Executive Summary

While much of the growth in P2P lending (over $5B in loan volume in 2014 alone!) has been driven by borrowers looking for appealing alternatives to traditional banks and financial institutions like credit card companies, the growth has only been possible because of the matching investor demand. After all, from the investor’s perspective, P2P loan investing is little more than an opportunity to lend money to other individuals and earn an interest rate yield, not unlike any other "bond" investment. Except in a world where Treasury Bonds and intermediate Corporate bonds or CDs may yield little more than 1% to 2%, the P2P loan has a starting yield of 5.3% for “high-quality” notes and an average rate of over 13%!

Of course, the significant caveat with Peer-to-Peer investing is that some loans will default, even over their relatively limited three to five year terms, and thus the final net returns will be substantively lower than the top-line interest rate suggests. After all, P2P loans are unsecured personal loans, often to people who have credit issues in the first place (and thus why they seek out loans with interest rates of 5.3% to almost 30%!).

Nonetheless, the rise of P2P platforms makes it feasible for investors to extensively diversify across hundreds of Peer-to-Peer lending notes by investing into fractional loan shares, managed by technology that facilitates the process of routing a borrower’s loan payments out to what might be dozens or hundreds of investors who each contributed incrementally to the loan.

In fact, the growth of the P2P marketplace, along with the introduction of institutions, is beginning to create the potential for advisors and their clients to access P2P loans, as a unique form of ‘alternative’ fixed income asset class with appealing yields. On the other hand, the growth of institutional buyers may also be pushing available investor yields down, making it harder for individual investors to compete... which is even more troubling given that P2P loans have enjoyed record net returns on the back of an economic expansion, but face the prospective risk that forward returns could be far lower if/when the next recession arrives!

Investing Into Peer-To-Peer Loans

![]() The basic structure of a Peer-To-Peer (P2P) loan is an unsecured personal loan made from a lender to a borrower, and facilitated by major P2P lending platforms like Lending Club or Prosper. Loan limits typically vary from $1,000 to $35,000, with loan terms of either 36 months (3 years) or 60 months (5 years), and monthly payments that amortize principal and interest over the time period.

The basic structure of a Peer-To-Peer (P2P) loan is an unsecured personal loan made from a lender to a borrower, and facilitated by major P2P lending platforms like Lending Club or Prosper. Loan limits typically vary from $1,000 to $35,000, with loan terms of either 36 months (3 years) or 60 months (5 years), and monthly payments that amortize principal and interest over the time period.

![]() From the borrower’s perspective, using a P2P lending platform like Lending Club or Prosper is essentially an alternative to borrowing via a bank or other financial institution like a credit card company, at what is often lower interest rates (theoretically due to eliminating some of the overhead of financial institutions) and more appealing loan terms for the borrower. Which has made peer-to-peer loans incredibly popular as a borrowing platform, particularly in scenarios like consolidation of existing loans.

From the borrower’s perspective, using a P2P lending platform like Lending Club or Prosper is essentially an alternative to borrowing via a bank or other financial institution like a credit card company, at what is often lower interest rates (theoretically due to eliminating some of the overhead of financial institutions) and more appealing loan terms for the borrower. Which has made peer-to-peer loans incredibly popular as a borrowing platform, particularly in scenarios like consolidation of existing loans.

But from the lender’s perspective, loaning money out via a P2P lending platform that facilitates the origination of the loan is simply the functional equivalent of investing into a bond (which itself is nothing more than a contractual loan). And like other fixed income investments, a P2P loan will include payments of interest and periodic repayments of principal for its investor.

Interest Yields And Net Returns On P2P Loans

In an environment where 3-year Treasury Bonds yield less than 1% and 5-year A corporate bonds still only pay about 2%, and 5-year CDs can barely clear 2% yields, the fact that even the highest grade P2P loans offer a whopping 5.3% interest rate may seem highly appealing (even net of the 1% scrape that P2P platforms take for facilitating the borrower-lender marketplace). And in point of fact, the average interest rate across all loans of varying terms is currently over 13%!

Default Risk For P2P Investors

Of course, the significant caveat of any loan-based fixed-income investment – for which P2P loans are certainly no exception – is that not every loan will benefit from the full repayment of principal and interest. Instead, some borrowers will default at some point along the way after having made a few principal and interest payments, and no longer continue to make their payments. This results in either a total loss for the remainder of the loan, or a costly collections effort (of which the P2P platform keeps a share to facilitate the collections process) to recover the remaining principal and interest that will still likely result in a significant charge-off.

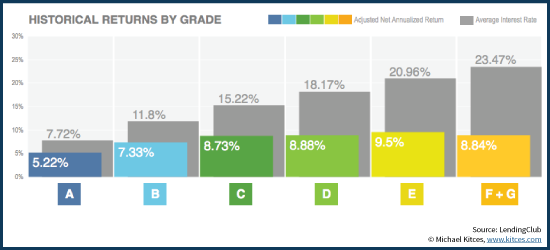

And in point of fact, when it comes to P2P loans, even the highest quality A-rated loans have historically shown a material default rate, resulting in charge-offs that reduce the net investor return. For instance, the chart below shows the difference between the average interest rate charged to borrowers, and the actual net annualized return to the investors who funded the loans; the difference between the two is driven by defaults and the associated charge-offs (as well as the 1% cost drag of the P2P platform), and while the lowest grade loans show the biggest gap (the largest write-offs), even the A-grade loans reflect a non-trivial default rate!

P2P Investment Defaults and Charge-Offs Over Time

Notably, an important caveat of the chart above is that it includes both P2P loans that have fully run their course, and also loans that are still currently open and in payment status (the data includes all loans where borrowers have been making payments for at least 18 months).

This is important, because the default rise generally rises over time, as more and more borrowers are impacted by some financial or life event that may trigger a failure to make timely payments. Thus, just because a loan is performing over the first 18 months at a high rate of return doesn’t mean it will necessarily sustain at that level for the remainder of the 36-month or 60-month loan term.

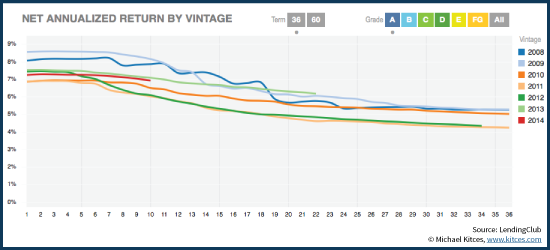

In fact, the Lending Club data shows that net annualized returns on loans ‘inevitably’ decline over time, as the defaults and charge-offs accumulate. And the impact can be quite material.

The chart above shows the net annualized returns over time for loans of various starting vintage years of A-rated Lending Club P2P loans. While interest rates have started as high as 7% to 9% in the past, the subsequent write-offs have led the typical net returns to be closer to 5%, and in the case of the 2011 vintage as low as 4%. Thus, while the more recent 2013 vintage is still hovering around a 7% annualized return, the historical data suggests that this will ultimately decline further. And given that current A-rated loans are only starting with a 5.3% return, the forward-looking default-adjusted expected return may well land in the lower end of the historical range, or even come in below it.

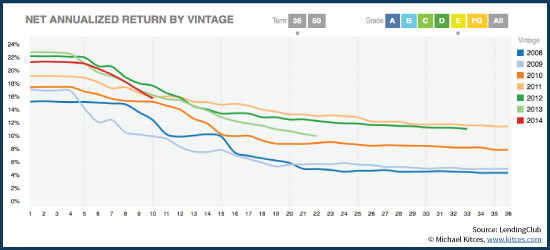

In the lower quality loan categories, the impact of write-offs is far more dramatic, both because the starting interest rates are much higher, but also because the frequency and magnitude of defaults and write-offs can be far more severe. The situation is especially impacted by the economic environment; as the chart below shows, the lowest returning E-rated loans from Lending Club were those made in 2008 and 2009 leading up to and in the midst of the recession, where starting interest rates of 15%-18% finished with net investor returns of just 4% to 5%. As the economy improved (and the platforms increased their risk-adjusted interest rates on low quality loans to adjust) the returns have improved, with more recent vintages enjoying as much as 8% to 11% net returns.

Of course, the improved returns of recent loans were also buoyed by the lack of any recession for the past five years, and the question remains open about how badly the lower quality loans may perform through the next recession. On the other hand, that’s the whole point of taking on a riskier loan in the first place; Lending Club A-rated loans have generally finished with net investor returns in the 4.5% to 5.5% range, while E-rated loans have produced returns varying wildly from barely over 4% to nearly 12%!

Managing Default Risk For P2P Investing With Diversification

As any financial advisor knows, the key to managing default risk (or in general, the idiosyncratic risk of any particular singular investment) is diversification. And this is true more than ever when it comes to making unsecured personal loans to individuals!

Fortunately, today’s P2P platforms are built to allow extensive diversification, by allowing investors to allocate their dollars into fractional loans. The fractional loan process means that when a borrower comes to request a loan – e.g., for $10,000 – the entire $10,000 doesn’t have to be funded by a single peer investor/lender. Instead, investors can allocate as little as $25 towards funding any particular loan, which means one borrower’s loan for $10,000 could be fulfilled by 400 different investors, each of whom puts no more than $25 into that loan.

In turn, not only does the fractional loan process mean that borrowers might be funded by a wide range of investors, it also makes the investing process far easier if lenders wish to diversify into a wide range of loans. Thus, an investor who has $10,000 to invest into P2P loans isn’t required to “bet it all” on a single $10,000 borrower; instead, the investor can allocate $25 into 400 different notes, achieving an extensive level of diversification.

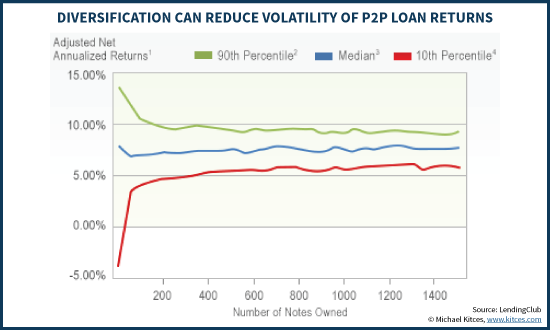

Of course, an investor may still be a little more or less lucky in the particular loans selected, but as the Lending Club data again shows, the number of loan notes the investor owns can dramatically reduce the prospective range of returns. In fact, the historical data shows that once an investor allocates amongst at least 100 notes, where no note is greater than 1% of the total loan portfolio, the probably of having a negative return drops to less than 0.1%, and returns further stabilize as the investor diversifies across 200-400+ loans.

Interest Rate And Liquidity Risk Of Investing In P2P Loans

In addition to the outright default risk of Peer-to-Peer investing, those who wish to allocate dollars must also consider the liquidity of the investment. Or rather, the lack thereof. While major P2P lending platforms like Lending Club and Prosper facilitate the creation of the loan and transfer of the money, once the loan is made the investor is "stuck" waiting for all the principal and interest payments to come in (or not, if there's a default).

Fortunately, though, the growth of the P2P lending world has recently spawned the beginning of a secondary market for P2P loans, which is facilitated through a note trading platform on FolioFN. This creates the potential for investors who have a change of circumstances to have at least some means to sell the note to a third party, though those who are selling notes will not only pay a 1% fee to have the trade brokered, but will also be compelled to accept the highest available bid in a market that won’t necessarily always have competitive bids. In other words, if there aren't many buyers and the only ones available are offering 10% less than what you think the loan is worth, you have no choice but to accept the lower price, or not sell and remain stuck with the loan.

On the other hand, thus far the demand for P2P investing and its appealing yields – and the fact that some investors would prefer to buy already-issued notes with shorter expiration dates – has allowed for a reasonably robust secondary market, with some investor guides suggesting that demand is strong enough that investors may actually be more profitable by selling their notes on the secondary market rather than holding them to maturity. At least given secondary market liquidity and demand today. Nonetheless, investors should be very wary about putting any money in P2P loans that they might need back before the loan is scheduled to mature in 3-5 years!

Notably, another challenge when it comes to the liquidity of P2P loans is that if interest rates rise, buyers will adjust their bids (lower) to account for the change in interest rates. In other words, rising rates will depress the marketable value of P2P loans, just as is the case for any market-traded fixed income investment when interest rates rise. Given their relatively short three-to-five year maturities, the underlying duration of a P2P loan is modest, so even a moderate rise in interest rates shouldn’t impact the price too severely (and as with any “bond” in a rising rate environment, the investor can always choose to hold to maturity and recover the principal payment at par). Still, though, an investor who does need to liquidate by selling a P2P note before maturity will have to consider the impact of both a potential change in price due to changes in interest rates, and also the ‘risk’ of a less-than-desirable bid/ask spread when trying to sell.

Investors should also recognize that if/when the economy turns and a recession occurs, the rising rate of defaults and increased risk causes any bond price to fall as investors and bond buyers reprice risk. When it comes to P2P loans, which already have default rates far higher than even most corporate bonds, the adverse price swing in the event the investor needs to sell early in the face of limited liquidity could be quite severe.

Of course, from the investment perspective, the interest rate risk and relative illiquidity (or at least risk of illiquidity) of P2P loans is also why their yields are more appealing than other more-liquid fixed income investment choices!

Ways For Financial Advisors To Help Clients Participate In Peer-To-Peer Investing

While peer-to-peer investing started out as a largely “do-it-yourself” phenomenon through sites like Lending Club and Prosper, its rapid growth in both borrower demand for loans and investor demand for their appealing interest rates has created new paths and options for investing.

Of course, the starting point for most clients may simply be opening up their own Lending Club or Prosper accounts directly, and beginning the process of selecting loans to invest in. However, as noted earlier, even just investing all of one’s money into a “high quality” P2P loan still entails a material risk of default somewhere along the way (even Lending Club’s A-rated loans from 2009 to 2014 had a 6% default rate where at least one payment was missed along the way). Consequently, as noted earlier, “effective” diversification may require funding 100+ loans (or ideally 200-400+), which in turn entails a potentially-time-consuming process to pick all of those loans (at $50/loan x 400 loans just to allocate $20,000!). For those who were inclined enough to delegate investing decisions to the advisor in the first place, this will probably not be appealing!

The process of selecting loans can be somewhat expedited with the “automated investing” features – Lending Club calls it Automated Investing, and Prosper has an “Automated Quick Investment” (AQI) solution. These tools allow the investor to set up a series of filters to identify new investing opportunities when they come in, and automatically allocate to them. For instance, a filter might target all loans that are A-rated or better, for the purpose of Loan Consolidation, with an Income-Verified borrower, a loan term of three years, and a maximum investment of $200 or 1% of the total loan value. Once the investor funds their P2P platform account with cash, the tool will “go to work” allocating the dollars as new lending/investing opportunities come in, until eventually all the cash has been deployed into various P2P loans that fit the criteria. (Advisors should beware of simply obtaining client passwords to log into P2P lending sites to do this on behalf of clients, which may trigger SEC custody rules!)

The growth of the P2P marketplace has also spawned a number of pooled investment funds designed to allocate dollars into these types of fixed income ‘alternative’ investments. These ‘institutional’ investors include NSR Invest, Prime Meridian Income Fund, Petra Credit Fund, and Blue Elephant Capital Management, who all make various forms of P2P-investing funds available to investors (through various types of investment vehicles/structures). And earlier this year Blackrock was the first to securitize a package of Prosper loans into the $327M “Consumer Credit Origination Loan Trust 2015-1”.

In fact, some P2P marketplace commentators have suggested that the entrance of institutional investors means the P2P lending space will soon be dominated by them, and individual investors will be edged out of the process. As is, institutional investors allocating larger dollar amounts have begun to buy/invest into whole P2P loans rather than just investing fractionally (an individual diversifies $20,000 into 400 fractional units of $50, but an institution can buy 400 loans of $20,000 each to allocate “just” $8,000,000!). As a result, the volume of fractional loans to plummet from 100% of the marketplace to barely 10% in just the past two years (and now the new startup Orchard is working on deepening the whole loan secondary marketplace for P2P loans).

Advisors who want to explore P2P investing through a separately managed account structure now have a few solutions as well, including a managed account structure with NSR Invest, and the first self-proclaimed “robo-advisor” of the P2P industry called Lending Robot.

Notably, since P2P loans are ultimately little more than a form of bonds – and are even registered as such with the SEC – they can not only be purchased with after-tax dollars in an investment account, but be held within an IRA or Roth IRA as well. However, most ‘traditional’ custodians are not prepared to hold P2P loans, thus generally requiring either a retirement account directly with one of the P2P platforms, or through a self-directed IRA custodian that knows how to handle such investments. Nonetheless, given the high yields on P2P loans – and especially the high rate of interest that is initially paid, until any defaults and charge-offs begin – holding P2P loans generating a high level of ordinary income within an IRA or Roth may be especially appealing from an asset location perspective.

Ultimately, though, the bottom line is that in a world where advisors and their investment clients have struggled to find appealing fixed income investments, the availability of the P2P investing marketplace raises the potential of a new form of ‘alternative’ fixed income investment solution. Some have even called it a new asset class. The fact that investment choices are still limited, and may require removing assets from a traditional investment platform makes it challenging for advisors to ‘manage’ the funds (and charge fees accordingly) in today’s environment.

Nonetheless, the continued growth of peer-to-peer investing, including the expansion of new pooled investment funds, institutional investment managers, separate account managers, and technology overlays to facilitate the investing process, suggests that choices will increasingly become available for advisors. However, advisors must still bear in mind that P2P investment involves risk – even when diversified across hundreds of notes – and that gross investment yields shouldn’t be confused with the expected net returns, especially recognizing the impact that a future recession will someday have.

So what do you think? Have you ever guided clients to invest in P2P loans? Have you ever participated on a Peer-to-Peer investing platform personally with your own dollars? Do you see the P2P marketplace as a new fixed-income asset class? Share your thoughts in the comments below!