Executive Summary

While crafting a “financial plan” for clients has been a staple of financial planning for decades, virtually no financial plan today actually constitutes a real “plan” for anything. After all, the whole point of planning is to formulate the strategy of how to handle a range of possible future scenarios. If A happens, then we’ll do B. If C happens, we’ll do D instead.

Yet financial plans today, and the financial planning software that supports the process, is incapable of illustrating such scenarios and the appropriate responses! Answering a simple planning question like “how much do the markets have to decline before I need to cut spending in retirement, and how much would I need to adjust my spending to get back on track” cannot be easily answered with any financial planning software available today!

Ultimately, as financial planners, we cannot eliminate the uncertainty of what the future may unfold, but we can eliminate the uncertainty of what to do and how to respond to those possible future scenarios. And by crafting a real plan about how to deal with that future, we can make it far less stressful as well, and eliminate the danger of needing to make a potentially regrettable high-stakes decision in the worst possible (and highly emotional) moment!

But ironically, in the end the very software that we rely upon to do financial planning and help clients navigate their uncertain future may actually be the greatest inhibitor to truly formulating a real financial plan for clients to deal with it!

What Does It Really Mean To Formulate A “Plan”?

The dictionary defines a plan as “a detailed proposal of doing or achieving something”, and the verb of plan(ing) as deciding upon or arranging in advance.

In the military context, battle plans are recognized as essential. And this is true despite the famous saying that “no battle plan ever survives contact with the enemy” because the process of engaging the plan, progressing towards the goals, and seeing what happens once the enemy is engaged, will itself change and alter what the next step should be. Notwithstanding this challenge, the military engages in planning because it’s only by trying to consider what the plan should be, and how it might be impacted by future events, that contingency plans can be created to know how to handle “unexpected” problems that arise.

The process of forming contingency plans across a wide range of potential futures is the exercise of scenario planning, where the military practices various scenarios and watches to see how they unfold, to gain a better understanding of how a real-world future situation might evolve and how it would best be handled. In fact, ironically the military’s training scenarios are often done in a manner that is so “life-like” (to ensure good learning opportunities) it sometimes scares civilians who don’t realize it’s just practice; thus, last year the military’s disaster training scenario included how to plan for a zombie apocalypse! And even though that particular scenario is rather unlikely to occur, it still provides an opportunity for learning from scenarios where it’s necessary to contain a widespread threat, secure critical infrastructure, provide medical services, and secure the safety of the general population.

What Is An Actual Financial Plan?

In the context of financial planning, drafting a “battle plan” for the future should similarly involve formulating contingency plans about how to handle a range of possible future scenarios. The key distinction is not just about looking at different scenarios, but about crafting plans about how to respond to them (particularly the problematic ones).

For instance, traditional financial planning once modeled the future by simply projecting how the plan would fare given average returns. Of course, the caveat is that while the future might involve getting average returns (or a sequence of returns close enough to approximate that result), there are other future scenarios that might involve lower returns (or a worse sequence of returns) as well.

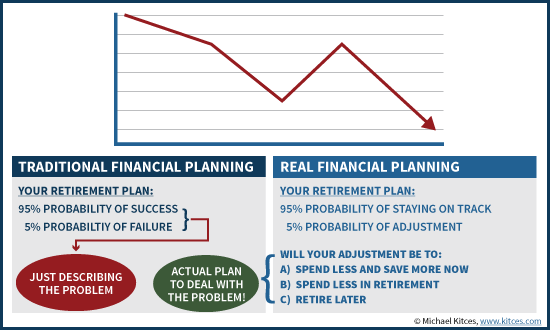

Accordingly, financial planners shifted to using Monte Carlo, so that we can quantify how often the future scenarios are likely to turn out to be problematic. We might run 10,000 future scenarios, find that 9,500 of them succeed and 500 of them fall short, and quantify the results as a “95% probability of success” in achieving the goal.

Yet as previously discussed on this blog, rarely does anyone in “the other 5%” of scenarios actually just keep on spending under the original plan until one day he/she wakes up broke and all the checks are bouncing. Instead, at some point, an adjustment occurs to get back on track. Of course, the later the adjustment occurs, the more significant it may have to be in order to get back on track. But ultimately, most probabilities of “failure” are really just probabilities of needing to make an adjustment to get back on track.

In fact, one might say that anticipating those adjustments – how much of an adjustment, and under what conditions it should occur – is the whole point of doing a plan in the first place. After all, the point of planning is not really about figuring out what to do if nothing bad happens. It is about figuring out what to do if something bad does happen, and how to respond and stay on track.

Thus for instance, if the financial planning projection shows that a 20% market decline would necessitate an “adjustment” of some sort, the whole purpose of planning is to figure out, in advance, what that adjustment will be. In other words, it's not just about recognizing that there's a 10% (or whatever) probability of adjustment, but also what the magnitude of the adjustment would be, based on the magnitude of the event that triggered it in the first place. If an adjustment becomes necessary, is the plan to spend less and save more now, to make up for the market losses in time for retirement? Or to keep saving as is, but try to stay on track for retirement by planning to spend less in retirement? Or is the plan to keep saving as is now and spending as planned in retirement, but simply retire later to ensure the money doesn’t run out?

In fact, an ideal plan might even go one step further, and formulate the tactics of how to handle each of these potential planning scenarios. If a market decline would necessitate an adjustment, and the plan is to cut spending to save more and make it up, what spending will be cut? The restaurant and entertainment budget? Travel? Something else? If the plan is to cut spending in retirement instead, then which spending cuts will be enacted? A smaller retirement home? A smaller travel budget? And if the plan is to retire later, how many years later would the client need to work after a 20% market decline, in order to get back on track?

Using Financial Planning Software To Formulate An Actual Plan For An Uncertain Financial Future

If the fundamental goal of financial planning is to come up with tactics to handle (i.e., to formulate a plan for) future contingencies, it is notable that today’s popular financial planning software solutions are not actually capable of facilitating and illustrating such scenario planning!

While some tools at least allow for an initial stage of collaborative planning, where a client might be able to see how the plan would be impacted if there was a market decline or another adverse event, the software tools all lack the ability to model what an effective response would be. In other words, to formulate a real plan with a client, software should be able to illustrate an adverse event, and the appropriate steps to respond, to formulate a plan that can be expected to work and get the client back on track!

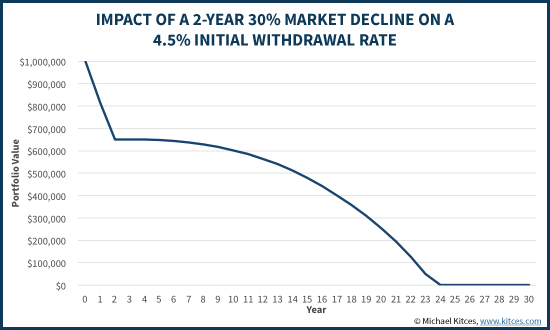

For instance, imagine that a prospective retiree has a $1,000,000 portfolio and plans to withdraw $45,000/year (adjusted for inflation) over a 30 year time horizon from a balanced portfolio invested for a 7% return. The financial planning software might show that this strategy has a 5% probability of failure, given that a significant (e.g., 30%) market decline in the first few years which doesn't recover quickly could severely damage the longevity of the portfolio.

In this case, simply showing the potential retiree that the plan "could" fail, if the adverse market event does occur, is simply describing the problem. It's not actually formulating a plan to resolve the issue.

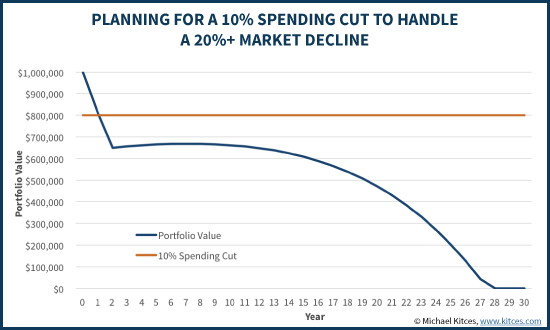

An actual plan might be an intention to cut spending if the portfolio declines severely. Thus, the ideal planning software might illustrate for the potential retiree what happens if the plan is to start with an initial withdrawal rate of 4.5% (which is $45,000 of inflation-adjusted income on a $1,000,000 portfolio), but to cut spending by 10% if the portfolio drops at least 20%. Now the retiree actually has a plan about how to handle the market decline.

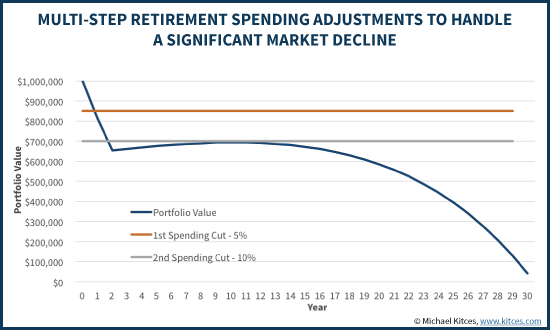

Unfortunately, as shown above, the planning software would reveal that a 10% cut isn't enough of an adjustment if the portfolio declines as much as 30% in the first two years. A deeper cut is needed. However, the retiree might not want to implement a drastic cut immediately, since 1-year portfolio declines often recover, rather than declining again for a second year. So the plan is altered to create a two-stage spending adjustment - spending will be cut by 5% if the portfolio declines by 15%, and then will be cut by another 10% if (and only if) the portfolio falls yet another 15% (for a 30% total decline in value).

Fortunately, this approach actually works, and the software illustrates that the retiree's new plan - to engage in certain spending cuts as appropriate/necessary based on what happens in the market - will work. Of course, in the overwhelming majority of scenarios, the markets will perform better, and these spending cuts will never be necessary. But that's the whole point of having a plan in the first place - to know what to do if the adverse event happens, along with having a strategy (for even better spending) if the markets "cooperate" (with favorable returns) instead!

From the perspective of financial planning software, the key distinction here is that good planning software can – or at least, should – help facilitate the discussion about what kinds of tactics will be necessary to get back on track after an adverse event, so the client can plan accordingly. Planning software should be able to illustrate not just the decline, but how a 10% spending cut after a 20% decline isn’t enough, but a 5% cut followed by an additional 10% cut is sufficient. And again, the point of the exercise is to determine what actually “works” – whatever spending adjustments are necessary based on certain market declines or target portfolio levels – to formulate the actual plan, which in turn can then be enshrined into a withdrawal policy statement to document the actual “plan” for the future.

And notably, formulating plans doesn’t have to be exclusive to retirement withdrawals and liquidations. The same is true when planning for accumulators trying to decide when to retire, those who are planning around job and career changes, or simply planning for the contingencies of adverse health events that could impact the ability to earn and the cost of medical bills. Not because the goal is to sell insurance – although that might be the outcome – but simply to illustrate the risks, and formulate whatever the plan would have to be to get back on track.

In fact, arguably all financial planning should begin by looking at scenarios and making adjustments, because in reality most people don’t even know how to set long-term financial planning goals in the first place, until they actually see what the possible scenarios are!

Formulating A Real Plan To Achieve Goals Requires Real Plan Monitoring

Because a real plan involves not only setting goals, but also formulating a plan about how to respond to the inevitable speedbumps along the way, in the end financial planning software should not only help in the formulation of a plan, but then also help clients track their progress on an ongoing basis!

In other words, financial planning software should not just give clients access to run their own long-term projections, but specifically monitor whether they’re approaching the agreed-upon thresholds that would trigger an adjustment in the plan in the first place! Otherwise, financial planning software is just the equivalent of training a pilot in a flight simulator without including any way to control the plane; if the pilot can’t control the plane and monitor its path, the simulator will do little more than illustrate the plane crashing, rather than the more relevant opportunity to practice steering out of the disaster!

For instance, if the real retirement plan calls for a 10% spending cut if the portfolio is down 15%, and another 10% spending cut if the portfolio falls 30%, the planning software should help clients easily see whether they are close to needing to engage “the plan” and make the spending adjustment. If that’s the plan, a client with a $1,000,000 portfolio shouldn’t need to wonder whether recent market volatility is a problem or not; instead, the client knows that if the account balance hits $850,000 there will be a spending cut, at $700,000 there will be another spending cut, and can even have a plan for what those cuts would be. At that point, the software simply reports whether the client is or is not close to those points where the cuts must occur.

Reducing The Fear Of Uncertainty With Real Financial Planning

Ultimately, the key point of all this planning is to reduce the natural fear that clients have about their uncertain future. While it’s not possible to actually know the future, and which contingency plans will have to be enacted, there’s a difference between uncertainty about the future, and uncertainty about what to do in the future. Financial planning can’t resolve the former, but it can do a lot to eliminate the latter.

In fact, from my own personal experience, I find that one of the greatest contributors to client anxiety in the face of market volatility is that most are struggling to figure out “does this market volatility really matter” and will it impact goals? As advisors, we are trained to always tell clients to “stay the course” and stay invested and ride out the volatility… which both fails to fully acknowledge client fears, and more substantively fails to clarify for clients the difference between “temporary” volatility and a genuine impairment of their plan.

In other words, “everyone” knows that at some point, a market decline is so severe that stay-the-course platitudes aren’t enough, and it will require adjustments to get back on track. What clients don’t know is the point at which those adjustments will be necessary, and how much of an adjustment will be necessary – in part because financial planning software gives us no tools to formulate and illustrate such a plan. Instead, the ‘point of no return’ threshold for the client is unknown. And that uncertainty is often exacerbated by the fact that clients tend to overestimate the significance of short-term volatility, and misjudge how little of an adjustment is usually necessary (if any!) to stay on track.

Thus, formulating the plan can reduce anxiety by reducing the uncertainty. Now clients know exactly what they will do in any of the possible scenarios – if the market falls by X%, cut spending by Y% - and it’s only a question of when and whether to execute the next step of the plan, with no longer any uncertainty about what needs to be done. And in the process, clients will be able to make real-time decisions about how to respond to market volatility with a plan formulated during times of rational calm, rather than trying to formulate the response itself in the midst of emotionally turbulent times!

The bottom line, though, is simply this: real financial planning is not just about projecting the future and what does or does not work, but is also about formulating plans on how to handle various future scenarios and the adjustments that would need to be made to get back on track. It is time for financial planning software to facilitate real planning by actually giving advisors and clients the tools necessary to formulate such plans… along with the ability to monitor how clients are progressing towards their goals, and whether they are close to reaching trigger points that require an adjustment to stay on track!

I would say no. I’ve always had to cobble together a plan to get it to say what I wanted the way I wanted. I think that speaks to the complexity and judgement that goes into what we do… and to the job security we’ll enjoy.

Excellent, thanks Michael. In addition to adverse portfolio sequence risk, one could just as easily substitute and insert a long term care event for a spouse at a variety of ages, and test portfolio failure, and plot remedial action.

The difficulty of course are all the variables one must include when considering such an adverse retirement event, such as: What age of onset? 66? 70? 75? 85?

Duration? Six months? Six years? 12 years?

One spouse, or both?

Anticipated inflated care costs? 5% 3% 8%?

Two of my affluent clients have seen their wives suffer massive strokes at their ages 65 and 73. Their care costs have been staggering-due to level of care required, one left his career due to his wives stroke, and the other needed to sell their beautiful home to move closer to the optimal care facility some 75 miles away.

Their spouses have already required five years of care, and could easily require another 5-10 years more.

Call it adverse sequence of care risk.

Now, just imagine piling on adverse sequence of return risk, to their very real care reality/risk?

You’re staring at a retirement Financial Hurricane.

Great points, WiseOwl. If you don’t mind my asking, was there any reason to suspect that those two women were at an elevated risk of stroke? Or were those strokes just out of the blue? In any case, I wish them and their spouses the best.

Hello Pat, yes, one spouse did have some health history which was cardiovascular in nature, the other? None. Had they applied for a long term care policy five years earlier, both would likely have been approved for coverage. I frame the ownership of a long term care policy as financial body armor, and that when you pay the annual premium for a robust LTCi policy, in essence, your premium becomes your “cost of care”, known and quantifiable. And, LTCi policy premiums can be paid for via income tax free 1035 exchanges and distributions out of life policies and variable annuity contracts. Thus, after cost basis is consumed in the life policy, we are able to redeem taxable gains and convert them into tax free distributions-again, to pay the LTCi policy premium.

A LTCi policy is also a highly efficient asset, freeing up other retirement assets to enjoy, because they need not be allocated into disuse to pay possible unknown future LTC expenses-which cannot be predicted until they occur.

Hybrid life/LTC combo’s also can help, although benefits tend not to be as robust, or, require heavy annual premiums spread over a ten year time period.

And thanks for your kind words. The men are hanging in there, although they would share with you that their personal quality of life and living, has suffered and been greatly reduced.

Thanks for the reply, WiseOwl. I’m sure the couples involved appreciate having a wise advisor.

Michael, This kind of article is so valuable and it shows the hangover that Wall Street exerts on our industry. A ‘plan’ is defined as anything that looks appreciably more like a plan than what we have come to expect over the last few decades based on what American Express or Wells Fargo conjured up. The only thing I’m not clear of from this article is whether software can conquer the scenario challenge.. Brooke

Brooke,

Frankly, most “plans” are really just built to illustrate the need for a financial services product that “solves” the problem illustrated by the plan. But that’s a discussion and article for later this month. Stay tuned. 🙂

– Michael

Mike I completely agree! “Most financial plans are built to show the need for products” Bravo!

This is precisely the problem, our industry is designed around delivering a product as a solution to clients problems, when in fact there are difficult planning needs that never get adressed.

This is a great question! To me, it raises several statements or questions worthy of examination:

I. Most such software is designed for financial forecasting, or at best financial modeling. It does nothing to identify goals or rank & weight them. Nor does the use of such software make one a “financial planner” [which need some definition also].

II. The CFP Board’s 6-step process [“Let’s make a plan”] may not do much better, unless Steps 3 and 4 are done “better” than a robo-advisor, in generating alternative scenarios, decision trees, and outcomes that vary in their responsiveness to current and expected economic conditions, and resilience in producing positive forecasted outcomes.

III. It seems the essence of financial planning is providing decision-making guidance along the pathways of life. Yet virtually all business models in our field dilute this benefit by focusing on “just investing” and its reductionist-driven efficiencies in generating profits. So, it’s not just the software – it’s the software we all asked for.

IV. Another question then arises: who decides what is a good plan? Not the consumer – see behavioral finance generally. Are we being served optimally by a self-regulatory organization deciding what is a good-and-proper financial plan [see CFP Board’s new Center for Financial Planning]?

May the discussion ensue . . .

Michael,

I have been saying for years that financial planning software can not actually generate a meaningful financial plan. This goes back to the 70’s when Stanford Research Institute (SRI) established what configuration of financial services constitutes a financial plan. The premise being trying to make financial planning commercially viable. As recently as the early 80’s, there was the question of whether client’s would pay for a financial plan. Of course things have evolved. The original SRI premise was largely focused on commissionable product revenues. Non-commissionable services like budgeting were not considered being part of a financial plan as establishing the economic viability of planning was the objective.

Technically, professional standing in advisory services entails fiduciary duty which is different from financial planning as there is no statutory requirement for education funding, etc.. Planning is a needs based selling discipline used to persuade consumers to abstain from consumption and fund very specific objectives literally planned for. A financial plan (1) must incorporate fiduciary duty (presently not possible in a brokerage format) and (2) address each consumer’s objectives, which is not easy given most consumers have not put away the financial resources to fully fund all their hopes and aspirations. Thus, perhaps the most pertinent advisory services lesson here is to choose your clients well, have them (1) simply save, (2) abstain from consumption and (3) keep their goals and objectives accordingly within reason. This is what makes institutional business so much fun and attractive.

Financial planning software, is trying to treat advisory services like physics where there are immutable laws of science and mathematical precision inconsistent with the lives of investors dealing with the unpredictable circumstances and highly volatile financial markets.

SCW

Stephen Winks

The financial plan, regardless of the underlying resource, isn’t “the answer”. It is only the product of examining goals and resources available and crafting an approach to achieve the goals. Will it be the “right” answer? I tell my clients that one thing is sure; I did not get it right. None of us can forecast the future with accuracy. We all must make assumptions. The catastrophic events some have noted will happen. We cannot predict them, but should be able to at least identify them as a possibility and recommend risk reduction approaches.

Let me comment on the military analogy. I think it was Eisenhower that postulated “the plan is worth nothing; planning is invaluable”. Every military plan looks at things the enemy can do along the course of events and how we might respond. We don’t just run exercises like the zombie example. For every operation plan there is a series of responses if the enemy does this or that. Both you and Jonathan Guyton have done the same. If the market does this and inflation does that then the client will have to do thus and so. I believe that to be a realistic approach. There isn’t any software that is going to belch out “the solution”. That’s why clients pay us. We are supposed to use our brains, experience, knowledge, etc. and advise them. I tell my clients here is a base projection. It is pretty conservative and might work out, although never as I projected. Every year (at least) we’ll meet to see if we are on track. We’ll adjust as needed. There is flexibility in the spending plan. If they won’t accept that I really don’t want them as a client. It makes no sense. And it isn’t any fun for me. BTW, I’ve never had anyone insist on a 100% success rate. I guess the 23 years I’ve been practicing isn’t long enough.

John,

Thanks for the comment, but you’re making my point here.

I’m not lamenting the lack of “an answer” in today’s planning software. I’m lamenting the fact that the exact “if this then that, if something else then this other thing” that is the core of PLANNING (of all types, from financial to military) is MISSING from planning software today.

If a client came in and said “So if the market drops 20% starting 2 years from now, will I need to cut my spending by 5%, 10%, or 15% to stay on track, given my financial goals and situation” no financial planning software today can effectively model that “if this then that” scenario to answer what the “then that” should be. That’s a serious shortfall for actual PLANNING! :/

– Michael

Understood. I recall your presentation about the future of our profession and how we should be able to easily do those “what ifs” on line with a client. Certainly a valid objective.

I’m shocked the financial planning software doesn’t have those capabilities. From what you say Michael, the software seems more geared to getting assets under management than actual planning.

I’m in Ireland but I use the UK software, Prestwood Truth. The software provides a number of different solutions to shortfalls in cashflow, including earning more, investing more and taking more risk. It also has a capacity for loss tool to simulate what the scenario would be if there was a crash and what is needed to recover. Another handy tool for the more frugal clients, is showing them how much more they can spend without running out of cash. There are also default scenarios to show the financial situation is one of a couple died or became disabled.

I always thought these things were standard in financial planning software?

Well said Steven! Sometimes it seems us on the other side of the pond are streaks ahead! So much discussion appears to be about ‘the Industry’ and doing what appear to be ‘once only plans’ (to get the assets under management, because that’s all that matters!!!) rather than an ongoing service with constant adjustment considering numerous scenarios (but without geeking out and boring clients to tears!) and with alll planning done on prudent assumptions. I always say that Financial Planning is like getting fit. You can’t go to the gym once and be fit for life!

If anyone is looking for software to provide ‘the perfect answer’ they are diluted! It’s more about engaging clients in meaningful relationships and conversations about the possibilities (good and bad) and keeping these under constant review in return for the fees. That’s where you earn your money NOT through messing with the money. Prestwood Truth has a 30 year Cashflow modelling pedigree, and having used it with clients through countless ups and downs it simply works – if the planned has the right mindset and prudence is the driver.

Steven,

Most of what you’re discussing here is available in US financial planning software as well. The problem is that it still doesn’t quite hit the mark.

Yes, I can run a projection of what happens if there is an immediate market crash, or how their retirement projects at different spending levels.

The issue here is more dynamic. What I’m talking about is “Show me a Monte Carlo analysis of 1,000 scenarios, where in ANY scenario, IF the market ever declines by 20% – whether next year or in 5 years or in 10 years – dynamically cut the client’s spending, THEN, by X%, and see what the effect is.”

I have yet to see any financial planning software that projects client spending DYNAMICALLY, where spending is assumed up front to move up/down based on future unknown market volatility. Even though that’s exactly what a real “plan” would/should specify!

– Michael

Michael, please take a look at pralana retirement calculator. They just released an updated version that does monte carlo and historical analysis against different withdrawal strategies and for consumption smoothing. It’s probably not entirely what you are looking for, but this is best (retail) software for planning that I have found. I have no financial interest with the company, just a satisfied user. http://www.pralanaretirementcalculator.com/html/introducing_prc2016.html

Mike what a great article! I have been a CFP since 2004 and I have always felt that building financial plans is so important but also such a waste of time all in one. You articulated how I have been feeling all of these years much better than I ever could.

Some of my best financial planning has come just sitting around and discussing planning topics without ever using software or running a projection, go figure!

I agree WiseOwl, LTC events are very hard to model, let alone plan for adjustments. In many case, I’ve modified the plan 25 different times based on two different variables, and provided the client with a 5 by 5 grid of outcomes. At least this helps identify what the tipping points are and what possible reactions can be considered.

On a separate note, we have found the Monte Carlo outcomes of Money Guide Pro to be somewhat suspect. In our experience, the probability of success actually goes down when taxes on gains are deferred (which is what actually happens for most clients), rather than paid in real time (as the defaults in MGP assume) . This is a confusing result to us….not sure if others struggle with the same issues.

Michael, thanks so much for writing about this. I’ve been asking this question for a long time. I find it both inexplicable and disappointing that no one has come up with software that models, for example, the various dynamic spending rules that Guyton, Wade Pfau and others has researched. Even inStream, which incorporates some decision-rule options in its Safe Savings Rate plans (for younger clients in the accumulation phase), doesn’t do that for its goal-based plans for retirees and pre-retirees. You know these researchers and have worked with some of them; what’s your guess as to why none of them has taken their work to the next step, a la Kotlikoff with Social Security?

What I would like to see is planning software that allows the advisor to test a number of different built-in scenarios, perhaps with the ability to adjust parameters within those scenarios, and then present various options to the client. Your example of a 10% spending cut if the portfolio is down 15%, and another 10% spending cut if the portfolio falls 30%, is but one of a myriad of alternative strategies one could employ for one client! It would be extremely helpful, for the advisor and for the client, to see what strategies work best with a given set of parameters.

Michael- thanks for a thought provoking article. This has me thinking about the topic of insurance rather than retirement distribution. As you know, premiums are decided to insure against a probability and magnitude of an event. We seem more comfortable as an industry to agree that market risk needs to be taken to ensure we achieve a risk premium in return (over the long term) to help us retire. The problem with insurance is that it is an expense that prohibits us from saving more. In a perfect world, everybody would have enough to both save and spend on premium to insure against all risk. The reality is that dollars are limited and there needs to be some sort of capital budgeting framework to help a client understand opportunity cost (if I spend more on insurance to mitigate one type of risk => I have less money to save for retirement => I need to take more market risk to reach a goal). When we trade one risk for another, is there a larger framework to make a decision (such as economic utility theory)? We understand we need to take risk in life but how do we prioritize which ones to take?

Fantastic topic! Thanks!

Software – in this case for financial planning – is nothing more than a tool.

A tool in the right hands can be used to do wonderful things. In the wrong hands . . . well, we know how that can end up.

Nowhere is the spectrum of potential results from a tool wider than in financial planning software.

However, I believe the financial planning software I use along with a disciplined planning process offers what you say doesn’t exist today . . .

For example, armed with Financeware and the Wealthcare process, I work with clients to first determine not just a singular set of goals, but “ideal” and “acceptable” versions of each goal that is important to them. This can include dollar amounts, time frames, investment risk, savings levels, etc.

For instance, I often ask new clients if they would save less if we demonstrate they can afford to. Or would they take less investment risk, even if they’re comfortable taking more.

Now, instead of working with a singular set of goals, each client has a discussed and documented range of goals.

This range of goals combined with a prioritized “goals exchange” leads to a thorough discussion with clients – before the first proposal, plan or decision has been made – about which goals are more important to them than others and which goals they would be willing to “exchange” for other goals.

As an example, a client may want to spend more money in retirement, but they’re not willing to work a minute past age 58 (their acceptable retirement age) to make that happen.

The real magic happens when instead of considering the interplay between just return and risk or retirement age and retirement spending, we now have a framework to identify and understand the trade-offs between each of the variables within a client’s control.

As the market does its thing and the client’s life unfolds, we utilize monte carlo analysis to keep their plan in our “comfort zone” of between 75% and 90% plan confidence.

If/when their plan falls below 75% (due to the market, unanticipated expenses or new/increased goals), we can move one or more of their lower priority goals closer to their acceptable values.

And if/when their plan rises above 90% confidence (due to the market, inheritance or goal adjustments) we can move one or more of their higher priority goals closer to their ideal values.

Does this process work automatically in the software? No.

But software + a process focused on making the most of a client’s one and only life can actually can deliver much, if not all, of what you say doesn’t exist today.

Or at least I believe my approach does.

Very nice post. I’ve been thinking about that for a long time. Thanks a bunch.

As i would like to share with you our formulation software for cosmetics and personal care businesses, it’s name is Cosmetri. We provide an affordable, secure web-based software application for empowering cosmetics businesses.

http://www.cosmetri.com/

Thanks for writing this! Its really a helpful blog for all. Visit my blog for other solutions too:

I struggled with these issues for years until I read “Unveiling the Retirement Myth” by Jim Otar. Then I began using his software: Otar Retirement Calculator @ http://www.retirementoptimizer.com/

It’s given me so much more confidence in guiding my clients. I highly recommend it…

Great points, Michael and great timing!

The ability to illustrate potential problems and how to handle them is actually just one of the many questions that our AI at http://www.Perfiqt.com can easily answer. Have a look here: https://twitter.com/perfiqt/status/810198845619576832

Would love to hear your opinion on what we have at some point and thank you for the great posts (they actually contributed to our product)!

Great article! Hits on a major problem with software designed around product sales.

Such an interesting topic for sure. As I see it, the consensus of all comments so far is basically a frustration with measuring the future based on stock market returns. I believe this insufficient view of financial planning integration with stock market returns is comparable to the thought that the earth is flat.

Fact is that there are no investments that can be accurately assessed for future performance never the less the “stock market”.

I believe that we all know that the ultra-wealth clients attained the wealth by inheritance, owned a business, gambled and got lucky as well as any other ways other than stock market investing. Very HNW clients treat stock market investing as an afterthought. Here, we find financial advisers pitching AUM strategies ad Nauseam.

The wealthiest clients I have had the luck to know (over 40 years) mastered diversification in many different assets and certainly could not care less whether the stock market was up, down or sideways. They instead, have or had advisers that advocated VALUE buying of artwork, various collections such as oriental carpets, Tiffany lamps, antiques, multiple businesses if they were inclined and enjoyed the risk nuance of that arena. So many other ways as well such as various forms of real estate etc, as well as some occasional stock market investments. None of these people started wealthy.

The point is that why just focus on software and Monte Carlo simulations based on stock market scenarios?

Might it make sense to advocate wealth building to the mass audience that most financial advisers work with in the first place?

For instance, buy a small antique piece of furniture, invest in the house next door an rent it out, buy a small high-grade carpet, invest in a collectors version of Tiffany glass. It really doesn’t matter what it is as long as the item invested in is for the long haul. Quarterly or even yearly projections and forecasts as per stock market returns ends up being a suckers game.

Sure there will be some investments that tank, while others appreciate. So, what. That is the nature of things. I believe all advisers would be best served to step up and learn about the world. It is not flat. It’s round. There are many things to invest in.Why worry about the “stock market” and the million ways to forecast it? Not sure that ever made any sense to anyone except the people that invented the software in the first place.

I have stated all of the above because of around 1978 or so I lived on the old Vanderbilt Whitney estate located on Long Island. I rented the upstairs of the old chauffeur’s cottage for $400/ month. I lived there for four years. The owner was Harry Glass, a significant collector of old master art, Tiffany lamps, antiques, etc. Harry explained everything to me that I have mentioned above. Harry certainly had his ups and downs. Harry bought the entire estate at the time (26 acres and homes on the property located in Old Westbury on a bid of $300,000. The property in Old Westbury at the time was worth a minimum of $200,000/acre without buildings.

Harry taught me much about investing, getting up off your back when things don’t go your way as well as many other concepts that my uncle Morris who was an accountant in a rural area of NJ. They were both value buyers; Both achieved significant wealth over many years.The most important lesson was that life has its ups and downs. You really can’t see what the future will bring. You can run all the proposals you like. In the end, all of that planning can go in the crapper overnight. Harry motivated my wife and myself to start small. It all worked.

Over the years I turned around numerous businesses, built two family offices to seven figures, lost much twice due to stupidity because I varied from the message above and once because of severe illness as my wife did. Somehow we have survived what is called life. When necessary, we sold some antiques and some other collectibles to pay for unplanned catastrophes. The point has we had it because we had followed the lessons above.

Along the way, when you operate in this manner you learn much about whatever you value buying. It comes over time. However its all worth it in the end. One of the most successful and well-managed businesses in the world who has based their entire model on value buying is none other than COSTCO. Notice that I did not say Sam’s Club. If you do not know the difference, then this is the starting point. Learn this model and follow the leaders.

All life experienced advisers are capable of bringing a ton of value to right clients. Life experience and speaking in life transition terms will go a long way. If you focus on stock market investors only, then you are nothing more than a “Vegas croupier.” I know, I attended UNLV.

Last words. The world is round, not a good idea to think in “Flat terms.”

The above article is a great and very useful , but I would like to draw a point .

You have not touched when market are up with 15 % then what we should do.

So that when portfolio drops it help to manage .