Executive Summary

While the launch of direct-to-consumer “robo-advisors” hasn’t exactly disrupted the existing AUM of (human) financial advisors, the technology tools of robo-advisors have done much to highlight the inferiority of many of the technology solutions available to advisors today. So much, in fact, that a number of robo-advisors are beginning to pivot and offer their tools for advisors to use with their own clients.

This robo-advisors-for-advisors trend, though, raises interesting questions about how exactly advisors should position themselves and their own value proposition. What is the value of an advisor offering a largely self-service automated investment solution? Is it still in portfolio design and investment selection? Or managing the behavior gap? Or simply an opportunity to focus on other financial planning advice and value-adds instead? And does a robo-advisor-for-advisors solution support AUM pricing, compress it, or force advisors to unbundle instead?

Ultimately, it seems that the adoption of robo-advisor solutions will vary depending on the nature of the advisory firm. For newer startup advisors, the robo-advisor trend may simply be an opportunity to build a more efficient firm from scratch, especially in a world where many investment custodians aren’t welcome of new advisors with no AUM anyway. For other financial-planning-centric advisors, the robo-advisor platforms may simply be a new form of TAMP solution with superior technology. And for existing investment management and wealth management firms, the end point for robo-advisor platforms may be a form of marketing and “feeder” system for clients below the firm’s minimums to start themselves, and then “graduate” to higher level services of the firm as their investment assets, net worth, and financial complexity grow. Though in the long run, robo-advisors that continue to iterate towards new ways to implement investment management through technology – such as Indexing 2.0 solutions – may ultimately present the potential for advisors to offer clients entirely new and previously unseen investment solutions to clients!

The Trend Of Robo-Advisors For Advisors

Over the past 3 years, the “buzz” around robo-advisors has exploded, along with the venture capital being invested to fund them – now to the tune of several hundred million dollars across platforms like Wealthfront, Betterment, and more.

Yet for all the buzz about their potential for disruption, the core value proposition that a robo-advisor delivers on is actually little more than crafting a relatively straightforward passive strategic asset allocation, paired with the trading software to implement and rebalance those portfolio models, and an online onboarding process to make it easy for investors to invest. In essence, the automation of a self-service balanced mutual fund-of-funds, but without the mutual fund itself.

Notably, though, this technology is not entirely unique to robo-advisors. Human advisors have designed asset-allocated portfolios for years, had automated rebalancing software that can keep clients invested to those models for about a decade now, and the industry has (albeit slowly) been adopting digital e-signatures to facilitate the client onboarding process (which most robo-advisors simplified for themselves by only taking investor deposits as cash transfers, avoiding the complexity of managing through the ACAT system).

Nonetheless, it’s hard to argue against the sheer quality of the robo-advisor user experience; while the concept of the portfolios and the technology to implement them is not new, the sophistication of the algorithms powering the rebalancing and tax-loss-harvesting tools of at least some robo-advisors is arguably a “version 2.0” improvement on the rebalancing 1.0 software that most advisors are using. Similarly, the onboarding process of robo-advisors is clearly superior a superior client experience compared to the capabilities of human advisors to manage account paperwork and signatures digitally (for those who can even do so in the first place).

In fact, advisors have so lamented the quality of the technology tools made available to them – illustrated in sharp relief by the quality of many robo solutions – that some robo-advisors are responding by pivoting to offer their tools for advisors. With more than half a dozen such platform solutions making a splash at the recent T3 Advisor Technology conference, advisors suddenly find themselves with the opportunity to use some of the same tools that were once threatening to challenge them.

Yet in turn, this raises a challenging question: for what are still largely self-directed automated investment solutions for clients – whether offered by the “robo” advisor or “human” advisor – what is the value proposition of a human advisor offering a robo solution, and how should advisors explain and charge for their services?

The Value Of An Advisor For A (Mostly) Self-Directed Automated Investment Solution

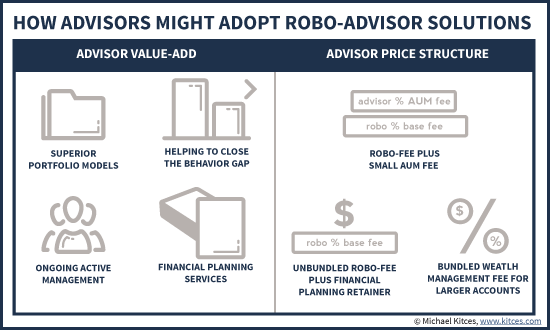

If there’s one thing that the proposition of robo-advisor-for-advisors solution makes clear, it’s that the price point for offering a basic passive strategic asset allocation that is regularly (and automatically) rebalanced is no longer the “industry standard” 1% AUM fee. Just providing access to the market return through a diversified portfolio – “buying the market beta” – is being commoditized by technology to an ever-declining price point. Instead, for advisors to survive and thrive, they must add value by some other means – either by adding alpha to further enhance returns, or by offering “gamma” in the form of non-portfolio (e.g., financial planning) value-adds.

Accordingly, an advisor might try to offer an “alpha” value-add with a robo-advisor solution by creating “superior” portfolios – e.g., a “better” asset allocation that uses more asset classes, has more diversification, is constructed with superior investment selection, etc. In essence, the advisor would charge more than the robo-advisor’s baseline cost for the value-add of constructing the portfolio (or a “better” portfolio than what the robo-advisor offers by default). For instance, Upside Advisor allows the construction of (the advisor’s own) model portfolios, and Betterment Institutional has indicated they are working on allowing advisors to craft their own portfolio allocations. In other words, while “robo-advisors” have generally gone directly to consumers with their own asset allocation portfolios, you won’t (necessarily) have to use their models to deliver to your own clients.

Alternatively, the advisor might use the capabilities of the robo-advisor tool to be more active in managing the portfolio on an ongoing basis – a notable parallel to the value-add that a number of advisors provide already with various forms of active strategies. The only difference is that the strategies might be executed using the trading, rebalancing, and portfolio design tools of the robo-advisor platform, instead of “traditional” advisor software tools on a custodian’s platform. For instance, advisors can easily craft sophisticated Socially Responsible Investing (SRI) portfolios using the Motif Advisor platform without needing a separate traditional custodian relationship at all.

For other advisors, the value-add of the advisor themselves to an otherwise self-directed robo-advisor solution might simply be the availability of the advisor – that person to talk to in the event that markets become volatile. In essence, the value of the advisor is being available to help manage the so-called Behavior Gap. This could be complemented by additional value-adds like ongoing educational events/webinars for clients. Though notably, it’s not entirely clear what consumers will pay for “education and the right to talk to someone if there’s a bear market” in the absence of any other value-add; unfortunately, avoiding the behavior gap is something more evidently valuable to consumers after the fact, and not necessarily something they may wish to pay for up front (as so many think they will be fine when market volatility comes… until it actually does).

And of course, beyond the various portfolio-centric forms of value-add, many advisors may look to support their value proposition on top of a robo-advisor solution by providing a more comprehensive and ongoing financial planning solution. In fact, arguably a robo-advisor solution may be especially effective for financial-planning-centric advisors, who would rather focus on the client’s holistic financial planning issues, and for which the portfolio is truly just viewed as one part (and not even a central one). In this context, the robo-advisor solution might function more like a traditional TAMP, albeit one with an even better ease of use for the advisor and user experience for the client.

How Might Advisors Charge For Robo-Advisor Solutions?

Given the wide range of potential ways that advisors might aim to add value on top of a robo-advisor solution, there are similarly a number of different ways advisors might try to charge for their role and offering of such services.

One approach may be to simply layer a small additional AUM fee onto the robo-advisor solution to account for the advisor’s value-add. If the robo-advisor platform fee is 25bps, the advisor might charge another 25bps, for a total cost of 50bps. This may be particularly appropriate/effective where the advisor isn’t otherwise aiming to add value to the portfolio – i.e., using the robo-advisor as a TAMP with their models, not the advisor’s own. The last 25bps advisory fee effectively becomes a fee for offering education and being available to talk as needed for basic portfolio advice. On the other hand, advisors don’t necessarily need to line item their fees out this way either; just as most advisors charge a single AUM fee without detailing how much of its cost goes to their portfolio accounting and reporting software and operations staff, so too may many/most advisors simply charge a single AUM fee, and navigate for themselves how much is available to the firm and how much covers the cost of the robo-platform supporting it.

For financial-planning-centric advisors, it may be preferable to simply unbundle fees altogether, and to charge a standalone or ongoing annual or monthly retainer fee for financial planning services, and again just a modest “administrative” fee for the investment platform. If the financial planning fees are sufficient, some advisors might even choose to just pass through the robo-advisor fee “at cost”.

On the other hand, if substantive ongoing financial planning services will be provided, along with portfolio management, some advisors may prefer to continue to bundle their fees together, and keep charging a 1%-style AUM fee for the “whole suite” of investment management and financial planning services, even if the reality is that the fee comes primarily from the portfolio but the advisor’s value-add comes primarily from financial planning. Though notably, such an approach may not be practical for “small” clients with lower asset levels, where a higher AUM fee on a limited account balance still cannot cover the cost of deeper financial planning services alone.

Notably, the reality is that these pricing structures are not really very different than those already in use by advisors today, which include a range of AUM fees for varying levels of investment management services, separate financial planning retainer fees, and “bundled” wealth management fees. The difference, though, is that building on top of a robo-advisor platform continues to accentuate how robo-advisors are turning the traditional AUM fee schedule upside down, where pricing may be the lowest for smaller accounts where the advisor provides limited value-add and the service is most a self-service automated solution, and the pricing rises as clients have increasing assets, net worth, and complexity, that merits deeper advice services.

Ways That Human Advisors Might Adopt Robo-Advisor Solutions

So given these different dynamics around advisor pricing and value proposition, what might the adoption of robo-advisors-by-advisors look like in “the real world”? While ultimately advisors might try out a wide array of approaches to adopt these platforms – which in the end, is really just a discussion how advisors might creatively implement technology – some likely “early adopter” approaches have or probably will include:

Startup Advisory Firms

For the financial advisor just getting started in launching a firm, today’s robo-advisor solutions may be quite compelling, especially those that actually provide the actual TAMP-style investment implementation of the accounts as a custodian (e.g., Betterment Institutional and Motif Advisor). For those getting started, it’s already difficult to find a “traditional” custodian who will work with an advisor that doesn’t already have $10M-$15M+ of AUM (the most popular exception to the rule being the “start-up friendly” Shareholders Service Group [SSG]). And working with a traditional custodian still requires a significant amount of additional work implementing investment portfolios, and/or spending additional dollars on technology to help.

From this perspective, robo-advisors-for-advisors basically become a “TAMP”-style solution with modern technology to allow the non-investment-centric advisor to gather assets and handle AUM clients without spending a great deal of time on that portion of the business. For those who actually want to be more hands-on to the portfolio construction process, a traditional custodian may still be preferable, though as the trading and portfolio design tools for robo-advisors continue to improve (for instance, Motif Advisor’s ability to customize portfolios for Socially Responsible Investing and other ‘tilts’), this gap may close over time as well.

Existing Financial-Planning-Centric Firms

For existing firms that are “financial-planning-centric”, the advisors by definition tend not to assign a lot of time/attention/effort to the role of portfolio management, and either eschew management client assets altogether, adopt relatively straightforward passive strategies, or delegate their investment management to a TAMP. For such firms, the appeal of the robo-advisor platform – especially one that provides TAMP-style investment implementation like Betterment Institutional, or makes it relatively easy for the advisor to build their own models, like Upside Advisor or Trizic – is an opportunity to shift to a more technology-enabled client-friendly investment solution.

If the firm was already implementing portfolios with a traditional custodian, the transition may provide a time savings, and may or may not produce a cost savings as well (depending on what the advisor was already spending on supporting technology for portfolio accounting, reporting, trading/rebalancing, etc.). If the firm was using a TAMP, the robo-advisor may simply represent a TAMP alternative (albeit with some client tax consequences to navigate if portfolios will shift from one platform to the other). If the advisor wasn’t actually offering investment implementation services already, the robo-advisor platform offers a way to provide clients a relatively easy and straightforward investment solution, for which the advisor might charge a very modest AUM fee to supplement what is probably already a separate financial planning retainer fee structure.

Existing Investment-Centric Firms

For advisory firms where their investment management process is already a major component of the value proposition they provide to clients, the adoption of robo-advisor platforms is more complex at a minimum, but two initial paths seem likely.

The first is for the robo-advisor platform to become a “feeder” system for the firm’s core investment management clients. In other words, as a client segmentation strategy the firm would likely offer its automated robo-platform as a self-service solution for “small” clients below the firm’s existing minimums, and any clients who don’t meet the firm’s minimums would be directed to this self-service option (or might even find it on the advisor’s website as a starting point in the first place). In this scenario, clients would likely receive “simplified” portfolio models, probably at a lower AUM fee, and as assets rise clients would “graduate” into the firm’s more sophisticated investment strategies (which may not even be feasible to implement with smaller household account sizes anyway), and possibly receive additional financial planning/wealth management advice as well. Examples in this context would be solutions like Trizic or Upside Advisor - the latter can overlay its technology right on top of an existing custodial relationship (e.g., TD Ameritrade), and in point of fact this is exactly how Ritholtz Wealth Management uses Upside Advisor with their “Liftoff” solution for smaller clients.

The second alternative is for a subset of larger advisory firms to actually shift and use a robo-advisor solution as their entire “full stack” comprehensive investment platform for the practice. Current robo-advisors-for-advisors aiming to provide a full wealth management/investment platform service include Oranj and Vanare/NestEgg. The biggest caveat to adopting this kind of robo transition will simply be its potential disruptive impact to the practice, as it would potentially require retraining on multiple software tools and systems, could lead to staff members that need to be repositioned in the firm altogether, and may be difficult to integrate into some existing systems that the firm may not be ready to let go off. While the disruptive impact may not be as severe for “smaller” advisory firms, the larger the firm the more challenging such a transition may be, especially as new comprehensive robo-advisor platforms are still ironing out their own technology, value-propositions, and exactly where they want to focus. In the near term, smaller advisory firms that have “hit a wall” in their current practice may find such a change to be appealing (or even necessary), but larger may likely end out waiting to see how the platforms evolve, and/or whether and how existing custodians step up.

The True Disruptive Potential Of Robo-Advisors (For Advisors)

Notably, from this perspective, the true disruptive potential impact of robo-advisors may be their impact on how advisors implement investment portfolios through the existing custodian channels and what technology they do (or do not) need to purchase to support the process (e.g., portfolio accounting and reporting tools, trading and rebalancing software, etc.). This may be especially true for advisors who build a practice on a robo-advisor platform and get clients accustomed to the use of the associated technology, and who may not have interest in switching later even if/when/as the advisor’s AUM rises to the point where they would be eligible for make a platform change. In other words, there is a “risk” that traditional custodians become a Baby Boomer advisor platform, while robo-advisors become the Gen Y advisor platform for the future, leading to a shift in industry AUM over time as the demographics play out.

In addition, it’s important to bear in mind that the “cutting edge” of robo-advisor implementation goes beyond even just the ability to automate much of the new client onboarding and investment implementation. Future solutions may include more sophisticated rebalancing and tax loss harvesting tools (as exemplified by the tax loss harvesting algorithms being developed by Wealthfront and Betterment), and even “Indexing 2.0” solutions that allow a robo-advisor platform to allocate clients into an index without actually using an index mutual or ETF fund and instead just buying all of the underlying stocks in the appropriate (fractional-if-necessary) shares.

The bottom line, though, is that while the initial launch of “robo-advisors” was all about gathering investment assets directly from consumers, their underlying technology tools are similarly relevant and useful for advisors as well… though the exact way that various robo-advisor solutions will fit into existing (or new) advisory firms will vary greatly depending on the exact needs and service model of the firm with its clients!

So what do you think? Do you have interest in implementing a “robo-advisor” solution in your practice? What problem would it solve or role would it fulfill? Are some platforms more or less appealing to you than others? Would a robo-advisor offering change how you charge your clients or offer services to them?

Michael, thanks for your insights. But there’s a most-important effect

the robos will bring to investor guidance that you haven’t quite mentioned:

exposing the irresponsible dishonesty of the switch as taught by fi360 and

mis-labeled “fiduciary.”

Now is the time to expose and bury this malpractice! Now, as promotion

of the fiduciary standard gains steam, friends of fi360 are attempting to have

this malpractice labeled “best practices” for investment “fiduciaries.”

Asset classes are defined and performance-measured by indexes. They

offer best grounds for future-performance estimates: decades of return-rate

history, and widest diversification. That’s why they are used for allocation –

allocation to asset classes defined and measured by indexes.

For execution of such allocations, placement of the client’s money,

there is ONE responsible, honest, fiduciary way: for each asset class, invest

in that asset class, defined and measured by its index, through an index fund

or ETF designed to match the performance of the asset class. That’s what robo Wealthfront

does.

Fi360 does the very opposite. Fi360 drops the standards,

years-of-history and diversification, letting in floods of Wall Street gambles,

which it calls “peers.” It trains and arms investment advisors to switch the

client from his selected asset classes, to gamble the client’s money on picks

from the flood of “peers” with greater risk and higher fees. And fi360 presents

this switch with the false appearance of faithful investment in the client’s

chosen asset classes.

For expose of this malpractice, see fiducio.com/the-switch.

Ever since introduction of this malpractice in software backed by names

of professors back in the 1990s, presented as if this malpractice were part of

MPT, the sellers of investment-advisor credentials have taught it; our community

of investment/finance professors has failed to blow the whistle and stop it; and

our many planners and advisors who know better have failed to blow the whistle

and stop it. Now, at last, robos such as Wealthfront will expose it — and gain

market share for doing so.

Dick Purcell

Considering robo software in place of current rebalancing software. Problem is no control over execution. I’d be weary of making large $$ trades as an open market order with robo when best practice is to call trading desk.

John,

Robo-advisors have their own responsibility for best execution (as they are functionally an RIA).

It’s not as though Betterment or Wealthfront are going to rebalance $2B of AUM with blind market orders and no due diligence about their own execution. At least, I really hope not, or they’re going to have their own issues the next time the SEC comes to review their execution practices on examination!

– Michael

Hi Michael,

Thanks for clarifying. The one I spoke with this week was not RIA (yet) and said all trades were market orders. That made me a little nervous!

To answer your post’s question, interest is there but need to be comfortable with execution, customization, integration, and cost.

– John

Michael – Just to keep this issue on the radar. I spoke to another robo platform who is an RIA with a focus on building branded platforms for advisors. They also said all orders are pushed out as market orders. I agree with you on best execution and wonder how this will all shake out for the robos and real advisors who use them.

John,

Wow, that’s a little scary. I wonder how long it will be before that robo platform feels compelled to step up its execution efforts. Hopefully not long…

– Michael

John or Michael – Who are the RIAs that are using robo platforms, that focus on building platforms w/Advisers / IARs ?

I’ve kept my eye on the robo-advisor technology for advisers, but have yet to be convinced to incorporate them. Until I know that the firm is truly profitable and can stand on its own without VC funds, I don’t want to make the effort to use one only to have it fold up!

Also, you mentioned the inability to process ACATs, which I was not aware of. A majority of my new clients involve at least one ACAT so that would be a huge issue. And the discussion highlights the use of market orders only, which is also concerning.

Consider me in the “curious but wait and see” category.

Michael – any update to the available options out there? Ideally I’d love full-service for all account sizes, with an ESG option for my socially responsible clients.

With this article being 5years old, I hope that Advisors have taken the step to implement a robo-advisor into their practices! Technology is ever-changing, and we need to be at the forefront of these changes and learn to adapt. A robo-advisor such as AdvisorEngine (www.advisorengine.com) is able to provide you with a well-rounded wealth management practice. Everything is done digitally, so you will not only be paperless, but you will be saving time and be more productive. Your clients can access their investment data at anytime, and you’ll get to do goal-based planning for all your clients. Robo-advisors are the way of the future, and we need to start embracing this technology!

The way you share the information is really amazing. In near future, I really want to read more on Investment Advisors in US. Thanks In Advance.