Executive Summary

A growing base of research shows that even though money itself is fungible, the way we think about our various money assets is not; instead, we tend to “mentally account” for money into various buckets of current income, current assets, and (assets for) future income. The fact that we tend to categorize our income and assets into various buckets helps to explain the popularity of so-called “bucketing strategies” for retirement income, whether segmented by time (short, intermediate, and long-term needs) or type of spending (essential vs discretionary needs).

However, the research also suggests that the way we mentally account for income and assets also has an intrinsic hierarchy of priorities – first, we need to cover our current income needs, then our current assets, and finally our savings towards future income needs (ideally, with some potential for further upside and the possibility that our future income could continue to improve over time).

The significance of this “hierarchy of retirement needs” is that it helps to explain why some types of retirement income strategies like annuitization are very unpopular (despite the fact that retirees routinely state their biggest fear is outliving their retirement assets and annuitization can guarantee that will never happen), while others are used far more often even if their current guarantees are inferior to available alternatives (e.g., most guaranteed living benefit riders on today’s variable annuities).

However, perhaps the biggest caveat to the hierarchy of retirement needs is that if retirees must satisfy a desire for current income, and future income, and have liquid current assets available, they may actually feel compelled to save more for retirement than they actually need (even if there is no desire to leave a legacy behind). After all, it “should” be sufficient to just save for future and current income, without a separately holding of liquid assets; nonetheless, recent research finds that the amount of “cash on hand” (or at least, liquid bank holdings) a person has is directly (and positively) related to their self-reported well-being and life satisfaction, even if they didn’t have a financial need for it. Nonetheless, if the need for future income cannot be achieved until the need for current assets has been mentally satisfied first, retirees may continue to feel constrained by not having enough – even if they do – and/or to choose retirement income solutions that are mechanically inferior but psychologically more satisfying to our hierarchy of retirement needs!

Mental Accounting Buckets And The Hierarchy Of Retirement Needs

Various types of “bucketing strategies” have long been popular as a way to both illustrate and implement various retirement income strategies.

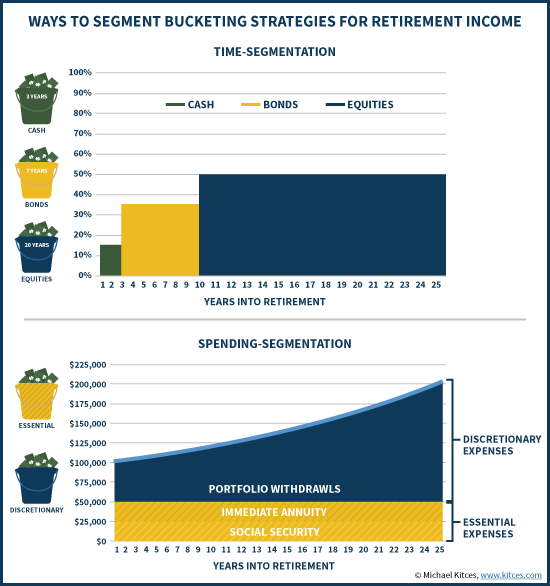

The classic “time segmentation” strategy typically divides retirement assets into three buckets – a short-term bucket to cover the next few years of spending (invested in cash), an intermediate-term bucket to cover the subsequent 5-10 years of spending (in bonds), and a long-term bucket to cover spending beyond a 10-year time horizon (invested into equities). Notably, such bucketing strategies don’t necessarily produce a materially different asset allocation than a classic diversified balanced portfolio; nonetheless, for an investor who might have a 60/30/10 stock/bond/cash portfolio anyway, it seems to be far easier for most retirees to conceptualize.

An alternative version of bucketing is to segment spending longitudinally over time, dividing long-term expenditures into “essential” expenses (the food/clothing/shelter kind of expenses you really can’t afford to outlive), and “discretionary” expenses (the ones that we want, but don’t need to survive, and can be more flexible about). Once expenses have been separated (which can be a challenge unto itself!), assets can be allocated to appropriately match the buckets; for instance, the essential expenses might be paired with Social Security and lifetime immediate annuitization, while the discretionary expenses can be funded with a diversified portfolio.

In the financial planning context, these bucketing strategies are often used as a means to help retirees get more comfortable with the impact of market volatility on retirement assets, by deliberately tying retirement accounts to either distant future retirement income needs (the time-segmentation strategy), or the more flexible retirement income needs (the spending-segmentation strategy).

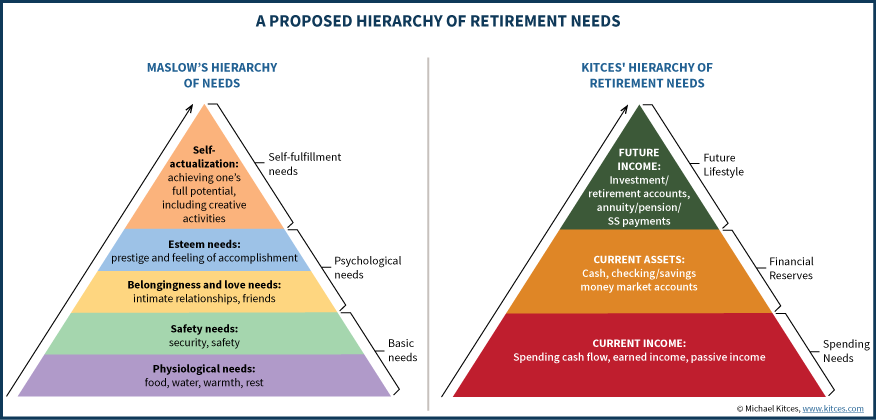

More generally, though, these strategies appear to “work” because they align reasonably well with how our brains appear to engage in “mental accounting”, turning otherwise fungible assets into separately accounted buckets. Although the research suggests that mental accounting doesn’t necessarily always tie buckets directly to particular goals; instead, Shefrin and Thaler have found, in looking at the available research, that consumers most typically account for their wealth in three separate buckets: current income, current assets, and (assets to support) future income.

These mental accounts matter because, even if the actual investment accounts are otherwise similar and the money is fungible, consumers react differently depending on where they feel the “squeeze” (or the wealth) as their situation changes over time. Thus, for instance, a household that feels less wealthy is most likely to constrain their current income to get back on track (and focus the blame for their shortfall on their latest expenditures). And a household that is otherwise wealthy in net worth may still feel “poor” and be unhappy if it doesn’t have a reasonable amount of liquid cash on hand (even if they don’t need it).

Perhaps the most significant distinction of having these mental account buckets, though, is that because of their implicit prioritization – where current income matters more than current assets, which matters more than future income – it’s difficult to be satisfied with the status of the longer-term buckets until the nearer-term ones are satisfied. Or viewed another way, just as Maslow found that people have a motivational hierarchy of needs that must be satisfied in a certain order – for physiological and safety needs first, then psychological needs (e.g., belongingness, love, and esteem), and finally self-fulfillment needs – so too does the retiree appear to have a hierarchy of retirement needs that must be satisfied in the proper sequence.

And as it turns out, this hierarchy of retirement needs also reveals a lot about our actual preferences for various retirement strategies!

The Value Of Cash On Hand – The Conflict Of Cash And Annuitization

It’s long been observed that a prospective retiree’s number one concern is the potential that he/she won’t have enough money to afford retirement and/or will outlive available retirement assets and go broke. In essence, it’s the fear that the “future income” bucket of the retirement needs hierarchy won’t be satisfied. Yet the most straightforward solution to this fear – buying a lifetime immediate annuity at retirement – is rarely implemented, with immediate annuity sales continuing to hover at barely $2B every quarter, which is barely more than 1% of total annuity sales every quarter, and an even more miniscule proportion of total retirement assets.

Yet in the context of the research on mental accounting and the hierarchy of retirement needs, this is easily explained: even if we fear a shortfall of future income, we’re not willing to give up the liquidity of current assets to secure it, because having sufficient current assets is a required foundation first. In other words, even if immediate annuitization solves the “future income” need, and even if we can afford to do it, we’re still not willing to undermine the lower levels of the hierarchy to satisfy the top, because the hierarchy must be fulfilled in order. Or viewed another way, it’s not actually a “fear of outliving money” but “a fear of outliving the money that’s available after having enough liquid cash on hand (and income to pay current bills)” instead.

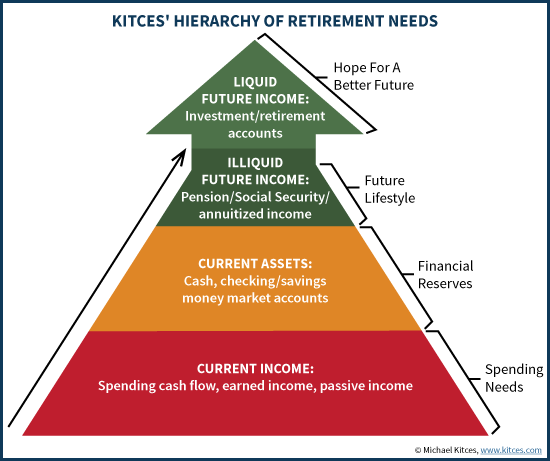

Accordingly, it’s not very surprising to find that to the extent that retirees do choose annuitization, they strongly prefer partial annuitization options to an all-or-none strategy – because it has less of an impact on the “current assets” tier of the hierarchy. Similarly, the retirement needs hierarchy and the fact that it’s necessary to have liquid current assets before committing to future-income assets helps to explain the popularity of variable annuities with guaranteed living withdrawal benefits as well – generally, the actual future-income guarantee is far superior with a pure immediate annuity than with a GLWB, but the variable-annuity-with-GLWB strategy is a more liquid version, helping to satisfy the desire for current assets. Notably, this suggests that even within the “future income” tier of the hierarchy, consumers appear to be making some distinction between allocations to “liquid” future-income sources, and “illiquid” versions (that are more guaranteed, but again at the cost of being less liquid).

The “As Good As It Gets” Problem With Annuitization And Retirement Income Guarantees

Another challenge emerging in the research on retirement income is that ultimately, it appears retirees don’t just want to have future income in retirement to satisfy their needs… they want the potential for an increasing standard of living over time, too.

In other words, it’s not enough to say “here’s a strategy to guarantee your retirement income” if it’s implicitly paired with the outcome “but this is as good as it gets”. Notably, this is distinct from a retiree who may have an explicit “legacy” goal to leave assets to heirs; in fact, the whole point is that even those who don’t want to leave assets to heirs may still refuse to annuitize their assets because of the lack of personal upside potential.

Of course, the most straightforward way to resolve this issue is to purchase a rising stream of guaranteed income, such as with an inflation-adjusting immediate annuity. Yet, in practice, inflation-adjusting immediate annuities are even less popular than traditional fixed immediate annuities. Though again, in the context of the hierarchy of retirement needs, this too makes sense: because most households have limited assets, spending the same available dollar amount on an inflation-adjusted immediate annuity will result in a lower starting payment (that increases later with inflation)… but the requirement to take a lower starting payment now causes a deficit in the tier of “current income” needs!

On the other hand, this again helps to explain the popularity of the GLWB annuity, or more generally various “floor-with-upside” retirement income strategies – because the floor helps to secure current and future income, the upside satisfies the “as good as it gets” syndrome, and the liquidity (usually associated with the investments that produce the upside potential) satisfies the need for current assets. Even if, ironically, the cumulative outcome may be an inferior retirement income guarantee!

The Hierarchy Of Retirement Needs And The Conflict Of Behavioral Biases And Reality

One of the fundamental challenges that the hierarchy of retirement needs illustrates is that retirees may have a demand for more retirement income and assets than they actually need.

Because in theory, retirement income needs can be fully satisfied with some allocation to current and future income needs. However, the research on mental accounting suggests that people typically have a “current assets” bucket as well, and that they may not be happy if it is depleted, even if it is not needed; one study found that having “cash on hand” (e.g., a liquid checking/savings account balance) was directly correlated with life satisfaction, even after controlling for investments, total spending, and indebtedness (suggesting that it wasn’t a need for cash, but simply the satisfaction of having it)!

Yet, if retirees want to have everything they need for retirement income and additional liquid assets, they will cumulatively want more than they actually need! And the situation is further exacerbated by the “as good as it gets” syndrome, and the desire to not only secure future income in retirement, but a desire for a rising future income in retirement, even though the research finds that retiree spending actually declines with age. In other words, even though we probably need less in assets to cover declining future income needs, we want even more to satisfy a desire for upside potential even if we won’t likely end up needing or using it.

A key distinction, though, is that the hierarchy of retirement needs suggests that retirees will be unwilling to convert the bulk of their assets to (illiquid) guaranteed retirement income, even if there is no desire to leave a legacy, but simply due to the “irrational” desire to have current and future income and liquidity and a potential for income upside (even if may never be spent when the time comes).

More generally, though, what the hierarchy of retirement needs suggests is that any/every retirement income strategies should probably be reframed around its ability to answer all three of these core questions for the prospective retiree:

1) Where does my current income come from?

2) Do I have a reasonable (albeit even irrationally sized) base of liquid current assets?

3) How am I funding or securing my future income, in a manner that can still grow?

And in the context of financial planners in particular, it’s crucial to remember that while we most commonly focus on #3 for the long run, the client may not be satisfied with the result until you also resolve their needs for #1 and #2, first – because the hierarchy of retirement needs must be satisfied in order!

So what do you think? Is there a hierarchy of retirement needs? Does this hierarchy help explain some seemingly irrational consumer preferences? Must we resolve the current income and liquid current asset goals of clients before they'll be satisfied addressing future income? Please share your thoughts in the comments below!