Executive Summary

While the standard rule-of-thumb is that financial advisors charge 1% AUM fees, the reality is that as with most of the investment management industry, financial advisor fee schedules have graduated rates and breakpoints that reduce AUM fees for larger account sizes, such that the median advisory fee for high-net-worth clients is actually closer to 0.50% than 1%.

Yet at the same time, the total all-in cost to manage a portfolio is typically more than “just” the advisor’s AUM fee, given the underlying product costs of ETFs and mutual funds that most financial advisors still use, not to mention transaction costs, and various platform fees. Accordingly, a recent financial advisor fee study from Bob Veres’ Inside Information reveals that the true all-in cost for financial advisors averages about 1.65%, not “just” 1%!

On the other hand, with growing competitive pressures, financial advisors are increasingly compelled to do more to justify their fees than just assemble and oversee a diversified asset allocated portfolio. Instead, the standard investment management fee is increasingly a financial planning fee as well, and the typical advisor allocates nearly half of their bundled AUM fee to financial planning services (or otherwise charges separately for financial planning).

The end result is that comparing the cost of financial advice requires looking at more than “just” a single advisory fee. Instead, costs vary by the size of the client’s accounts, the nature of the advisor’s services, and the way portfolios are implemented, such that advisory fees must really be broken into their component parts: investment management fees, financial planning fees, product fees, and platform fee.

From this perspective, the reality is that the portion of a financial advisor’s fees allocable to investment management is actually not that different from robo-advisors now, suggesting there may not be much investment management fee compression on the horizon. At the same time, though, financial advisors themselves appear to be trying to defend their own fees by driving down their all-in costs, putting pressure on product manufacturers and platforms to reduce their own costs. Yet throughout it all, the Veres research concerningly suggests that even as financial advisors increasingly shift more of their advisory fee value proposition to financial planning and wealth management services, advisors are still struggling to demonstrate why financial planning services should command a pricing premium in the marketplace.

How Much Do Financial Advisors Charge As Portfolios Grow?

One of the biggest criticisms of the AUM business model is that when financial advisor fees are 1% (or some other percentage) of the portfolio, that the advisor will get paid twice as much money to manage a $2M portfolio than a $1M portfolio. Despite the reality that it won’t likely take twice as much time and effort and work to serve the $2M client compared to the $1M client. To some extent, there may be a little more complexity involved for the more affluent client, and it may be a little harder to market and get the $2M client, and there may be some greater liability exposure (given the larger dollar amounts involved if something goes wrong), but not necessarily at a 2:1 ratio for the client with double the account size.

Yet traditionally, the AUM business has long been a “volume-based” business, where larger portfolios reach “breakpoints” where the marginal fees get lower as the dollar amounts get bigger. For instance, the advisor who charges 1% on the first $1M, but “only” 0.50% on the next $1M, such that the with double the assets does pay 50% more (in recognition of the costs to market, additional service complexity, and the liability exposure), but not double.

However, this means that the “typical financial advisor fee” of 1% is somewhat misleading, as while it may be true that the average financial advisory fee is 1% for a particular portfolio size, the fact that fees tend to decline as account balances grow (and may be higher for smaller accounts) means the commonly cited 1% fee fails to convey the true sense of the typical graduated fee schedule of a financial advisor.

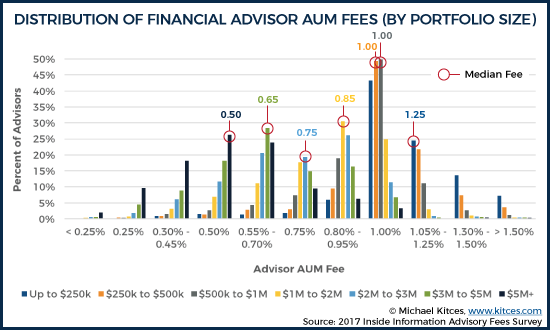

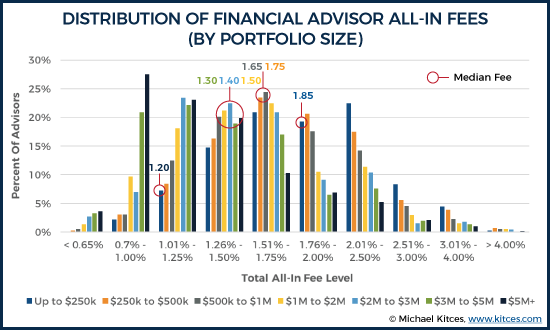

Fortunately, though, recent research by Bob Veres’ Inside Information, in a survey of nearly 1,000 advisors, shines a fresh light on how financial advisors typically set their AUM fee schedules, not just at the mid-point, but up and down the scale for both smaller and larger account balances. And as Veres’ research finds, the median advisory fee up to $1M of assets under management really is 1%. However, many advisors charge more than 1% (especially on “smaller” account balances), and often substantially less for larger dollar amounts, with most advisors incrementing fees by 0.25% at a time (e.g., 1.25%, 1.00%, 0.75%, and 0.50%), as shown in the chart below.

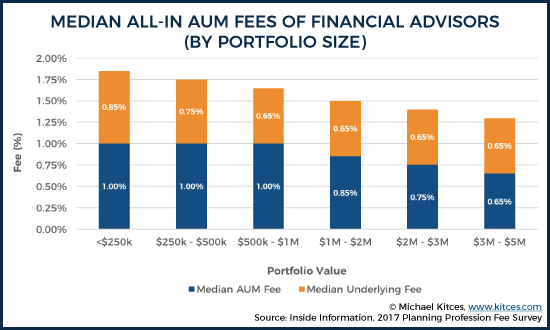

More generally, though, Veres’ research affirms that the median AUM fee really does decline as assets rise. At the lower end of the spectrum, the typical financial advisory fee is 1% all the way up to $1M (although notably, a substantial number of advisors charge more than 1%, particularly for clients with portfolios of less than $250k, where the median fee is almost 1.25%). However, the median fee drops to 0.85% for those with portfolios over $1M. And as the dollar amounts rise further, the median investment management fee declines further, to 0.75% over $2M, 0.65% over $3M, and 0.50% for over $5M (with more than 10% of advisors charging just 0.25% or less).

Notably, because these are the stated advisory fees at specific breakpoints, the blended fees of financial advisors at these dollar amounts would still be slightly higher. For instance, the median advisory fee at $2M might be 0.85%, but if the advisor really charged 1.25% on the first $250k, 1% on the next $750k, and 0.85% on the next $1M after that, the blended fee on a $2M portfolio would actually be 0.96% at $2M.

Nonetheless, the point remains: as portfolio account balances grow, advisory fees decline, and the “typical” 1% AUM fee is really just a typical (marginal) fee for portfolios around a size of $1M. Those who work with smaller clients tend to charge more, and those who work with larger clients tend to charge less.

How Much Do Financial Advisors Cost In All-In Fees?

The caveat to this analysis, though, is that it doesn’t actually include the underlying expense ratios of the investment vehicles being purchased by financial advisors on behalf of their clients.

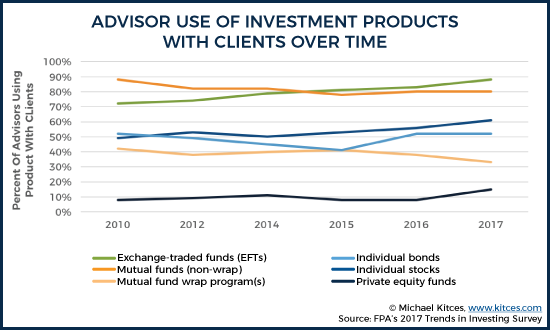

Of course, for those who purchase individual stocks and bonds, there are no underlying wrapper fees for the underlying investments. However, the recent FPA 2017 Trends In Investments Survey of Financial Advisors finds that the overwhelming majority of financial advisors use at least some mutual funds or ETFs in their client portfolios (at 88% and 80%, respectively), which would entail additional costs beyond just the advisory fee itself.

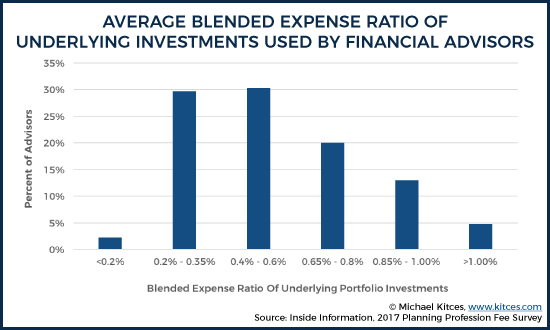

Fortunately, though, the Veres study did survey not only advisors’ own AUM fee schedules, but also the expense ratios of the underlying investments they used to construct their portfolios. And as the results reveal, the underlying expense ratios add a non-trivial total all-in cost to the typical financial advisory fee, with the bulk of blended expense ratios coming in between 0.20% and 0.75% (and a median of 0.50%).

Of course, when it comes to ETFs, as well as the advisors who trade individual stocks and bonds, there are also underlying transaction costs to consider. Fortunately, given the size of typical advisor portfolios, and the ever-declining ticket charges for stock and ETF trades, the cumulative impact is fairly modest. Still, while most advisors estimated their trading costs at just 0.05%/year or so, with almost 15% at 0.02% or less, there were another 18% of advisors with trading costs of 0.10%/year, almost 10% up to 0.20%/year, and 6% that trade more actively (or have smaller typical client account sizes where fixed ticket charges consume a larger portion of the account) and estimate cumulative transaction costs even higher than 0.20%/year.

In addition, the reality is that a number of financial advisors work with advisory platforms that separately charge a platform fee, which in some cases covers both technology and platform services and also an all-in wrap fee on trading costs (and/or access to a No-Transaction-Fee [NTF] platform with a platform wrapper cost). Amongst the more-than-20% of advisors who reported paying such fees (either directly or charged to their clients), the median fee was 0.20%/year.

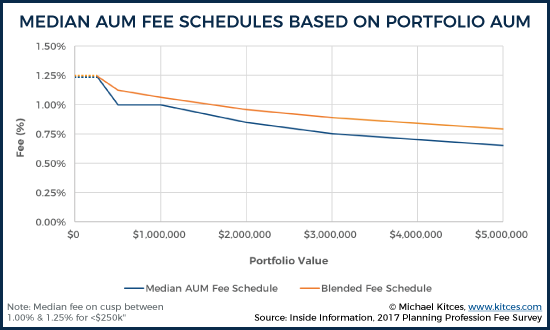

Accordingly, once all of these various underlying costs are packaged together, it turns out that the all-in costs for financial advisors – even and including fee-only advisors, which comprised the majority of Veres’ data set – including the total cost of AUM fees, plus underlying expense ratios, plus trading and/or platform fees, are a good bit higher than the commonly reported 1% fee.

For instance, the median all-in cost of a financial advisor serving under-$250k portfolios was actually 1.85%, dropping to 1.75% for portfolios up to $500k, 1.65% up to $1M, and 1.5% for portfolios over $1M, dropping to $1.4% over $2M, 1.3% over $3M, and 1.2% over $5M.

Notably, though, the decline in all-in costs as assets rise moves remarkably in-line with the advisor’s underlying fee schedule, suggesting that the advisor’s “underlying” investments and platform fee are actually remarkably stable across the spectrum.

For instance, the median all-in cost for “small” clients was 1.85% versus an AUM fee of 1% (although the median fee was “almost” 1.25% in Veres’ data) for a difference of 0.60% - 0.85%, larger clients over $1M face an all-in cost of 1.5% versus an AUM fee of 0.85% (a difference of 0.65%), and even for $5M+ the typical total all-in cost was 1.2% versus a median AUM fee of 0.5% (a difference of 0.70%). Which means the total cost of underlying – trading fees, expense ratios, and the rest – is relatively static, at around 0.60% to 0.70% for advisors across the spectrum!

On the one hand, it’s somewhat surprising that as client account sizes grow, advisors reduce their fees, but platform fees and underlying expense ratios do not decrease. On the other hand, it is perhaps not so surprising given that most mutual funds and ETFs don’t actually have expense ratio breakpoints based on the amount invested, especially as an increasing number of low-cost no-load and institutional-class shares are available to RIAs (and soon, “clean shares” for broker-dealers) regardless of asset size.

It’s also notable that at least some advisor platforms do indirectly “rebate” back a portion of platform and underlying fees, in the form of better payouts (for broker-dealers), soft dollar concessions (for RIAs), and other indirect financial benefits (e.g., discounted or free software, higher tier service teams, access to conferences, etc.) that reduces the advisor’s costs and allows the advisor to reduce their AUM fees. Which means indirectly, platforms fees likely do get at least a little cheaper as account sizes rise (or at least, as the overall size of the advisory firm rises). It’s simply expressed as a full platform charge, with a portion of the cost rebated to the advisor, which in turn allows the advisor to pass through the discount by reducing their own AUM fee successfully.

Financial Advisor Fee Schedules: Investment Management Fees Or Financial Planning Fees?

One of the other notable trends of financial advisory fees in recent years is that financial advisors have been compelled to do more and more to justify their fees, resulting in a deepening in the amount of financial planning services provided to clients for that same AUM fee, and a concomitant decline in the profit margins of advisory firms.

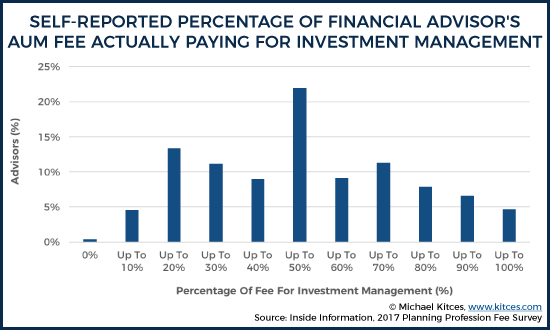

To clarify how financial advisors position their AUM fees, the Veres study also surveyed how advisors allocate their own AUM fees between investment management and non-investment-management (i.e., financial planning, wealth management, and other) services.

Not surprisingly, barely 5% of financial advisors reported that their entire AUM fee is really just an investment management fee for the portfolio, and 80% of advisors who reported that at least 90% of their AUM fee was “only” for investment management stated it was simply because they were charging a separate financial planning fee anyway.

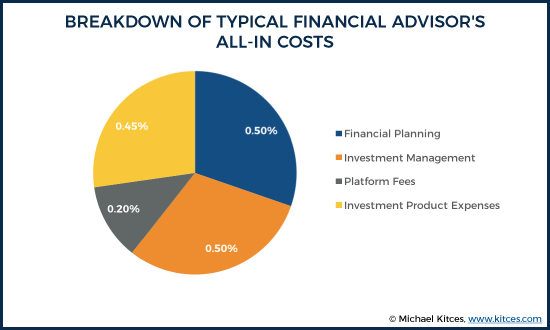

For most advisors who do bundle together financial planning and investment management, though, the Veres study found that most commonly advisors claim their AUM fee is an even split between investment management services, and non-investment services that are simply paid for via an AUM fee. In other words, the typical 1% AUM fee is really more of a 0.50% investment management fee, plus a 0.50% financial planning fee.

Perhaps most striking, though, is that there’s almost no common consensus or industry standard about how much of an advisor’s AUM fee should really be an investment management fee versus not, despite the common use of a wide range of labels like “financial advisor”, “financial planner”, “wealth manager”, etc.

As noted earlier, in part this may be because a subset of those advisors in the Veres study are simply charging separately for financial planning, which increases the percentage-of-AUM-fee-for-just-investment-management allocation (since the planning is covered by the planning fee). Nonetheless, the fact that 90% of advisors still claim their AUM fees are no-more-than-90% allocable to investment management services suggests the majority of advisors package at least some non-investment value-adds into their investment management fee. Yet how much is packaged in and bundled together varies tremendously!

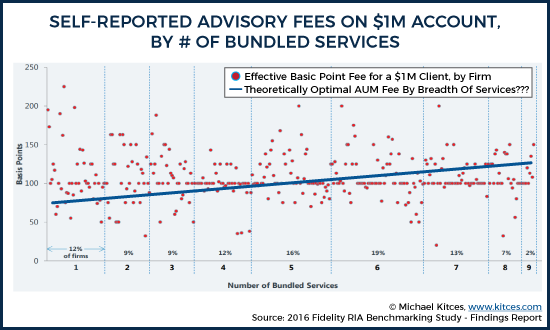

More broadly, though, this ambiguity about whether or how much value financial advisors provide, beyond investment management, for a single AUM fee, is not unique to the Veres study. For instance, last year’s 2016 Fidelity RIA Benchmarking Study found that there is virtually no relationship between an advisor’s fees for a $1M client, and the breadth of services the advisor actually offers to that client! In theory, as the breadth of services to the client rises, the advisory fee should rise as well to support those additional value-adds. Instead, though, the Fidelity study found that the median advisory fee of 1% remains throughout, regardless of whether the advisor just offers wealth management, or bundles together 5 or even 9 other supporting services!

The Future Of Financial Advisor Fee Compression: Investment Management, Financial Planning, Products, And Platforms

Overall, what the Veres study suggests is that the typical all-in AUM fee to work with a financial advisor is actually broken up into several component parts. For a total-cost AUM fee of 1.65% for a portfolio up to $1M, this includes an advisory fee of 1% (which in turn is split between financial planning and investment management), plus another 0.65% of underlying expenses (which is split between the underlying investment products and platform). Which means a financial advisor’s all-in costs really need to be considered across all four domains: investment management, financial planning, products, and platform fees.

Notably, how the underlying costs come together may vary significantly from one advisor to the next. Some may use lower-cost ETFs, but have slightly higher trading fees (given ETF ticket charges) from their platforms. Others may use mutual funds that have no transaction costs, but indirectly pay a 0.25% platform fee (in the form of 12b-1 fees paid to the platform). Some may use more expensive mutual funds, but trim their own advisory fees. Others may manage individual stocks and bonds, but charge more for their investment management services. A TAMP may combine together the platform and product fees.

Overall, though, the Veres data reveals that the breadth of all-in costs is even wider than the breadth of AUM fees, suggesting that financial advisors are finding more consumer sensitivity to their advisory fees, and less sensitivity to the underlying platform and product costs. On the other hand, the rising trend of financial advisors using ETFs to actively manage portfolios suggests that advisors are trying to combat any sensitivity to their advisory fees by squeezing the costs out of their underlying portfolios instead (i.e., by using lower-cost ETFs instead of actively managed mutual funds, and taking over the investment management fee of the mutual fund manager themselves).

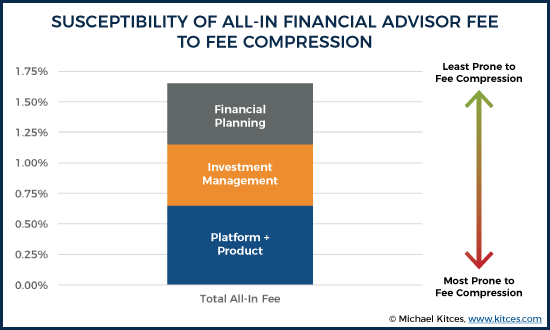

In turn, we can consider the potential implications of fee compression by looking across each of the core domains: investment management, financial planning, and what is typically a combination of products and platform fees.

When it comes to investment management fees, the fact that the typical financial advisor already allocates only half of their advisory fee to investment management (albeit with a wide variance), suggests that there may actually not be much fee compression looming for financial advisors. After all, if the advisor’s typical AUM fee is 1% but only half of that – or 0.50% - is for investment management, then the fee isn’t that far off from many of the recently launched robo-advisors, including TD Ameritrade Essential Portfolios (0.30% AUM fee), Fidelity Go (0.35% AUM fee), and Merrill Lynch Guided Edge (0.45% AUM fee). At worst, the fee compression risk for pure investment management services may “only” be 20 basis points anyway. And for larger clients – where the fee schedule is falling to 0.50% anyway, and the investment management portion would be only 0.25% - financial advisors have already converged on “robo” pricing.

On the other hand, with the financial planning portion of fees, there appears to be little fee compression at all. In fact, as the Fidelity benchmarking study shows, consumers (and advisors) appear to be struggling greatly to assign a clear value to financial planning services at all. Not to say that financial planning services aren’t valuable, but that there’s no clear consensus on how to value them effectively, such that firms provide a wildly different range of supporting financial planning services for substantially similar fees. Until consumers can more clearly identify and understand the differences in financial planning services between advisors, and then “comparison shop” those prices, it’s difficult for financial planning fee compression to take hold.

By contrast, fee compression for the combination of platforms and the underlying product expenses appears to be most ripe for disruption. And arguably, the ongoing shift of financial advisors towards lower cost product solutions suggests that this trend is already well underway, such that even as advisory firms continue to grow, the asset management industry in the aggregate saw a decline in both revenues and profits in 2016. And the trend may only accelerate if increasingly sophisticated rebalancing and model management software begins to create “Indexing 2.0” solutions that make it feasible to eliminate the ETF and mutual fund fee layer altogether. Similarly, the trend of financial advisors from broker-dealers to RIAs suggests that the total cost layer of broker-dealer platforms is also under pressure. And TAMPs that can’t get their all-in pricing below the 0.65% platform-plus-product fee will likely also face growing pressure.

Notably, though, these trends also help to reveal the growing pressure for fiduciary regulation of financial advisors – because as the investment management and product/platform fees continue to shrink, and the relative contribution of financial planning services grow, the core of what a financial advisor “does” to earn their fees is changing. Despite the fact that our financial advisor regulation is based primarily on the underlying investment products and services (and not fee-for-service financial planning advice).

Nonetheless, the point remains that financial advisor fee compression is at best a more nuanced story than is commonly told in the media today. To the extent financial advisors are feeling fee pressure, it appears to be resulting in a shift in the advisor value proposition to earn their 1% fee, and a drive to bring down the underlying costs of products and platforms to defend the advisor’s fee by trimming (other) components of the all-in cost instead. Though at the same time, the data suggests that consumers are less sensitive to all-in costs than “just” the advisor’s fee… raising the question of whether analyzing all-in costs for financial advice may become the next battleground issue for financial advisors that seek to differentiate their costs and value.

In the meantime, for any financial advisors who want to access Veres’ White Paper on Advisory Fees and survey results, you can request a free copy here.

So what do you think? Do you think financial advisors' investment management fees are pretty much in line with robo advisors already? Is fee compression more nuanced than typically believed? Please share your thoughts in the comments below!

Michael,

This is an extremely timely piece and the issue of “value received” for “fees charged” will continue to accelerate in importance. What I did find intriguing is the apparent trend of advisors to provide distinct investment management solutions that are weighted toward expense reduction, which, in turn, might tend to preserve advisor profit margins.

One item that I believe still warrants consideration are those business models which rely upon third-party separate account managers, some of which continue to charge at the 1% fee level before the advisor layers in his or her fees. There are many clients who are still incurring total fees at the 2% and greater level.

Additionally, when distinguishing portfolio management from financial planning fees, I find it difficult to believe that the financial planning side of the ledger warrants an annually re-occurring percentage based fee arrangement. Regardless, I cannot help but imagine that the AUM Fee Model is going to fall under much closer scrutiny in the coming years. — David F. Sterling, Esq., Consultant

Great article. Thank you!

Hi – I’m hoping this is part 1 of the article, as it is thorugh, but only touches on one side of the financial relationship, just as the media choose to pick. The article quotes throughout the ‘costs’, but what it is discussing is the fees. The cost is what provision of the service costs the adviser, and without that information there can be no relevant view of value.

Is a robo charge of 0.3% better value than an adviser fee of 1%? Who knows – if they are both execution only fees then robo is probably best, but a full service client who thinks he will cut costs by moving to robo will squeal to himself loudly when he suddenly realises just what admin work and calculations and research is needed to actually run his account.

When we closed all charging methods down to one flat fee of 1%, for all clients, we switched on a very fierce clock on each client account – at each review meeting we produce both the charges we make, and the costs we have incurred – never had a squeak from any client, and we have some hefty fee payers.

In my experience, adviser costs are ignored throughout the industry, and I for one would gladly support the relevant research.

This is a very important article and i appreciate your reply. Would you kindly expand on how you illustrate your cost you have incurred? Clients never see this part of the cost of business. I have been looking at a flat fee platform that takes away percentage billing to remove higher clients paying more to support lower clients.

Not being facetious here but one solution is to not have “lower” clients. In other words, have a minimum asset value you will accept for a new client. If that minimum value is $500K, then most likely 3/4’s or more of your clients will be in the $500K to $1MM range and no group of clients will be subsidizing another group to any great extent. Most advisors will not take the leap of faith to drop the small clients out of fear that they will not get new clients in the higher asset range.

For the costs, there are two elements. The first is that it costs 0.5% of funds to cover the costs of our office – we can show clients our statutory accounts online. The next cost, the relevant item, is the professional time spent on their account, and that comes off the clock.

I think a key difference we may have is that we point out to those who are more financially fortunate that they will inevitably cross-subsidise those who are less financially fortunate. We happen to think that’s fair, just in the same way the % tax charge works. We don’t like to work with people who are penny pinchers (unless they need to be). If we don’t look after the retired spinster primary school teacher then she’ll be thrown to the lions at a bank, and in her line of work she didn’t get paid much.

Not sure I trust the self-reported expense ratio stats; it’s too easy to “ballpark” the numbers. Though not exactly comparable because it includes all investors in mutual funds, the annual 2016 ICI study shows the “median” expense ratio for equity mutual funds at 1.21% (not asset-weighted); and this does not include sales loads for commissioned planners. As the article indicates, platform fees need to be included. Also, the mutual funds on those platforms tend to have much higher fees in the 1% range, especially since the platforms tend to focus on “active” managers, not “index” funds.

Thanks. one of the most comprehensive treatment of this important topic.

I don’t know the rules here, though I do find the site to be an interesting read.. I am an investor running my own money (7 figures) but I recently helped a nonprofit on a search for an advisor to run about $4M. With 8 competitors I saw a lot of fee discussions.

I think this article and all of the focus on percentages misses an important consideration: How much advisor time does the account take? Granted some expenses to the advisor are a % of AUM, but his/her time spent on the account doesn’t change much as AUM varies. So for example, if I have $2M at 1%, then I am paying the advisor $20,000.to cover his/her time and overhead expenses. Arbitrarily assume that half of that $20K goes out the door as a %. So I am paying $10K essentially for personal services. Now double my portfolio to $4M. His out-the door expenses double, to $20K, still 0.5% of the AUM. Now suppose his time spent on the account rises by 30%. I doubt it is more than that. If so, then his compensation ought to go from $10K to $13K. $13K is .00333% of $4M, so the total fee on the $4M should be, equitably, 83bps.

Now I am totally making up numbers here, but I hope you see my point. Fee reductions for larger accounts are not some kind of volume discounting based on AUM, they are equitable adjustments that reflect that fact that the advisor’s costs do not rise linearly with AUM. The advisor should not get a raise in hourly pay from the client just because the client adds money to the account.

Hello “Old Shooter”. Thanks for your insight. I am an old shooter as well 35+ years in the business, comprehensively trained in value investing in all disciplines including investments outside listed securities. This is my take. The very large majority of advisers are asset gatherers.

90% of their day is based on attracting additional AUM clients invested in listed securities.

The real value comes from older line advisers and professional investors who were trained and are very experienced managing portfolios/investments directly. The best utilize individual securities and alternative investments such as real estate, various art collections, business ownership in many forms, as well as many other alternatives.

Very few wealthy clients have attained their original wealth by investing solely in listed securities. Most owned businesses, inherited wealth, art collectors and many other means.

More than likely they are old line value guys and professional business people who specialize in investments as well as investments in other businesses that are not listed securities. Licensed advisers, for the most part cannot advise nor are they knowledgeable in areas other than regulated products.

With the advent and popularity of ETF’s etc there tends to be a feeling that packaged securities are safer and easier to manage. Maybe so. However, portfolio cost reduction is best achieved when an adviser can manage portfolios with individual securities. Most anyone can buy various services and pick packaged products. It really does not take much talent to diversify a portfolio using those products.

The very best money managers I have met are astute at picking stocks and outside alternative investments. They understand the risks and certainly have the talent. However, in today’s very litigious society we are pressed to follow a format that advocates packaged products. It’s all about delegate the portfolio to “experts”, cover my butt and attain new AUM clients. As a result, their really isn’t much value that the typical AUM adviser brings to the table.

If the overall goal of the financial adviser business is to become of substantive value, then advisers need to step up their game and develop expertise that will effectively serve as a very trusted partner. Very few Mercedes, BMW’s, art collections etc. are purchased at a deep discount. The AUM business is under pressure simply because there is very little value brought to the table in the first place. Regards, Mike Chindamo, Founder Fautores Family Offices.

Depending on the advisor and his/her abilities, you may be paying for above 1) average investment performance, and/or 2) unique service and/or 3) an advisor’s niche that fits you .

1. Some advisors are better investment managers than others of course. An advisor who consistently outperforms majority of other advisors, or invests in a manner that is less expensive for clients, then clients will pay more to have that advisor working for them. Some advisors are better at asset allocation and getting a portfolio reasonably diversified but not going overboard with diversification.

2. Unique service can be a number of things:

–communicating with clients more than once or twice a year;

–a business model that is easily understood;

–limits the number of relationships to 50 or less (90+% of all advisors who have been in the industry long-term have well over 100 relationships of all asset sizes on their books);

–limits the relationship based on assets ex: does not take any relationship under $500,000

3. “Niche” can mean some of what is listed in 2. above and include things such as an advisor who:

–invests client accounts primarily in individual equities rather than more expensive mutual funds and separately managed accounts, which substantially reduces client investment costs (obviously, the advisor has to have this expertise and research ability);

–is not all things to all clients: specializes in one area whether it is planning or investment management: planning does not help much if you do not realize the returns to fulfill the plan.

–has a specialized background or education or work experience: former lawyer, or banker, or has post-graduate degree;

–fiduciary (as all fee-only advisors are) who is legally obligated to put clients’ best interests first at all times.

Just items to consider when thinking about what you may pay for in a financial advisor. Not all the same by a long shot.

In very broad terms I agree with most of this. My point was about the nonlinear economics of AUM fees. I frequently buy wine that is not the cheapest, which is essentially your argument. Especially your #2 and #3.

But your #1 is ludicrous IMO. As an investor I am not looking for the tallest midget: the advisor who outperforms other advisors. I want at least the market-beating equity performance I can get easily from passive investments. Statistically speaking, essentially zero advisors will consistently deliver something better. (ref S&P SPIVA and Manager Persistence report cards, WSJ last week on Morning-stars, and William Sharpe’s 1991 paper.) The ones who claim anything else are frauds or delusional, pure and simple.

Same comment applies to #3/investing in individual equities. Saving costs with a statistically doomed strategy is small compensation.

The problem with advisors is that it is hard to justify a fee for selecting the simple investments necessary to succeed with a passive strategy. So they have to make things look complicated and blather about individual stocks, diversification, etc.. Actually the investment guys at pension funds have the same problem. If they do the statistically correct thing, their bosses will realize that a passive strategy does not require expensive investment guys..

Re fiduciary, any advisor who is NOT a fiduciary has not met the minimum bar for using the word. A non-fiduciary is a salesperson, not an advisor. End of story.

Sounds like you are set and managing your own investments. Most are not capable of doing that. Behavioral problems usually get the individual investor who attempts to go it alone. I would like some of the “market beating equity performance” you say you can get from passive investments. The passive investments may do fine (not sure about market beating though) but the holder of them does not necessarily follow along for the entire ride.

And who wants or needs “market beating” investments? Give me inflation + 7% on average per year and I’ll be as happy as can be.

Sorry if I was not clear. If I am going to pay an advisor I want market-beating performance. I can get market performance on my own, less maybe 30bps. I was kind of making a joke because the advisor who can beat the market is not stuffing himself into a suit and hustling business every day. He is on a private tropical island somewhere drinking from a glass garnished with an orchid.

Behavioral, yes. Keeping people from panicking and selling may well be worth every dime they’ve ever paid the advisor, even net of his/her underperforming investment choices. In my case, I learned after October 19, 1987 that just ignoring these things is a winning strategy and it has worked just fine several times since.

Just for reference, inflation + 7% IS outperformance.over most periods.

Shooter, perhaps I’m coming into this discussion a bit late, but take my two cents for what it’s worth. You seem to be someone who does fine managing their own investments and controlling their emotions. In my experience, most people do not possess one of these traits, much less both. In addition, many clients of ours are “smart” enough to pick a diversified portfolio but frankly they don’t care to manage it and are happy to employ our firm to do the heavy lifting so they can spend time on other things in life. Frankly, if we met and based on what you’ve shared here, I’d likely recommend that we don’t work together. And that’s fine, please don’t take this as a personal insult, it’s just that we don’t attempt to compete or win business based on performance relative to some benchmark that honestly has no bearing on your life, whether it’s the S&P, Barclays Agg, etc. When we meet with prospective clients who expect us to beat the S&P, it’s usually not a good fit. Simply put, not many if any investors should be 100% allocated to stocks, so we set expectations right from the start – your goal is to get from Point A to Point B in your life. We help you get there with the least amount of risk. Is our advisory fee worth it – we think so. Not to mention, it includes comprehensive planning work at no additional cost. Our entire firm is comprised of CFP professionals. Also, you mentioned Vanguard and DFA. We use both and you can’t access DFA as a do-it-yourself investor. You can buy Vanguard funds, but strangely enough, even Vanguard has produced a report related to the “Advisors’ Alpha,” which centers on the premium provided to clients primarily around the behavioral side of this equation. Again, you seem to have a good grasp of keeping your wits when the markets go south. In our experience, MOST people do not and our 1% (or whatever) fee more than makes up for the “cost” of making a poor decision even once in your lifetime.

I’m 4 years late, but I’ll say this: If an investor’s main concern is whether or not an advisor can beat the market, then they’re a danger to their own portfolio and their own retirement. They can’t see the forest for the trees. A great advisor is valuable because he will ask the right questions.

One more thing, OS. Regarding “passive investments”, aka, ETFs that track an index, be aware of what can happen and has happened in the recent past with index funds and ETFs…2000 and 2008-09.

ETFs buy stocks with no thought whatsoever given to valuation. If you give an index fund $1 million, it buys the stocks it has to, whether they are trading at 3,000 times earnings or at 6 times earnings. Whatever the index holds that the ETF is tracking. This is mindless investing any way you slice it, but folks like to rationalize.

I’ll give you a personal example. I was managing my small business’ Profit Sharing Plan in late ’90’s. It was in individual equities for most past. I did not own any of the high flying tech stocks. Not even the more established companies like Intel and Microsoft. My year was a fiscal one, from 8/1 to 7/31. From 8/00 thru 7/01, the PSP was up 24.88% and S&P 500 was down 14.3%. The next year, the PSP was down 3.65% and the S&P was down 23.6%. The small cap indices were even worse. Point is, for those 2 years and even a few after those 2, thank God I was not in index funds. The S&P 500 never caught me over the next 8 years (we shut the PSP down in 2011 when we sold the business) thanks to those 2 years. Just one personal experience/example. You can probably shoot holes in it.

Well, life is too short to re-hash the debate. I’ll just point out a few things. First, buying an S&P index fund is NOT passive investing. It’s just making a sector bet. Dumb. As Gene Fama says, “We have to hold the market portfolio.” IOW, everything. VTWSX or similar. DFA has some attractive ideas on this, too.

Second, I’ll bet that you can look at your watch and tell me what time it is. I’ll also bet that you can’t explain to me how the watch works. In a decade or more of reports, S&P has been telling us what time it is. All the blather about “mindless investing” or even the EMH is just discussion of how the watch might work, completely irrelevant to investing based on what time it is.

Yes, when the market goes down the passive investor’s portfolio goes down too. Duh. Very few people believe that the market can be timed and most of those guys are selling investment letters because they are not good at investing. So the advisors’ portfolios will go down too. On average, just as much as the passive investors’ portfolios did. Ho hum. Move along folks, nothing to see here.

Wow! Best article I’ve read in a long time. The data was organized very well and was easy to follow but most importantly it got down to the heart of the matter. I can see where some of my fellow advisors could read this article and become a bit defensive but I believe that it points to one simple truth which is that we can and should improve this industry. In this context, I’m defining industry as “the industry of providing investment management and financial planning advice to human beings that benefit from the advice”. I imagine a future that allows client’s to walk into a local financial advisors office and be face to face with the advisor/company that manages his or her portfolio from top to bottom at roughly I/2 the current cost. I not only believe this to be true but have implemented this at my firm. It simply requires an insatiable appetite for learning/improving and a mild paradigm shift. The shift is from a growth-only focus to growth and cost reduction/efficiency focus (without firing employees). Mr. Kitces please call me if you are able and willing. 440-622-8041.

Sincerely,

Landon Jones

Michael – We are very grateful that you have taken the time to break this down. It has been extremely helpful as we review our own pricing and provides excellent clarity into industry pricing trends. Is there any chance you have updated data on the Median All-In AUM Fees of Financial Advisors (By Portfolio Size) or if not, is this something you anticipate updating in the future? Thanks again!

I moved a large amount to an advisor, kept about 1/4 to self-manage to see how they do. Right now we are about dead-even after almost a year, but I'm earning a higher income in my self-directed portfolio (I assume I'm probably being a bit riskier.) I'd say that if it's only investment management, go with a Robo-Advisor unless the human advisor wants to match that price. I am getting some good tax advice on the side, so I do appreciate the value of the 1% that I am paying.