Executive Summary

While the use of pensions as an employee benefit is on the decline, many of today’s workers nearing retirement have participated in a pension plan for the past several decades, and have already accumulated a significant pension benefit. And as those individuals begin to retire, they are faced with the classic decision of whether to keep the lifetime pension payments, or choose a lump sum instead.

While there are several factors that go into the pension-vs-lump-sum decision, ultimately the trade-off can be boiled down to calculating the internal rate of return (IRR) of the promised pension cash flows, which reveals the “hurdle rate” of return that a lump sum portfolio would have to earn to generate to reproduce those same payments over the same time horizon. Of course, the longer the retiree is expected to live, the greater the number of anticipated pension payments, and the greater the portfolio hurdle rate will be.

Ultimately, though, because life expectancy will vary by the individual, and in practice the size of a lump sum relative to a pension payments will also vary from one plan to the next (and also over time, as the GATT rate used to discount the pension payments fluctuates from month to month and year to year), the decision of whether to keep a pension or convert it into a lump sum will vary from one person to the next. In some cases, choosing a lump sum will clearly be best (e.g., when life expectancy is short or the hurdle rate is especially low), while in others there will be no way for a portfolio to generate similar cash flows without a significant amount of risk – at least, as long as the pension plan itself remains secure and isn’t facing a potential default or being forced to rely on PBGC backing!

Pension Versus Lump Sum Decision

Retirees who are eligible for a pension are often offered the choice of whether to actually take the pension payments for life, or instead to receive a lump sum dollar amount for the “equivalent” value of the pension – with the idea that the retiree could then take the money (rolling it over to an IRA), invest it, and generate his/her own cash flows by taking systematic withdrawals throughout retirement.

The upside of keeping the pension itself is that the payments are guaranteed to continue for life (at least to the extent that the pension plan itself remains in place and solvent and doesn’t default). Thus, whether the retiree lives 10, 20, or 30 (or more!) years in retirement, he/she doesn’t have to worry about the risk of outliving the money.

By contrast, selecting the lump sum gives the retiree the potential to invest, earn more growth, and generate even greater retirement cash flows… and if something happens to the retiree, any unused account balance that remains will be available to a surviving spouse or heirs. On the other hand, if the retiree fails to invest the funds for sufficient growth, there’s a danger that the money could run out altogether, and that a long-lived retiree may regret not having held on to the pension’s “income for life” guarantee.

Ultimately, though, whether it is really a “risk” to outlive the guaranteed lifetime payments that the pension offers by taking a lump sum depends on what kind of return must be generated on that lump sum to replicate the payments. After all, if the reality is that it would only take a return of 1% to 2% on that lump sum to create the same pension cash flows for a lifetime, there is little risk that the retiree will outlive the lump sum even if withdrawing from it for life. However, if the pension payments can only be replaced with a higher and much riskier rate of return, there’s also a greater risk those returns won’t manifest and the retiree could run out of money.

Calculating The Internal Rate Of Return (IRR) Of A Lifetime Pension

The necessary return that must be earned on a lump sum to replace the payments of a pension will depend on how long the pension payments are anticipated to last. After all, if the retiree passes away after just a year, technically even a -90% investment loss would still leave more money behind than taking the pension and having all payments cease in a year! On the other hand, for a retiree who lives to age 90 and beyond, collecting decades’ worth of payments, it may take a more significant return just to ensure the portfolio keeps up with what the pension would have guaranteed in the first place.

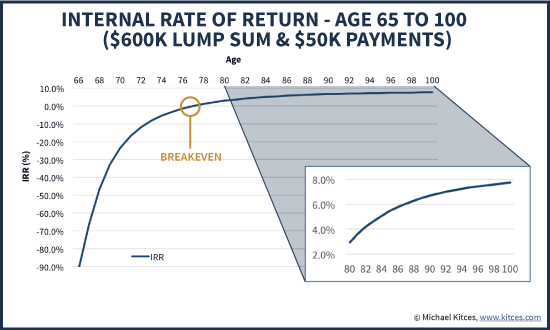

For instance, imagine that Jerry, a 65-year-old male, is eligible for a pension of $50,000/year (on his life only), or he can receive a lump sum payment of $600,000. How does Jerry choose?

Just looking at the simple math of the situation, if Jerry selects to keep his pension, it will take him 12 years just to get back the original lump sum he could have had on day 1 (where $50,000/payment x 12 payments = $600,000 lump sum). Of course, had he actually taken the lump sum, he would have been able to invest the money over those intervening years – which means even if he was actually taking $50,000/year all along, there would likely still be some money left over after 12 years as well (due to the growth on the remaining account balance as it was being spent down).

However, if Jerry lives to his (single male) life expectancy of age 82 – receiving payments for 17 years – his cumulative payments will add up to $850,000, spread over 17 years. By contrast, Jerry would have had to invest the lump sum at a 4.2% annualized growth rate for all those years to generate the same $850,000 of cash flows over time. In other words, if Jerry had taken the $600,000, withdrawn $50,000/year from it, while growing the remaining balance at 4.2%/year, he could have re-created the same cash flows for 17 years that the pension provided. Notably, Jerry “only” needs a 4.2% return, even though the pension is paying out $50,000/year on a $600,000 value (which is 8.3% of the account balance), because the reality is that a significant portion of each payment is not actually growth but simply a return of the original $600,000 principal; this is why it’s necessary to calculate an internal rate of return that accounts for both the growth and return-of-principal payments inherent in a pension payout.

Or viewed another way, by calculating the internal rate of return of the cash flows, we can determine the required rate of return - in essence, a "hurdle rate" of return - that Jerry would have to achieve over any particular time horizon for his lump sum such that withdrawals from the lump sum principal-plus-growth can replicate the same payments that the pension was providing for that same time period. The longer the time period, the more pension payments there are, and the higher the return Jerry must invest for - and actually achieve in the portfolio - in order to generate those same pension-equivalent cash flows as portfolio withdrawals from a $600,000 lump sum.

As the chart reveals, in this particular scenario the required rates of return to replicate what the pension provides are fairly modest in the early years, but get significant in the later years. To secure the pension payments until age 90, Jerry would need his portfolio to generate a 6.7% return. If Jerry lives to 100, he would have needed to grow the money at 7.7%/year to get the same $50,000/year-for-35-years payments that the pension was going to provide anyway.

In essence, then, the decision about whether or not to keep a pension is a form of risk/reward trade-off. If Jerry lives a long time, he gets a rather healthy implied rate of return for his lump sum – especially given that the pension payments are fixed and not subject to market volatility – but the value of those long-term returns are offset by the fact that if Jerry dies sooner rather than later, it can be the equivalent of losing 25%, 50%, or even 90% of the account value (as the pension payments can cease at death, even if only 1 payment was ever made!).

Lump Sum Vs Joint Survivor Pension Payouts

When it comes to a married couple, the dynamics of evaluating a (joint and survivor) pension versus a lump sum payout are slightly different.

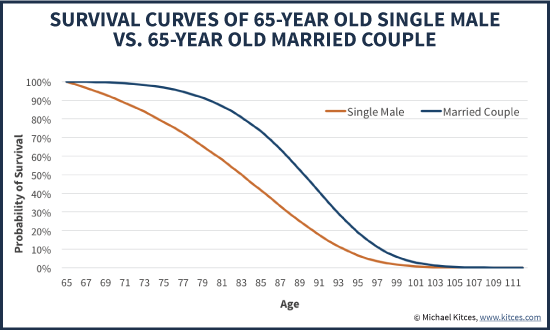

The good news is that with a joint pension, payments can continue for the lives of two spouses, and as long as either is alive, the payments can continue. This increases the likelihood that payments will continue, and reduces the risk of a ‘catastrophic’ loss where an untimely early death causes most or all of the value of the pension to be lost. For instance, the chart below shows the anticipated survival rate of a single 65-year-old male, versus the joint survival rate of a 65-year-old married couple. Simply put, the odds of both people passing away is much lower than either one individually, so the survival rates of a married couple are much higher (and life expectancy is much longer) than for an individual.

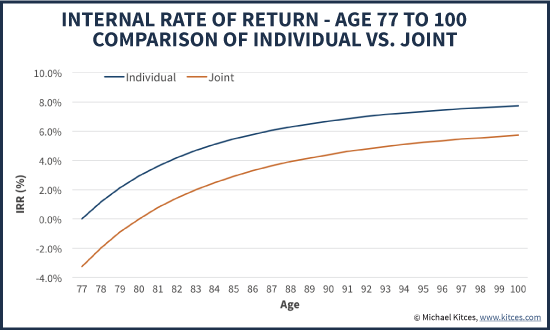

The bad news, however, is that pension providers also realize that there is a greater likelihood of making payments for a longer period of time with a joint pension payout – which is why the amount of the pension payments is typically reduced for joint and survivor pension payouts. For instance, continuing the earlier example, if Jerry’s pension offers a $50,000/year payment for the rest of his (individual) life, the payment might be reduced to $40,000/year as a joint payment over the combined lives of Jerry and his spouse.

In this joint pension scenario, the couple will now require 15 years of payments just to recover their principal (instead of only 12 years), though ultimately if they live to their (joint) life expectancy of age 88 (in 23 years), the internal rate of return is still about the same as the individual scenario (right around 4%). In other words, if the couple lives to their life expectancy, the required rate of return on the pension lump sum to replicate the pension payments is similar. But the couple has to live much longer just to reach life expectancy and get the similar internal rate of return as the individual payment, because the payments are already adjusted down in the first place in recognition of the higher survival probabilities of the couple.

Notably, the fact that the joint pension payout is inherently less risky over the time horizon means there’s also much less upside in the long run. As shown in the chart above, even when the couple lives into their 90s and out to age 100, the implied rate of return of the pension payments is diminished by the fact that there is a greater likelihood of the couple living that long in the first place!

Pension Maximization And Evaluating Pension Versus Lump Sum Trade-Offs

The challenge of trying to maximize the value of a pension is that ultimately, the “best” strategy will depend most heavily on the anticipated time horizon (i.e., anticipated life expectancy). Over short time horizons (i.e., an untimely death in the early years), taking a pension can result in outright “losses” compared to just selecting the lump sum, receiving a few payments, and then having the remainder left over (of course, some pensions offer "period certain" guarantees that ensure a certain number of payments are made, which reduces the downside risk, but at a 'cost' of getting smaller payments if the pensioner does survive!). On the other hand, over long time horizons (i.e., those who live well past their life expectancy), a lump sum might have to generate a relatively high rate of return (with all the risk that involves) just to keep up.

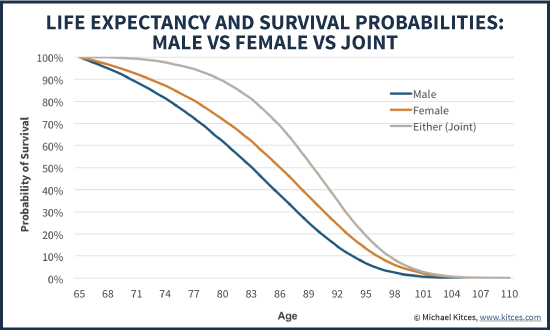

The fact that time horizon is so material means that first and foremost, the key factor to consider when evaluating pension-versus-lump-sum strategies is the anticipated life expectancy of the retiree. As a starting point, retirees can at least look at general life expectancy tables, and see at least the probable time horizon over which pension payments might be received. The chart below shows survival probabilities for a single male, a single female, and the joint survival probability that at least one of the two members of a couple are still alive.

In some cases, a retiree may have reason to know that his/her life expectancy situation will likely vary from the general case. Perhaps the retiree already has some health complications that will reduce anticipated life expectancy, tilting towards the decision to take a lump sum. Or perhaps the retiree has longevity in the family – and is still caring for two parents in their 90s! – suggesting that his/her own life expectancy may be well above average. Notably, being above-average income/wealth alone tends to be correlated with a life expectancy a few years beyond that of the general population.

Notably, though, while poor life expectancy significantly tilts the scales in favor of taking a lump sum, above-average life expectancy doesn’t necessarily mean that a pension will always be better. In some cases, the issue may be that one person’s life expectancy in a couple is above-average, but the other’s is not; in such cases, it may be better to take the single life pension payout, and buy life insurance with some or all of the higher payments, to protect the second spouse (a strategy often called “life insurance pension maximization” or “pension max” for short).

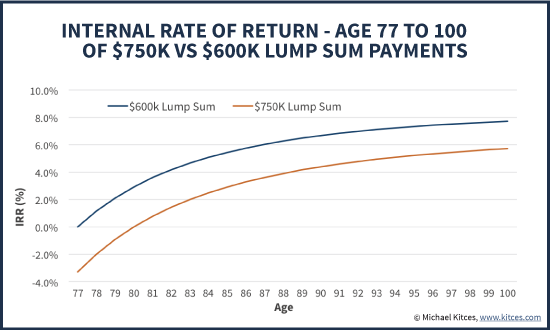

The biggest caveat for why a long life expectancy doesn’t always make a pension the winning choice is simply because some pensions have lump sums so “generous” that it is still relatively easy to generate a rate of return superior to the “hurdle rate” of the internal rate of return, even over a long payout time horizon. For instance, if Jerry’s pension offered a lump sum of $750,000 instead of just $600,000, the internal rates of return would be low enough that even if he lived under his 90s, a long-term investment portfolio would likely beat the required return threshold (and usually by a significant margin). Ironically (or perhaps not), the more generous the lump sum is up front, the more incentive there is to just take the lump sum, because it doesn't take much of a return on that lump sum to generate comparable pension-like payments from a portfolio.

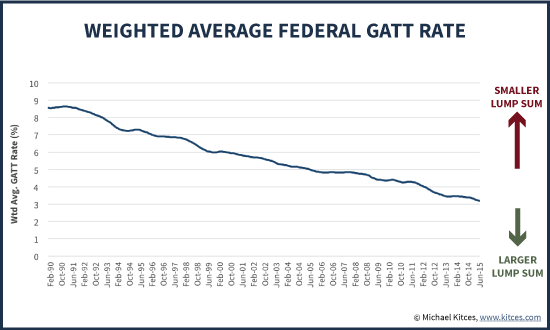

The Discount GATT Rate And Determining The Size Of A Pension Lump Sum

So what determines the size of a pension lump sum, and the associated internal rates of return? Ultimately, it comes down to the factors that each individual pension plan uses to calculate the conversion of its pension into a lump sum, including plan’s own life expectancy assumptions (which may be more or less favorable than the general population life expectancy tables), and the plan’s “discount rate” (the rate of return used in the plan calculations to calculate the lump sum amount).

The discount rate in particular is significant, because in higher interest rate environments, the higher discount rate translates directly to a higher internal rate of return that must be achieved, and similarly means that the lump sum pension amounts shrink; as a result, it becomes harder and harder to replicate the pension payments with a portfolio-plus-growth in higher rate environments. By contrast, though, lower discount rates will be associated with larger lump sums… which means in today’s lower interest rate environment, the discount rates have been especially favorable for producing larger lump sums that have easier-to-clear hurdle rates for the portfolio. For instance, the chart below shows the Federal GATT (General Agreement on Tariffs and Trade) rate, commonly used in many pension plans to calculate pension lump sums, which is at historic lows right now.

As the chart shows, with GATT rates at historic lows, pension lump sums will tend to be higher – resulting in personalized internal-rate-of-return targets that may be easier to achieve with a retiree’s portfolio. Though ultimately, the analysis of whether to take a pension or lump sum must still be done on an individual basis, taking into account not only the internal rates of return the lump sum must reach to match the pension, but again the retiree(s) and their own health and life expectancy.

And of course, in today’s environment where many private pension plans are underfunded, some retirees simply may not want to take the risk that the pension payments could be limited if the pension plan defaults. While the Pension Benefit Guaranty Corporation (PBGC) does provide backing to most corporate pension plans, the current maximum pension benefit the PBGC backs is “only” $60,136/year for an individual ($54,123 for a joint-and-50%-survivor payout), which means retirees with larger pensions could still be at risk for part of their payments. And sadly, many states have pension plans that are even more underfunded, and in the case of state/local government pensions, there is no PBGC backing at all. In these situations, retirees may wish to take a lump sum and the associated investment risk because it’s more appealing than the risk of the pension plan itself. In other words, pension payments may not be volatile like markets from day to day and year to year, but they can still have a material risk in some circumstances.

The bottom line, though, is simply this: the decision of whether to take a pension or lump sum is ultimately driven by the retiree’s ability to use the lump sum to re-create what the pension would have paid anyway. Depending on the retiree’s life expectancy, and the implied internal rate of return of the pension payments relative to the lump sum (and presuming the retiree can implement that lump sum portfolio investment appropriately, with the advisor's help), it may be relatively easy to create a comparable portfolio return to replace the pension payments, or not. The only way to know is to evaluate each, one by one!

This is an excellent article and it’s timely for me since I am working on this decision for a client today. Thanks!

I wonder how taxes might play a part in this decision. Assuming that the lump sum would get rolled into an IRA, then all pension annuity payments or IRA distributions would be taxed as ordinary income. But the individual would have more control over the amount of IRA distributions at least until age 70.5. I am trying to think of situations where it might benefit an individual to choose the pension annuity or lump sum for tax purposes. Thoughts?

Taxes are another good example of why this decision is not just a battle of the IRRs. Obviously, any client whose income level and tax bracket are expected to change in some way during retirement (whether in a smooth predictable way or in some sort of fluctuating or spikey way) would benefit from the flexibility of being able to regulate the timing of taxable income from qualified plans. There are dozens of reasons why this could be the case, and to some extent, they argue for the lump sum. Another argument is that RMDs occur on an accelerating scale, while pension payments are usually flat, so that taking a lump sum and putting it into an IRA allows you to defer taxation longer — which could make a big difference if you don’t actually need the monthly pension income to live on and are already in a high tax bracket. On the opposite side, a typical person in the middle-income range might be in a zero or 10% marginal tax bracket and therefore would probably be better off smoothing out their taxable income so as to keep themselves out of a higher bracket late in life when RMDs can get quite large; this would argue for keeping the pension benefit.

The exercise may become moot for many pension plans since Treasury and IRS are curtailing the option for many pension plans http://www.forbes.com/sites/ashleaebeling/2015/07/14/treasury-curtails-lump-sum-payouts/ IRS Notice 2015-49 http://www.irs.gov/pub/irs-drop/n-15-49.pdf

Yes, but those regulations apply only to people already receiving pension payouts, and arguably only for those already over age 70-1/2. These decisions most often involve people who are terminating from employment, and some plans actually offer lump sums as a standard option at retirement. Michael’s analysis appears directed mainly to this younger crowd.

Notice states: “The regulations, as amended, will provide that qualified defined benefit plans generally are not permitted to replace any joint and survivor, single life, or other annuity currently being paid with a lump sum payment or other accelerated form of distribution.” It is not age specific, however the notice does reference the Required Beginning Date associated with RMD rules, and that changes after RBD are not allowed unless an exception applies. This would mean for those younger than 70 1/2 in general. Main point though is that these offers will likely be curtailed as a result. “These arrangements are sometimes referred to as lump sum risk-transferring programs because longevity risk and investment risk are transferred from the plan to the retirees.” Treasury and IRS are not in favor of transferring risk from pension to retiree is the main takeaway. After 9 July 2015, I would tread carefully on a pension lump sum option making sure the company is indeed able to make such an offer without running afoul with this revision. http://www.irs.gov/pub/irs-drop/n-15-49.pdf

Larry,

You cited the key part in the middle of the first sentence: “currently being paid”. The ruling isn’t about lump sums AT retirement. It’s about pension plans that want to get off the hook of being underfunded by offering current retirees a chance to ‘buy out’ their pension with a (potentially reduced) lump sum.

I’ll be digging further into the Notice and writing about it for the blog in another week or two, and maybe will uncover more. But as far as I’m aware – and from what you quoted yourself – this is primarily about people who ALREADY chose pension over lump sum, and now try to go BACK and commute the pension into a lump sum AFTER the original election.

– Michael

Indeed … and most plans are paying benefits well before age 70 1/2 which is my not-so-well stated point. Agreed, it is for those already receiving benefits – and I’ve had more than a handful of clients receive offers for lump sum buyouts once on benefits. My reading of the notice is that the ruling is clamping down on the company efforts to transfer the risk – not so much an employee trying to go back on their election. In either case, the option of lump sum goes away once benefits start regardless. So it becomes an irreversible decision AT retirement regardless of whether employee or employer would like to do something else later. The notice also has some interesting references in the footnote as to intention and rationale. Agreed, until one retires and makes the now irrevocable election, the choice is still available – so far. Seems to be integrated with the QLAC option, although unstated. It will be interesting to see if those choices AT retirement may be undone once retired too. The main point I take from it all is who is on the hook for future income risk? Company or retiree?

What you uncover in your future post will be interesting.

It’s also worth keeping in mind that if an employer is completely terminating a plan, as opposed to simply “derisking it”, the Dept. of Labor rules on terminations would almost certainly take precedence, and lump sum offers COULD be made even to retirees already in pay-out status. You’re right of course, that the IRS ruling will to some significant extent curtail some of the kinds of offers that people have been getting recently, though, and it’s a point worth noting.

Michael, we have a client in this very situation. One question I have is the risk of antiselection i.e. that the unhealthy will disproportionately take the lump sum and put those that stay in the plan more at risk for a default.

This is a very helpful analysis, but the idea that the decision can be boiled down to an IRR and a hurdle rate ignores the reality that these decisions are made in a real-life environment where not just a few, but a dozen or more other issues can affect or even determine the decision. One reason for that is that there are a lot of things you can do with a lump sum other than roll it over into another qualified plan. Just to throw one example out there, a certain person might be able to use the funds to get job training that would enable her to double her income over the next 10 years, producing a rate of return way better than the IRR of any pension plan or IRA. Conversely, someone else might be a soft touch, and end up giving away most of his lump sum to importunate children, churches, or charities, and even a truly superior return on an IRA would be moot. Retirement is only incidentally about math. It’s mostly about non-financial realities, many of which (directly or indirectly) have significant financial consequences.

Chuck, this is so important. I have many clients that face this decision (from the same employer), and in every case, the discussion is different due to life circumstances, financial circumstances, etc. As you said, it cannot simply be boiled down to an IRR analysis. In my case, the IRR’s are often very good (even in our current rate environment), so I make it clear that the ash flow they are being offered cannot be replicated (on a guaranteed or even probable basis) with private investment (or a SPIA or LB rider). That being said, many clients still opt for the lump-sum; due to fear, greed, comfort, etc. Or, in many cases, clients already have plenty of guaranteed income and low living costs, and would prefer to use the funds as they see fit.

What was the return of the S & P 500 during the Great Recession? What happened to the invested capital during this historically long period of very, very low interest rates? During such periods the invested capital is subject to massive reduction which is exacerbated by the fixed withdrawals. A DB plan can weather the storm because of the annual additions to the plan—there are no annual additions in a rollover to IRA scenario. This makes the pension fund payout the superior choice.

Pension Max is designed to generate income for the insurance company and their network of sales people. If it is a bad idea for the pension plan member to take the lump-sum it is equally as hazardous for the beneficiary to invest the proceeds of a life insurance policy.

If you do not want to outlive your lump-sum investment take your pension payout and sleep at night.

Bogleheads’ Wiki has a very good article on this.

https://www.bogleheads.org/wiki/Lump_sum_vs_pension

I think Michael’s article misses the point that the lump sum is a windfall and may be squandered.

Keith

Keith,

Although I know a number of consumers read these articles directly, nominally my primary audience is advisors – and for better or worse, we already presume that one of our roles in working with clients is to help them implement these strategies responsibly, and not squander a lump sum.

Though you have a fair point that even as advisors, we need to know our clients and their ability to implement responsibly. I’ve added a brief note accordingly to the article. 🙂

Thanks!

– Michael

I didn’t read all of the comments. I would like to make 1 comment on the decision to take a lump sum or pension pay-outs. Obviously you have to run the numbers first. But, what if there was a common accident where husband and wife passed. Pension is gone. I’ve never seen a pension pass to the kids. If they did, I would bet that company will have some financial problems moving forward. I personally would like to take control of my money. Companies are not creating new pensions, in fact they are going away. They are a large strain on a companies cash flow. Part of that is not due to pension investment management, but the fact we are living longer. At the end of the day, it is a personal decision.

As an individual investor with a fairly significant nest egg, I am leaning toward payout vs monthly payments for exactly the reasons that Bob and Chuck mentioned. This money will stay in my estate and I can spend as needed and fluctuate with RMD’s. I will not squander just because I have a balance available. I understand the concept of 4%, 5% and 6% withdrawals along with the fluctuation of the market.

Thanks for a great article Michael and for the interesting input from the other planners. Signed Happy I started investing at 24YO

Joel,

I have to agree. If the numbers are even remotely close, I’m going with the pension. It’s just too risky, unless the client already has enough assets to make it impossible to run out of money even without a pension. I hate to imagine the stress of managing the cash flow during a prolonged bear market — for the client and me.

Mike

Same here Rob, we received a phone call today from a client facing this decision. Very thought provoking article. One comment Michael, going forward for those clients it applies to we’ll also need to compare Joint Life comparisons for same-sex spouses (Male/Male, Female/Female), as the life expectancy calculations may provide different results than for traditional comparison of Single vs. Joint Life (male/female).

Good point Landon! I’ll look at posting some updated same-sex-couples tables at some point here. Interesting implications, especially given that male/male couples have lower joint life expectancy than a male/female couple, and that female/female couples go the opposite direction with a longer expectancy…

– Michael

If memory serves, private pensions must use the same life expectancy table for all plan participants (i.e., no gender discrimination). Since women have longer life expectancies this means the annuity will often be a better deal for them, while for men it is often better to take the lump-sum and shop elsewhere (obvious overgeneralization here :-).

Yep. That is why we kept our DBP as a female couple. We would have had to pay out much more to buy an equivalent immediate annuity than the lump sum that was offered.

Michael, isn’t the analysis of whether to buy a SPIA very similar to this? In the one case, one decides whether to *accept* a lump sum in return for payments, and in the other, one decides whether to *give up* a lump sum in return for payments. In either case, the choice is between having the lump sum and receiving payments. The biggest differences, I think, are the source of the payments — a company or government vs. an insurance company — and the associated guarantor — the PBGC vs. the state.

Neal is spot on. This attempt to try to play actuary probably isn’t the right way to go because it always comes down to picking some random age to compute and 1 year of age difference in the statistically mean life expectancy you have for someone can make a huge difference.

Instead lump sum analysis should start by taking the income stream and running it through a SPIA quote estimator like http://www.annuityquickquote.com/ (not affiliated… first result on Google and don’t have to “talk to anyone”) and then compare the lump sum spread to ascertain how good of a deal lump sum valuation is against the market (i.e. SPIA’s are the market and your analysis is just your arbitrary analysis).

From there if it lines up close to the SPIA pricing than the decision becomes typical SPIA vs. Safe Withdrawal Rate… like any other client coming to you with money. If there is a large spread in the sums (pension income being a lot better than market valued lump sum of that stream) then you factor that into the consideration. I.e. if SPIA is 30% higher lump sum than Pension Lump Sum than you need to compare that to how much you value SPIA vs. SWR to determine whether the relative value is sufficient to change the picture.

I frequently use the hurdle rate approach when analyzing pension payments for clients. Most that I have seen of recent are in the 4.5-5.5% range on joint and 50 & 75 options. I usually use a 10-20% threshold when estimating life expectancy for the clients.

My question for Michael (or others) that I struggle with when running the analysis is that a 4.5-5.5% hurdle rate is relatively low when comparing it to a diversified portfolio that we could put the lump sum into. However this is not really an “apples to apples” comparison because the pension plan is more or less an investment grade corporate bond, especially if the plan is fully funded, backed by tax revenue, etc. Now you should (at least on a theoretical/comparable risk basis) be saying to yourself: “can I structure an IG portfolio to earn the client 4.5-5.5% overtime?” that becomes a stickier issue. However, maybe this comparison is more academic because in reality the lump sum will go into a diversified portfolio. I didn’t really see this addressed in the above article and would like to hear your thoughts or if you even think this is relevant to think about when doing the analysis.

Most DB holdings have at least 50 percent in common stock. This is why they have wiped out all of their sustained losses in the great bear market of 2007-08. During this period the SP 500 lost 50 percent of its value.

If both the lump-sum and the DB plan have the same investment holdings the person who elected the lump-sum is still way behind because of the fixed monthly withdrawals. THIS FACT IS THE GAME CHANGER AND SHOULD BE ADDRESSED BY MICHAEL.

How is Cost of Living Adjustment factored into this as well? It would seem purchasing power erosion will require a lower hurdle rate over time.

Greg,

The calculations here were based on nominal (flat) pensions.

You could do the same analysis for a pension with a cost-of-living adjustment (and some assumed inflation rate for how it will adjust). Though as you imply, yes all else being equal a pension that ALSO has a COLA attached will end out with higher hurdle rates to clear than one without.

– Michael

Michael,

We recently had a client, about to retire, who was given the choice between a pension or a lump sum distribution from his plan. The pension was clearly a much better choice actuarially. Yet he chose the lump sum because he was worried about the solvency of the plan in the future.

I just don’t get it. I thought a DB approach is superior to a DC approach. With that said, why would you want to convert your personal payout, at retirement, from a DB payout to a DC payout? Why would you want to take on all the risks that are now borne by the DB plan? While lump sum settlements are available from DB plans we have DC plans offering their participants a life annuity. Like I said—I just don’t get it.

With that said, public employees are being targeted by the Pension Max salespeople. The Utah retirement system has done its clients a GREAT service by publishing a research paper on the Pension Max concept. Anyone who is seriously contemplating take a lump-sum settlement or electing Pension Max in lieu of survivorship option must read this paper which can be downloaded on the website of the Utah Retirement System.

Because with some DB plans, their payouts are literally SO bad you could stuff the money in your mattress for the next few decades, dole out wads of cash to yourself, and have more income. And for many, you could buy nothing but government bonds for the rest of your life, and get a payout.

Granted, many DB plans have quite reasonable payouts, and then the trade-off wouldn’t be compelling. But that’s the ENTIRE POINT of this article. If you don’t do the analysis, you’ll never know…

– Michael

Michael,

If the DB plan has a dismal formula payout then the lump-sum settlement is proportionately dismal. My analysis remains—please see my first post.

Joel

Joel,

Not true at all. What DEFINES a dismal payout is actually that the lump sum settlement is generous.

If two pensions pay $50,000/year, and (A) has a lump sum of $500,000, and (B) has a lump sum of $1,000,000, then by definition (B) has a dismal payout BECAUSE it has a generous lump sum. That’s a directly inverse mathematical relationship.

– Michael

I disagree. The lump-sum is the present value of future pension payments. If the guaranteed pension payout is dismal then it stands to reason that the present value (lump-sum) of those future payments is dismal.

With that said, based on the plan’s actuarial assumptions two DB will calculate two different present values or lump-sums even though they both guarantee a $50,000 annual pension. i.e.; One DB plan needs a pension reserve of 12 times the $50,000 ($600,000) to guarantee a 55 year old his $50,000 pension while another DB plan requires a pension reserve of 11 times or $550,000.

Joel,

Your statement would be true if every pension plan always universally used the same perfectly risk-adjusted discount rate to calculate their lump sum.

Unfortunately, that assumption is quite false in practice. Pension plan lump sums are often calculated with discount rates based on plan documents written literally decades ago, and may or may not bear resemblance to the risk-adjusted reality of the plan or its payments.

In fact, the whole reason why some pension payments are more ‘valuable’ than others is the fact that an individual’s own risk-adjusted discount rate for that lump sum could in fact be higher or lower than what the plan ACTUALLY uses to determine the lump sum payment.

– Michael

A plan will run afoul of the IRS/DoL Regs if they are using actuarial factors adopted “literally decades ago”. This practice was outlawed in 1974—-see ERISA!

Good article and starting point in evaluating this decision in isolation, which helps when presenting to client. Starting with a SPIA quote for comparison is also helpful.

Of course have to consider in conjunction with overall planning — expected compounded return on lump sum reinvestment (challenging today), risk capacity & preferences of the client, return sequence risk, coordination of other income streams or cash inflows (Social Security timing, deferred comp payouts, other pensions, NQSO exercise, etc.), and tax planning/smoothing.

Every client and plan is different. You have to run the numbers and deliver customized advice and not take an unwavering, simple-minded approach to what is a significant and irrevocable decision for many.

Has anyone seen estimates on what the new mortality table will approximately do to increase pension lump sums in 2016?

An excellent article and follow-up discussion, and I thank you very much for it. I realize that the target audience is financial advisors, but I am an individual consumer wrestling with this decision who had no problems at all following your logic. What led me to this article was struggling to understand why 95% of my co-workers (high tech engineering and scientific community with advanced degrees, so people who thrive on numbers and formulas) take a lump sum, when I keep looking at the numbers from various different angles and can’t make anything but pension make any sense. As one commentator concluded, it must be greed or arrogance. Regardless, thanks for the reassurance that my reasoning is sound, and that more than a few professionals have drawn similar conclusions.

Very nice explanation. I’m faced with this very decision as we speak. 55 yrs old. Can get $3,077 a month in April 2016 lifetime or take a lump of $472K. I’ve tried figuring out the lump sum factors they used but it’s pretty confusing. I’m thinking that 472 will be pre-tax too. One simple calculation with what I’ve stated I came up with an IRR of 6.5%. That assumes a ~ 27 yr lifespan (male, single)

My choice at this moment is to take ~$205/month, taxable, for my life, whether it be 2 days or 30 years, or about $36K in a lump sum, which can be rolled over and invested tax-free until when-or if-I need it. Taking it as a pension means there’s something there, guaranteed, for heirs. If I use Clark Howard’s (monthly pension x 12)/lump sum, I get 6.77%, which his article states is above his threshold of 6%, which would point to taking the monthly pension. However, that doesn’t factor in the tax aspect. When one deducts the 20% tax withholding, then the calculation drops below 6%. His calculation also fails to account for the “time value of money,” i.e. a dollar today – in this case – about $36K – is worth more than $205/month. Using this calculation, what I would need to earn on the $36K is <3% provided I live into my 80s. It seems to me, even though my health is good, and I don't have any imminent concerns about the company's ability to pay the pension, that the lump sum is better.

Michael, Thank you for this very thorough and educational analysis . I am deciding Lump Sum vs Pension at this very time and the clarity of the definition of the “hurdle rate” with the life expectancy sensitivities is really helpful. I am currently waiting for the August 2019 IRS NPV segment rates to come out and they appear to be moving favorably for a lump sum. So then the question for my financial advisor is can we beat the hurdle rates. I prefer to control my own monies. My wife and I have been excellent money savers/managers and she also has a defined benefit pension vs lump sum decision in a few years.