Executive Summary

Wealth management – a combination of investment management and holistic financial planning advice, typically for affluent clientele – has become an increasingly dominant model in recent years. The transition to wealth management has spurred a massive shift to fee-based accounts, the explosion of independent and hybrid RIAs, and the success of a growing number of providers to independent advisors, from custodial platforms like Schwab and Fidelity to asset managers like Vanguard and DFA.

Yet an emerging transition appears to be underway, as a growing number of asset management platforms are no longer just providing support services to financial planners, but are entering the business themselves. From Schwab’s growing number of managed-account solutions (including its new Schwab Intelligent Portfolios) paired with increasingly-CFP-based branch consultants, to Fidelity’s acquisition of financial planning software and push for hiring CFP professionals as well, to Vanguard’s massive launch of its Personal Advisor Services platform - and TD Ameritrade announcing they plan to expand both their Amerivest and "Private Client Services" programs that blend technology with humans providing financial advice - the trend of “insourcing” financial planning has begun.

And what’s notable about this trend is that, given the existing size of these asset managers, their transition to offering financial advice allows them to immediately offer services at a size and scale beyond even the largest independent advisory firms. This gives the companies not only the potential to compete aggressively on price, but to utilize their massive marketing budgets and already-nationally-recognized brands to rapidly scale their marketing and drive growth even faster.

The end result is that independent advisors may increasingly find themselves in competition in the future with a number of large companies who also serve them as asset managers and RIA custodians. This will not necessarily undermine the existing clients of advisory firms – there are lower-hanging fruit for the new players to pursue, including converting retail clients already on their platforms – but presents a significant new headwind and challenge for future clients and growth, unlike anything independent advisors have ever seen before.

And perhaps most notable of all will be the rise of Vanguard’s personal financial advice solution. Not only because Vanguard is already the largest asset manager with the largest existing client base to solicit for planning services, but because its unique “mutual” company structure means it may simultaneously become the largest financial planning firm, and the first to operate solely in the interests of the clients who implicitly own it, without having a separate corporate profit motive. Welcome to the new disruption – the first “mutual financial planning” company has arrived.

The Growth Of Financial Planning And Business Models For Holistic Financial Advice

The growth of the financial planning movement over the past several decades has been phenomenal. From a first class of 35 CFP certificants in 1973, to a total of over 72,000 CFP professionals today (plus another 85,000 outside the US!), plus thousands more in other ‘related’ designations like the ChFC and the PFS, financial planning has been the epicenter of the transition of the financial services industry from using “advisors” for the mere distribution of products, to having advisors who are primarily in the business of actually delivering valuable advice.

And as the movement towards financial advice has grown, so too have advisor business models morphed. From their roots as stockbrokers and insurance agents, the first wave of financial planners sought a different way to distribute and deliver financial products, not by selling whatever the stock or insurance product of the day happened to be, but by understanding a client’s goals, and delivering them whatever product best matched their needs. Not surprisingly, when the recommendation was more consistent with what the client actually needed anyway, more clients implemented the solutions, and planning-centric advisors were more successful than pure product-pushers.

Nevertheless, the fundamental challenge of personal financial advice is that given how client needs change over time, the need for advice itself is ongoing, yet the industry’s roots as a product distribution system were not conducive to the delivery of ongoing advice. The search for alternative business models to support ongoing relationships ultimately drove the rise of the assets-under-management model, where financial planning became the value-add and the differentiator that allowed “wealth management” firms to attract clients by offering more than just investment management alone, while enjoying the sustainable recurring revenue that ongoing management provides.

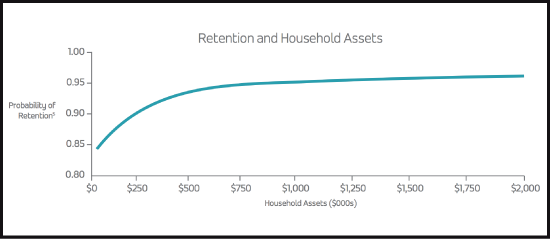

An ancillary benefit of financial planning that emerged in the rise of the AUM model is that delivering quality advice not only helps attract clients and gather assets, but the deep advisor-client relationship that is formed helps to support the retention of those clients and assets as well. With retention rates of 85%, 95%, or even higher for ‘top’ firms, clients who came on board initially became clients who stayed ‘forever’, and the higher the net worth (and the greater the capacity to deliver value-add advice), the higher the retention has become.

Source: "Stay Or Stray" by PriceMetrix

And as advisory firms grew increasingly focusing on delivering advice for advice’s sake, and not functioning as a product distribution model, advisors themselves shifted increasingly independent – after all, there’s limited value to being associated with an insurance company, wirehouse, or broker-dealer, when the advisor is not in the business of distributing their proprietary products and solutions anyway. And as the independent advisor movement grew, so too did the amount of technology tools and platforms to support them, further reducing the need to rely on the resources of a large traditional firm.

The end result has led to the development of an incredibly large and remarkably robust landscape of technology, platforms, and solutions to support independent advisors as well. Technology solutions for portfolio accounting, like Orion Advisor Services, Tamarac, Black Diamond, and Advent have been on the rise (so much that they’ve all been the subject of numerous M&A transactions in recent years!). And increasingly relationship-centric CRM systems from Junxure to Salesforce have triumphed amongst advisors over older sales-centric software like Act and Goldmine.

Though nowhere has the growth supporting independent AUM-based financial-planning-centric advisors been more significant than the custodial platforms and asset management firms serving them, from Schwab Advisor Services now supporting over $1.1 trillion in assets, to Vanguard also estimating having about $1.1 trillion of its AUM that are ‘advisor sold’, not to mention almost $400B of AUM of advisor-centric asset manager DFA funds, and a growing number of independent-advisor-centric solutions that have followed.

The Insourcing Of Financial Planning

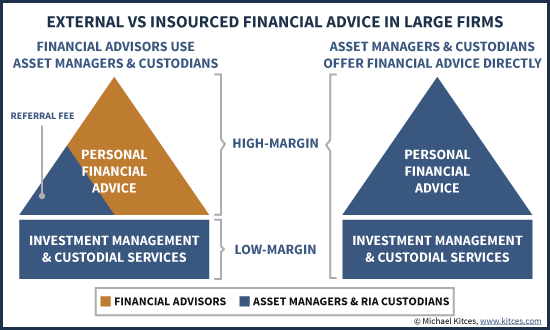

While the growth of financial planning and the AUM model has helped to create some incredibly large businesses that serve advisors, the evolution has also relegated those custodians and asset managers to the increasingly commoditized position in the value-chain of financial services. Notwithstanding their size and scale – or perhaps, because of it – transaction costs and investment expense ratios just continue to grind lower and lower, compressing margins further and further.

In essence, this means asset managers and custodians are now stuck in a cutthroat low-margin business, trying to support higher-margin financial planners who build businesses on top of their platforms. For a time, custodians have tried to get a “piece of the advisor action” by developing advisor network programs that refer retail consumers on their (commoditized transactional) platform to work with advisors, who in turn must share a portion of their (recurring) revenue back to the custodial platform as a referral fee.

Yet the transition that is now emerging is that custodians and asset managers no longer want to solely function as the low-margin base underlying the higher-margin advice business. In other words, why ‘just’ take a slice on a referral, when you can control the whole relationship, and enjoy the profitability of delivering the entire advice solution (with even better margins at better scale) and move up the value chain?

Accordingly, some mega-custodian and asset management firms are beginning to “insource” their financial planning solutions, hiring their own CFP certificants to deliver their own advice solutions. For instance, Schwab’s “Private Client” group has become an increasingly sophisticated, RIA-like solution, now charging similar-to-independent-RIA fees on a whopping $64B of AUM (as of their latest Form ADV). And Schwab also recently launched their “Schwab Intelligent Portfolios” solution, which has been billed as a “robo-advisor” but in reality gives consumers access to any of the (rumored to be increasingly-CFP-qualified) financial consultants at their branch offices. In other words, from the holistic perspective, Schwab’s “robo-advisor” is really just another managed account available to be paired with their retail personal financial consultants, along with the existing Windhaven and ThomasPartners managed account solutions.

Notably, though, the focus is not just at Schwab. Fidelity has also been actively hiring CFP certificants to support its own branches – and appears so eager for talent, it became the launch partner for the CFP Board’s new Career Center last year, and is currently one of the two firms with the largest number of job postings for CFP professionals on that site. Fidelity also recently acquired financial planning software provider eMoney Advisor for more than $250M, signaling the depth of its serious commitment to steering the entire company more deeply into financial planning services directly to consumers. And TD Ameritrade just announced its own solution, a digital expansion of its Amerivest offering that will include technology upgrades while still pairing investors together with human [advisor] specialists (which means, similar to Schwab, the new offering has been covered in the media as a "robo" launch, but it's really another technology-human-advisor hybrid solution). Notably, TD Ameritrade also announced an expansion of its premium "Private Client Services" (PCS) for millionaire clients that will deepen its financial advice offering with affluent clients and again risks increasingly competing with RIAs on the TD Ameritrade custodial platform and in their advisor network if/when/as the PCS offering continues to deepen further over time.

Asset managers have also gotten involved. Beyond Fidelity, the other firm rapidly hiring CFP certificants on the CFP Board’s Career Center is asset manager TIAA-CREF, though perhaps the most visible asset manager to recently enter the world of financial planning is the indexing behemoth Vanguard, and its launch of Vanguard Personal Advisor Services (VPAS) last year. Like Schwab Intelligent Portfolios, Vanguard’s solution has also been characterized as a “robo-advisor”, but in fact it is not either – instead, Vanguard has been heavily staffing dozens (now rumored to be over 100) CFP professionals in Pennsylvania to deliver personal financial advice directly to Vanguard customers... for a 0.30% annual fee and an asset minimum now as low as $50,000! And last week, Capital One announced that it would merge its online Sharebuilder trading platform into a new "Capital One Investing" solution... that will offer clients with at least $25,000 in their portfolio the opportunity to meet face-to-face with a Capital One financial advisor.

In fact, the most notable theme of the progression of major custodians and asset management firms towards financial planning is that they are not opting for purely automated “robo-advisor” solutions. Instead, they are all pursuing “hybrid” strategies that blend together human advisors and technology, a major bet that the real opportunity is not in robo-advisors, and that financial planning delivered by technology-augmented humans – the “cyborg” or “bionic” advisors – will be the winner in the long run. Which – perhaps frighteningly? – is actually even more of a head-to-head threat with today’s independent advisors than a solely-robo offering would be!

Growing Revenue For Scaled Financial Advice With Big Brand And Scaled Marketing

While advisory firms often think of adding deeper financial planning services as a ‘margin squeeze’ – hiring expensive staff to deliver sophisticated advice with the hopes that it will pay off in the long run with improved retention and greater referrals – the context is notably different for large custodians and asset management firms.

The reason is that for many large firms, there are already an astounding number of clients who may be engaged with some of the company’s products or services, but in the most-commoditized lowest-margin solutions. This might be Schwab or Fidelity retail clients who just occasionally trade stocks for $9.95 or less, or Vanguard investors who own Vanguard Total Stock Market Index in the Admiral class at a 0.05% expense ratio. For these companies, moving a client from $9.95/trade into Schwab Private Client at 0.90%, or from Vanguard Total Market at 0.05% into Vanguard Personal Advisor Services for 0.30%, represents a dramatic uptick in revenue (and ultimately profit potential) for the firm. In other words, while for traditional advisory firms adding financial planning is a profit margin squeeze, for asset managers and custodians it’s an opportunity for profit growth.

And the opportunity is significant, given the sheer size of the platforms. Schwab has over $1 trillion in its retail investment business, and Vanguard’s retail business (excluding advisor-sold) is about twice as large. This gives the companies the potential to immediately roll out a standardized and structured financial advice offering at a scale that instantly dwarfs almost every independent advisory firm. More important, though, it means not only is there an incredibly large potential asset base to which advice can be delivered at scale, but converting even just a small percentage of their retail clients would instantly result in an enormous advice platform.

And in point of fact, that appears to be exactly what is happening, as Vanguard Personal Advisor Services has quickly vaulted to adding $7B of AUM to its new service in the past year (with assets totaling $17B including existing funds already in its predecessor Vanguard Asset Management Services platform), and Schwab Private Client is up to $64B (while its Intelligent Portfolios solution has added $2.3B in just the first few months). Rumors are that a significant amount of assets in both cases are new to those particular advisor-based solutions, but not necessarily new assets to the companies – instead, they’re transitions of existing assets into a ‘more profitable’ line of business. No doubt, TD Ameritrade as well is hoping to better monetize its more affluent clientele - particularly the ones not already working with RIAs - with the expanded Amerivest and PCS offerings.

Nonetheless, the disruptive potential of the platforms to expand beyond the existing asset base and into truly “new” clients at companies like Vanguard and Schwab are significant. The key distinction is that for most advisory firms, the great challenge ultimately boils down to the high cost of client acquisition for financial advisors – it’s really hard to get new clients, especially in volume. However, scaling the marketing of an advisory firm allows it to drive down its client acquisition costs, which has already led to the recent trend that the largest independent advisory firms are growing more rapidly, while the small-firm majority is “stuck” small.

In this context, the threat of companies like Vanguard and Schwab going into direct competition with independent advisors is significant. These companies market at a scale that utterly dwarfs even the largest RIAs – which at $10B+ of AUM are still less than 1/100th the size of just Schwab’s retail direct-to-consumer division – and have truly national recognized brands. This will create the potential for them to grow at a far more rapid pace than large RIAs, even more rapidly than small RIAs, and potentially leave the “robo-advisors” in the dust as well. In a low-trust industry like financial services, where it’s hard to evaluate the benefits of an intangible service like financial planning, don’t underestimate the incredible selling power of having a massive marketing budget and a high-trust brand!

Industry Implications Of The New Disruptive Threat To Independent Advisors

Ironically, while the entrance of major asset management firms and custodians into the business of financial planning may create disruptive pressures on existing RIAs, there are actually some major plusses to the financial planning profession of these emerging mega-behemoth financial advice brands.

The Financial Planning Career Track Of The Future?

The first is that the growth of standardized financial advice at scale comes the basis of the “financial planning career track” that has been sorely missing for the profession.

Right now, college students who study financial planning graduate into a wide array of financial services jobs, from true financial planning support positions in some advisory firms, to what are really just product sales jobs at other firms, and they often have little ability to tell the difference. And even in the “good” planning firms, the career track for new advisors is often tenuous at best, as the advisory firm is so small and still growing, it doesn’t even know what the career track might be because the firm doesn’t know what it will look like in 5-10 years!

By contrast, just as most accountants start out after graduate school in a “Big 4” accounting firm for a few years, learn their trade, and then decide what they will do next for the rest of their careers, so too will many future financial planning graduates follow the same path through a small subset of big national asset-managers-turned-financial-advice firms. As these large firms – that today hire hundreds of CFP professionals may in a few years hire thousands – continue to grow, they will be able to form that core career track to bring new people to the profession. And ultimately, just as in the accounting context, some of the advisors who go into those professional career tracks will stay at those firms, and others will leave to join a ‘boutique’ firm, or perhaps even go entirely independent and launch their own RIA instead. But regardless, national firms will likely be where truly standardized career tracks emerge.

On the other hand, as career tracks emerge at large national firms where young planners learn their profession before going out on their own, the future of building an independent firm after working at one of those firms may not look so bright. Competing head-to-head with massive marketing campaigns and national brands is beyond the capabilities of all but a few of the largest RIAs fighting to create their own national brands, like Edelman Financial Services and United Capital.

Growing Competitive Pressures For Existing And Especially New Clients

For almost all other advisors, the pressure will be on to prove their worth and value by going above-and-beyond in terms of expertise or other value-add services. This will force many (or even most?) advisory firms to either go deeper into finding a niche where they can be more clearly differentiated, create more unique “boutique” style experiences that can still attract the most affluent high-end clientele, or try to get large enough to compete nationally or at least as an established regional player (similar to the regional law or accounting firms that establish a presence as the “go-to” firm in their geographic region).

Notably, the primary point of competition going forward will probably not be firms like Vanguard, Schwab, Fidelity, or TD Ameritrade going after the existing clients of RIAs. First and foremost, serving advisors is still profitable for these companies, and realistically they will want to minimize the channel conflicts to the extent possible (though growing tension seems inevitable?). And from a practical perspective, it’s difficult to convince established RIA clients to make a change.

Instead, the real competition will for be future clients and growth. The asset management firms will likely pursue the “lowest hanging fruit” first – consumers who still don’t have an advisor and are currently do-it-yourselfers (which includes clients already on their own do-it-yourself platforms), those consumers who have a poor-quality “advisor” who is selling products and not even really delivering advice, and those who simply aren’t served well by advisors in the first place (e.g., much of the mass affluent). This includes populations that are currently underserved; a second major benefit of the transition of scaled financial advice from asset management firms is that when brokerage firms raise the question of who will deliver personal financial advice to the mass affluent in a fiduciary world, the answer may be companies like Vanguard and Schwab!

Nonetheless, asset management firms delivering personal financial advice are likely to become increasing competition for the more affluent clientele of many RIAs today. When Vanguard markets its advisor services for 0.30%, and Schwab offers their Intelligent Portfolios solution “for free” (because it’s a distribution channel for their proprietary ETFs and Schwab Bank where they earn a profit instead), inevitably there may be a few existing cost-sensitive RIA clients who decide to make a switch. And going forward, even “high end” advisory firms that still charge their full 1% AUM fee to deliver “high end” advice will still have to justify, over and over again, why their added depth and expertise is worth that extra cost. In other words, just as active investment managers must justify their added expense ratios in portfolio value-add over the cost of a pure index fund, so too will financial planners be increasingly compelled to justify their added cost in financial planning value-adds over the “financial planning indexing” cost of 0.30% from Vanguard Personal Advisor Services.

Will Vanguard's Personal Advisor Services Become A Financial Planning Juggernaut?

In fact, ultimately I believe that the transition of Vanguard into the delivery of personal financial advice at scale may be a watershed moment for the industry, and the greatest personal financial advice disruption of all. Not merely because Vanguard is already the largest asset management firm, with the largest base of clients to market and grow their business, and one of the biggest and most trusted brands in the industry – all of which will allow them to quickly become a dominant player.

In the end, the unique disruptive potential of Vanguard against independent financial advisors may be the same reason it continues to be so disruptive to the asset management industry, and even other index fund providers: Vanguard’s unique corporate ownership structure where it operates as a “mutual” mutual fund company, effectively owned by its retail investors, such that the company does not have to pursue a corporate profit margin. That structure has allowed Vanguard to continue to offer services at a lower cost than any of its competitors – and even attract a recent lawsuit about whether its approach amounts to tax evasion – a differentiator that up until now has made it an advisor favorite due to its low costs.

In other words, we may be witnessing the first ever creation of the “mutual” company model being brought to personal financial advice. And when advisors now have to compete head-to-head against that cost structure, which operates to bring the cost of personal financial advice to new lows… well, beware being a for-profit independent advisor in competition with a “non-profit” adversary that has a $3 trillion head start!?

You wrote in April last year: “Notably, the Vanguard financial plan does not appear to go in depth into income tax strategies, estate planning issues, or an insurance analysis, nor into cash flow and budgeting issues.”

https://www.kitces.com/blog/vanguard-personal-advisor-services-vpas-the-first-low-cost-indexing-solution-for-financial-planning-services/

So what is the true potential for a service that is intentionally limited mainly to portfolio and investment-related goals?

Bill, Michael,

This is exactly how I feel my service differentiates from Vanguard and is superior. Will Vanguard be using financial planning software to analyze a client’s prospects for retirement or to help craft an income plan for the retiree. What about tax planning for employer stock options, RSU’s and ESPP’s, unkonwn cost basis, roth conversions, insurance policy surrender? Will they help the client understand their need (or lack of need) for long term care, life, disability, liability insurance? How to get kids through college? Budget, manage debt, live within ones means? What I’m worried about is that people will get the impression that the things Vanguard *will* help with (investing) are the only things that matter when they are not.

The other thing I’m not yet sorting out here is, if they are charging an AUM fee, how does this work in a “mutual” mutual fund company. AUM isn’t “mutual” is it? How do the AUM fees paid make the payer an owner of the company in the same way as owning shares of a Vgd mutual fund makes you an (indirect) owner of the company (because the funds own the company)?? Who gets the profits from the AUM? Will these profits drive down even further the costs of the funds?? How does AUM fit into the “mutual” part of the Vanguard value proposition?? Has VAnguard addressed this question?

I suspect Bogle is fit to be tied.

Michael, thanks for this helpful “big picture in perspective” article!.

Kay

Mutual fund companies have several challenges that preclude their use in advisory services application to include (1) real time holdings data essential for continuous, comprehensive counsel required for professional standing in advisory services and (2) redundancy in account administration cost at the fund level and client level that add no additional value. These two particular innovations pertaining to transparency and cost structure are essential to fiduciary standing and are best managed by a more modern approach to portfolio construction which will drive the industry forward.

SCW

Stephen Winks

.

USAA was one of the first large firms to discover the power of providing advice through financial planning to meet their members needs in the late 1990s, and its deployment became the keystone to the integration of its investment, banking and insurance services. They remain committed to the approach and today have one of the largest corporate populations of CFPs.

Their new CEO, Stuart Parker, is a CFP® who came from their financial planning division.

Yes, USAA was 1st. I was just thinking that when I scrolled down to your comment…

They don’t scare me. Most are nothing more than a glorified allocation fund that will subsist on young/inexperienced labor to “trick” people into thinking they are getting a true financial planner. This advice will never be of the same caliper of our small “boutique” firms, which many of us started because we were fed up with the large financial companies’ insatiable, profit motives and to get outside of the infuriating bureaucracies of the large B/Ds, wirehouses, and insurance B/Ds.

Also, I believe the largest intangible in our profession is the strong interpersonal relationship that we build with our clients that enable us to actually successfully implement our planning and advice. That was my biggest problem when I was a younger advisor, trying to get people to implement was super hard and most times unsuccessful; they will have this problem regardless of how good the tech is that they purchase. My firm is specifically built to optimize the probability that I can actually implement my advice to clients (as I’m sure many other RIA’s are as well), it is am super nimble and able to adapt to change/progress, but unfortunately, it does not scale well because of liability and costs when you start to layer on the necessary bureaucracy to scale it up past a few advisors…

This is just another iteration of the same game: they want our profit margins and they think they can duplicate what we do at scale, but there will be no escaping the inefficiency of their bureaucracies, regardless of their supposed “pure” intentions and/or economy of scale. Plus, if they’re truly a fiduciary at this scale then I think their liability could be much more than they’re counting on (if the SEC and the courts would ever actually hold their feet to the fire for the eventual bad client outcomes in the future).

I’m commenting as (it would appear) the first consumer (vs. professional financial planner) on the off chance my perspective is of interest.

I started out as a thoroughly uneducated investor in my 30’s who was lucky to have a fairly high-powered job for awhile and to receive stock options. I started off with Schwab and Vanguard and got decent albeit generic allocation advice and began reading books on investing. ~75 books and countless research hours later I consider myself reasonably knowledgeable.

I’ve followed the Roboadvisor disruption since the beginning and think it’s very positive for young, tech-savvy millenials. I also had an account with a very sophisticated advisor in California who uses primarily DFA funds for a 7 year period that included the 2008 market implosion.

I think you’re absolutely correct Mr. Kitces that Vanguard’s entry into this arena is a potentially highly disruptive. They are indeed the only “mutual mutual fund” company and as an investor and long time Boglehead I’m well aware that the main reason there are low cost funds and ETFs available in the marketplace is that other discount firms have had no choice but to respond to Vanguard’s low costs – while they cannot, structurally, equal its alighnment of customer with firm interests (as evidenced by Schab’s thoroughly bungled roll-out of its cash-laden Robo service – and I say that as a generally very happy Schwab client!).

The only way an FA could effectively get my business at this point would be to be extremely knowledgeable and experienced, be thoroughly committed to passive index fund investing (and know that “smart alpha” is B.S.) AND be a fixed fee, not a percentage of assets, provider of services as my former DFA access firm was (and still is – and they’re booming). I think the hand-holding during times of market crisis and the insightful macroeconomic and financial market perspective that a great advisor provides is worth it for most investors, but it seems to me that Vanguard’s .30 fee is now the outer limits of what’s viable as a baseline cost – and it is likely to come down as their AUM increases.

Just one consumer’s two cents. Thanks for the fantastic resource of this blog.

Thanks for the comment Kevin!

Indeed, ultimately I see the whole robo-advisor movement as putting ongoing pressure on advisors to demonstrate their value-add beyond the portfolio (or for the small subset who can REALLY figure out how to add alpha in the portfolio?).

That won’t “kill” advisors, but it will continue to force us up the value chain. Which means those at the front of the transition will prosper as the market shifts, and those who lag behind… well, at least they’ll hold on to most of their current clients due to existing relationships…

– Michael

Kevin,

I like your vantage point as a consumer, a wise one at that. We tell our clients that the Investment piece is the easiest part of our planning work if they embrace a passive approach to Investing. As a matter of fact, it’s damn near automatic. It’s not too hard to put together model portfolios using DFA, Vanguard. The hard part is getting to know the clients, their values and goals and how to align that to their Investments.

The real value comprehensive advisors offer their clients is to tie in all of ther financial concerns–tax planning, retirement planning, estate planning, and cash flow. This is the approach ACP members utilize (acplanners.org) and find we have very little attitrtion of clients.

Of course, they are really not offering fiduciary advice. They’re pitching Vanguard funds and they don’t really know how to do planning. So, it’s easy to sell against them but, like the wirehouses, they have a lot of marketing power.

I am now a financial planner, but for a good part of my previous life, I was a consumer desperate for good financial planning advice. I started out just like Kevin did: thoroughly uneducated investor in the beginning, lucky to save few $$ in my first career, followed the robo movement closely (Michael, I would say your thoughts on the movement are quite ‘disruptive’ as well). I do actually believe the robo advisor platforms could be very useful for new planners, and planners who want to minimize their time on the Investment management.

Coming to Custodians providing financial advice and reaping the higher margins, I have an interesting story that I like to share: I have some good sums of personal savings @ fidelity. Few

Years ago, I met a young relationship manager @ fidelity and asked him naively if fidelity offers financial planning services and he referred me to their “advisor network program” where I can use the services of a CFP. My next question was “Are these CFPs Fidelity Employees?” and the answer was “No, we have a professional relationship with the planners.” And then we talk about the fees and how much I pay who etc., and finally I ask a Q “I am curious. Why doesn’t fidelity bundle up the fees and provide these services itself instead of referring us to a third party?” I don’t remember getting a straight answer, but Michael, your blog post explains it all. Thank you!

First of all, I just want to say thanks Michael for creating such a valuable blog – as I contemplate a potential career change from law back to financial services, your posts have been my primary way of understanding the changing landscape that I would be encountering. (From my research, your posts offer depth and breadth that appear to be unmatched.)

This move by Vanguard seems highly disruptive. Sure, advisors can compete by offering planning that Vanguard currently doesn’t offer (income tax, insurance needs analysis, etc.), but it would seem only a matter of time before Vanguard PAS incorporate those services as well.

Advisors can cater to niche clientele (Doctors, Entrepreneurs, etc.) and add certifications for further differentiation, but I believe I read in the recent McKinsey report that the big “Insourcing” firms like Vanguard are also moving to organize groups that also cater to these niche clientele. I would imagine that these firms also would encourage their CFP’s to gain other certifications as well.

My thoughts have been maybe to join a Vanguard, or similar firm to sort of have that standardized career track like accountants have, as you’ve mentioned. However, even then, assuming I wanted to stick with them long-term, their non-profit status would seem to make it likely that they will continue passing on as much savings to the clients at the expense of the tenured CFP’s salary.

On the other hand, if I wanted to go independent – which would likely be the case – with clients working within a team of advisors, it seems it would be relatively more difficult to pry away clients to take with me as they would be more “entrenched.” In addition, the “mutual mutual fund” ownership structure seems to give them a huge advantage: it seems it would be very difficult for a for-profit, RIA upstart with limited resources to compete with such a huge non-profit with a brand name.

What is your opinion on the effect of the increased efficiency of these “Insourcing centers?” I think it was the McKinsey report that talked about how many more clients they can service per day – that would seem to put even more of a squeeze on the CFP per mass affluent supply-and-demand relationship, that one of your posts mentions (revealing how the growth of the number of CFP’s per mass affluent makes the demand for advising not as favorable as many suggest).

Also,do you foresee an even further reduction of the .3% fee as their AUM increases

and/or added efficiencies? Reading stories like James Osborne at Bason Asset Management in Colorado is encouraging to me, because of his ability to attract such a significant amount of capital in such a short period (all while providing what I believe to be a more fair compensation model), but the threat of a further reduction is mildly concerning.

Having completed my first year of law school – and seeing way too many of my (very

intelligent) classmates stuck with $15-$25 per hour contract work (or University-funded “positions,”) I thought utilizing my CFA background (I’ve passed all three examinations) coupled with working towards a CFP would offer relatively better prospects than law.

However, after reading many of your posts, I’ve quickly gathered we’ve come a long way

from the product-oriented planning model of the past (I used to work for one of the big insurance mutual companies). This move by Vanguard seems very disruptive for advisors (though an excellent product for consumers), and one that makes the advising path appear a bit less attractive.

That was a novel – my apologies. Tl;dr version:

Do you think it would be viable for an even further reduction of the .3% fee as Vanguard’s AUM increases, or through additional efficiencies?

Also, how much of an effect do you think Vanguard’s CFPs improved efficiencies will have on the CFP/mass affluent ratio? (The McKinsey report said the “Generalist hub advisors working with mass affluent clients, for example, can work with 500 to 600 clients, far above the typical book of 300 clients in in-person networks.”)

Thanks for providing such valuable content.

Micheal – I was wondering about the Vanguard and Schwabs providing investment advice but only with their products. Clearly, Vanguard is a cost leader, but at some level the suggestions of proprietary products has got to raise conflict of interest questions. Thoughts?

*Michael