Executive Summary

Financial planning, and the process of creating a financial plan, has changed extensively over the nearly 45 years since the first class of CFP certificants. While early on, the financial plan was used primarily as a Calculator to do Needs-Based Analyses for the products they had to sell, over time it evolved into a Comprehensive Financial Plan that advisors could actually get paid for independent of any product implementation, which advisors then in turn Customized even further, and are now increasingly delivering Collaboratively with clients (where the focus is on the planning experience, and The Plan itself is merely delivered after the fact to commemorate the planning decisions already made).

Yet unfortunately, remarkably little research exists on how, exactly, financial advisors are actually preparing and delivering financial plans today. How often do advisors charge separately for planning? What is it that they actually deliver to clients? When advisors complain that it is very “time-consuming” to do financial planning, which part, exactly, is so time-consuming? And to what extent does financial planning software expedite the process… or exacerbate the problem?

In this context, we’re excited to announce the first Kitces Research initiative – a comprehensive study on the process that financial advisors actually go through to create and deliver a financial plan. Think of it as a benchmarking study for the creation of the financial plan itself, with a focus on identifying best practices.

So whether you’re frustrated that financial planning software doesn’t “do” what you need it to in order to demonstrate its value, or are simply looking for ideas to refine your own financial planning process to be more time-efficient or cost-effective (or valuable and able to command a higher price!), I hope you’ll take a few minutes to participate in our Financial Planning Process survey and help the world better understand what real financial planners actually do!

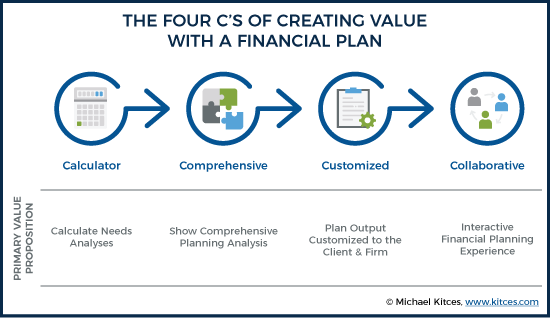

The Four Cs Of The Evolving Financial Plan Value Proposition

In its early days, Financial Planning was simply a form of “needs-based selling”, a more consultative-style approach of sales where, instead of simply trying to talk about the features and benefits of whatever product(s) the company had in inventory, the advisor tried to first understand the concerns and needs of the client… and then show how their available product(s) could help address the client’s needs and achieve their goals.

In this context, financial planning software served a valuable “Calculator” function, aiding advisors in calculating with clients exactly how much the client needed to save per month for retirement (into the advisor’s recommended investment product), or calculating a capital needs analysis of exactly how much life insurance the client needed (of the advisor’s recommended insurance product).

Over time, though, the financial plan began to get more and more comprehensive, as insurance companies began to cross-licensed their insurance agents into brokerage products, broker-dealers established affiliated insurance relationships. After all, the more comprehensive the plan, and the wider the shelf of insurance and investment products available to the advisor, the more opportunities there were to do business with the client!

Yet the evolution of financial plans from Calculating individual product needs (and how the advisor’s products could help to address those needs) into a more Comprehensive solution began to turn the financial plan into a “thing” that was valuable unto itself. Particularly in a world where most consumers didn’t have access to sophisticated analytical software that could really compute how all the different pieces fit together and show a comprehensive view of it all.

Accordingly, “The Plan” was born – a physical Financial Plan deliverable, that advisors could produce and deliver and actually get paid for with a standalone financial planning fee… regardless of whether the client actually implemented anything at all! Because the advisor wasn’t being paid to use the plan to demonstrate a product need; the advisor was paid for the Comprehensive plan itself.

In practice, though, the Comprehensive Financial Plan deliverable still emerged in an era where most advisors were affiliated with large companies that were in the business of distributing products, and as a result they largely treated the Comprehensive Financial Plan as a product – assembled in a standardized manner, often with a centralized planning team (conducive to efficiencies and economies of scale), and assured that “The Plan” would be consistent for every client because the output of the planning software itself could be controlled.

The rise of the Comprehensive Financial Plan drove a rapid growth in financial planning software and adoption, yet the constraint of traditional financial planning software output mean that the growing volume of comprehensive financial plans were increasingly “cookie-cutter” ones. Which in turn set the stage for the next step in the evolution of the financial plan, aided by the growth of CFP certification, rising expertise of advisors, and a shift of more and more financial advisors aiming to demonstrate unique and differentiated value in their advice: the Customized Financial Plan.

Of course, the reality was that every Comprehensive Financial Plan was based on the data and inputs from – and therefore “customized” to – the needs of the client. The distinction of the Customized Financial Plan was that, in an attempt to differentiate, advisors began to supplement the output of financial planning software with their own financial plan deliverables not part of the standard template, from Executive Summaries and advisor-written Recommendations and Action Items, to customization of the physical plan deliverable itself (e.g., custom binders, emblazoned with the firm’s logo, with the plan printed in the firm’s color palette with custom graphics). Which, notably, entailed far more time for customization than the standard cookie-cutter Comprehensive Financial Plan that preceded it.

Ultimately, though, a more fundamental problem began to emerge with this approach, beyond just its increasingly-time-consuming nature: the realization that, even with customization, few clients ever actually read the customized comprehensive plan once they leave the advisor’s office! And the more the advisor customized and expanded the depth of the financial plan, the more likely clients were to feel overwhelmed by it all.

In addition, from the client’s perspective, being “presented” a thick comprehensive financial plan, customized though it may be, is still not necessarily very engaging or motivating. Which matters a lot, in a world where, in the end, the client will measure the value of advice not by how thorough or accurate it is, but by the extent to which it actually creates a positive change and outcome for the client.

Accordingly, financial advisors began to deliver their plans more collaboratively with their clients, using sliders and other interactive tools to turn the financial plan deliverable into a financial planning experience instead. Just as when we want to buy a car, we don’t ask for a written comprehensive family transportation plan – we instead take it for a test drive! – so too was there a realization that clients didn’t just want a plan that told them what to do… they wanted to be part of the process in co-creating what the plan should look like alongside the advisor. Which is notable, because in a collaborative and interactive plan delivery, “The Plan” itself may be little more than a document sent out after the fact to commemorate the planning decisions that were already made!

In today’s world, financial plans are still delivered across this spectrum of value propositions – from the plan as a Calculator of (product) needs, to a Comprehensive Plan, a Customized plan deliverable, and a Collaborative planning experience. Yet the distinctions are important, because they entail a substantively different process in preparing and delivering financial planning to the client, require different time and other resources, and place very different demands on what financial planning software must provide to support the process.

New Research On How Financial Planners Actually Do A Financial Plan?

Unfortunately, though, in today’s financial planning world, there’s remarkably little information about how most financial advisors actually do financial planning, the time it takes, and the extent to which financial planning software effectively supports the process (or not).

We don’t know how many advisors use a financial plan as a calculator for a focused needs analysis, versus offering comprehensive plans, how often advisors customize their plan output for clients, and to what extent a more collaborative financial planning is really gaining traction (or not)?

And there’s even less information about where the pain points are in the financial planning process – from the advisor’s perspective – and how to make the process itself more efficient. For instance, many advisors complain about the time-consuming nature of producing and delivering financial plans… but which part(s) are actually the most time-consuming? Is it the data gathering? The analytical stage? The amount of time it takes to customize a financial plan for the client and produce the deliverables? To what extent can these tasks be outsourced or delegated, or better automated with technology?

And these questions in turn raise additional ones… to what extent is today’s financial planning software up to the task of modern financial plan creation? Are some planning software tools better suited to certain types of planning approaches and value propositions than others? And how often are financial advisors forced to go “outside” of their financial planning software to create their entire financial plan (or financial planning experience) using word processors, spreadsheets, or other more specialized tools?

It’s in this context that we’re excited to announce the first Kitces Research initiative – a comprehensive study on how financial advisors actually do a “financial plan”. It is our goal with this research to gain a better understanding of the current state of how financial plans today are actually created, the time it takes and costs to produce, the ways that financial planning software (and other software tools) are used in the process, and where there are opportunities to improve. Think of it as a benchmarking study for the creation of the financial plan itself, with a focus on identifying best practices.

Accordingly, I hope you’ll take a few minutes to participate in our Financial Planning Process survey. It will likely take you about 30 minutes to complete, and all participants will receive a free copy of the final Research Report that we produce, providing relevant information you can use to compare your financial planning process to others, and best practices you can potentially implement for yourself.

The Survey itself will remain open until Sunday, July 22nd, with the full Research Report due out at the end of August.

Thank you in advance for taking a few minutes to participate in this important financial planning research study!

So what do you think? How do you think the financial plan has evolved over time? What pain points do you experience in the financial planning process? Please share your thoughts in the comments below!

Leave a Reply