Executive Summary

After giving a ‘sneak preview’ in early 2014, this week the CFP Board formally launched its new Center for Financial Planning, a “virtual entity” within the CFP Board that aims to support the future of the financial planning profession.

Armed with a multi-million-dollar founding sponsorship from TD Ameritade, the Center for Financial Planning will focus on attracting and developing the next generation of financial planning professionals, improve gender and racial/ethnic diversity amongst financial planners, and provide a home for financial planning academics, including the launch of a new Wiley-published academic journal for financial planning researchers to publish and get credit towards tenure.

Yet while these are laudable goals for the CFP Board to pursue, it is notable that the new Center for Financial Planning initiatives move the CFP Board into even further conflict with the FPA, which similarly has its own NexGen effort, its own diversity initiative, its own partnership with the Academy of Financial Services to provide a home to academics, and its own Journal.

In fact, the Center for Financial Planning’s vision to become “the premier resource in the financial planning profession for educators, researchers, practitioners, financial services firms and the public“, combined with the CFP Board’s effort to raise a whopping $10M of capital for the organization in the next five years – far in excess of what it needs to operate its current initiatives – raises the question of whether the CFP Board is seeding the Center of Financial Planning to become a competing membership association against the FPA, just as the FPA’s own market share of CFP certificants continues to sink to record lows.

Given the CFP Board’s long history of its own debacles, arguably in the long run it is better to have a strong and vibrant FPA operating as a membership association outside the CFP Board, and functioning as a check-and-balance to hold the CFP Board accountable. But with FPA facing its own woes as revenues continue to decline, and the potential Department of Labor fiduciary proposals risking a disruption to FPA’s own crucial sponsorship revenues, the CFP Board appears to be positioning itself for the possibility that the FPA may stumble… and perhaps is even trying to compete and hasten the FPA’s demise.

The CFP Board’s Center For Financial Planning – Sponsored By TD Ameritrade

This week, the CFP Board formally launched its new Center for Financial Planning, an initiative that was initially announced early last year but took over 18 months to fully take shape.

The declared purpose of the Center for Financial Planning is “to ensure a vibrant, sustainable future for the financial planning profession” with a focus on: creating a sustainable (and more diverse) supply of advisors to replacing those who will soon retire; conducting third-party research; building a repository of the financial planning body of knowledge; providing a home to financial planning academics; and convening a wide base of stakeholders to achieve these outcomes.

The Center for Financial Planning will be funded by a massive “multi-million-dollar multi-year” lead founding sponsorship from TD Ameritrade, and also includes contributions from individual donors as well. Additional corporate sponsors will be solicited in the coming year as well, and CFP Board CEO Kevin Keller has indicated a goal of raising $10M to $12M in the next five years.

Expanded And New Initiatives Of The Center For Financial Planning

Initially, the Center for Financial Planning will focus primarily in the areas of workforce development (attracting and developing the next generation of financial planning professionals), diversity (improving both gender and racial/ethnic diversity within the financial planning profession), and establishing a home for the growing base of financial planning academics teaching and doing research in financial planning.

Notably, the CFP Board has already made efforts in several of these areas. Late last year it launched a Career Center sponsored by Fidelity to support workforce development, and has spent nearly a decade ramping up the growth of financial planning undergraduate and graduate school programs (which now number a whopping 140 baccalaureate programs with 45 more in development, up from only 54 programs in total just 15 years ago!). Last year, the CFP Board launched its Women’s Initiative to increase the percentage of female CFP certificants above the 23% threshold where it has hovered for over a decade. And the CFP Board already supports financial planning academics with both an annual Program Directors conference for financial planning academics, and publishing the Financial Planning Competency Handbook.

All of these existing initiatives will be housed under the CFP Board’s new Center for Financial Planning, along with additional programs that will roll out in the coming years. The CFP Board has indicated that it will convene a “design summit” in early 2016 to delve further into deciding what the Center’s structure and programs will be in the future, though a new racial/ethnic diversity initiative to complement the Women’s Initiative is already planned.

Launching A New Journal For Financial Planning Academics

Also included as part of the Center for Financial Planning’s already-announced new initiatives is the launch of a new journal for academic research on financial planning.

While other journal publications already exist – from the Journal of Financial Planning published by the FPA, to Financial Services Review published by the Academy of Financial Services – the primary challenge of those publications is that professors seeking publishing credit for tenure, particularly at AACSB-accredited business schools, often get little or no “credit” for research in these publications. Unfortunately, while both are peer-reviewed publications, they are not viewed as “competitive” enough compared to other business journals, and the Journal of Financial Planning is further adversely impacted because it operates as a ‘blend’ of academic journal and industry trade magazine.

The CFP Board hopes to fill this gap with its new Journal offering, which will be published by Wiley (the organization that also publishes respected Journals like the Journal of Finance, and many of the AICPA’s Journals as well). Ultimately, the goal is not only to support a wider and deeper range of financial planning research to advance the professional body of knowledge, but also to encourage business school academics to adopt and advance financial planning programs by providing a “reputable” journal in which they can publish actual financial planning research and earn academic tenure credit.

The new Journal has yet to receive a formal name, and still awaits the appointment of a formal editor, but will ostensibly launch sometime in 2016.

Governance And Structure Of The Center For Financial Planning

Although dubbed with a unique standalone name – the “Center for Financial Planning” – the CFP Board has indicated that ultimately the organization will simply be a “virtual entity” housed within the CFP Board’s existing infrastructure. Although currently supported by existing CFP Board staff, Keller indicates that future staff are expected to be hired, both to lead the Center’s various initiatives, along with an editor to direct the new Journal. On the other hand, the significant fundraising effort of the Center should avoid any need for the staffing and infrastructure of the Center to impact ongoing CFP certification dues (as a multi-million dollar fundraising effort should be more than ample to cover the handful of staff that would be needed to support the Center’s currently proposed initiatives).

The leadership/governance structure of the Center will include an advisory council (to be formed after the design summit) for directing programs and providing guidance to CFP Board leadership, supported by a second advisory council to direct specific initiatives (e.g., for diversity), and a development committee for additional fund-raising.

Center For Financial Planning To Support The Future Of The Financial Planning Profession

In a world where the CFP Board has historically focused all of its effort on establishing and maintaining the CFP marks and not necessarily championed the broader financial planning profession – a focus consistent with its mission, but one for which it has often been criticized – the CFP Board’s shift to supporting the advancement of the financial planning profession is notable. As the Center notes on its new website, its ultimate vision is “To be the premier resource in the financial planning profession for educators, researchers, practitioners, financial services firms, and the public” with a mission focused on “building capacity for the financial planning profession” along with “building a body of knowledge and an academic home to support the growing discipline of financial planning”.

In this context, the CFP Board’s effort is laudable, and helps to fill the gap in several crucial areas. Although it will take years to fully establish credibility, a bona fide ‘academic’ journal able to generate tenure credit for professors in AACSB-accredited business schools is a significant step in expanding financial planning into business schools and higher-tier academic institutions. And diversity – in terms of both gender and racial/ethnic inequality – has been a long-standing issue for both financial planning in particular, and the broader financial services industry.

The CFP Board’s efforts to further attract and retain younger professionals into financial planning is equally crucial for the long-term viability of the profession – an area where the CFP Board has already made notable progress, as while there are still more CFP professionals in their 70s than their 20s(!),the CFP Board recently announced that the average age of a CFP certificant is finally beginning to decline, and has dipped under age 50 for the first time in many years. Continued efforts to increase the number of undergraduate and graduate students coming into financial planning programs, and then encouraging them to sit for the CFP exam and actually become financial planning practitioners, is crucial for the long-term growth and viability of the profession.

The Converging Collision Course Of The FPA And The CFP Board

On the other hand, while the CFP Board’s efforts to improve diversity, workforce development, and the academic base of financial planning are laudable, the fact that it’s the CFP Board making the effort – albeit through its new Center for Financial Planning – puts the organization in ever-increasing competition with the Financial Planning Association.

For instance, while the CFP Board has announced an intention to grow a diversity initiative (to complement its Women’s Initiative), the FPA already has a diversity initiative. The CFP Board will engage in research on how to improve and advance the financial planning profession, but the FPA already has its own Research and Practice Institute. The CFP Board will now provide a financial planning research journal, but the FPA already has a financial planning research journal, and when the FPA expanded its relationship last year with the Academy of Financial Services to support the Financial Services Review Journal it was the CFP Board that pre-empted the news with its own Center for Financial Planning announcement – despite the fact that we can now see the CFP Board was still over 18 months away from being ready to launch

And these conflicts between the CFP Board’s new initiatives and the FPA’s existing programs are simply an extension of other recent CFP Board expansions into the FPA’s role as a membership association. For instance, the CFP Board also launched its Career Center late last year, but the FPA has had its own financial planning Job Board for years. And of course, there’s the CFP Board’s ultimately-thwarted attempt to become a CFP CE provider that would have put it directly into competition with the Continuing Education events and programs that are the financial lifeblood of the FPA.

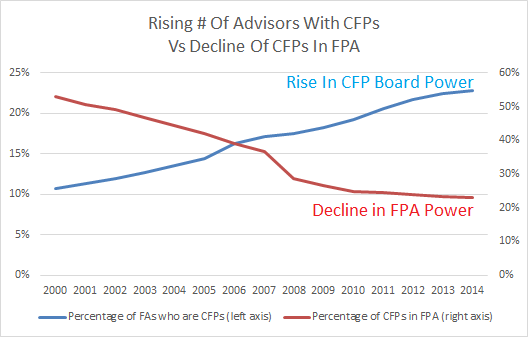

And notably, in a world where the CFP Board and the FPA will be engaged in simultaneous initiatives, the CFP Board is still a significantly larger organization, with 73,000 CFP certificants as a base, compared to “just” about 24,000 FPA members (of which only roughly 18,000 are CFP certificants). According to their respective Form 990s, the FPA runs an annual budget of just over $9M, with just under $3M in net asset reserves, while the CFP Board operates its core on almost $15M of revenue and a total of nearly $30M including the dollars it allocates to its public awareness campaign, plus a $23M war chest of reserves. And the CFP Board’s new fundraising efforts for the Center for Financial Planning only gives it even more of a financial and resources lead to outpace the FPA in its own initiatives.

In other words, the CFP Board has far more resources to deploy towards the success of its ever-converging collision course with the FPA, as the CFP Board increasingly expands its role from being “just” the credentialing organization for CFP certificants, to becoming the central organization for the financial planning profession. This collision course is perhaps most directly shifted by the shift in its vision, as while the CFP Board has remained focused on the CFP marks, the vision of its the new Center for Financial Planning is remarkably close to the FPA’s own:

CFP Board of Standards Vision:

The mission of Certified Financial Planner Board of Standards, Inc. (CFP Board) is to benefit the public by granting the CFP certification and upholding it as the recognized standard of excellence for competent and ethical personal financial planning.

Center for Financial Planning Vision:

To be the premier resource in the financial planning profession for educators, researchers, practitioners, financial services firms and the public.

Financial Planning Association Vision:

The Financial Planning Association is the principal professional organization for CERTIFIED FINANCIAL PLANNER™ (CFP®) professionals, educators, financial services providers and students who seek advancement in a growing, dynamic profession.

Is The CFP Board Seeding A Future Competing Membership Association?

Perhaps most notable of all, though, is the CFP Board’s massive fundraising effort for the Center for Financial Planning, including the initial multi-million-dollar commitment from TD Ameritrade over the next five years, and the CFP Board’s goal to raise upwards of $10M in total funding over the next five years… for a Center that doesn’t even yet have any dedicated staff or clarity about its initiatives.

In other words, with little or no staff, and a mission that isn’t necessarily all that resource intensive (at least in its current form), why exactly is the CFP Board being so aggressive in raising substantial capital for the Center for Financial Planning? Is it possible that the CFP Board has a grander vision for the Center for Financial Planning… perhaps to expand into so many of the FPA’s membership association functions that eventually the CFP Board spins off the Center for Financial Planning into its own membership association?

Of course, the caveat to the CFP Board’s aspirations of membership is that the organization is ultimately a 501(c)(3) charity, and not a 501(c)(6) membership association, which limits its ability to directly deploy its assets and income to become a membership group. However, as also noted last year:

“While it’s not clear whether the organization could legally use its some of its own $23M war chest of net assets on its balance sheet to fund a new membership organization spin-off, it might use its relationships to leverage sponsors that could “seed” a new replacement membership organization, and then establish a tight integration between the CFP Board and the new association to rapidly accelerate its growth.”

In other words, raising $10M+ for the Center for Financial Planning doesn’t make very much sense when it has no staff and few clear programs and initiatives that would necessitate such funding. But it makes a lot of sense to seed the Center for Financial Planning with the kind of multi-million-dollar capital it would take to launch a competing membership association.

To put it in context, FPA’s own institutional sponsorship revenue across all sponsors is barely $1,000,000 per year according to its last audited financials, and the CFP Board may have just raised that much from TD Ameritrade alone. And the FPA’s total net assets are barely $3M, while the CFP Board’s Center is aiming to have triple that amount of seed capital within the next five years. The CFP Board is even soliciting ongoing individual donations, in what may easily be a precursor to ongoing membership dues?

Is An FPA And CFP Board Merger Inevitable?

Notably, while the CFP Board continues to entrench itself into what historically has been the FPA’s roles and responsibilities as a membership association, it’s unlikely that the CFP Board wants to see the FPA outright fail. The FPA’s chapter system in particular, and its growing capabilities to support a state advocacy effort, are a key asset in the ability of the CFP Board (directly or through the Financial Planning Coalition) to potentially support future standalone regulation for financial planning.

Nonetheless, as the FPA’s market share of CFP certificants continues to dwindle – and its average member age continues to grow older, even as the CFP Board’s average age is now turning younger – the FPA’s waning power, and its increasingly precarious financial position, may force the issue in the next recession. As is, the FPA’s revenue according to its last public financials remains down 36% from its peak in 2008, even as the CFP Board has grown significantly. Which means the CFP Board may simply need to continue to encroach into the FPA’s territory, and compete for its sponsor revenues by growing the Center for Financial Planning, and wait for a recession to create an organizational crisis that compels the FPA to merge for survival; as illustrated last year when the discussion of an FPA-CFP Board merger arose, CFP Board CEO Kevin Keller simply said "there are no current discussions about a merger between CFP board and FPA" (emphasis mine), distinctly leaving the door open to the possibility in the future.

Alternatively, if recession-driven financial woes don't drive the FPA to seek out a merger, the organization may also soon face a crisis driven by the Department of Labor’s fiduciary proposal. Ironically, while the FPA has advocated for the legislation through its Financial Planning Coalition efforts, if enacted the rule threatens to be highly disruptive to not only FPA members who are advisors at potentially impacted broker-dealers, but more significantly to FPA's sponsors that include broker-dealers themselves and the insurance and investment products that are distributed through broker-dealers. In other words, if the DoL fiduciary rule ends out significantly curtailing commissions, it could both impact FPA membership as some commission-based advisors leave the industry, and adversely impact FPA’s sponsorship revenue at conferences as those commission-based-product distribution companies would have little reason to exhibit at FPA conferences in a future with little or no advisor commissions. While these aren’t reasons for the FPA to back down from its profession-advancing fiduciary efforts, it’s not entirely clear that FPA has sufficiently diversified its sponsorship base enough to handle the coming industry disruption its lobbying efforts have helped to bring about.

Fortunately, though, the decline of the FPA doesn’t have to be a foregone conclusion. The CFP Board’s long history of mis-steps, both in recent years (e.g., the recent issues with definitions for compensation disclosure) and extending back for decades (e.g., the “CFP” debacle of the late 1990s), has long validated the FPA’s role in advocating on behalf of CFP professionals to push back on the CFP Board when it does something questionable. In fact, the FPA’s best path to survival at this point may be to explicitly capitalize on the collective nervousness of the CFP certificant community about what happens when the CFP Board goes “unchecked” for too long. And the FPA still has a small time window remaining to get its financial house in order, preparing for the necessary sponsorship restructuring that may be necessary in a post-DoL-fiduciary world. Though its biggest issue, by far, is simply figuring out how to turn around its 15-year decline in the market share of CFP certificants, as if there are “too many” CFP certificants without any membership association to serve them, it really does become inevitable that the CFP Board will fill the void.

Ultimately, it’s likely no coincidence that the CFP Board announced its Center for Financial Planning this week, just as the FPA’s own Board of Directors convenes its fall meeting, followed this weekend by its Chapter Leadership Conference. The announcement provides an opportunity for the CFP Board to gauge how much pushback there is to its new initiative, with enough ambiguity about its future initiatives to deny its competitive effort, before it decides how aggressively to roll out future FPA-competing programs from the Center for Financial Planning in the coming years. Which means the FPA has an immediate opportunity to aggressively defend its own turf, both to the CFP Board and more importantly to its own stakeholder community, and justify to the 73,000+ CFP professionals why they should continue to pay for both the CFP marks and a separate membership association to represent them. Otherwise, it may only be a matter of time before the CFP Board, and its Center for Financial Planning, fulfill both roles on behalf of the financial planning profession.

So what do you think? Is the CFP Board's new "Center for Financial Planning" just a research initiative, or do you think the $10M+ fundraising effort signals an intention for more? Should the FPA acquiesce to the initiative? If not, what should it do in response?