Executive Summary

After years of tepid increases in the average compensation of financial advisors, the latest bi-annual industry benchmarking studies from both Investment News and FA Insight reveal that the industry’s long-forecasted talent shortage appears to be taking hold.

According to the latest data, the average Paraplanner with 4 years of experience is earning total compensation of $65,000/year (with a nearly $60,000 salary base and 10% bonus potential), an experienced financial planner responsible for client relationships is earning $94,000/year with 8 years of experience, and Lead advisors who are skilled at developing new business are earning an average of $165,000/year, with the top quartile earning more than $250,000/year, and the top practicing partners earning nearly $500,000/year in a combination of salary, bonus incentives, and partnership profit distributions!

Of course, even within those numbers, there can be substantial regional variability. But still, financial advisor compensation across the board was up nearly 6.5%/year for the past two years – from paraplanners to lead advisors – with base salaries for financial advisors growing even faster, especially amongst the largest independent advisory firms that are both winning the bulk of new clients, and the most likely to be working with affluent clients (which generate the most revenue, and therefore allow their advisors to earn above-average compensation). And the demand for talent is leading to a rise in advisory firms attempting to poach advisors from other firms, a growing focus of large firms to build talent pipelines with colleges and universities, increasing use of third-party recruiting firms to hire even young financial planning talent, and a rise in the average time to hire a financial advisor to a whopping 4-6 months.

The trends may not be entirely surprising given that the overall financial advisory industry continues to see the total headcount of financial advisors decline a mere 1% to 2% per year. Yet with the number of CFP certificants actually up by nearly 50% in the past decade, perhaps the real challenge may not merely be a shortage of financial planning talent, per se, but the industry finally discovering that as investment management is increasingly commoditized and firms seek to add value through financial planning and wealth management as the “anti-commoditizer”, that the number of true financial planners was never enough to meet consumer demand in the first place?

The Latest Data On How Much Financial Advisors Make?

Every two years, the leading industry benchmarking studies – the “Investment News Advisor Compensation and Staffing Study” and the “FA Insight Study Of Advisory Firms: People And Pay” – release their bi-annual latest on the latest compensation trends for financial advisors.

Each study surveys 300+ advisory firms, with a concentration amongst independent RIAs, but including some registered representatives of broker-dealers and hybrid RIA/B-D advisors as well, and gathers detailed data on what advisory firms are paying all the possible roles within an advisory firm, from the investment team to the operations and administrative staff, and of course the financial advisors themselves.

When it comes to the financial advisor data in particular, the industry standard is to break up financial advisors into three core categories:

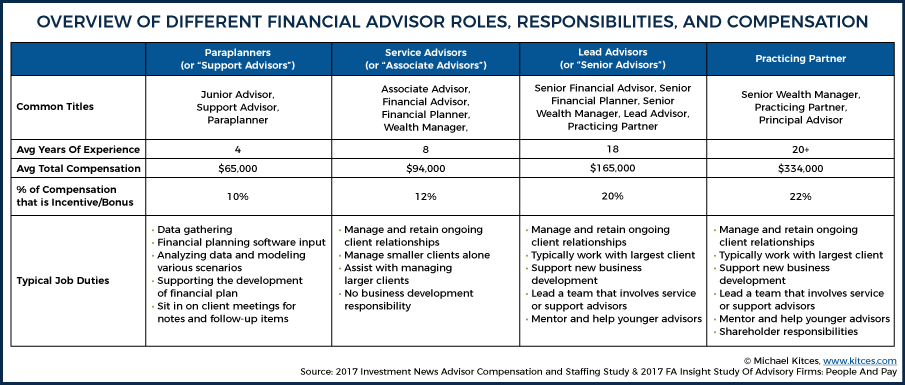

Paraplanners (or “Support Advisors”) – Provides support to more senior advisors in the firm, and is typically responsible for data gathering, financial planning software input, analyzing data and modeling various scenarios, and supporting the development of the financial plan. Paraplanners may also sit in on client meetings, typically to take notes and handle follow-up items, but are not responsible for actually delivering financial advice.

Service Advisors (or “Associate Advisors”) – Responsible for managing and retaining ongoing client relationships, either independently (for “smaller” clients) or in a co-advisor role with a lead advisor (for “larger” clients). While Service Advisors are expected to manage and retain relationships, they typically do not have responsibility for new business development.

Lead Advisors (or “Senior Advisors”) – Responsible for both managing and retainer ongoing client relationships (typically the “larger”, more complex, and most valuable clients of the firm), as well as developing new business for the firm. May lead a team that involves additional Service and/or Paraplanner support advisors as well, and often has an obligation/expectation to mentor and help develop those advisors as well.

According to the latest data, the “typical” paraplanner or Support Advisor has 4 years of experience, and now receives a total compensation of about $65,000, including 10% incentive compensation. Anecdotally, we find at New Planner Recruiting that starting salaries for Paraplanners appear to be approaching $50,000/year (albeit with adjustments for geographic location and cost of living).

Associate or Service advisors, given their higher level of responsibility for managing client relationships, have an average of 8 years of experience, and earn $94,000/year, of which about 12% is incentive compensation and bonuses.

And Lead financial advisors, given both their client relationship management and business development responsibilities, have an average of 18 years of experience, and earn an average of $165,000/year, of which nearly 20% of incentive/bonus compensation.

Notably, across the board, compensation is typically 80% to 90% in the form of a base salary, and only about 10% to 20% bonus or incentive compensation. Though there are a smaller subset of firms that pay their advisors primarily based on incentive compensation, and not based on a salary – primarily when it comes to Lead Advisors. For those advisors, average total compensation was substantially higher, at more than $200,000/year. With the caveat that if the market declines or growth slows down, that advisor may take a substantial income hit.

In fact, the most common forms of incentive compensation – both for incentive-heavy firms, and the ones that rely primarily on base salary and a more modest bonus structure – are typically tied to either total revenue managed, new revenue brought in, or firmwide bonus pools (typically again tied to total and new revenue). About 1/6th of firms base these bonuses on AUM rather than revenue, but most simply target revenue.

Of course, at firms where the Lead Advisors are also partners, they may take home substantial additional income for both their additional management responsibilities, and their share of partnership profits. According to the Investment News data, median income of a practicing partner was $247,000/year (including 22% of incentive compensation), and total compensation was $334,000/year including profit distributions, with a median of 20 years of experience.

Notwithstanding the broad industry averages, it’s also important to recognize that there is also a substantial skew in advisor compensation towards larger advisory firms. In part, this may simply be because larger firms tend to be located in metropolitan areas that have a higher cost of living (and the FA Insight authors explicitly emphasize that compensation levels should be adjusted based on local cost of living). In addition, larger advisory firms also tend to serve more affluent clients who pay more revenue per client, thus allowing Service and especially Lead advisors at larger firms to get paid more for the higher levels of revenue they manage.

Nonetheless, both the FA Insight and Investment News studies found that Lead advisor base salaries, in particular, are as much as 20%-30% higher in the largest advisory firms (with more than $8M of revenue) compared to “smaller” firms with just a few million in revenue. Though the difference is more slight for Service advisors, and not evident at all for Support advisors.

Gaining Experience And The Income Trajectory Of The Financial Advisor Career Track

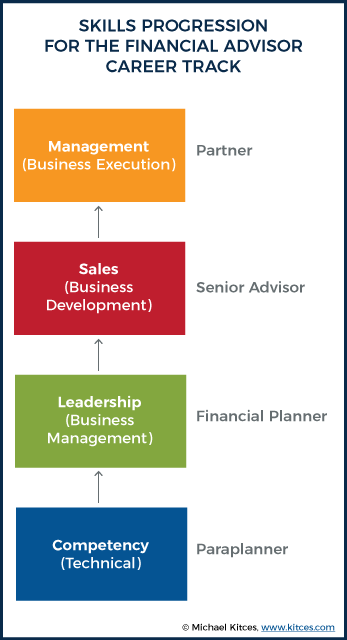

As the financial advisory industry continues to formalize its career tracks, a standard progression is emerging in how advisors can climb the career – and income – ladder.

As noted above, the starting point is the Paraplanner, who must learn the technical competency to master the job of supporting the financial planning process. Then in order to move up and become a full Financial Planner (Service Advisor) who delivers advice directly to client relationships that he/she manages, it’s necessary to learn the empathy and relationship management skills. From there, moving up to the next tier of being a Senior or Lead Advisor is all about learning the skill of new business development. And those who want to move to the very top of the pyramid as a partner must eventually master the skills of leadership and management to execute the business.

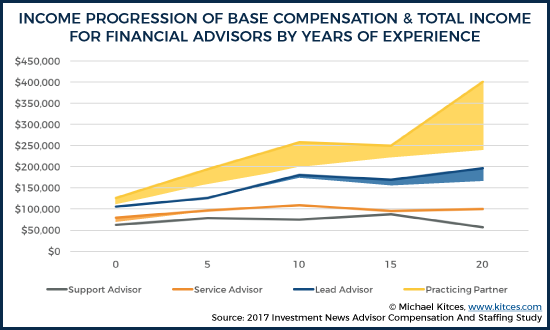

Thus, as the financial advisor gains experience in each of the four domains over time, income rises with improving skills, and then jumps further as the advisor masters the skills necessary to move up to the next tier. Accordingly, even the top paid (75th percentile) paraplanners with 8 years of experience only earn $72,000/year in compensation, while a full Associate Advisor with similar experience (but full responsibility for managing client relationships) typically makes more than $90,000/year.

On the other hand, it’s notable that once advisors are “fully” compensated for managing client relationships, increasing compensation further – above and beyond just raises for additional years of experience and a growing base of client revenue, that also tends to generate at least some moderate flow of new business through existing client referrals – is more and more reliant on “bonus” incentive compensation for going above-and-beyond when it comes to new business development (the essential skill to become a senior advisor). Accordingly, the typical compensation for Service or Lead advisors with 12 years of experience is around $116,000/year. But overall, the top tier of Lead Advisors earn a whopping $250,000 or more, with a heavy component of incentive compensation. (And as noted earlier, those who become practicing partners unlock even higher tiers of compensation.)

Which means that as years of experience increase, the range of compensation for financial advisors also widens dramatically, dictated primarily by the size of the advisor’s clients (and total revenue he/she is responsible for), and the advisor’s ability to develop business. Accordingly, while top-quartile Service advisors “only” earn about $25,000 more than the typical Service advisor, top-quartile Lead advisors earn almost $100,000 more than the typical lead advisor, and top-quartile Practicing Partners earn more than double a top-quartile Lead advisor (including both salary, incentive compensation, and partnership profit distributions) in the long run.

Nonetheless, the reality is that the income trajectory of paraplanners starting with total compensation around $50,000/year and averaging $68,000/year after 4 years is equivalent to an 8%/year raise. Similarly, being able to grow from $68,000/year to $97,000/year as the advisor moves from a paraplanner role with 4 years of experience to a Service advisor with 8 years is another 9%/year in income growth. And even in the progression to a lead advisor with 17 years of experience is associated with average annual growth rate in income of 6%/year, with upside potential for far, far more for those who can unlock their business development prowess.

Of course, these raises aren’t “automatic” for advisors who gain experience, as they are ultimately contingent on the ability of the advisor to master each skill domain and move up the career track ladder. Nonetheless, there are few industries with job opportunities that have a steady path of 6% - 9%/year raises that can continue unabated for a 20+ year career, and accelerate even faster if the key final skills – of business development and firm management/leadership – can be mastered! In fact, the upwardly mobile financial advisor who quickly climbs the career track has the potential to move from a $50,000 starting salary to a $250,000/year total income in 10 years, by mastering the successive skill domains that it takes to move up the line!

Though notably, advisors who do not continue to move up do eventually stagnate... as support advisors at 10 years of experience (who haven't moved up to service and lead advisors) make less than those at 5 years of experience, and service and lead advisors at 15 years of experience (who fail to master business development and become partners) make less than those at 10 years of experience!

The Emerging Talent Shortage For Financial Advisors

In recent years, there has been extensive discussion in the industry about the looming wave of retiring financial advisors, and the prospective talent shortage that it would create.

But notwithstanding these fears, the 2015 editions of both the Investment News and FA Insight compensation studies had shown only very modest increases in advisor compensation. Median compensation for Lead advisors had been up only 3.4% over the prior 2 years according to Investment News data, and up just 2.6%/year over the prior 6 years in the FA Insight study. Similarly, median compensation for Service advisors was rising at only 1.4% - 2% per year, and Support advisor compensation had been rising at barely 1%/year for the preceding 6 years!

However, the latest benchmarking data shows a substantial shift is underway. Between the Investment News and FA Insight data, the median compensation of Support Advisors leaped by almost 6.5%/year for the past 2 years since the 2015 versions of the studies! Service Advisor compensation rose by a similar 6.5%/year on average. And in the Investment News study, Lead Advisor compensation was also up by 6.7%/year, with salaries up by 11%/year as lead advisors were able to command a higher guaranteed base (albeit in exchange for less incentive compensation).

Notably, in the FA Insight study, the typical compensation for lead advisors actually declined since the 2015 study, but only because the average age and experience level of lead advisors declined as well (even though all the original advisors in the sample are 2 years older now!). Which suggests that firms are only paying “less” to Lead Advisors because the talent shortage is so severe they’re being forced to promote even younger lead advisors with fewer years of experience just to fill the void (but are able to pay them less thanks to the lower levels of experience). Accordingly, even in the FA Insight study, lead advisor compensation also shifted from 73% to 77% base salary, suggesting that advisors still have more pricing power than ever to demand a higher base compensation guarantee.

What all of this suggests is that after years of warnings, the talent shortage of financial advisors may finally be starting to play out. In prior years, lead advisor compensation was growing the fastest, likely on the back of both what was already a shortage of experienced advisors willing to switch firms, and a multi-year bull market that was lifting up lead advisors the most (since their compensation tends to have the most revenue-based incentive bonuses).

But now, the growth rate of Support and Service advisor compensation have leaped from a 6-year average of just 1% to 2%/year from 2009 to 2015, to a whopping 6.5%/year for the past two years. The trend appears to be driven by a subset of the largest independent advisory firms, that are experiencing accelerating growth as they scale their marketing efforts, and are rapidly hiring Support and Service advisors as quickly as they can.

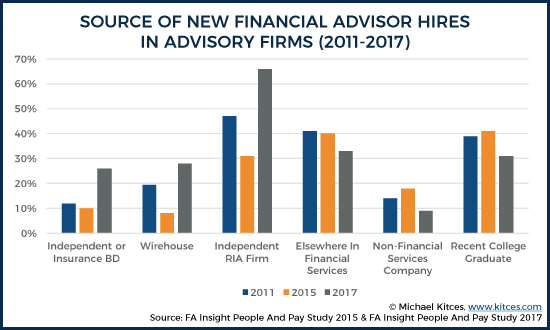

Accordingly, the Investment News data shows that 73% of “Super Ensemble” firms (those with $10M+ in annual revenue) were hiring for new advisor positions last year, and 24% still have unfilled positions. And the FA Insight data reveals that, after a slight pause in 2015, advisory firms are now seeking in full force to hire away from competing advisory firms, whether it’s wirehouses, independent broker-dealers, or especially other RIAs (though the most rapidly growing firms are also still the ones most likely to be targeting recent college graduates as well).

Of course, successful experienced financial advisors still have little incentive to make a move. In most cases, they’re either already working with an established client base they don’t want to leave, may be on a partnership track or succession planning path already, or if they don’t want to remain in their current firm, have the confidence and experience to simply go out and launch their own advisory firm and leverage the resources of an advisor support network (a path we commonly see at XY Planning Network).

Thus, Investment News reports that despite the hiring demand, advisory firms are still only seeing turnover of only 8.4% amongst Service advisors, 6% amongst Lead advisors, and just 2.1% amongst practicing partners, as the more experienced the advisor gets, the more likely they are to be established in their current firm! (Though as the earlier data showed, advisory firms are clearly feeling the pressure to give healthy annual raises to retain those advisors, too!)

The bottom line, though, is this means if you’re a “below-average-age advisor” – which at this point, still means any Gen X or Gen Y advisor under the age of 50(!) – the future prospects of advisor compensation are very bright, and we find through New Planner Recruiting that even college graduates are now seeing rapidly rising entry-level salaries as the competition for talent comes all the way down to paraplanners.

On the other hand, for advisory firms, the fight for talent in the midst of a substantial shortage will put even more pressure on advisory firm margins, and will be especially challenging for smaller firms that don’t have the depth to hire multiple young advisors in the hopes that at least one or two successfully develop into lead advisors down the road.

Or viewed another way, despite the fact that there are still about 300,000 “financial advisors” in the industry, the fact that barely 25% of them are CFP certificants suggests that, as investment management is increasingly commoditized and firms switch more and more to financial planning and holistic wealth management services as the “anti-commoditizer”, we’re just now discovering how much of a true financial planning talent shortage there really is!

In the meantime, any financial advisors who are interested in checking out the full benchmarking studies can go directly to the companies’ respective websites to purchase their copies of the “Investment News Advisor Compensation and Staffing Study” and the “FA Insight Study Of Advisory Firms: People And Pay”!

So what do you think? Is there really a talent shortage for financial planners? Will advisor compensation continue to increase at 6%+/year in the future? Is the shift being caused by the growing number of advisors who are retiring, or the rise of financial planning as technology commoditizes investment management? Please share your thoughts on the comments below!