Executive Summary

Historically, different financial advisors operated different business models depending on their industry channel - RIAs managed investment portfolios, while wirehouses sold proprietary products and securities from their inventory, and independent broker-dealers sold third-party investment products. Accordingly, asset managers and product manufacturers aligned their investment wholesalers to those channels, with one for wirehouses, another for independent broker-dealers, and a third for the independent RIA community. The challenge, though, is that as the advisor value proposition evolves, along with industry business models, and the regulatory environment, the "traditional" industry channels are breaking down as a way to segment financial advisors!

In this week’s #OfficeHours with @MichaelKitces, my Tuesday 1PM EST broadcast via Periscope, we discuss, from the investment wholesaler perspective, the four different types of financial advisors that have emerged, how they differ based on client approach and value proposition, and how wholesalers can best add value to these different types of advisors!

The key issue is to recognize that financial advisors tend to have fundamentally different ways in which we frame our own value proposition, and approach client situations, that are no longer necessarily defined by industry channel. And this matters, because when companies with their own wholesalers are trying to reach advisors, the ways in which an advisor approaches their clients and define their own value proposition heavily impacts what that advisor will and will not see as valuable from their wholesalers!

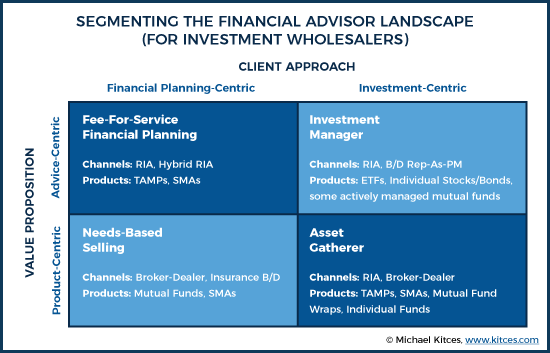

For instance, some advisors taking a very financial planning-centric approach to clients, while others are more investment-centric. And when it comes to delivering value to clients, some are more advice-centric, and others are more product-centric. Thee various combinations result in four categories of financial advisors: (1) fee-for-service financial planners; (2) investment managers; (3) needs-based sellers; and, (4) asset gatherers.

From the perspective of the wholesaler, it is crucial to recognize that each of these segments receives different value from a wholesaler, and demands different types of products and services. Because if an advisor is an asset gatherer, they are going to want to see a product that can easily help them gather assets... but if they are needs-based sellers, they will want planning strategies and sales ideas... and if they are an investment manager, they will want products that they can manage to demonstrate their own expertise (without outsourcing to other active managers!)... and if an advisor is a fee-for-service financial planner, they will want solutions that help them simplify investment management to free up time to service clients and focus on planning. Thus, investment managers (which might be an RIA or a Rep-As-PM at a broker-dealer) tend to use stocks, bonds, and ETFs, but asset gatherers (which might be RIA or at a broker-dealer) are more likely to use multiple TAMPs and SMA, and fee-for-service financial planners (usually RIAs) will typically just use one TAMP for all of their assets and be uninterested in individual investment products at all!

The bottom line, though, is simply to recognize that the whole advisory industry is in the midst of reorienting itself, and trying to segment financial advisors by wirehouse, broker-dealer, and RIA industry channel no longer works. Advisors are reinventing their value propositions and where they focus, while DoL fiduciary further forces firms to re-draw their lines and tech innovation accelerates these trends. Which means, if wholesalers want to reach financial advisors and add value to them, wholesalers need to pay attention to the four different types of financial advisors!

(Michael’s Note: The video below was recorded using Periscope, and announced via Twitter. If you want to participate in the next #OfficeHours live, please download the Periscope app on your mobile device, and follow @MichaelKitces on Twitter, so you get the announcement when the broadcast is starting, at/around 1PM EST every Tuesday! You can also submit your question in advance through our Contact page!)

#OfficeHours with @MichaelKitces Video Transcript

Welcome, everyone! Welcome to Office Hours with Michael Kitces!

You may have noticed from the background here that I'm not at the office today. I'm actually here at Morningstar. I've been talking a little bit about investments and asset managers today. Actually, it's kind of been the theme for the week. Yesterday, I was onsite with another firm, consulting with the leadership of a fairly big investment management outsourcing firm that's looking to grow its reach with RIAs. And they made this comment that despite the fact that all of us call ourselves "financial advisors" by name, that advisors in the RIA channel are very different than advisors in the broker-dealer channel. And I thought it was a good reminder that despite how widely we use this label 'financial advisor', that those of us in different industry channels focus our advisory firms in some very different ways.

And part of that is just because the different channels tend to be built around different business models. Brokers historically earned a commission and RIAs earned AUM fees. But even amongst broker-dealers, some advisors are employee-based and their home office provides most of the guidance and resources. Others are independent broker-dealers where the advisors themselves have a lot more independence about how they structure their own firms. And, as a result, I find when investment firms try to sell to financial advisors, they often delineate us across the channels.

For a lot of big national asset managers, there's a set of wholesalers for RIAs, there's another set of wholesalers for independent broker-dealers, there's maybe another set of wholesalers just to call on the wirehouses, and maybe there's a separate national account or key accounts team that focuses on wholesaling to firms that centralize their investment offerings. Because, if I'm a registered rep at broker-dealer but I use the home office to design portfolios, it doesn't really make any sense for the wholesaler to spend time with me as the rep. You've got to send someone from national accounts wholesaling to the home office if you want to get onto that platform.

But beyond just the different industry channels, I think we also have fundamentally different ways that we as advisors are now framing our own value propositions in approaching client situations. And it matters because so many investment firms now, I find, with their wholesalers, they're trying to reach us as advisors, whether it's firms looking to serve advisors outsourcing investment manager responsibilities, other tech firms and platforms serving us, and especially financial services product manufacturers trying to distribute products through us to our clients, the ways we approach our clients and define our value proposition really impacts what we do and don't see as valuable from wholesalers. But when the wholesalers don't recognize that, we get all these awkward mismatches that just don't line up anymore with traditional industry channels.

Financial Planning Oriented vs Investment Oriented & Product-Centric Vs Advice-Centric [Time - 2:49]

I'll give you an example of this. Some financial advisors have a client approach that is very investment oriented. They approach clients as, "I'm here to help you invest your money." So, the advisor might manage it themselves or maybe they buy mutual funds or maybe they outsource it to someone else, but they focus on portfolios.

By contrast, other advisors are very financial planning oriented in the approach. They lead with financial planning. Every client starts with a financial plan. They might produce the plan themselves, they might delegate it, they may use a third party firm or home office to help create it, but they view the financial planning as the primary approach and focus, and only secondarily do they then plug in investment products because at some point, even if you're giving advice, the money's got to land somewhere.

Now, a second way to think about advisors, is what we get paid for. Some of us get paid for our products and some of us get paid for our advice itself. So, an advice-centric financial advisor views their primary product value proposition usually as themselves. They see it as, "It's my knowledge. It's my expertise. The client pays me for my personal value." That's an advice-centric value proposition.

Now, for other advisors, they're more product-centric. The primary value that they bring to the table is the quality of the products they provide. So, the job is to implement a financial services product, and the better products I have as a product-centric advisor, the more things I could sell, and the more things I can implement with clients. But the value isn't me per se, the value is my ability to bring valuable products to the table, for my clients.

Four Types Of Financial Advisor Value Propositions [Time - 4:20]

Here's why this segmentation matters. Bear with me a moment. Think about this as like a two-dimensional grid. So, on the left side we've got financial planning-centric advisors, on the right side we have investment-centric advisors. And then across the top we have the advice-centric advisors, and across the bottom we have the product-centric advisors. So, we now kind of got this two-by-two grid where people line up in different categories.

The upper left would be financial planning oriented advisors that are advice-centric. This is the domain of those who offer a primarily fee for service financial planning. They focus on financial planning advice, the value is the person who gives the advice. It's the advisor. So, this would include advisors that charge hourly, project, and retainer financial planning fees. I think it even includes a subset of advisors that maybe charge for assets under management, but in the end, the portfolio is not meant to be the value. It's usually a very simple portfolio. Because the client isn't really paying for the portfolio, they're paying for financial planning advice, and maybe it just might be easier to bill a portfolio if they have assets anyways.

So, when we look at financial planning-centric advisors, we have a different grouping than the rest. And the interesting phenomenon is that I find they often span channels. Now, planning fee for service advisors tend to be independent RIAs or at least dual-registered, because I can't actually get paid a fee under a broker-dealer form and I've got to have an RIA or a hybrid registration.

But here's why it matters from the perspective of investment wholesalers that come at us. When we're financial planning-centric, we tend to outsource our investments. For instance, these are the RIAs that use TAMPs, because the advisor's value proposition isn't focused on the investments, it's focused on the financial planning. They're often quite comfortable to delegate the non-essential investment process to a TAMP. And many advisors that are planning centric, they just kind of pick one TAMP for everything. Pnce you find a reasonable solution to plug in after you do the real planning stuff for clients, why bother with more?

Now, the upper right corner is different. These are the investment oriented advisors that are still advisor-centric. So, these are typically the advisors that view their primary value proposition as their ability to implement quality investments for clients. Now, the key distinction here is the investment oriented advisor who is advice-centric doesn't want to use products to implement. They don't want to use actively managed funds, they don't want to use separately managed accounts, they don't want to use TAMPS. Their investment ideas, their strategies, their ability to pick the right investments, that's their value as the advisor.

Again, this matters from the perspective of wholesalers who typically approach us, and particularly because this isn't specific to a channel. There are RIAs who are investment oriented and advice-centric. They created the RIA to build portfolios for the clients, but there are also registered reps and broker-dealers who did the same thing. It's even got a label now. It's called Rep-as-PM, which is short for rep as portfolio manager, because as the name implies, it's the rep who's trying to create the value for clients by being the portfolio manager.

Which is important because if you're a wholesaler and I'm an investment oriented advice-centric advisor and you come at me with actively managed funds, SMAs, and a TAMP, you're wasting your time. Whether I'm an RIA or a Rep-as-PM or at a broker-dealer, I'm not investing with your solutions because I'm going to do it myself, because that's my value.

And I think this is actually where ETFs are shining right now. For a lot of investment-oriented advisors, we don't necessarily have time to do individual stock analysis. Though some may have a stock picking process or they grew large enough to hire an investment team to help, it's certainly not all advisors.

For a lot of advisors that are in this investment oriented category, ETFs are just an easier building block to manage than individual stocks. And so, the investment oriented advisor often then ends up using ETFs. But here's a key point to it. It's not that the investment oriented advisor is buying ETFs because they're going passive. They're actively managing the ETFs.

But because the advisor says their value proposition is actively managing the ETFs, this is why even with all the growth of ETFs, I'm incredibly negative about actively managed ETFs. Because I think the investment product manufacturers have missed that the advisors who are using ETFs and managing them in their portfolios, it's because the advisor wants to be the one adding value. I don't want to hire some other active manager because then the client's going to say, "What do I need you for? I could have bought the active fund directly." The advisor says, "This is my value," so they're not going to adopt actively managed ETFs they're not going to adopt actively managed mutual funds, they're not going to adopt SMAs, and they're not going to adopt TAMPs, because they build the portfolios themselves. But again, this isn't specific to industry channels. This can be Rep-as-PM at a broker-dealer, or this can be a particular subset of independent RIAs that say investments are their value proposition.

The lower right corner is the third group. These are the investment oriented folks, because we're still on the right, but product-centric because we're across the bottom now of our little two-by-two grid. For these advisors, they may be focused on implementing investments, but their value isn't meant to be hands-on management of the portfolio. It's their ability to find good products, good third party managers, and bring those solutions to the table for their clients. This is where you see actively managed mutual funds, or maybe in the future, actively managed ETFs. This could be a series of separately managed accounts, this could be a TAMP, or several TAMPs.

And in fact, one of the key points of investment-oriented but product centric advisors is that they often use a pretty wide range of solutions. So, if the client wants a bond manager, they'll get a bond manager. If the client wants a socially responsible investing approach, they'll find a TAMP or an SMA to build it. If the client wants a certain portfolio, they'll find a manager or bring it to the table. Because if they're really trying to build a scalable business, they may eventually simplify that down to a couple of core providers, the go-to products that I know work, that I know I can sell my clients on, that they're persuaded by.

But for the investment oriented product-centric advisor (and this is where most investment sales people really live), they function more like asset gatherers. Their goal is just to gather assets. I'll gather assets into actively managed mutual funds, or SMAs, or TAMPs, whatever it takes. I'm just trying to gather assets, sell products, bring in dollars, and might use a wide range of solutions to do it.

But here again, asset gatherers exist across channels. There are RIAs that are very focused on asset gathering, they might use one or multiple TAMPs to collect assets. There are registered reps at broker-dealers that focus on asset gathering and might use a wide array of funds and SMAs and TAMPs in their platform. You know, whatever it takes to gather assets, they'll find a product to fill the void.

But from the wholesaling perspective, this is a very different type of advisor. This is the advisor where you can give them products to check out and try to get a share of their wallet, or clients' wallets, with that product. But you have to show them how to sell it, like what's the pitch? How is it different and better than the products that they currently pitch? That doesn't work for investment oriented firms that are advice-centric because the advisor says, "No, no, I'm the gatekeeper that picks the stuff. I don't sell the stuff." That's the key difference between advice oriented advisors, where the value proposition is me, and product oriented advisors. With advice oriented advisors, they tend to be a gatekeeper. With product oriented advisors, they tend to be a sales distribution channel.

Now, the bottom left, the fourth of our little two-by-two grid is the financial planning oriented but product-centric advisor. This is the classic domain of needs based selling. Advisors who lead with a financial plan, find out what clients need, and then just implement whatever product they need at the end. But the key point is that they lead with financial planning and then get paid for product implementation. This is the domain of planning oriented brokers and planning oriented insurance agents as well. They'll do financial planning for the clients because that's how they determine what's appropriate to sell at the implementation phase. They don't lead with the products. They don't say like, "Hey, I've got this cool fund that you should check out." They lead with, "I'm going to do some financial planning for you, but ultimately, the value at the end is..." and then I'm going to implement some products to solve whatever problems come up.

Because these advisors are product-centric and get paid for products, they are in practice most likely to be at broker-dealers. Because, historically, that's where needs based selling essentially emerged, broker-dealers and insurance companies. Do the financial plan, implement the client needs at the end. You know, financial planning is a highly effective way to determine clients' needs and then sell them whatever they need. We've proven this over several decades now.

But from the wholesaling perspective, this approach is a little bit different. Investment-oriented advisors who are product centric want product ideas they can pitch and sell. Financial planning oriented advisors who are still product centric want planning strategies, sales ideas that fit planning strategies. If you see a client with this situation, here's a cool product we have that fits this particular need. Because it's not about selling the products, it's about solving client needs with a product. It's a different approach.

And, as a result, I actually find in practice that these are often the advisors that end up with the widest range of different investment products. Perhaps lots of actively managed funds that fit one client need and some SMAs that fit another client need. As a wholesaler, you can get a share of their wallet by only having a product that fits a specific planning strategy or need. Because, if they see a lot of clients with a lot of different needs, eventually you'll get a share of that advisor's wallet. But you have to lead with, "How does this fit a client's planning need?" not, "What are the features of this product in particular?" It's an important difference.

The Breakdown Of Financial Services Industry Wholesaling Channels [Time - 13:30]

We've got these four different types of advisors: the fee for service financial planners, investment managers, asset gatherers, and needs based sellers. Four different ways that advisors approach client situations and frame their own value proposition, four different perspectives on what kinds of investments are best to meet the needs of their business, and very different likelihoods to use different types of solutions. TAMPs are primarily the domain of the advice oriented financial planners on the upper left, and the asset gatherers on the lower right. Those investment oriented product centric folks or planning-centric advisors who just don't even really want to do the investment stuff. They just recognize the client's money, hustle it in somewhere.

SMAs may also get used by asset gatherers, but unique SMA strategies are particularly good for those in the needs based selling category in the lower left. By contrast, ETFs are primarily getting bought by investment managers in the upper right, as well as TAMPs themselves that are kind of being investment managers and then gathering assets under it. Because they view their value proposition as being the investment manager, so they don't want to pay an active fund manager, TAMP, or an SMA. They want to get that advisory fee for managing the assets and then pick the appropriate building block. I think that's where a lot of the adoption of ETFs in particular has been.

But again, I can't emphasize enough that for any wholesalers out there, just looking at industry channels at this point is a terrible way to segment advisors. There are investment manager types in broker-dealers, there's Rep-as-PM, and then RIAs. But not all RIAs want to be investment managers. Some just want to do financial planning and might outsource to a single TAMP. And then others are aggressive asset gatherers and then they might also still outsource to some TAMPs and SMAs. But if you come with a better product, you might get a slice of their business. If it's a planning-oriented advisor, you're either going to win all their business or you're probably going to win none of it because they tend not to split because they just want to find a straightforward investment solution so they can get back to focusing on the financial planning.

The other key point of this is to recognize that however the advisor is focused, that's also how the advisor wants to be approached. But if I'm an investment manager who picks investments for my clients, you have to approach me as a gatekeeper that picks investments. You know, show me your one best product that might make the cut in my portfolio and maybe I'll decide it's worthy. Although, in all likelihood, I'll probably just tell you, "Go away and stop bothering me. If your product comes up in my analysis, I will call you."

But if I'm an asset gatherer and you can give me a product that I can easily gather assets into, ideally one that this is so great it sells itself, I might be very, very interested. Now, on the other hand, if I'm focused on needs-based selling, don't come at me with products. Come at me with planning strategies and sales ideas which your product happens to fit into. And if I'm focused on fee for service planning, again, just don't even bother trying to get a slice of my assets. Either be my trusted partner that I can outsource to entirely, or just don't waste your time and mine.

But the bottom line is just to recognize that the whole advisory industry is in the midst of reorienting itself, of redrawing its dividing lines, where we're reinventing our value propositions and we're refocusing. And frankly, I think DoL Fiduciary is just accelerating some of this change, as is the tech innovation overall. And just think about it for a moment. There are advisors at large independent RIAs, Merrill Lynch, Vanguard, Schwab Private Client, who all operate as fiduciaries, use centralized investment management propositions, and lead with financial planning. Whoever thought that an independent RIA, Merrill Lynch, Vanguard, and Schwab would be a shared distribution channel in the industry, in the same category, or that RIAs and subset of asset gatherers at broker-dealers would fuel the growth of managed ETF portfolios? All of these dividing lines in the industry are getting redrawn across the channels to the point that channels don't work anymore. You have to carve it up differently.

I hope that's some helpful food for thought, and perhaps for some of you a new or different way to think about how to divide and segment the financial advisor landscape. This is Office Hours with Michael Kitces. Normally 1 p.m. east coast time on Tuesdays, but because I was onsite consulting with a large investment manager that's trying to understand our space yesterday, I had to record today instead. Thanks for hanging out. I appreciate you joining us, and have a great day, everyone!

So what do you think? Do financial advisors vary based on client approach and value proposition? Do you wish wholesalers would better segment the market to provide value to you? Please share your thoughts in the comments below!

This matrix of 4 clear cut new channels is exactly what prevents financial professionals from being a fiduciary and causes the lack of value and lack of credibility with the public. Any one doing needs-based selling is just selling whatever client wants to buy with no context of what is in client’s best interest, rep as a PM investment manager is again has no clue of what is client’s best interest because he has not done the necessary discovery with a comprehensive financial plan, financial planner has discovered what is best for the client but now disintermediates himself from executing on it by outsourcing investments to cookie cutter third party and thus fails the client by not delivering investment execution of the plan, and asset gatherer is just a pure salesman who want to sell as much as possible by doing the least possible. If this is the definition of advice in our industry we deserve what we get. Why can’t a good advisory team be focused on asset gathering and implementing a fiduciary personalized solution set for each client consisting of comprehensive financial planning closely integrated with investment execution in a portfolio management context which includes asset allocation and manager selection including active and/or passive managers or if a TAMP exists that has the right methodology and portfolios that optimally fit the specific client than potentially outsourcing that portfolio management to that TAMP?

Hi Michael – great content, as always!

I was thinking about how a fund company would approach this and I got stuck.

I’d love to divvy my sales team up according to the 2×2 to align the pitch to the (accurate) buyer personas you laid out.

RIAs aren’t that difficult because of the sheer amount of information (Form ADV 2A in particular).

Broker-dealers/IBDs are FAR more difficult – they don’t report discretion, AUM, and in many cases, there is scant information on the site (for example, UBS is about as sparse as it gets, generally).

In other words, there’s little information despite some vague leading indicators that might help sort them into their representative buyer persona. Even then, that’s a highly manual process of investigating each prospective advisors’ site and inputting the data.

I agree with your admonishment to wholesalers not to force a square peg into a round hole. However, one can only segment as deep as the available information permits.

Do you mind commenting on how one might approach this problem from the wholesaler perspective?

Thanks in advance!

-Alex @clarky1120 on Twitter

Alex,

Thanks for the comments!

I definitely hear your concern that once our segmentation transcends ‘normal’ industry channels, it quickly gets a lot harder to figure out who’s who. :/

From a practical perspective, I have to admit that I don’t know offhand where you can go to slice-and-dice rep-level data at a broker-dealer. However, you CAN look at the broker-dealer itself, and often get some sense as to where at least a majority of their reps are probably tilted, which provides some baseline to work from. For instance…

– Many/most broker-dealers will provide information about whether or how much Rep-as-PM business they do. That at least lets you begin to understand how many B/D reps are acting as investment manager.

– You can generally find out if the broker-dealer has a corporate RIA, and if so what portion of their reps are dual-registered (and sometimes even the split of their revenue between B/D and corporate RIA). This can give you at least some sense as to whether there are advisors there in the upper left (planning-centric) or lower right (asset-gatherers that might be using the corporate RIA as their internal TAMP).

– Looking at the percentage of B/D revenues that are commission-based vs fee-based (available from a number of media publications that track B/Ds) can give some indication as to whether the B/D is tilted more towards the fee-based asset gathering activities (lower right) or not.

– Ask the B/D what percentage of their reps have CFP certification. It’s certainly not perfect, but can actually be a decent proxy for their planning tendencies, which can help to guide you about whether the advisors there are likely to be lower-right or lower-left.

I hope that helps a little as food for thought?

– Michael

This is very over-simplified and misleading

There are plenty of what you call planning and advice-centric advsiors at both wirehouses, independents, etc., not just RIAs and Hybrid RIAs

Having been in both worlds over the last 10+ years, it seems that anyone who is in an RIA model and hasn’t seen the wirehouse from the inside post-2005 has no concept of how their business models have changed with regards to their advisors

Most of the big wirehouses now have a diverse group of FAs at nearly every branch with individual and teams that cover all 4 of your quadrants; fee-only teams, corporate retirement plan teams, straight up old school brokers, PM asset gatherers, etc.

The real problem is that whether wirehouse, independent, hybrid, bank, insurance company, etc., the public cannot differentiate between true nature of advisors, their credentials, their quality, etc.

It would be nice to see one of the regulating bodies come out and apply the fiduciary standard (not the micromanagement DOL law, but a true simple fiduciary standard) across all activities for FAs that qualify themselves as “Financial Advisors” and then label brokers as “Brokers” and insurance salesmen as “Insurance Advisors” etc.

That would be a good start

Jeremy,

You can be operating as a hybrid under all of the channels you listed. “Hybrid” vs “independents” aren’t alternatives. By definition, a hybrid is a COMBINATION of an RIA (independent or corporate) and a broker-dealer (independent or wirehouse).

I never stated that planning and advice-centric advisors can’t be found at wirehouses and independent B/Ds – I simply noted that they’d have to be operated as a hybrid (either under an independent or corporate RIA), because you can’t legally charge a client a planning fee under a pure B/D arrangement. There has to be SOME (corporate) RIA involved, thus hybrid (or at least dual-registered under the parent company)…

– Michael

I’m forever bemused at the universally used term ‘advisor’ as relates to personal financial counsel. If I, the consumer, am looking to buy a replacement car and I go into the new-car showroom, should I refer to the person who cheerfully greets me as my personal transportation consultant? No?? Well, that’s the new car version of a financial advisor as we use the term today.

Advice is not advice if a third party is paying someone else to give it to me….that’s sales. In such an arrangement, it is my job as the consumer to take the advice in the context it is offered….sales…. and from this to make the decision I feel will be in my own best interest. Its not that I think vacuum cleaner, furniture or car salesmen are corrupt liars trying to extract as much money from me as they possibly can….they may indeed be trying to meet their perception of my need with the product line(s) they carry. But the hard reality is if they don’t move the product, they don’t get paid. My actual need as the consumer may be central, peripheral or have nothing to do with this.

When a second party is compensated only by me, the consumer, and the advice eventually provided to me is completely independent of what they charge me, and the second party offering the advice has comprehensive technical training and creditable experience…..this arrangement is as close to a true personal advisor.as we’re going to get.