Executive Summary

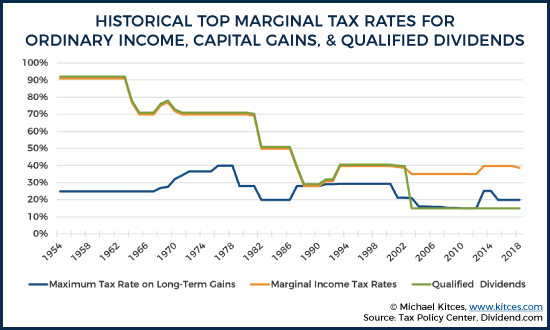

While long-term capital gains have had preferential tax rates for most of their history (and receive similar treatment in most developed countries around the world), it’s only in recent years that long-term capital gains have been subject to not just one, but a series of tiered preferential rates, from a 0% rate for those in the lowest tax brackets, to 15% for those in the middle, and 20% for the highest earners (albeit still a “deal” relative to a 37% top tax rate on ordinary income). Plus a 3.8% Medicare surtax that stacks on top of a portion of the 15%, and all of the 20%, long-term capital gains rates.

The significance of this phenomenon is that, similar to ordinary income tax rates, generating “too much” in capital gains can drive the household up into higher capital gains tax rates. And because capital gains income stacks on top of ordinary income, even just increasing ordinary income can effectively crowd out room for preferential long-term capital gains rates.

In fact, the interrelationship between ordinary income and long-term capital gains creates a form of “capital gains bump zone” – where the marginal tax rate on ordinary income can end out being substantially higher than the household’s tax bracket alone, because additional income is both subject to ordinary tax brackets and drives up the taxation of long-term capital gains (or qualified dividends) in the process.

For instance, individuals with as little as “just” $30,000 of income (after deductions) and some capital gains on top who would normally be in the 12% tax bracket may face marginal tax rates as high as 27% due to the capital gains bump zone. And upper-income households eligible for the 35% tax bracket may face a marginal rate of 40% as the top capital gains tax bracket phases in. The effect can be even worse for retirees who also claim Social Security benefits, where the combination of phasing in Social Security benefits, and driving up long-term capital gains to be subject to the 15% rates, can trigger a marginal tax rate of nearly 50%(!) for a household otherwise in the 12% ordinary income tax bracket!

As a result, it’s crucial to consider the coordination of long-term capital gains with ordinary income, and the phase-in of Social Security taxation. For those with negative taxable income, it is generally still appealing to do partial Roth conversions at a marginal tax rate of 0%. But for others in the bottom tax brackets, it may be preferable to harvest 0% long-term capital gains instead (and not do partial Roth conversions that will undo the 0% rate on those capital gains!). While higher-income individuals may prefer to once again do partial Roth conversions in the 22% and 24% brackets, or even the 32% bracket… while avoiding the additional capital gains bump zone that occurs in the 35% bracket.

The bottom line, though, is simply to understand that with 7 ordinary income tax brackets, plus 4 long-term capital gains brackets (with the 3.8% Medicare surtax), tax planning and evaluating marginal tax rates is a function of not just the ordinary income or long-term capital gains rates themselves, but also the interrelationship of the two and the indirect but substantial tax impact of adding more ordinary income when there are already substantial long-term capital gains stacked on top!

The Four Preferential Long-Term Capital Gains Tax Brackets

For most of its history, the modern tax code has provided a tax preference for (long-term) capital gains, as a means to support and incentivize economic investment. In fact, most developed nations around the world have preferential rates for capital gains over ordinary income. And since 2003, “qualified” dividends (for investors into companies that choose to pay out their profits as dividends instead of reinvesting them to increase the value of the company) have also been eligible for the same preferential (long-term capital gains) rates.

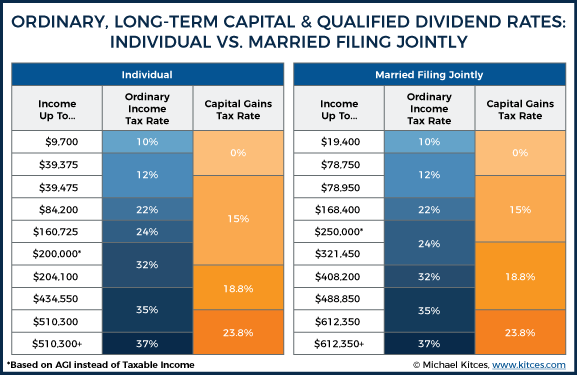

However, preferential capital gains tax rates are not just taxed at a single more favorable rate. Instead, similar to the regular tax system, capital gains are actually subject to three different tax brackets – a series of graduated tax rates similar to the ordinary income tax brackets. Though since the Tax Cuts and Jobs Act, long-term capital gains rates have their own tax bracket thresholds that are separate from the ordinary income tax brackets!

In addition, long-term capital gains (and qualified dividends) are also subject to the 3.8% Medicare surtax on net investment income, which has its own thresholds of $200,000 of Adjusted Gross Income (AGI) for individuals, and $250,000 for married couples (not adjusted for inflation).

Which means in practice, there really aren’t just three long-term capital gains tax brackets… there are actually four, at 0%, 15%, 18.8% (the 15% bracket plus the 3.8% Medicare surtax), and 23.8% (which is the top 20% long-term capital gains tax rate with the 3.8% Medicare surtax stacked on top).

Notably, though, long-term capital gains rates are still graduated tax rates, akin to the ordinary income tax system. Which means just landing in the 0% long-term capital gains tax bracket doesn’t give the opportunity for “unlimited” long-term capital gains at 0%. As while the tax rate may be 0%, capital gains are still income, and would eventually push the individual out of the 0% bracket and into the higher brackets.

Example 1. Phoebe is considering whether to take a $100,000 distribution from her IRA (all ordinary income), or liquidate $100,000 of zero-basis stock (all capital gains). [Assume any other income Phoebe has was already offset by her available deductions.]

If Phoebe takes the $100,000 from her IRA, the income will span across the 10%, 12%, and 22% tax brackets, resulting in a tax bill of 10% x $9,700 + 12% x $29,775 x 12% + $60,525 x 22% = $19,069 in total taxes, or a blended effective tax rate (combining the income across each of the three tax brackets) of about 19.1%

By contrast, if Phoebe took a $100,000 long-term capital gain this year, and is in the bottom tax bracket, she is eligible for the 0% long-term capital gains rate. However, the 0% rate similarly only extends up to $39,375 of income (for a single taxpayer), beyond which the 15% capital gains bracket kicks in.

As a result, Phoebe will owe $9,094 in long-term capital gains taxes, which includes 0% on the first $39,375 of long-term capital gains, and 15% on the last $60,625 of long-term capital gains, for a blended effective tax rate of 9.1%.

The end result is that, just like the ordinary income tax system, long-term capital gains will typically end out being taxed at a blend of multiple tax brackets. Though at the margin, planning for the next dollar of income or deductions will still be based on the current marginal tax bracket (for ordinary income or long-term capital gains).

Stacking Preferential Capital Gains And Ordinary Income Tax Brackets

Unfortunately, the process of managing long-term capital gains and ordinary income tax brackets is messier when there is a combination of each – which in practice is common, as most taxpayers that have capital gains have at least some ordinary income as well. Because once there is some of each type of income, it’s necessary to figure out the order to stack one on top of the other.

In practice, though, the rules for stacking ordinary income and long-term capital gains are relatively straightforward: ordinary income first, long-term capital gains (and qualified dividends) come second and stack on top. And any available deductions are applied against ordinary income first.

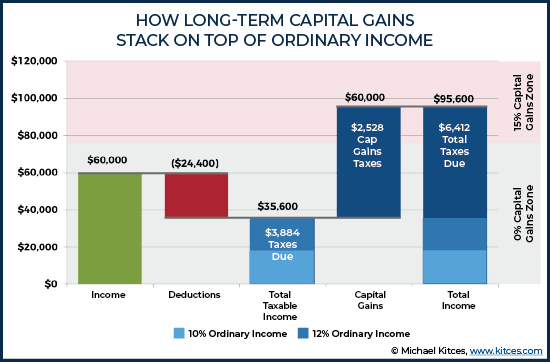

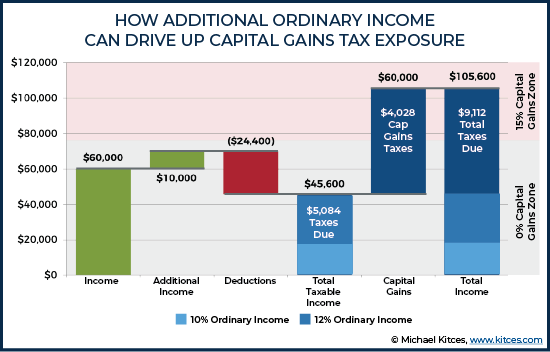

Example 2. Joseph and Rachel are married and have $60,000 of ordinary income, on top of which they are taking a $60,000 capital gain as well. In 2019, they will be eligible for a $24,400 standard deduction.

Under the ordering rules for ordinary income and capital gains, the $24,400 standard deduction will be applied first against the $60,000 of ordinary income, on top of which the $60,000 long-term capital gain will stack. Which results in $35,600 of ordinary income that falls within a combination of the 10% and 12% tax brackets (for a total ordinary income tax liability of $3,884), while the remaining $60,000 long-term capital falls across the 0% and 15% long-term capital gains tax brackets (with the first $43,150 falling in the 0% bracket up to the threshold, and the remaining $16,850 taxed at 15%, for a total capital gains tax liability of $2,528).

Historically, the fact that ordinary income came first, and long-term capital gains stacked on top, was a “good” thing and always produced the most favorable result. As until the advent of the 0% capital gains tax bracket, it was better to get the lowest ordinary income tax brackets first and then stack a “flat” 15% capital gains tax on top, than having long-term capital gains come first and then stack ordinary income at ever-increasing tax brackets on top.

In the current tax environment, though, the fact that ordinary income stacks first has a different effect: it crowds out the available 0% long-term capital gains tax bracket. As to the extent that ordinary income fills the bottom two tax brackets first, there literally isn’t as much room left to claim 0% long-term capital gains tax rates, before the capital gains get pushed up into the 15% tax bracket.

How Coordinated Capital Gains And Ordinary Income Rates Cause A Capital Gains Bump Zone

From a planning perspective, the reason that the ordering of ordinary income and long-term capital gains matters so much is that, because long-term capital gains always stack on top of ordinary income (after deductions), a growing level of ordinary income can end out not only increasing the tax bracket on ordinary income, but by crowding out the bottom tax brackets can also bump up the long-term capital gains rate that stacks on top as well!

Example 3. Continuing the prior example, assume that Joseph and Rachel decide to take out another $10,000 IRA distribution, on top of their $60,000 of existing ordinary income (and $60,000 of long-term capital gains).

Thanks to the ordering rules, the additional $10,000 of income will still be taxed at the favorable 12% ordinary income bracket, bringing their total ordinary income (after the Standard Deduction) to $45,600, for a total tax liability of $5,084.

However, because the 0% long-term capital gains bracket ends at $78,750, there is now “only” $33,150 of room remaining in the 0% capital gains tax bracket, which means $26,850 gets taxed at the 15% long-term capital gains rate, for a total capital gains tax liability of $4,028.

The end result is a total tax bill of $5,084 + $4,028 = $9,112, compared to a tax liability of “just” $6,412 previously. Which means even though the $10,000 distribution was in the 12% ordinary income tax bracket, the couple’s tax liability increased by $2,700 – including $1,200 of additional taxes on the IRA distribution itself, plus $1,500 of additional taxes on $10,000 of long-term capital gains that were pushed up from the 0% long-term capital gains rate to the 15% bracket instead!

As the above example highlights, the manner in which long-term capital gains stack on top of ordinary income can create a “bump zone” of higher marginal tax rates, where additional non-capital-gains income still increases the taxes on capital gains by driving them up into higher tax brackets. In this case, additional ordinary income in the 12% tax bracket was taxed at 27% because the income also drove up the capital gains tax liability by pushing more gains out of the 0% bracket.

This “capital gains bump zone” will occur any time capital gains span across one of the bracket thresholds – from 0% to 15%, from 15% to 18.8%, or from 18.8% to 23.8% - where non-capital-gains income can cause additional capital gains taxes. Even though, ironically, “just” having additional long-term capital gains is not taxed so severely, because additional capital gains go on top of the existing gains (rather than bumping them up).

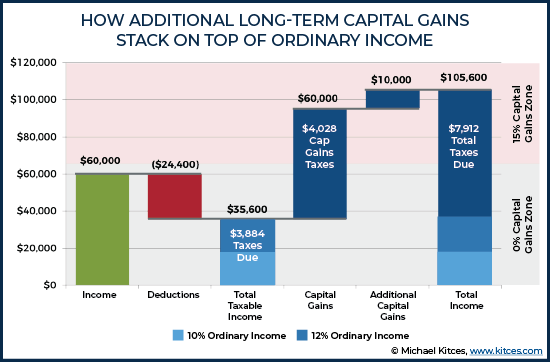

Example 4. Continuing the prior example, assume instead that Joseph and Rachel decide not to take a $10,000 IRA distribution (given the 27% marginal tax rate that will apply!), and instead simply liquidate another $10,000 of their zero-basis stock instead, producing an extra $10,000 of long-term capital gains (for a total of $70,000 in long-term capital gains).

The couple’s ordinary income tax liability will remain at its original $3,884 (a combination of $19,400 in the 10% bracket and the remaining $16,200 in the 12% bracket), while their long-term capital gains will continue to benefit from the 0% bracket for the first $43,150, and the remaining $26,850 taxed at 15% for a total liability of $4,028.

The end result is that the couple’s total tax bill is now $3,884 + $4,028 = $7,912, an increase of only $1,500, or a marginal tax rate of 15% on the $10,000 of additional income.

Notably, couple in this example ended out with a lower tax impact by claiming long-term capital gains at the 15% long-term capital gains tax bracket, than an IRA distribution at only the 12% ordinary income bracket, because of the capital gains bump zone that caused their ordinary income tax rate to actually jump up to 27% instead!

And a similar phenomenon can occur anytime additional ordinary income causes a portion of long-term capital gains to be pushed across a threshold to the next higher capital gains tax rate. For married couples approaching $250,000 of (modified) AGI, the 24% ordinary income tax bracket becomes a 27.8% bracket (as the 3.8% Medicare surtax begins to stack on the long-term capital gains that are pushed over the threshold), and the 35% tax bracket becomes a 40% marginal tax rate as the couple moves up from the 18.8% to 23.8% capital gains tax rates!

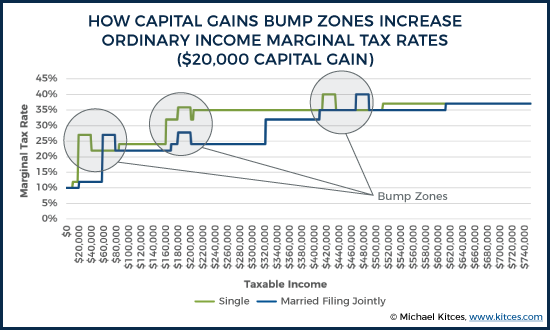

The graphic below shows the “capital gains bump zones” that would stack on top of ordinary income tax brackets for households that had $20,000 of long-term capital gains and incrementally added more ordinary income. As expected, three different bump zones emerge – as long-term capital gains cross the thresholds from the 0% to 15% brackets, from 15% to 18.8%, and from 18.8% to 23.8%. (Notably, the middle bump zone threshold is technically based on Adjusted Gross Income and not taxable income, and thus may occur at a slightly higher or lower level of taxable income in practice.)

How The Capital Gains Bump Zone Complicates Roth Conversions And Retirement Distributions

In many cases, the capital gains bump zone simply is what it is – a higher marginal tax rate that occurs on a portion of ordinary income because it drives up the taxation of capital gains stacked on top. As not all income is malleable in the first place. For instance, those who are still working (and earning wages) and also have some capital gains income may end out having their wages or bonuses trigger the capital gains bump zone… but it’s generally not feasible to ask the employer to wait and not pay wages just to avoid it.

However, in retirement income – and especially taxable income – is far more malleable. From making decisions about the sequencing of which retirement accounts to draw down first, to engaging in partial Roth conversions in order to fill up low tax brackets, there’s often a great deal of proactive tax planning available when some level of taxable income will occur in the process of generating the necessary retirement cash flows… but there’s a lot of flexibility in how, exactly, those cash flows are generated.

In this context, the capital gains bump zone should simply be viewed as a factor that increases the marginal tax rate, and may make the relative value of drawing on a retirement account (either via distribution or Roth conversion) more or less appealing. For instance, a single retiree who wanted to fill the 12% tax bracket with a partial Roth conversion but faces the 27% bump zone may not want to convert after all. While a more affluent married couple who is in the 24% tax bracket that is increasing to 27.8% with the Medicare surtax bump zone may still decide to take distributions from the IRA now, because it’s better than deferring too much and ending out in the 32%+ tax bracket in the future when RMDs begin.

In other words, the ultimate goal is still to minimize taxes on retirement accounts over life by accelerating income when tax rates may be lower (filling the more favorable tax bracket buckets today), and deferring income when tax rates are higher now (and are anticipated to be equal or lower in the future). The capital gains bump zone simply increases that marginal tax rate when doing the tax equilibrium comparison between current and future tax rates… which may or may not deter the appeal of creating the taxable income in the first place.

Nonetheless, for many retirees, it may be a surprise to discover that even with “just” $50,000 to $100,000 of taxable income (for a married couple, or $30,000 to $70,000 for singles), which would normally fall in the 12% tax bracket, that the marginal tax rate may actually be 27% if there is a mixture of ordinary income and capital gains. And the effect can be even more severe for those who are also phasing in the taxability of Social Security benefits, which can similarly create a “tax torpedo” that spikes the marginal tax rate on the 12% tax bracket to 22.2% instead (and conceivably can cause a married couple’s tax bracket to rise as high as 40.7% for those in the 22% ordinary tax bracket who are still phasing in the taxation of Social Security benefits). All of which can stack on top of the capital gains bump zone as well!

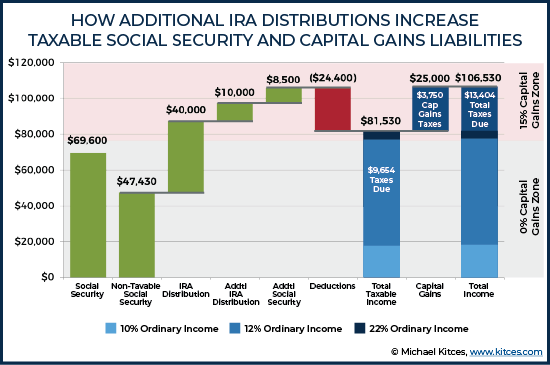

Example 5. Chandler and Monica are retired, and thanks to the fact that both had successful careers, are each eligible for nearly $2,400/month in Social Security benefits. And because Chandler is 4 years older, his Social Security benefits have been further increased to $3,168/month with delayed retirement credits.

In addition to their combined $5,568/month ($66,816/year) in Social Security benefits, the couple is also drawing $28,000/year from Chandler’s IRA (due to required minimum distributions), and liquidated another $32,000 in long-term capital gains this year.

For the purposes of Social Security taxability, the couple’s provisional income is $28,000 + $32,000 + $66,816 / 2 = $93,408, which is $49,408 in excess of the $44,000 threshold for Social Security taxation, resulting in $49,408 x 85% = $41,997 of their Social Security benefits being taxable, plus another $6,000 of taxable Social Security benefits (50% of the amount between the $32,000 and $44,000 Social Security taxability thresholds), for a total of $47,997 of taxable Social Security benefits.

Thus, the couple’s total ordinary income is $47,997 + $28,000 = $75,997, reduced to $51,597 after the $24,400 standard deduction (placing them in the 12% ordinary income tax bracket). On top of which the couple will have $32,000 of long-term capital gains (which spans the $78,750 threshold for the 0%-to-15% long-term capital gains rate for a married couple). Thus for any income that is created, Chandler and Monica will both face the phase-in of Social Security taxation, and the capital gains bump zone.

Accordingly, if the couple were to withdraw another $10,000 from their IRA while they are current in both the Social Security phase-in zone and the capital gains bump zone, not only would their ordinary income increase by $10,000, but the taxable portion of their Social Security would also increase by $8,500, and $10,000 of their long-term capital gains would be pushed up into the 15% zone.

The end result is that under the original scenario, the couple’s tax liability was $5,804 on their ordinary income (of $51,597) plus $727 of capital gains taxes (on the $4,847 of capital gains that was over the line into the 15% tax bracket) for a total tax liability of $6,531. With the additional $10,000 of income, though, the couple’s ordinary income rises to $70,097, producing an ordinary income tax liability of $8,024, in addition to increasing their capital gains tax liability to $3,502 (as now most of their long-term capital gain is above the 0% threshold), for a total tax liability of $11,526.

Which means their $10,000 of additional income generated $11,526 - $6,531 = $4,995 of additional taxes… or a whopping 49.95% marginal tax rate, due to the combination of Social Security benefits phase-in, plus the capital gains bump zone (and the interaction effect between the two!). Notably, the 49.95% tax rate is ultimately the combination of 12% (ordinary income) + 15% (long-term capital gains) = 27% x 1.85 (the Social Security inclusion multiplier) = 49.95%.

Coordinating Capital Gains Harvesting And (Partial) Roth Conversions

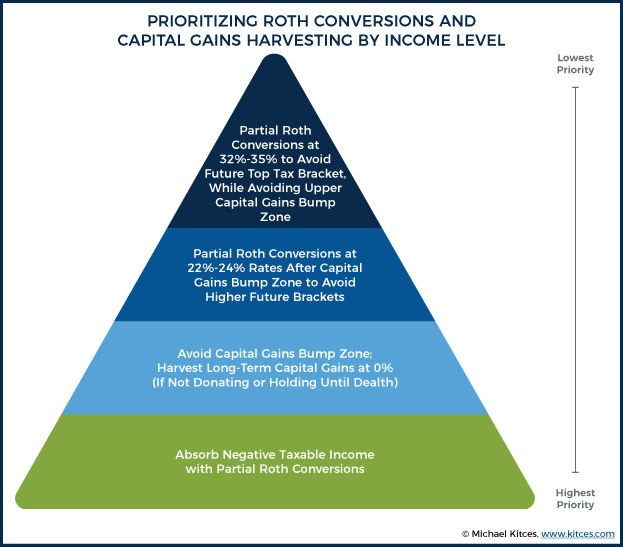

Another planning issue that arises from the capital gains bump zone is the coordination of capital gains harvesting (to take advantage of the 0% tax rate) and doing partial Roth conversions (to fill the lower ordinary income tax brackets and avoid potentially-higher tax brackets in the future). Because, as noted earlier… the decision to do a partial Roth conversion in order to fill up the lower ordinary income brackets also crowds out any room to do 0% capital gains harvesting as well!

In prioritizing the two, the ultimate question is to determine which produces a better long-term tax savings (i.e., the tax bracket that would apply now, versus the one that might otherwise apply in the future).

For those who have negative taxable income (i.e., deductions exceed income in the first place), partial Roth conversions will effectively have a marginal tax rate of 0% (at least at the Federal level), and arguably it’s hard to ever beat 0% on a pre-tax retirement account. Which means “absorbing” any negative taxable income with a partial Roth conversion comes first.

From there, it’s difficult to beat 0% on long-term capital gains… at least, unless the household anticipates either holding the stock until death (to get 0% capital gains with the step-up in basis at death) or donating it (directly to a charity or via a donor-advised fund) to avoid the capital gains tax liability. Thus, for anyone who does not anticipate dying with or donating their highly-appreciated portfolio investments, harvesting 0% capital gains (to avoid 15%+ rates in the future) will generally be superior (to ordinary income harvesting at 10% or 12% when the household would likely “just” increase to the 22% tax bracket in the future). Especially since partial Roth conversions (when there are also any capital gains present) can trigger the capital gains bump zone (making those conversions especially unappealing).

Once the 0% long-term capital gains bracket is crowded out, though – e.g., for those households that already have too much in Social Security benefits, pensions, passive income, Required Minimum Distributions, or other income sources, and are no longer exposed to the AMT bump zone – it again becomes more appealing to conduct partial Roth conversions, as harvesting retirement accounts at the 22% or even 24% tax rate, to avoid the 32%+ brackets (an 8% to 10% increase) will generally be more appealing than “just” avoiding the 3.8% capital gains increase that occurs as the capital gains rate rises in the future. And in the most extreme cases, it may even be appealing to harvest partial Roth conversions at 32% or 35% tax brackets just to avoid the very top (37%) tax bracket in the future… while again being mindful of the upper capital gains bump zone (that kicks in at $434,550 of income for individuals and $488,850 for married couples)

The bottom line, though, is simply to understand that while long-term capital gains stack in what is otherwise a favorable manner on top of ordinary income – with deductions applied first against the ordinary income base – any increase in ordinary income can be subject to a form of double taxation, by both being taxed directly and causing the capital gains stacked on top to fall into higher tax brackets. Which will be even more common in the coming years, as the Tax Cuts and Jobs Act misaligned the long-term capital gains and ordinary income tax brackets, created many scenarios where ordinary income in one bracket still causes a bump zone in the capital gains rates.

Which means when evaluating marginal tax rates – the anchor for any long-term tax planning – and trying to find the optimal tax equilibrium (to fill up low current tax brackets to avoid causing higher tax brackets in the future), it’s crucial to consider not just the tax brackets that apply to ordinary income, but the indirect effects of triggering additional capital gains taxes (the capital gains bump zone) on top!