Executive Summary

In the early days of the financial advice industry, the nature of client relationships was primarily transactional, and any “financial planning” that happened was done purely from the perspective of determining a client’s needs so that the advisor could get paid for implementing a product with them to meet that need. That transactional relationship meant that advisors could work with anyone them meet – or at least anyone who had an interest and the financial wherewithal to buy their products – and since there wasn’t any value to meet with the client again until there was another opportunity to implement another product, an advisor would need potentially several hundred clients to be able to call back upon over time in order to make a living. However, as the advice industry has increasingly moved towards a recurring-revenue model (where advisors provide ongoing advice and generate ongoing fees), the number of clients that any advisor needs to serve has decreased dramatically, and the biggest limiter to an advisor’s practice is the number of ongoing clients they can support with a limited amount of time in the week, month, and year. Which means that it’s become increasingly important for advisors to focus on the operational efficiency of their financial planning practice.

In recent years, a growing number of financial advisors have begun to focus into niches and specializations as a way to differentiate themselves in an increasingly crowded advice marketplace. But those who have focused on a particular target clientele have also begun to note that it’s possible to run a more efficient (and more profitable) business by serving a client base that shares similar characteristics, as it means that an advisor can develop a deep and repeatable expertise to increase their capacity to serve more clients (and reduce the time it takes to provide financial planning to each).

Yet, in practice, actually committing to serve ‘just’ one certain type of client and ‘niche down’ is a major decision. As while it might seem ‘logical’, the idea of actively excluding prospective clients outside of their niche is downright daunting, to say the least, and up to this point, there’s been little hard evidence to support the time and efficiency value of having a niche. Until now.

By analyzing data from both the 2019 Kitces Research Study on Advisor Marketing and the 2020 Financial Planning Process Kitces Research Study, our analysis shows that there is indeed material efficiency value in focusing on a niche clientele to serve.

Specifically, our research analysis finds that top advisors with a niche (versus top advisors without a niche):

- Spend 150+ more hours every year on high-value, client-facing activities (or 28% more time with clients and prospects, while spending 13% less time doing middle-office and back-office tasks)

- Are able to deliver a more focused and customized financial planning process (as not every possible area of financial planning is applicable to every particular niche)

- Serve an average of 14% more clients (since advisors with niches can more easily scale their practices)

- Have clients with an average of both 25% more investable assets and higher net worth

- Are able to set their AUM fees 9% higher, and generate 20% higher standalone planning fees

- Earn an average of $660,000 (versus $395,000 for non-niche advisors at the same income percentile)

Ultimately, the key point is that there are indeed clear and measurable advantages (in both the short- and long-term) when opting to serve a niche clientele. Not only do advisors enjoy greater efficiencies withing their practices (by spending more time on the most value-added activities and less time on the least productive business tasks and stages of the financial planning process, and by offering a more concentrated, specialized planning approach), they charge more for their advice, serve more – and more affluent– clients (or, conversely, have the option to reduce their number of total clients by focusing in on their most profitable clientele), and end out seeing substantially better bottom-line results. And any business decision that allows a professional to serve their clients better, and to see better business results is, at the end of the day, a positive for advisors and their clients!

“To niche or not to niche” is a question that many advisors face. On the one hand, there are clear benefits of more specifically being able to articulate the value you deliver to the clients you work with and hone your efficiency in doing so. On the other hand, the idea of niching can be a bit unnerving, since a good niche strategy that communicates who your ideal clients are will also inherently tell a much larger number of individuals they are not a good fit for you. Of course, that’s the point of having a niche – it sets a clear message in the marketplace of not only who you serve, but who should be referred to you – but feeling as though you are limiting your potential options for business can be unsettling nonetheless.

Unfortunately, the industry has remarkably little data to speak to the value of niching. What we “know” primarily comes from anecdotal accounts and philosophies espoused by colleagues, advisor mentors and coaches, and various pundits in the industry.

However, thanks to the now over 2,000 financial planners who have participated in Kitces Research Studies over the past 3 years, we continue to be able to dive deeper into nuanced advisor business topics just like this. We recently wrapped up the analyses from our 2020 Kitces Research Study on the Financial Planning Process (available in the latest Kitces Report white paper for Members), and we are excited to begin sharing some insights based on our most recent research, which adds to a number of topics we have already examined in the past:

- How Much Does A (Comprehensive) Financial Plan Actually Cost?

- How Do Financial Advisors Actually Spend Their Time And The Limitations Of Productivity?

- Financial Planning Software Doesn’t Make Advisors Faster… It Makes Them Better

We are very grateful for the many advisors who have taken the time to help us examine the ‘art’ of financial planning scientifically!

By combining results from our 2019 Kitces Research Study on Advisor Marketing with our 2020 Financial Planning Process study, we are now also able to gain some unique insight into how advisors with niches engage in the financial planning process differently, including how niche advisors use their time, how they actually go about the financial planning process, and productivity efficiencies achieved by advisors using a niching strategy.

(Editor’s Note: Unless otherwise noted, this discussion looks only at the subset of advisors who answered both our Advisor Marketing and Financial Planning Process surveys, so some numbers reported may deviate slightly from numbers reported elsewhere.)

Do Financial Advisors With Niches Use Their Time Differently?

Our prior Kitces Research studies have taken a deep dive in how financial advisors use their time, and the factors that drive time use and productivity.

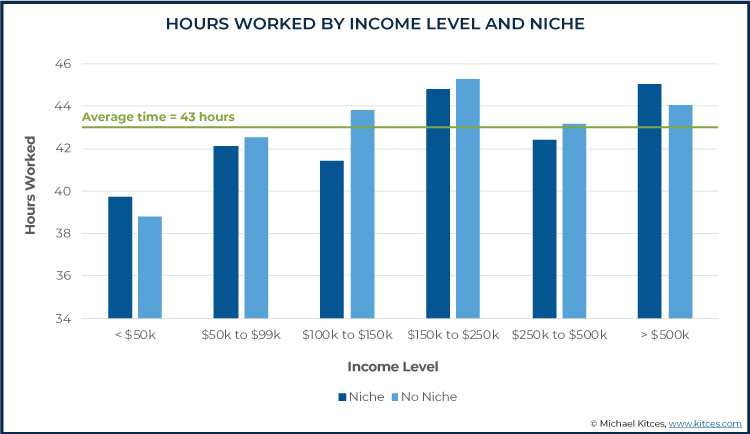

In our prior research, there has been a clear trend in advisors having longer work weeks as their income (and client base) grows. The trend isn’t surprising; when firms are first getting started, there just aren’t very many clients to service, and as the number of clients increases – and eventually, the number of staff to service those clients – the advisor’s workweek increases with the lift in both client management and staff management responsibilities.

Leveraging the data from our 2019 Advisor Marketing study, though, we can now segment advisor use of time by those with niches versus not. Generally speaking, we see some similar trends in work hours by income level (rising as the practice grows), and for the bulk of advisors with ‘mid-sized’ practices, the hours spent working in the practice are consistently lower for advisors with niches versus those without. It’s only practices still getting started (with less than $50k of income), and the largest firms (more likely to have greater staff to manage) that niche advisors are spending more time.

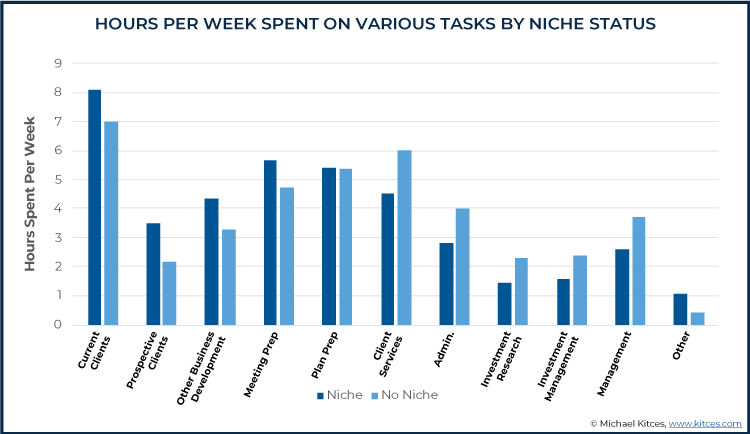

When we drill down further to look at advisor time use by categories, though, more significant differences begin to emerge between niche advisors and the rest. Looking at the individuals included in both our 2019 Advisor Marketing study and the 2020 Financial Planning Process study, we see some meaningful divergences in how advisors are using their time.

It is generally acknowledged that the most valuable work that an advisor does is the time they spend in front of their clients and prospective clients. As indicated in the graphic above, advisors with a niche reported spending roughly one hour more per week with current clients, another hour with prospective clients, and yet another hour in other business development activities. While this may sound small, spread across an entire year, it amounts to an additional 150+ hours working with current clients, prospective clients, and engaged in other business activity. And the time for 150 additional meetings with clients and prospects throughout the year amounts to a substantial increase in productivity and income potential. In fact, our Kitces Research has separately found that on average, the difference between the top 25% of lead advisors by income (earning a median of $400,000/year) and the rest (earning a median of $100,000/year) is that the former spend an extra 4 hours/week on client- and prospect-facing activities!

Likely due to the extra time spent meeting with clients and prospective clients, we see advisors with niches do spend about an extra hour per week in meeting prep as well. But, on average, niche advisors spend significantly less time in client service, administrative work, investment research and management, and other firm management-related work.

In other words, we see advisors with niches are able to do more high-value client-facing (i.e., front office) work less low-value (and more easily delegable) middle-office and back-office work. And while in the aggregate it amounts to slightly less overall time use, when it comes to the most productive “front-office” client- and prospect-facing activity, niching is associated with a 30% increase in front-office activity!

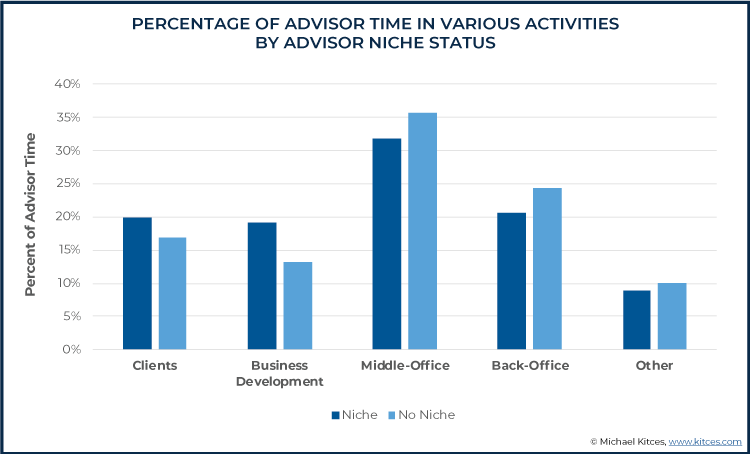

The graphic above makes these comparisons even clearer. In particular, we see niche advisors are spending a greater proportion of their time in front-office activities clients and in business development, and a smaller proportion of their time doing middle-office, back-office, and other work.

These trends are not surprising from the perspective that having a niche creates consistency in middle-office and back-office operations and a more repeatable expertise process that can lead to efficiencies, and those efficiencies increase potential time to be spent in crucial revenue-generating front-office activities with clients and prospective clients that are associated with significantly higher levels of advisor income over time!

Do Advisors With Niches Engage In The Financial Planning Process Differently?

Our survey results suggest that advisors with niches not only spend their time differently, but the engage in the financial planning process in a different manner as well.

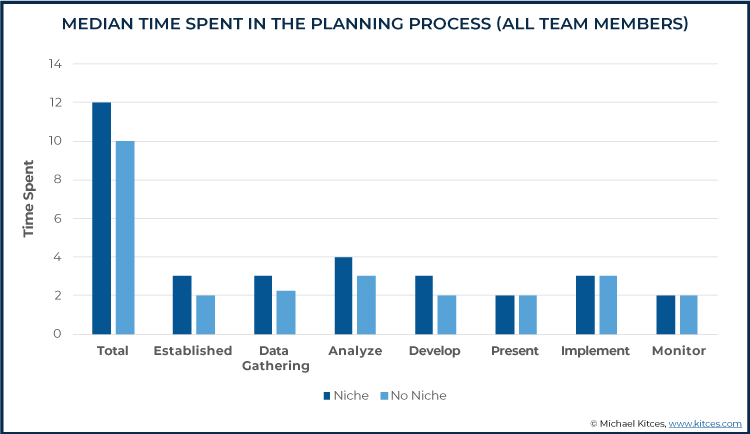

The first area we see some difference is in total time spent in the planning process to put together a plan for a client. In this area, we actually see that advisors with a niche are spending more time (among all team members) in total, particularly in the upfront areas of establishing the client relationship, data gathering, analyzing recommendations, and developing recommendations. All other categories at the plan presentation to implementing and monitoring stages were equal.

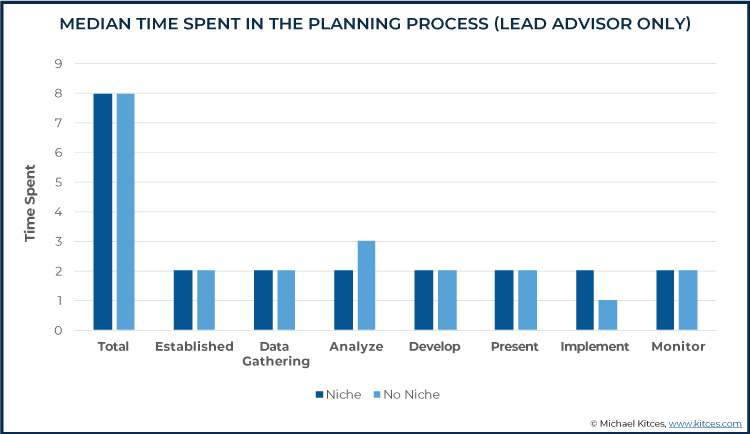

If we look at only time spent in the planning process by the lead advisor, though, the differences are less pronounced.

In this case, both lead advisors with and without a niche are spending a total of 8 hours in putting together a plan. The only difference we see is that advisors without a niche are spending more time in the analysis step (but less time in the implementation step), which makes sense in that systemizing repeatable expertise would be most likely to show up as time-savings in the otherwise time-intensive analyze step of the financial planning process. And these relationships broadly hold for the 25th and 75th percentiles of planning time as well, with the caveat that, if any differences are observed, generally advisors with a niche tend to be spending slightly more time in the planning process.

Which suggests that in general, while niche advisors appear to be spending more aggregate team time in the financial planning process, by and large it’s a result of hiring additional staff to support their niche practice. Which may actually be an indicator that niche firms are better positioned to reinvest into hiring to scale their niche practices (a trend to monitor in future editions of our research!).

Still, the key point is that even if niche advisors are finding some efficiencies within middle-office and back-office tasks generally, we don’t see advisors spending less time in the planning process itself.

This finding appears to be similar to our previous finding that advisors using account aggregation technology similar don’t actually spend less time in the data gathering process, implying that when the data gathering process is expedited, advisors don’t save time but instead reinvest that time to go deeper in their data gathering for clients. Similarly, we would anticipate that the process of, say, developing client recommendations and the depth of the planning analysis looks different for an advisor who has 50 physician clients and has built a practice around this niche, versus an advisor who only has 1 or 2 clients in this area. Two hours spent by an expert with deep knowledge in an area will likely lead to a different (i.e., much deeper) level of recommendations produced than two hours spent by someone who is not well versed in a particular area.

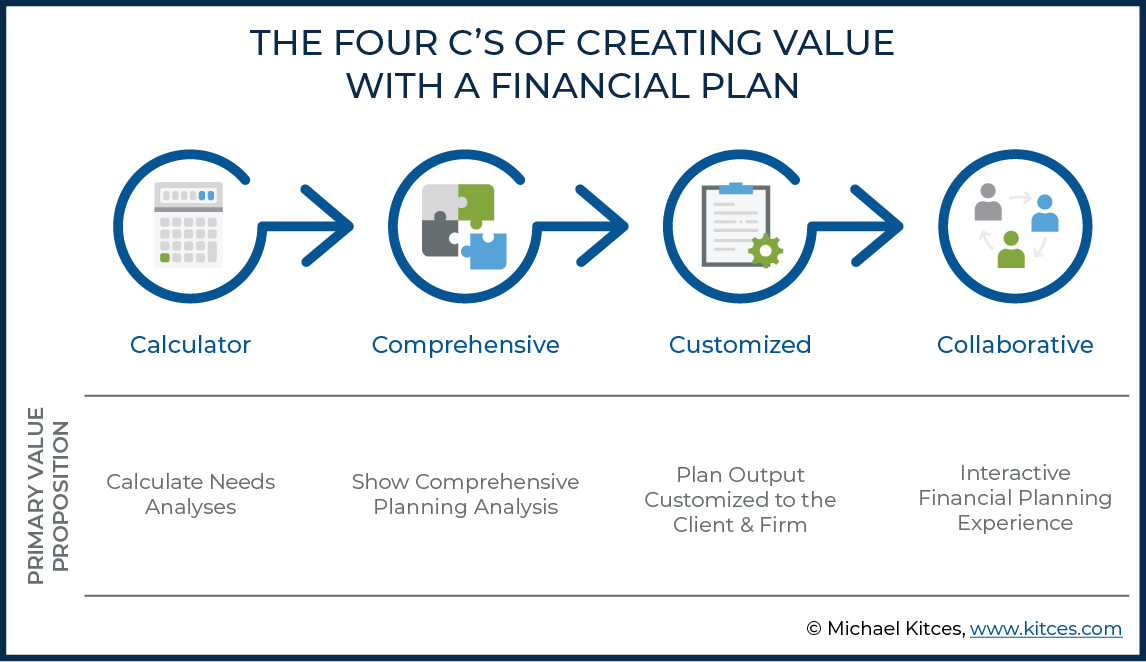

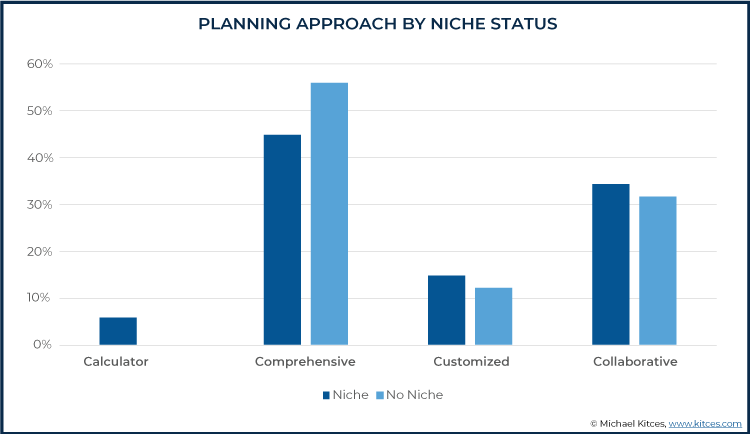

Accordingly, we do see differences in planning approach by financial advisors with a niche. We measured how advisors develop plans according to the “4 C’s” framework for classifying how advisors approach the planning process (calculator, collaborative, comprehensive, customized).

Within this framework, advisors with a niche were more likely to approach planning from a calculator, collaborative, and customized approach, and less likely to approach planning from a comprehensive approach. Which, notably, doesn’t necessarily mean that niche advisors aren’t giving “comprehensive” advice, but simply that they’re not relying on the standard output from comprehensive financial planning software as “The Plan” they provide to their clients; instead, they’re more likely to deliver a customized or collaborative planning experience, and/or to use planning software just as a calculator (ostensibly to supplement the rest of their planning process).

These findings also make sense from the perspective that more consistent client needs lends itself better to being able to systematically use a tool (e.g., calculator approach) and some additional need to go outside the confines of traditional software on a consistent basis (e.g., customized approach).

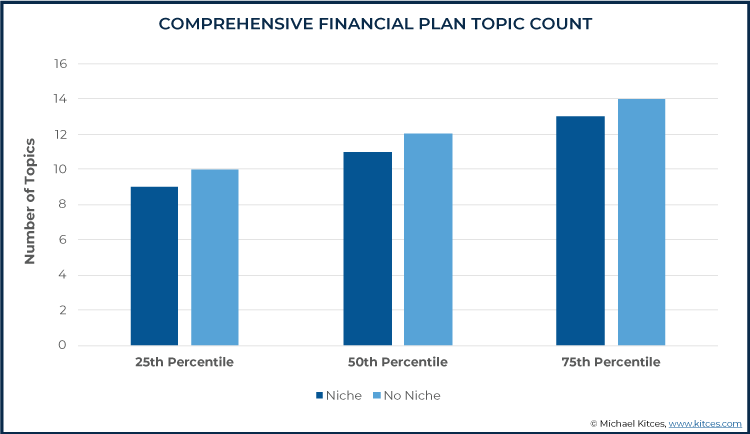

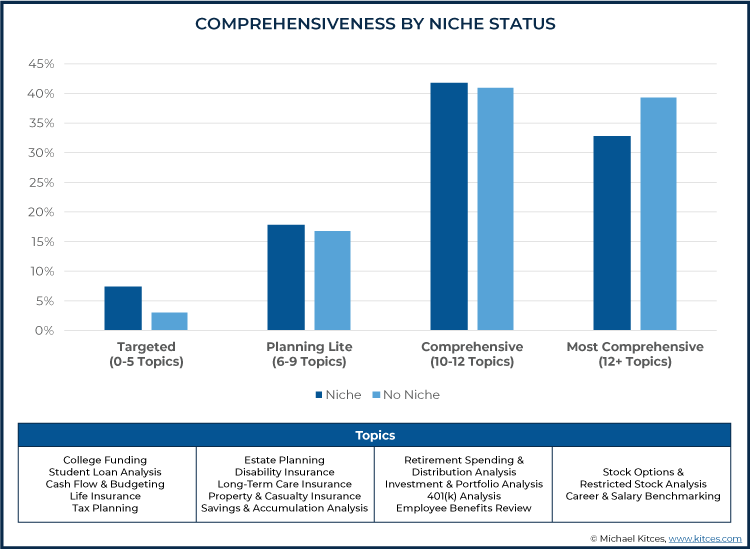

On the other hand, we do find that niche advisors tend to indicate they would cover a narrower list of topics in a comprehensive plan, suggesting that they really are producing more focused financial plans as well.

At the 25th, 50th, and 75th percentiles, advisors with a niche indicated that they would cover a lower number of topics in a “comprehensive” plan. After all, if an advisor is consistently working with a particular set of clientele, some areas of planning just aren’t likely to be relevant for any of their clients (e.g., very little college planning for a niche of retirees whose children are already adults, very little retirement planning for a niche of Millennials who are focused on career and near-term budgeting and cash flow, etc.).

Furthermore, we classified advisors as either targeted (0-5 topics), planning lite (6-9 topics), comprehensive (10-12 topics), or most comprehensive (12+ topics), which again shows the overall differences in defining what comprehensive means between advisors with a niche and those without, as niche advisors were most likely to produce “comprehensive” plans but not the most comprehensive (i.e., there were comprehensive, but not trying to cover every possible topic for every possible type of clientele!).

Overall, though, niche advisors were also significantly more likely to be in the “targeted” somewhat more likely to be in the “planning lite” categories of financial planning. Again, this likely speaks to the ability to be more streamlined in the topics that an advisor covers. If clients in one’s niche never need to deal with stock options, for instance, then advisors don’t need to worry about building considerations of that topic into offering a “most comprehensive” plan.

We also see some differences in the software used by financial advisors with a niche versus those without. Advisors with a niche are more likely to use third-party planning software, but also more likely to use proprietary firm-developed tools, Excel, and Word. The use of all of these programs to supplement a core third-party planning platform are consistent with the notion that niche advisors are systematically adding content to the planning process that goes outside of the cookie-cutter options that come out of their software.

The only area where we see less adoption among advisors with a niche is in the use of specialized tools (e.g., tax planning software, Social Security optimization software, etc.). We do find this somewhat surprising, although it is possible that customizations elsewhere reduce the need for these types of tools. In other words, ‘generalist’ advisors use specialized tools, but niche advisors are more likely to develop their own specialized tools and templates in Excel and Word. Furthermore, planning in these specialized areas for niche advisors may become more consistent, and reduce the need for some of these supplemental tools in the first place. And of course, many popular niches today simply won’t need the often-retirement-centric specialized tools that are available; for instance, an advisor focused on working with millennials will have no need for Social Security optimization software.

Does Niching Drive Greater Productivity For Advisors?

In the sections above, we saw some evidence for advantages to niching in terms of the composition of an advisor’s time (more time with clients and prospects; less time doing middle-office and back-office work), small efficiencies within the planning process (less time in the analysis planning step; with the caveat that lead advisors spent more time in implementation), and planning topic efficiencies in being able to concentrate their planning more narrowly. But with our Kitces Research surveys, we can also take a closer look at more direct metrics of advisor success, such as client service levels and income.

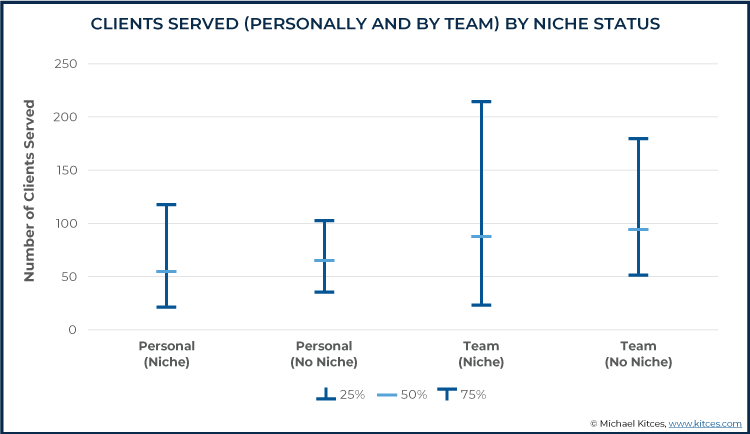

In terms of total clients served (by both an advisor individually and the advisor’s team), we do see some differences between advisors with a niche and those without.

At the 50th and 25th percentiles, we see advisors with a niche are serving slightly fewer clients than those without a niche (e.g., median of 65 clients for those without a niche versus 56 clients for those with a niche). Similarly, at the 50th and 25th percentiles, we see advisors with a niche are serving a lower number of clients through their teams.

However, at the 75th percentile, we see advisors with a niche are serving more clients both personally and in total via their team (e.g., 119 clients for advisors individually with a niche versus 104 clients for those without), further supporting the earlier time-use indications that the most effective advisors with niches are better able to scale their team delivery of financial planning to clients.

Notably, though, this doesn’t necessarily mean that niche advisors are significantly less efficient until they scale up. One alternative explanation of this greater dispersion in general among advisors with a niche versus those without is that having a niche may also allow advisors to choose to profitably serve fewer clients if more of those clients are an ideal fit (i.e., working with 20 doctors may be more profitable than working with 30 clients all with varying backgrounds). In other words, advisors with a niche are likely more “choosey” in who they work with. These factors could lead to the lower levels of clients served at the 25th and 50th percentiles within our dataset, because they’re able to similar or higher levels of revenue from a smaller client base.

On the other hand, for those who do want to scale up, niches are even more clearly providing efficiency and better ability to scale at the high end, which then leads to the higher number of clients served at the upper end of advisors within our survey. For instance, serving 150 retirees with similar needs will be more efficient than serving 150 clients with varying backgrounds and differing needs. All else being equal, this creates a higher ceiling in terms of client capacity (and thus income potential) for financial advisors with a niche over those without.

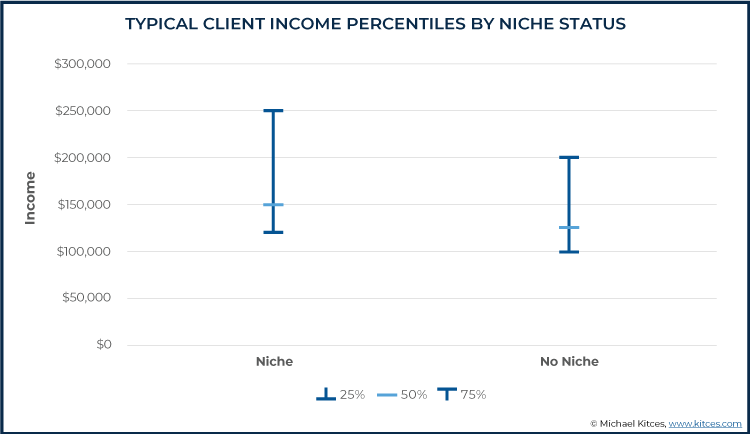

We also see some evidence that advisors with and without a niche are working with different types of clientele.

The graphic below shows income levels for a typical client of an advisor.

As we can see, advisors with a niche are serving clientele with higher incomes at the 25th, 50th, and 75th percentiles.

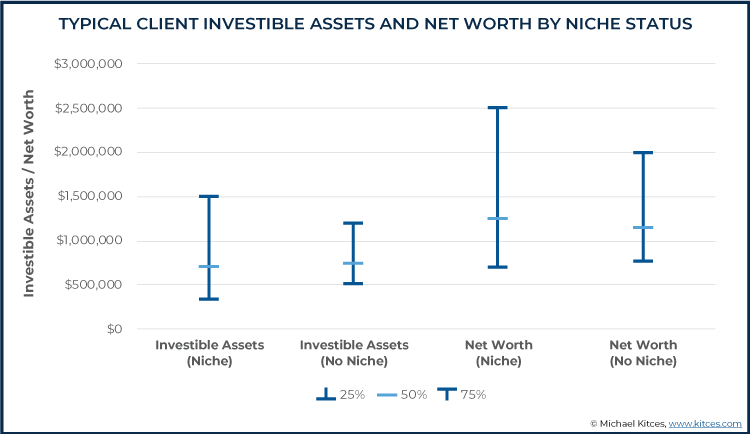

However, we see some different relationships among client investible assets and net worth.

In this case, we see lower levels of client investible assets and net worth at the 25th percentiles (e.g., advisors with a niche serving typical clients with “only” $325,000 of investible assets versus $500,000 for advisors without a niche), but higher levels of client investible assets and net worth at the 75th percentiles (e.g., advisors with a niche serving typical clients with $1.5 million in investible assets versus $1.2 for advisors without a niche).

This again speaks to the dispersion of how advisors appear to be adapting their business models when pursuing niches, as some advisors more “upmarket” and use their niche to attract more affluent clientele and thus are able to service fewer clients to generate similar or greater revenue, while other advisors use the efficiency benefits of niching to move “downmarket” and are able to effectively serve less affluent clients because they can do so more scalably with a niche offering.

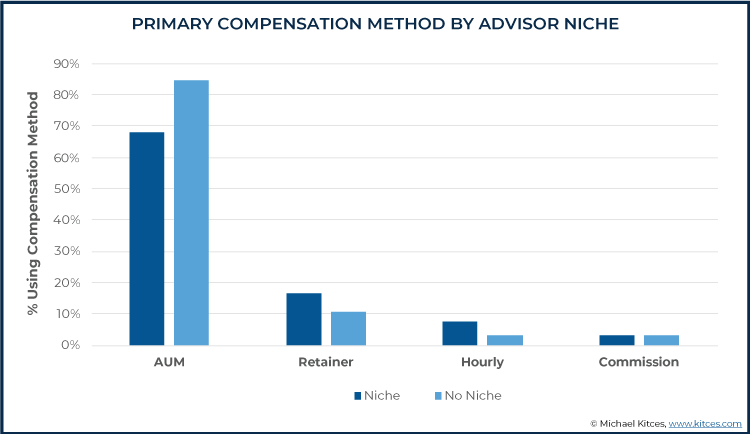

However, looking at these client demographics holistically at the lower end of the asset/wealth spectrum, there is some indication that advisors with a niche here are serving clientele that may be using newer fee models such as retainers, as we see lower levels of investible assets and net worth but higher levels of income. We can confirm this by looking at how advisor compensation methods break down by niche status.

As you can see above (and was expected given the client demographics at the 25th percentiles), advisors with a niche are primarily using compensation methods such as retainers and hourly at higher rates than advisors without a niche. In other words, niches appear to be helping advisors both attract ‘non-traditional’ non-AUM clients who can be served profitably with alternative fee models, and in general is more likely to be associated with charging standalone fees for financial planning advice.

Still, though, while the use of retainers and hourly models may also be disproportionate among niched advisors with clients at the higher end of the spectrum, it is worth noting that niche advisor clients at the 75th percentiles do appear to be more wealthy and affluent than clients of advisors without a niche at this upper end as well.

The more wealthy and affluent clientele at the 75th percentile likely speaks to the attractiveness of well niched advisors to clients within the most competitive segments of the market. As a high-income high-wealth affluent physician is shopping for an advisor, an advisor with a clear focusing of serving physician clients in similar circumstances will be better positioned to win this business (even when competing against a slew of other AUM advisors with whom the doctor would qualify by asset minimums).

How Do Niche Advisors Price Their Financial Planning Fees Differently?

When it comes to charging financial planning fees themselves, advisors vary tremendously. The ongoing dominance of the AUM model means that most advisors by numbers still charge primarily AUM fees, though a growing number are at least also charging hourly, retainer, or other minimum fee models. In addition to a small but growing base of advisors who are charging alternative standalone fee-for-service models (e.g., monthly subscription fees, annual retainer fees, etc.).

Accordingly, it is perhaps not surprising that we also see that advisors with and without a niche are pricing their services differently within these various compensation methods.

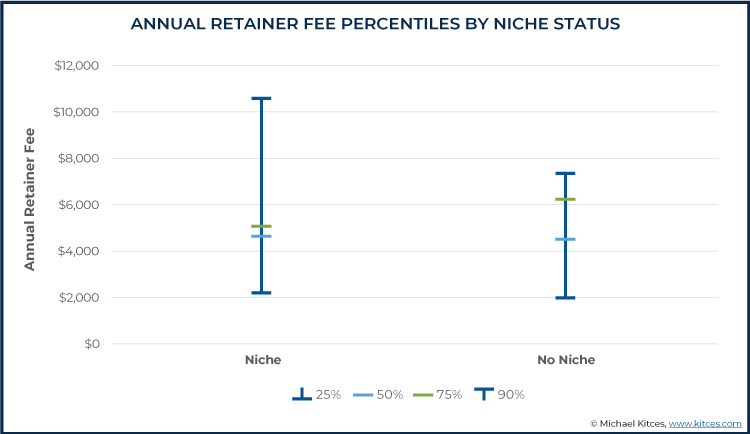

As indicated in the graphic above, advisor retainer fees are slightly higher for advisors with a niche at the 25th percentile ($2,125 versus $1,900) and the 50th percentile ($4,650 versus $4,500), but substantially higher among advisors at the 90th percentile ($10,600 versus $7,360).

Interestingly, advisors without a niche are the highest however at the 75th percentile ($6,250 vs $5,000), which may be due to clustering (25% of advisors with a niche in our study priced their typical retainer at $5,000) that is perhaps driven by psychological resistance to going above the $5,000 level amongst advisors who do have a niche.

Still, though, for advisors who break through their own fee resistance and gain confidence in their pricing, the high end of niche advisors are clearly finding the ability to charge materially higher retainer fees than non-niche advisors.

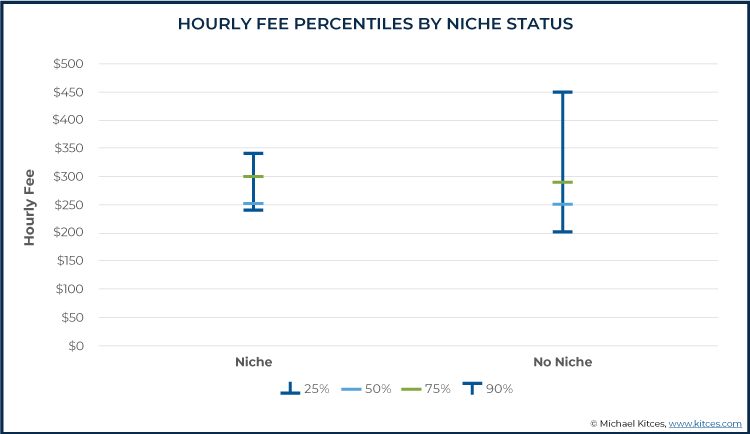

Advisors at the 25th, 50th, and 75th percentiles with a niche also priced their hourly fee equal to or higher than advisors without a niche. The median hourly fee was $250 amongst both advisors with and without a niche. The 75th percentile fee was $300 for advisors with a niche versus $288 for those without. However, advisors without a niche had higher hourly fees at the 90th percentile ($450 versus $340). Although our prior Kitces Research has suggested that a large subset of AUM advisors ‘offer’ hourly services but are not trying to scale the volume of their hourly advice, and consequently may deliberately price their services materially higher – in a way that would not attract but actually reduce their hourly engagements – in an effort to dissuade all but a small subset of the most profitable hourly business to supplement their otherwise-profitable AUM business. While advisors who are primarily in the business of hourly advice – and need to generate an ongoing volume of hourly engagements – price at least somewhat more modestly on average (and higher with niches).

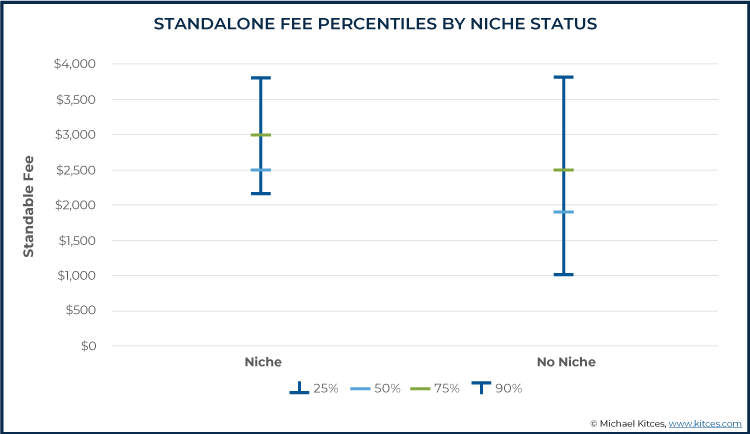

In terms of the price for a standalone comprehensive plan, we see no difference between advisors with a niche and those without at the 90th percentile ($3,800), but we do see higher pricing among advisors with a niche at the 75th percentile ($3,000 versus $2,500), the 50th percentile ($2,500 versus $1,900), and the 25th percentile ($2,150 versus $1,000). This may be an indication that advisors without a niche are more inclined to use standalone planning fees as a loss leader for new business development rather than a service that is intended to be profitable itself. While advisors with a niche are more able to command a viable financial planning fee for their financial planning advice alone, and actually generate enough income from their niche financial planning advice itself without being separately paid for subsequent implementation.

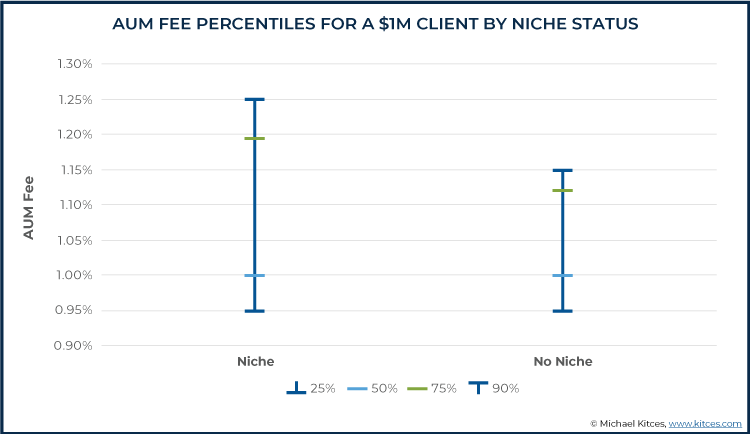

In terms of AUM pricing, we do not see any pricing differences between advisors with a niche and those without at the 25th and 50th percentiles for a client with a $1 million portfolio (0.95% and 1.00%, respectively). However, we again see that advisors with a niche are pricing their services higher on the high end, which comparably higher fees at the 75th (1.19% vs. 1.12%) and 90th (1.25% vs. 1.15%) percentiles. Which again suggest, similar to the data on retainer fees, that advisors in ongoing relationship models with clients are able to command a premium at the upper end of the pricing scale when they focus into a niche and can effectively differentiate their services enough to prevent clients from ‘price-shopping’ their above-average fees.

Average Financial Advisor Income Levels For Niche Vs Non-Niche Advisors

Of course, differences in pricing, productivity, and other metrics, may not matter so much if they don’t lead to actual differences in financial advisor income at the end of the day. However, by this metric, we again see strong performance from niche advisors at the high end.

A few items are worth noting in the chart above.

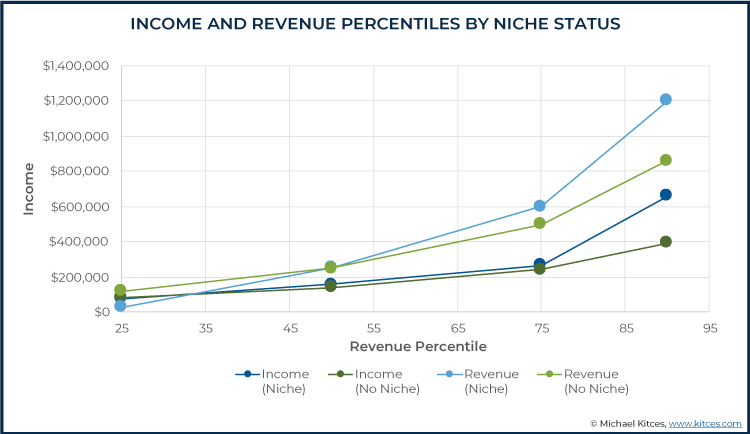

First, it is interesting that revenue of advisors with a niche at the 25th percentile ($30,000) is actually lower than income ($77,500) at that same level. We asked advisors for all income related to activities as a financial advisor, so it is possible that these advisors have some side income (e.g., paraplanning, etc.) that is supplementing their income while they grow their business. This was the only place we saw this relationship that advisors managed to generate more total income than they earned in revenue from their practices. Income among advisors without a niche was slightly higher at the 25th percentile ($86,250), while revenue for these advisors was significantly higher ($120,000).

At the 50th percentile, though, niche advisors were slightly higher in both income ($160,000 vs. $142,500) and revenue ($255,000 vs. $250,000). And as success rises further, a real divergence occurs above the 50th percentile, with niche advisors reporting higher take-home income and revenue at both the 75th ($267,500 vs. $243,750; and $600,000 vs. $500,000, respectively) and 90th ($660,000 vs. $395,000; and $1.2M vs. $860,000, respectively) percentiles. Notably, this data suggests that not only are niche advisors able to generate significantly more revenue at the high end, but the highest revenue niche advisors were also significantly more efficient at turning their revenue into take-home income, turning $1.2M of revenue into $660k of earnings (a 55% take-home rate) compared to only $395k earnings on $860k of revenue (a 45% take-home rate) for non-niche advisors.

Still, the fact that advisors at the lower end of the earnings spectrum appear to be struggling more in generating income and revenue in a niche is concerning. But while our data doesn’t speak directly to this, per se, the lower performance of niche advisors towards the lower end of the spectrum could be an indicator of several different things. First, it may be an indicator that there’s a long-term growth element to niching. Advisors who go out and accept any business they can may do better in the short run, but as they accumulate disparate clients it becomes difficult to scale a business and reach the highest levels of success.

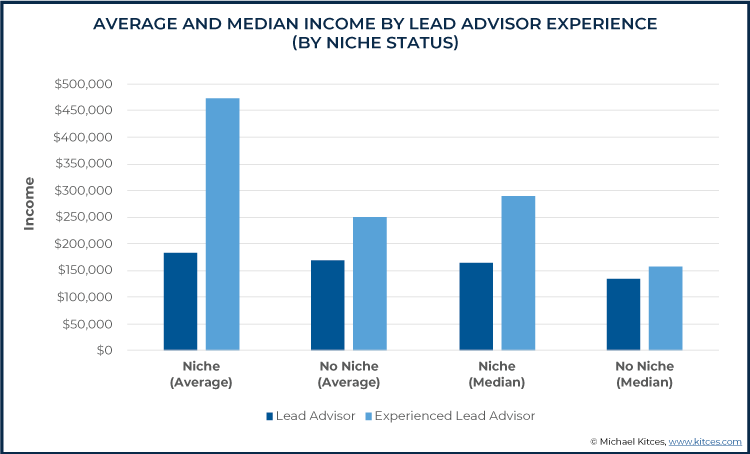

However, these findings may also provide some caution against niching too soon. With the exception of individuals who already have really strong networks within their target niche (e.g., a physician, executive, or other professional changing careers), it’s not clear whether the advisors in our study with the strongest niches grew those niches intentionally or may have accidentally stumbled upon them. However, we do see that the divergence between advisors with a niche and those without appears to be strongest among experienced advisors with more than 10 years of experience.

As the graphic above indicates, while there are minor differences between advisors with and without a niche with less than 10 years of experience (e.g., median income of $165,000 for those with a niche vs. $135,000 for those without), the differences are much larger among advisors with 10+ years of experience (e.g., median income of $290,000 for those with a niche vs. $158,000 for those without). Again, this could be consistent with niching being a long-term strategy… but also one that advisors may not want to adopt too fast (but not too slow, either!).

After all, the reality is that financial advisors are often surprised by where a niche emerges. Particularly in the early years, when it may be advantageous for an advisor to take anyone who is willing to work with them, advisors may want to be open-minded to the unexpected ways in which their business might evolve. Perhaps someone who thought they were going to work with engineers gets a tee time with a local physician, signs that physician as a client, that physician goes on to refer four of their partners to the advisor, and then a niche in working with physicians is born.

While our data cannot speak to it, per se, it is possible that niches are more commonly pivoted into once an advisor reaches some critical mass with a particular demographic, rather than being a result of planning from the start. Perhaps instead of niching from the start, advisors would be better off heeding the standard practice of taking everyone at first, but then being careful to not grow too large before finding a viable niche to pivot into (and possibly shedding some non-ideal clients at this point). Though alternatively, the fact that so many advisors find niches by serendipity and happenstance instead of a deliberate upfront plan may simply be a result of the fact that so few advisors have tried, and there are relatively few pathways and templates on how to pick a niche for those who do want to begin that way from the start.

Furthermore, we do see some evidence that waiting too long to niche could result in advisors getting “stuck” in their growth. For instance, advisors with a niche in the bottom 25th percentiles of income had an average of 4.8 years of experience as a lead advisor versus an average of 9.3 years of experience among advisors without a niche. This could suggest that more experienced niche advisors move forward more and/or faster. In fact, we see advisors with a niche have less experience at every percentile grouping, including an average of 13.9 years of experience at the 76th percentile and higher versus 15.8 among advisors without a niche. Which suggests that niche-based advisors are in fact out-compounding the growth of non-niche advisors, but generally may have smaller practices simply because niching is newer and the average niche advisor hasn’t had as much time to accumulate client growth in their niche (yet).

Ultimately, however, what we do see from our data are fairly consistent differences in advisors with and without a niche, and these differences become particularly pronounced among the high performers within each respective category. We see that advisors with a niche report spending their time in more productive ways (28% more time with clients and prospects; 13% less time doing middle-office and back-office tasks), greater efficiency within the planning process (25% less time in the analysis stage), greater concentration in planning topics focused on (20% less likely to adopt a “comprehensive” approach compared to a collaborative, customized, or targeted approach), often charging higher fees at the high-end of the spectrum (9% higher AUM pricing and 20% higher standalone planning fees at the 75th percentile), and earning significantly more take-home pay as an advisor at the high-end of the spectrum (an additional $265,000 at the 90th percentile). While our data, unfortunately, cannot speak to when advisors make the decision to niche within their career, we do see some clear value in niching across a broad range of metrics.

I really appreciate you taking the time to break this down. I am focusing on the real estate investor niche for real estate financial planning and super helpful to see the difference between niching versus not. Thank you!

Happy to be of service, James! I hope it helps!

Let us know what else you’d like to see, and we can focus there in future research! 🙂

– Michael

It would be interesting to see a comparison on the % advisors with and without a niche across different business models. I would guess niches are more common for planners in the RIA channel than the bank channel. Maybe ask whether having a niche is encouraged or not in their channel/workplace. How easy it is to do marketing may affect whether a person is in a niche. If you are owner of a small RIA you have total control over marketing and can more easily transition to a niche but if you are in a firm amongst many reps it may be hard to market yourself trying to publicize your niche or your fee model without going against the company’s branding/marketing. The revenue below income data may show a side hustle but may also show a new advisor being groomed in a firm that just started taking on clients but earns much of their income by assisting other more experienced reps. I also would be interested to see what the answer is to the question ‘for planners with a niche, was it intentional? Also, did you pick a niche from the start or adopt one only after getting some experience first.’