the purchase price), or be prepared to kiss this potentially estate-tax-saving benefit goodbye.

Finally, it should be noted that all aspects of the potential transaction must be completed prior to enactment for this to work. Specifically, in order for the trust not to be considered part of the Grantor’s estate (which would negate the estate tax planning benefit), the IDGT must be executed and funded prior to the date of enactment. Furthermore, in order to avoid capital gains on the sale of an appreciated asset, that sale must also take place prior to enactment!

“Stand-by IDGTs” For The (Future) Ultra-Wealthy?

There is, perhaps, a small case to be made for what one might consider a “Stand-by IDGT.” In short, imagine a situation where an individual is confident that they will both 1) have a future estate tax concern, and 2) purchase an asset in the future that will have the opportunity for substantial appreciation.

In such instances, there is an argument to be made that creating and funding an IDGT with a modest amount of capital now, before enactment, could make sense. In doing so, despite its Grantor trust status, the trust’s assets would be considered out of the Grantor’s estate. Later, if an asset with a high expected return is identified, it can be sold (or swapped) with the asset in the trust.

Such a sale (or swap) would trigger capital gains if it were made after the date of enactment, but if the Grantor is making the purchase ‘today’ and selling it to the IDGT ‘tomorrow’, there should be minimal, if any, capital gains. All future appreciation (less the promissory interest payments) could then accrue outside of the estate, in the IDGT.

Can Adverse Impacts To Spousal Lifetime Access Trusts (SLATs) Be Mitigated With An Adverse Beneficiary?

Another popular estate planning strategy that would be impacted by the proposed changes is the Spousal Lifetime Access Trust (SLAT). Such trusts provide a unique opportunity for individuals to “have their cake and eat it, too” by removing assets from their estate, while continuing to have indirect access to the income and/or principal to support their ongoing needs.

The proposed changes to the Grantor trust rules would largely eliminate SLATs as we know them today. However, if that happens, we could see a rise in the use of Non-Grantor style SLATs in the future.

Spousal Lifetime Access Trust (SLAT) Overview

Popularized only more recently, within the past decade, the Spousal Lifetime Access Trust (SLAT) has quickly become an estate planning go-to strategy for many married couples. In essence, the SLAT is a credit-shelter trust created during the lifetime of the Grantor, as opposed to one that is created upon their passing, that names the spouse as beneficiary and seeks to solve the question, “How can I use my exemption amount now, while still retaining access to the assets in case I want or need them?”

Simply put, you can’t. But the SLAT probably gets married couples as close to that magic combination as possible!

More specifically, a SLAT is an irrevocable trust that is created and funded using some or all of the Grantor spouse’s gift tax exemption amount. This removes the assets of the trust from the Grantor’s estate.

But similar to the typical application of a credit shelter trust, the SLAT is drafted to give the Grantor’s spouse (who is often a trustee – if not the only trustee – of the trust during the spouse’s lifetime) access to trust income, and potentially to trust principal as well. In some cases, other individuals, such as children, are named as additional income beneficiaries. The hope (of the Grantor spouse), of course, is that the SLAT beneficiary spouse (or the children) will use some of their SLAT distributions to support the Grantor spouse.

Impact Of Proposed Changes On Current SLAT Planning

Once again, the proposed new IRC Section 2901(a)(1) inclusion of Grantor Trust assets in the value of the Grantor’s gross estate deals the death blow to the utility of SLATs that are set up as Grantor Trusts.

Notably, under the current rules, most SLATs are structured as a special ‘flavor’ of an Intentionally Defective Grantor Trust (IDGT). Since naming a spouse as the beneficiary of a trust typically results in classification as a Grantor Trust, most SLATs are considered Grantor trusts. Under the current rules, that’s not a problem. In fact, in most cases, it’s preferable due to the continued ability of the Grantor to pay the income tax liability of the Trust (even though the assets have been removed from their estate for estate tax purposes).

But if the current proposed legislation is enacted as contemplated, it would eliminate any estate tax benefit of Grantor-style SLATs, since the value of all assets in the Grantor Trust would be included in the Grantor’s Estate. And if the SLAT can’t remove the assets from the Grantor’s estate, the trust serves no estate tax planning purpose!

Nerd Note:

Grantor SLATs could still potentially offer some limited creditor protection. More specifically, as irrevocable trusts, they could still help Grantors remove the assets from their control, which in many cases would put them out of the reach of their creditors as well.

What To Do Now – SLATs

As is the case with GRATs and IDGTs, if an individual is considering the use of a SLAT in planning, there is no time like the present to get things in motion. Since the SLAT, relative to other estate-tax-minimizing strategies (e.g., GRATs and IDGTs), allows the Grantor more flexibility to benefit (albeit indirectly) from the assets of the trust, individuals may be more willing to implement a SLAT strategy when they are concerned about having enough wealth to meet their own lifestyle objectives.

To benefit from today’s current favorable treatment, though, SLATs would have to be drafted and funded prior to enactment.

That said, unlike GRATs and IDGTs, which would effectively be destroyed by the proposed legislation’s enactment, there could be a place for certain SLATs in the future. While many challenges (and practical implications) exist when it comes to drafting and implementing such trusts, there appears to be an ability to create “Non-Grantor SLATs” (more on this in a moment).

More specifically, if a SLAT puts an “adverse beneficiary” between the Grantor’s spouse and trust distributions, the trust should be able to avoid Grantor status (which would remove the trust’s assets from the Grantor’s estate, albeit with the tradeoff of making the trust responsible for its own tax bill).

From a practical perspective, there are complex nuances that do create some challenges to Non-Grantor SLATs, as an “adverse beneficiary” is a beneficiary of the trust that would benefit from having assets remain in the trust until they become entitled to them at a future date, which means that they may potentially be in opposition to the use or distribution of any trust assets before they become entitled to their share of assets.

While some families with healthy marriages and relationships with their children may not see this as a deal-breaker, many would be uncomfortable with such an approach. And it would be particularly problematic in situations where the spouse and the future successor beneficiaries of the trust are truly adversarial, as there could be little to no reason for such individuals to consent to the distributions, as would be necessary for the distributions to be made in the first place.

Finally, it should be noted that it’s not yet entirely clear whether the IRS agrees that such a trust with an adverse beneficiary would indeed be a non-Grantor Trust. Notably, in 2020, the IRS put SLATs with adverse beneficiaries on its “No Rulings List”. Which means that the IRS does not intend to issue Private Letter Rulings (PLRs) on the matter that would give individuals the ability to move forward with total confidence, knowing for certain whether such trusts would be treated as Non-Grantor Trusts (which would be exponentially important to know if the proposed legislation was enacted). Accordingly, any individual choosing to use such an approach in the future should be appropriately cautioned about the potential for an IRS challenge.

The proposed legislation put forth by the U.S. House of Representatives’ Ways and Means Committee has the potential to dramatically reshape the estate tax planning environment. While most households will continue to have a total net worth less than the proposed exemption amounts, halving the current exemption would result in a meaningful increase in affected families.

And whereas today, such families have a host of tried-and-true strategies they can use to further minimize estate tax liability when net worth exceeds the available exemption amount, the proposed legislation would greatly reduce (if not eliminate) the benefits of many commonly used strategies such as those relying on GRATs, IDGTs, and SLATs.

But those changes, per the proposed legislation, would not become effective until the date of the bill’s enactment. Accordingly, individuals who could benefit from such strategies (may) still have an extremely limited window of time in which to act and implement to benefit from current rules.

For such individuals, the advice is clear. “Order now while supplies last.”