Executive Summary

With the rise of the robo-advisor – and FinTech more generally – all aiming to drive down the cost of investing for consumers, more and more have questioned whether the ‘traditional’ 1% AUM fee will even survive much longer.

Yet a deeper look at the history of the AUM fee reveals that not all costs based on assets-under-management are the same. While investment companies (i.e., mutual funds) typically have an expense ratio calculated as a percentage of AUM, and (registered) investment advisors have long charged AUM fees for investment advice, it’s only in recent decades that brokers have begun to earn AUM-like fees, either in the form of 12b-1 fees (an upfront sales commission paid out over time) or wrap fees (a AUM-based alternative to transactional trading commissions). In other words, some AUM fees are actually for advice, while others are really just a form of levelized commission for product sales or brokerage transactions.

The impetus for this shift does appear to be technology – not robo-advisors necessarily, but the ongoing impact of technology that has, for the past 40 years, brought down transaction costs and sales commissions, from the rise of discount brokerage to the availability of online brokerage accounts that allow consumers to buy no-load funds directly. Which means it’s increasingly difficult for brokers to get paid to broker transactions or sell products, driving them towards AUM alternatives instead.

The caveat, though, is that while there is a “great convergence” of brokers getting paid levelized commissions akin to AUM fees, and investment advisers that continue to receive AUM fees, the regulatory standards for the two are different. Accordingly, it is perhaps no surprise that the regulatory battleground for the past two decades has been about the distinction between brokers and investment advisers (and their suitability vs fiduciary standards) – because the two really are converging around a substantively similar business model.

From the perspective of the advisor, though, the significance of this trend is that the so-called “fee pressure” on the 1% AUM fee is primarily on the 1% distribution charge, not the 1% AUM fee for actual advice. In fact, brokers that struggle to justify their value proposition are increasingly getting their CFP marks and trying to add more value through financial advice, while investment advisers who already gave advice feel the pressure to step up and differentiate in an increasingly crowded marketplace. Which means overall, the real pressure is not on the 1% AUM fee for advice – at least, not at this point – but instead on how salespeople can shift the value proposition of the AUM fee from distribution to actual advice.

The History Of The AUM Fee Schedule

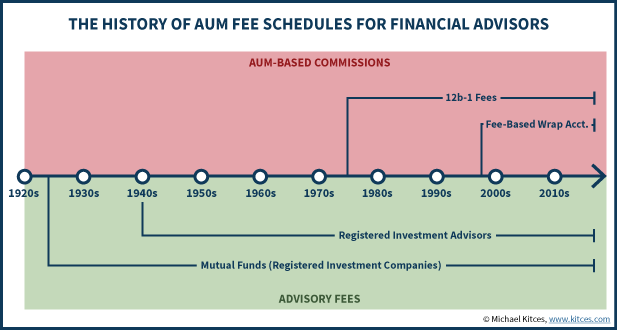

For most of the past century, the assets-under-management (AUM) fee has been the domain of those providing investment management services. It is, after all, a rather natural payment mechanism for investment management services – the asset manager’s fees are directly related to the amount of money that he/she is responsible for (and ostensibly is adding value for).

Accordingly, mutual funds charge an expense ratio based on assets under management for their services, dating back to when MFS launched the first mutual fund in 1924, and enshrined in the rules for mutual funds under the Registered Investment Company Act of 1940. Similarly, under the Investment Advisers Act of 1940, Section 202(a)(11) stipulates that a person who gives investment advice for compensation – whether an asset-based or a fixed fee – is deemed an investment adviser, and accordingly must register as an RIA.

However, the idea of setting a charge for services based on assets under management is not exclusive to the world of (discretionary) investment management. Brokers can also receive an “AUM fee” in the form of a 12b-1 fee, so named because it is authorized (since 1980) under Section 12b-1 of the Investment Company Act. Notably, the 12b-1 fee is technically a “distribution” charge (i.e., a sales charge, or a commission) paid by the mutual fund company to the broker who sold it, rather than a fee paid by the client. Regardless of who pays the fee, though, the net cost to the client is substantively the same, especially given that FINRA Rule 92-41 permits investment companies to pay 12b-1 fees of up to 0.25% for ongoing servicing, plus up to 0.75%/year for levelized sales charges, adding up to the “traditional” 1% AUM fee. Still, though, the majority of the 1% 12b-1 fee is simply a 0.75%/year levelized payment of an upfront commission (i.e., the upfront sales load of a mutual fund, paid out over several years).

At the same time, another version of the (1%) AUM fee comes from the brokerage world, which historically simply charged transactional trading commissions, and/or sold securities from their inventory and earned dealer compensation (in the form of mark-ups/mark-downs or similar fees). However, after the 1995 Tully Commission observed that per-transaction commissions incentivized brokers to churn accounts, and that a level fee-based charge that wrapped all the costs together could help reduce such a problematic incentive, the brokerage industry began to shift towards another version of the 1% “AUM fee” approach. First dubbed a “wrap fee”, or a “fee-based brokerage” account, the SEC proposed in 1999 and finalized in 2005 a rule that would allow brokers to charge AUM fees for such fee-based wrap accounts, though ultimately a subsequent lawsuit from the FPA forced the rule to be vacated in 2007 (on the grounds that the SEC had exceeded its authority in granting the exemption). Since then, scope of non-discretionary fee-based wrap accounts has been more limited (and spawning the growth of hybrid RIAs instead).

The fundamental point, though, is that over the years, more and more segments of the financial services industry has been adopting the AUM model (or at least, “AUM-like” fees).

Technology And The Convergence Of Fees For Advice And Commissions For Distribution

The significance of this history of multiple types of fees, all based on an investor’s assets under management, is that functionally there are actually two different “kinds” of AUM fees: one is for investment advice and/or discretionary investment management, and the other is a levelized “fee” that is actually a substitute for an upfront commission (either a wrap fee for brokerage trading commissions, or the payment of an upfront commission that is being spread out over time).

In other words, one type of AUM fee is actually for advice, while the other is simply a levelized commission for a product sale or brokerage transaction. Or viewed another way, the historically upfront-commission-oriented compensation of investment salespeople is converging on the AUM model traditionally used for investment management, as traditional commissions are increasingly levelized.

Notably, though, the driving force towards more levelized compensation for salespeople doesn’t appear to be solely driven by the altruistic goal of reducing churning, as highlighted by the Tully Commission. (In fact, the pendulum is now swinging so far in the other direction, that the SEC and FINRA are increasingly concerned about “reverse churning” of fee-based brokerage accounts that aren’t doing enough trading to justify the ongoing wrap fee!) Instead, the shift away from the commission-based transactional model also appears to be driven by the ongoing march of technology over the past several decades.

After all, there was little need to move away from transactional brokerage business and towards the AUM model of investment advisors in the first several decades after the Investment Advisers Act of 1940. Brokerage trading fees were fixed anyway, regardless of the size of the trade, which made them highly profitable (and overly expensive for the typical individual investor). It wasn’t until “May Day” of 1975 that brokerage commissions were allowed to float competitively in the marketplace, giving rise to the “discount brokerage” movement (and the explosion of discount brokerage firms, led by Charles Schwab).

In the 20 years that followed, though, the average cost to transact a trade fell by about 90%, destroying the traditional commission-based stockbroker business model. And in the subsequent 20 years after that, the average sales load on mutual funds began to fall as well, driven by the emergence of online brokerage firms (e.g., E-Trade and TD Ameritrade), which made it possible for investors to buy no-load funds directly, without paying an investment salesperson a commission at all.

And the trend is now accelerating, as more and more no-load and institutional class funds become available, along with ETFs, all of which exclude 12b-1 fees from their cost structure and therefore are presented as the cheaper alternative than the competition (and often also the better performer, given the significant impact of investment costs on performance).

In other words, technology is slowly but steadily driving down the cost of distribution (at least for a subset of the best and cheapest investment solutions), which is undermining the ability of investment salespeople to be paid commissions for distribution. The competitive forces of technology and the market pressure they apply, along with rising regulatory scrutiny on upfront commissions, is driving a great convergence – where the investment adviser’s AUM fee and the investment salesperson’s AUM-as-levelized-commissions fee are looking more and more the same.

The Difficulty In Differentiating Investment Advisers From Salespeople

While arguably there are some positives to this “great convergence” of advice fees and distribution commissions – in particular, the reduced incentives for brokers to churn investment products – it has also created significant confusion for consumers, because now two “advisors” who charge substantively similar (AUM) fees may or may not be providing substantively similar services.

To some extent, this is simply the natural outcome in any marketplace – producers (including advisors) can compete on the costs they charge and the value they provide, and allow consumers to decide which is best. However, the situation is complicated by the fact that our existing regulatory environment applies different legal and regulatory standards for salespeople versus advisors – where advisors are subject to a fiduciary duty on behalf of their clients, but salespeople must merely sell products that are not unsuitable for their customers – such that it’s important for consumers to be clear about which is which.

Historically, Congress attempted to establish this distinction with Section 202(a)(11) of the Investment Advisers Act of 1940, which stipulates that anyone who provides investment advice, for compensation, is required to register as an investment adviser. The only exception to this for salespeople at brokerage firms was under Section 202(a)(11)(C), where if the advice provided was “solely incidental” to the sale of brokerage products and services, and the broker did not receive any form of “special compensation” (i.e., AUM fees), then he/she could avoid investment adviser status. In fact, the entire controversy of the proposed broker-dealer exemption rule in 1999 (stemming from the Tully Commission that preceded it) was that brokers would have been allowed to charge AUM fees without registering as investment advisers, and was ultimately struck down precisely because the court concluded that the SEC didn’t have the authority to grant brokers an exception from registering as investment advisers if they were going to receive AUM fees like investment advisers.

Unfortunately, though, the SEC has continued to be lax in enforcing the dividing line between salespeople and advisors, as required under the Investment Advisers Act, which is why the recent expansion of the Department of Labor’s fiduciary rule was arguably an inevitable outcome. Given the ongoing converge, with a growing number of brokers operating an advisor-like business model, charging advisor-like AUM fees (even if paid via an asset manager’s 12b-1 levelized commission), and using advisor-like titles (such as “financial advisor”, “financial consultant”, “financial planner”, etc.), it became necessary to apply a consistent regulatory standard to them all.

In other words, as the AUM fees of brokerage salespeople and advisors converge, so too are the regulatory standards that apply to them.

Changing The Value Proposition Of The 1% AUM Fee

The significance of this great convergence of the 1% AUM fee, and the commoditizing forces of technology that are impacting it, is that while it’s increasingly popular to discuss whether “the AUM fee is toast” in today’s world of technology and robo-advisors, most of the pressure on the AUM fee is on the distribution version of the fee, not the AUM fee for advice.

For instance, a detailed look at the services of most robo-advisors reveals that their primary function is to help an investor select an asset-allocated portfolio that fits his/her risk tolerance and time horizon – a role that was classically filled by investment salespeople, who provided this “service” as a part of the sales process and in the name of determining suitability. Accordingly, robo-advisors fulfilling this function is the robo-advisor as an alternative distribution channel for investment products, not a reduction in fees for advice. Or viewed another way, the AUM fee for “beta” may be moving towards zero – you can’t earn 1% just to sell an index fund – but that simply means advisors must provide alpha or gamma to justify their value proposition instead.

In turn, this means that with an ever-declining price that investors are willing to pay for distribution costs (i.e., commissions and other sales charges), brokerage salespeople who want to defend their value and the (AUM) prices they charge will be compelled to deliver more financial advice above and beyond just recommendations relating directly to the product being sold. In other words, the broker must “do more” to justify the same compensation he/she earned in the past. This trend just further accelerates the foray of brokers into financial advice, the growth of the CFP marks, and efforts to offer financial planning and wealth management services as the “anti-commoditizer” to counterbalance the downward pressure that technology is putting on their commissions. Of course, this will only further accelerate the convergence of salespeople and advisors – both of whom are increasingly offering advice – lending further credence to the DoL’s decision to apply a fiduciary rule on all types of advisors and brokers who were providing recommendations to retirement investors.

In the meantime, though, it’s still not entirely clear whether there’s much of any pressure on AUM fees for advice directly. While some have discussed unbundling financial planning fees from AUM fees, the most financially successful advisory firms have continued to stick (successfully) with the AUM model. It’s not even clear that larger advisory firms benefit from economies of scale on providing financial advice, though there is ironically some indication that larger firms are more effective at scaling their distribution costs to bring in clients who will pay for that advice.

Nonetheless, the fundamental point is simply that the distribution costs that investors once paid brokerage salespeople for investment products is slowly but steadily converging towards the (1%) AUM fee that investment advisers have historically charged for advice. Given that these are still different “channels” for regulatory purposes, though, the great convergence of the AUM model – and the increasing convergence of advice-oriented services to earn those fees – is driving investor confusion about the difference between advisors and salespeople (and fiduciary vs suitability), and raising questions about whether the current regulatory structure for advisors is outdated (as fee-based wrap fees and 12b-1 fees were never intended to pay primarily for advice).

From the perspective of advisors and especially brokers, though, the real challenge of the great convergence is figuring out to how to keep earning the same 1% AUM fee, while shifting the underlying services being rendered to the end client from “just” selling products to actually providing advice. In other words, the “pressure” on the 1% fee is not so much about whether advice is worth 1%, but whether those who were historically salespeople can provide enough value-added financial advice to defend that 1% fee, and whether investment advisers who already charged for this advice can maintain enough differentiation and additional value-add to survive the increased competition.

So what do you think? Is there a difference between an AUM fee for advice, and a 12b-1 trail? Will technology undermine the 1% AUM fee, or just force a re-definition of its value? Please share your thoughts in the comments below!