Executive Summary

With last week’s “surprise” legislation that revealed Congress is killing the File-and-Suspend and Restricted Application claiming strategies for maximizing Social Security benefits, even those who weren’t previously aware of the strategies are now wondering whether it’s something to take advantage of before the new rules go into effect.

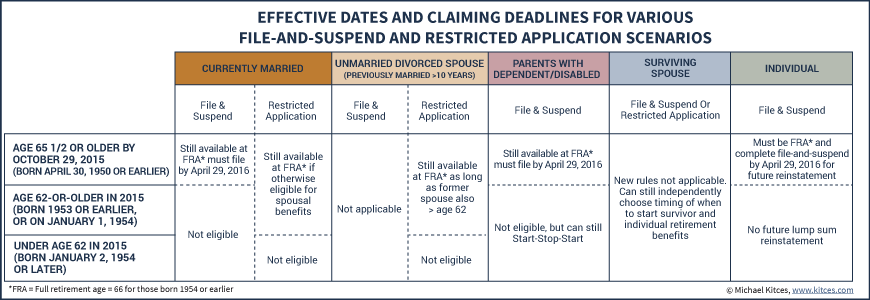

Fortunately, though, the new rules do not kick in immediately. Those who are already receiving benefits are not impacted at all. And those who are full retirement age – or will reach it in the next 6 months – will still have the opportunity to file-and-suspend before the crackdown takes effect after April 29, 2016. Furthermore, anyone who was born in 1953 or earlier (or January 1st of 1954) will still be able to do a Restricted Application for spousal (or divorced ex-spouse) benefits, even if the filing doesn’t occur until years from now.

Nonetheless, the next 6 months do mark an important transition period that merits a close look at Social Security claiming strategies, for the brief time window until the first "Social Security loophole" closer takes effect at the end of April 2016 - whether it’s an individual filing and suspending for a potential lump sum reinstatement in the future, a couple claiming spousal benefits, or a family claiming dependent or disabled child benefits while delaying individual retirement benefits until age 70. And for those “lucky” enough to be born in 1953 or earlier, only a few years remain to consider a Restricted Application, before that deadline ends, too!

(Michael's Note: This article was updated on November 5th at 8:37PM with updated details about the exact effective dates/deadlines and relevant birth-date requirements for file-and-suspend and restricted application.)

The Near-Term Expiration Of The File and Suspend Strategy For Married Couples

How File-And-Suspend Used To Work

The original version of File-And-Suspend allowed someone, upon reaching full retirement age, to file for Social Security retirement benefits, and then immediately suspend them. The fact that benefits had been filed for meant a spouse became eligible for spousal benefits (as spousal benefits cannot be claimed until the primary worker also files for benefits). However, the fact that benefits of the primary worker were subsequently suspended – and therefore were not actually received – meant that the original filer could still earn delayed retirement credit increases of 8%/year for waiting.

Example 1. John and Mary are both age 66, and have been married for 40 years, in a household where John was the primary breadwinner and Mary never worked outside the household. John is eligible for a retirement benefit of $2,000/month at his full retirement age, and Mary at her full retirement age will have no retirement benefit of her own, but will be eligible for a spousal benefit of $1,000/month, equal to 50% of John’s full benefit.

John wants to delay his benefits until age 70, increasing his benefit by 4 years x 8%/year of delayed retirement credits to $2,640/year (plus subsequent cost-of-living adjustments). Doing so not only boosts his own benefit, but increases the size of John’s survivor benefit that would be payable to Mary if John dies first.

However, waiting until John turns 70 means that Mary won’t receive any of her $1,000/month spousal benefits until then either, since Mary cannot get spousal benefits until John actually files for his own. And since there are no delayed retirement credits for spousal benefits, the extra 4 years of waiting just means Mary permanently loses those 4 years of $1,000/month benefits with no benefit in return!

To resolve this issue, John would File-and-Suspend upon becoming eligible at his full retirement age of 66. By doing so, Mary becomes eligible to claim her own $1,000/month spousal benefit (which she can receive in full, since she too is age 66), accumulating 4 years’ worth of spousal benefits she otherwise wouldn’t have received. (If Mary had been younger, she could have also claimed, but her spousal benefits would be reduced for starting early.) And John still gets the 8%/year delayed retirement credit increases for delaying his own benefits until age 70.

The fundamental point – with File-and-Suspend, John could allow Mary to get her spousal benefits, while still delaying his own benefits to earn the 8%/year delayed retirement credits.

How File-And-Suspend Will Work Now

Under the new rules in Section 831 of H.R. 1314, the Bipartisan Budget Act of 2015, when John suspends his benefits, he will suspend not only his own benefits, but any/all benefits payable to other individuals based on his earnings record. And since Mary’s spousal benefits are 50% of John’s benefits – and therefore are based on his earnings – then the entire File-and-Suspend strategy is effectively dead.

Now, if John were to file-and-suspend, he will suspend his benefits and Mary’s benefits, so no one gets any benefits. Which means if John wants to delay his benefits to earn delayed retirement credits, Mary will have to wait on claiming her spousal benefits, too.

Effective Date And Grandfathering Of File-And-Suspend

Under the final version of the Bipartisan Budget Act of 2015, the new limitations on File-And-Suspend will apply to anyone who requests a suspension of benefits more than 180 days after the effective date of the legislation. With the law being passed November 2nd of 2015, that means new suspensions occurring on April 30 of 2016 (when the deadline kicks in) will be subject to the new more restrictive rules (so file-and-suspend must occur on/by April 29th of 2016 to be grandfathered before the "Social Security loophole" is closed).

Accordingly, if John has already filed and suspended to give Mary access to benefits, the new legislation has no effect. There will be no adverse impact applied retroactively, as while there was an issue with retroactive enforcement in the original legislation, this was resolved with a subsequent amendment before the law was passed.

If John hadn’t yet reached full retirement age of 66, but would reach it between now and April 29th (i.e., he is already at least 65 ½, with a birthday of April 30 1950 or earlier, such that he will attain the age of 66 on April 29th of 1950 or earlier), he would still be able to file-and-suspend in that time window to give Mary access to spousal benefits while delaying his own.

However, if John is younger than 65 ½ now – such that he isn’t age 66 and won’t be by April 29 – he will not be able to use the file-and-suspend strategy at all, as the request to suspend benefits starting next April 30th will suspend Mary’s benefits as well, defeating the entire point of the file-and-suspend strategy.

Notably, if John had planned to just outright file for his benefits and get them, he can still do so, regardless of these new rules. The changes only impact the strategy of having John file to give Mary access to spousal benefits and then suspend his own. If he wants to file-and-get benefits (rather than file-and-suspend them), he can do so under the existing standard rules for Social Security.

Individual File-And-Suspend To Get A Lump-Sum Retroactive Reinstatement Is [Also] Dead

While the primary function of the file-and-suspend strategy was to allow a spouse to apply for spousal benefits while the primary worker delayed his/her own retirement benefits, a secondary version of the strategy was relevant for individuals.

Specifically, the opportunity was that at full retirement age, an individual who planned to delay benefits until full retirement age anyway could choose to file-and-suspend. While doing so would earn the same delayed retirement credits that were available by just delaying outright, the fact that the individual filed-and-suspended meant that if he/she had a change of mind later, it was possible to retroactively claim all benefits going back to the date of the original suspension.

Example 2. Jeremy is an individual who plans to delay benefits until age 70. However, just in case, he chooses to file-and-suspend upon reaching his full retirement age of 66.

If Jeremy has no change in circumstances, he will receive benefits at age 70, with the same 8%/year x 4 years = 32% increase for delayed retirement credits he would have received otherwise.

However, if Jeremy finds out he has a terminal illness at age 69, such that delaying benefits will no longer be beneficial, he can request a retroactive payment of his benefits going back to age 66. This allows him to be paid retroactively in a single lump sum for the 3 years of benefits he previously suspended.

Notably, the normal rules for “retroactive benefits” don’t allow this; it’s only possible to file a retroactive claim going back 6 months. However, under the Social Security Administration’s operations manual guidance (POMS GN 02409.130) regarding a voluntary suspension of benefits, those who had suspended payments had the option to reinstate them for the current month, a future month, or any past month during the suspension period.

Thus, as illustrated above, Jeremy can effectively get a lump sum payment of prior benefits, not by claiming “retroactive benefits” but instead by requesting a reinstatement of benefits back to the original file-and-suspend date. (Of course, doing so also meant the retiree would be treated as having claimed at the earlier date in the first place, forfeiting any delayed retirement credits, so this was generally only appealing if there was a change of health that meant the retiree didn’t expect to live long enough to reach the Social Security breakeven period for delaying benefits in the first place.)

What changed under the new rules, however, was that the Bipartisan Budget Act of 2015 created a new Social Security Act section 202(z), which defines the rules for how voluntary suspension will work in the future (including “unsuspension” or resumption of benefits). And the new rules stipulate under 202(z)(1)(A)(ii) that suspended benefits can only be resumed in the next subsequent month after the request is made, or at age 70. In other words, the new rules don’t have the option to reinstate going back to a prior month, which effectively means the optional-lump-sum-reinstatement strategy is dead.

Of course, since the new rules for suspension of benefits only apply to requests for suspension after the effective date, anyone who has already requested a suspension of benefits, or who does so in the next 6 months (if you reach full retirement age of 66 within the next 6 months!), remains eligible for the strategy. Even if the request to resume occurs years from now, as long as the original suspension occurred prior to the effective date of the legislation (by April 29 of 2016), the opportunity remains. Any suspension that begins after the effective date, though, will not be eligible for a subsequent retroactive reinstatement.

On the other hand, it’s also noting that because the reinstatement of benefits backdated to a prior month only exists because the Social Security Administration currently allows it in the Operations Manual, there also remains a possibility that the SSA will change its own manual shut down the strategy, even for those who have already filed and suspended, in a similar manner to the crackdown that occurred on the withdraw-and-reapply Social Security strategy back in 2010.

Of course, for those who were going to delay either way, there is little harm to file-and-suspend within the next 6 months just in case it turns out to be relevant in the future (though doing so will trigger enrollment in Medicare, and the end of eligibility to participate in a Health Savings Account). But be cognizant the availability of this reinstatement rule in the future is not unequivocally guaranteed, even for those who have filed-and-suspended before the effective date of the new legislation.

The End Of “Claim Now, Claim More Later” Restricted Application Strategies For Dual-Income Married Couples

How Restricted Application Used To Work

While the role of file-and-suspend was to allow someone else to get spousal benefits while the primary worker delayed his/her own benefit, the purpose of restricted application was for someone to get their own spousal benefit while delaying their own individual retirement benefit.

Example 3. Continuing the earlier Example 1 of file-and-suspend, imagine instead that Mary did spend some years working outside of the home, generating her own retirement benefit of $1,100/month. And because there’s limited benefit for both spouses to delay, Mary decides to start her own benefits now at $1,100/month, while John continues to delay.

The planning opportunity here is that John can file a Restricted Application to receive just his spousal benefit, and delay his own individual retirement benefit. This would allow John to receive his $550/month (which is 50% of Mary’s benefit) in spousal benefits for the next 4 years, and then switch to his own individual retirement benefit later. And since he doesn’t get any of his own individual retirement benefits along the way, they still earn an 8%/year delayed retirement benefit increase for 4 years, so when John switches back to his own benefit at age 70, it will have been boosted by 32% to $2,640 (plus subsequent cost-of-living adjustments).

Thus, while file-and-suspend was about allowing Mary to get a spousal benefit while John delaying his retirement benefit, restricted application is about John getting his own spousal benefit while delaying his own retirement benefit (and presuming that Mary is already getting her benefits as well).

A related Restricted Application strategy would even combine the two approaches.

Example 4. Continuing the prior example, instead of having Mary file for benefits and John file a restricted application for $550/month, John could file-and-suspend and let Mary get 50% of his benefit. Of course, there’s not much reason for Mary to claim a $1,000/month spousal benefit when she’s already eligible for a $1,100/month retirement benefit of her own, since upon filing for both benefits Mary will only receive whichever is higher, not both.

However, if John files-and-suspends, Mary can file a restricted application herself, receiving the $1,000/month spousal benefit from John while delaying her own. This way, Mary can delay her own benefit to earn the maximum 32% increase for delaying – pushing her $1,100/month benefit up to $1,452/month – and also get $1,000/month along the way until she switches back to her own benefit. And because John filed-and-suspended, he will get 32% of cumulative delayed retirement credits on his benefit, too.

Ultimately, which of these strategies is superior – having John file a restricted application, or having John file-and-suspend so Mary can file a restricted application – will depend on how long each of them lives. Nonetheless, the fundamental point of Restricted Application was/is to allow one spouse to claim spousal benefits while simultaneously delaying his/her own individual retirement benefits.

On the other hand, it’s also worth noting that because a Restricted Application is all about claiming a spousal benefit based on the other person’s retirement benefit, while also delaying your own retirement benefit, it’s only relevant for dual-income couples who each had enough in earnings to be eligible for a Social Security retirement benefit in the first place. For a single-income household, a Restricted Application is not relevant, only File-and-Suspend.

How Restricted Application Will Work Now

Under the new Section 831 rules of the Bipartisan Budget Act of 2015, when either John or Mary files for benefits, they are deemed to file for both individual and spousal benefits. And under the standard rules for Social Security benefits, anytime someone applies for multiple benefits they simply receive whichever provides the biggest benefit check (i.e., the larger benefit simply overwrites the smaller one).

In other words, there will no longer be such thing as applying for just one benefit and switching to the other later. Instead, for better or worse, either all benefits start earlier, or all are delayed later.

Effective Date And Grandfathering Of Restricted Application

In the case of Restricted Application, the effective date for the new rules is a bit different.

For those who turn age 62 or older this year – in essence, those born in 1953 or earlier, or someone born on January 1st of 1954 who technically "attains" age 62 as of December 31 of 2015 under POMS GN 00302.400 – Restricted Application is grandfathered under the current rules. Which means if you’re already receiving a spousal benefit under restricted application, you can continue to do so. And if you’re not receiving a spousal benefit yet, but planned to file a restricted application for it in the future, you can still do so – even if your filing for restricted benefits wouldn’t have happened until as late as 2019 when today’s 62-year-olds finally reach full retirement age.

On the other hand, for those who are under age 62 this year – i.e., born January 2nd of 1954 or later – there will simply no longer be any opportunity for doing a Restricted Application, now or in the future. Instead, a spouse eligible for spousal benefits will be required to file for all benefits, or wait on all benefits.

Notably, though, the entire question of filing a restricted application for spousal benefits is a moot point until the other member of the couple has already filed for benefits. In the next 6 months, that other member of the couple could file-and-suspend for benefits to activate the spousal benefits; beyond that point, while a restricted application may be possible, it can only occur if the other member of the couple files-and-gets benefits.

Impact of the New Rules On Divorced/Ex-Spouse Benefits To “Claim Now, Claim More Later”

In the case of a divorced spouse, file-and-suspend was not relevant, since the divorced spouse is eligible for a full spousal benefit at full retirement as long as his/her ex-spouse is at least age 62 (regardless of whether that person has filed for benefits).

However, filing a restricted application to obtain the ex-spouse spousal benefits while delaying individual benefits was an effective strategy to maximize retirement benefits while obtaining some (ex-spouse) benefits along the way.

This version of the “claim now, claim more later” strategy remains available under the new rules, but only for those born in 1953 or earlier (or on January 1st of 1954) who are grandfathered under the budget legislation. Thus, for those who are already claiming ex-spouse spousal benefits, or were born on January 1st of 1954 or an earlier year and planned to claim ex-spouse spousal benefits in the future, the option to claim spousal at full retirement age and delay retirement benefits until later remains available.

For those born on January 2 of 1954, or later, there will no longer be any option to delay individual retirement benefits while claiming an ex-spouse’s spousal benefit. Instead, a divorcee must either claim all benefits (both spousal and retirement) and receive whichever is higher, or wait to increase the individual retirement benefit and claim none until then. The claim-one-and-switch strategy will no longer be available.

A Potential Wrinkle For (Vindictive) Divorced Spouses

One significant caveat and complicating factor of the new rules is that while file-and-suspend was not normally relevant in divorced spouse situations, the new crackdown on suspended benefits may have unwittingly made it relevant.

The issue is that under the new Social Security Act section 202(z)(3)(B), when someone suspends a benefit “no monthly benefit shall be payable to any other individual on the basis of the [worker’s] wages and self-employment income.” This is the provision that eliminated the traditional form of file-and-suspend, by stipulating that when one person in a couple suspends benefits, the spousal benefit based on his/her record will also be suspended.

However, the reality is that an ex-spouse’s spousal benefit is also a benefit paid on the basis of the primary worker spouse’s earnings record. Which means while the reality is that while a divorced spouse didn’t need the other spouse to file for benefits to be eligible, a former spouse who suspends could potentially cause the divorced ex-spouse to lose access to benefits as well.

Example 5. Charlie and Betsy are divorced, after having been married for 10 years, and are currently unmarried. As long as Charlie is at least age 62, Betsy is able to file for an ex-spouse’s spousal benefit at her appropriate age, which wasn’t changed under any of the new rules of the budget legislation.

However, under the new rules, if Charlie plans to delay benefits until age 70 anyway, he could go into the Social Security Administration at age 66 (after the effective date of the new legislation), and file-and-suspend just to be vindictive and prevent Betsy from getting her ex-spouse’s benefits. After all, the new rules stipulate – as quoted above – that once effective, when Charlie suspends, “no monthly benefits shall be payable to any other individual [such as an ex-spouse] on the basis of [Charlie’s] wages and self-employment income.” In other words, while Charlie doesn’t have to file to give Mary benefits, Charlie’s suspension may potentially suspend his ex-wife’s benefits.

This was almost certainly not an intended outcome of the legislation, and may be within the Social Security Administration’s control to be fixed. If not, though, it may require subsequent legislation from Congress to further amend the Social Security Act to prevent this undesirable outcome. Either way, it will not matter until the new rules take effect after April 29 of 2016, so there is at least a 6-month period for the issue to be resolved.

The (Non-)Impact of the New Rules On Survivor Benefits (Including Divorcee Survivors)

When one member of a married couple passes away, the survivor is eligible for a survivor’s benefit (also known as a widow or widower’s benefit), equal to 100% of the decease spouse’s benefit. The rule also applies to a divorcee whose former spouse has passed away, as long as the couple was married for at least 10 years, and the divorcee remained unmarried until age 60.

As with any/all Social Security benefits, in the event that a surviving spouse claims multiple benefits – such as a widow’s benefit and his/her own individual retirement benefits – only the higher of the two is paid, not the cumulative total of both.

However, surviving spouses have a choice about when to claim each – the widow’s benefit and his/her own individual retirement benefit – and the new budget legislation does not change these rules.

As a result, a surviving spouse still has the flexibility to choose whether to begin widow’s benefits as early as age 60 or as late as full retirement age (at age 66), and also can choose whether to start his/her own retirement benefits as early as age 62 or as late as age 70. In both cases, starting earlier than full retirement age results in a reduced benefit, and with retirement benefits delaying past full retirement age still earns delayed retirement credits. But either way, the surviving spouse can choose independently when to start one and then the other.

Start-Stop-Start And File-And-Suspend For Parents With Dependent Or Disabled Children

When someone claims individual Social Security retirement benefits, an additional payment of 50% of his/her Primary Insurance Amount is also payable for each dependent child in the household (including biological and legally adopted children, as long as the child is unmarried and under the age of 18). The rules also apply to disabled children with no upper age limit, as long as the disability started before the age of 22. Furthermore, an “early” spouse’s benefit is also available to a spouse under age 62, if he/she is a parent caring for a disabled child (of any age) or a young child under the age of 16. These payments collectively are subject to a maximum family benefit, which varies between 150% and 180% of the primary worker’s full retirement benefit.

Because these dependent and disabled child benefits apply only once an individual has actually filed for benefits, the claiming of such benefits was eligible for the file-and-suspend rules. Thus, someone at full retirement age could file-and-suspend to activate dependent and disabled child benefits (in addition to spousal benefits), while delaying his/her own benefits to age 70 to earn delayed retirement credits.

Given the crackdown on file-and-suspend, though, only parents who are at least 65 ½ by November 1st (such that they reach full retirement age of 66 by the end of next April) will be able to pursue this file-and-suspend strategy at their full retirement age (but must file after full retirement age and before the new rules take effect!).

For younger parents who won’t be full retirement age until after the effective date, the only option will be to either start all benefits – including both retirement, spousal, and dependent/disabled child – or delay all benefits.

On the other hand, since the rules for voluntary suspension of benefits at full retirement age remains in effect, the option remains to engage in the “Start, Stop, Start” approach, where a parent starts Social Security benefits early to claim the full family benefits (including dependent/disabled child benefits), and then suspends benefits at full retirement age. Doing so will fully suspend all family benefits beyond the effective date of the legislation, but if the children are old enough to be over age 18 by then, it may still be appealing to claim full family benefits for a period of time (starting at age 62), then stop benefits to earn delayed retirement credits at 66, and then resume just the increased retirement benefit (and also the spousal benefit if available) at age 70.

A 6-Month Transition Period Until The File-And-Suspend Effective Date Deadline

Ultimately, the fact that the final version of H.R. 1314, the Bipartisan Budget Act of 2015, left a 6-month “transition period” for file-and-suspend means any/all couples who have a member that either already reached full retirement age, or will in the next 6 months, needs to carefully evaluate whether a file-and-suspend strategy makes sense or not. Because once the time window has passed, any subsequent voluntary suspension will be subject to the far-less-favorable new rules.

For those who are at least 65 ½ but were born in 1953 or earlier (or on January 1st of 1954!), the window for filing a restricted application for spousal benefits (including a divorced ex-spousal benefit) remains available for a few more years, though the ability to coordinate that strategy with file-and-suspend will still be over in 6 months when this proclaimed Social Security loophole closes in April 2016.

And for everyone else in the long-term future, coordinating the benefits planning of a couple will remain relevant… but unfortunately, with far fewer tools in the strategy toolbox to maximize those benefits!

So what do you think? How are the new rules impacting your claiming strategies and decisions with clients? Are you finding any new/unique scenarios coming up? Please share in the comments below!

Isn’t the date May 1, 1950 to determine eligibility for suspend, not 1949?

I had the same question. There might be a flaw or two on the dates in the chart, but wow, what a helpful article

Oy, yes, that’s what I get for working on this late at night tired on an airplane. :/

Will update with the proper birth year math shortly!

– Michael

Michael –

This is extremely helpful. I am still unclear on one particular piece. Take Example 4 with John and Mary: if John is 66 (or will be by April 30th) and Mary is 64, what would happen if John filed and suspended by April 30th? Would this then allow Mary, upon her FRA in 2017, to file for her spousal benefits while delaying her own? Or do they both have to be 66 by April 30th for this to work?

Thank you,

Ricky

Michael – have you been able to get any clarity if the above scenario would be possible?

This is the question on several minds…<iMichael K, can you please clarify?

Why does File & Suspend trigger enrollment in Medicare?

Apparently it doesn’t. I spoke with a person at Fidelity retirement and with a person at SSA. Both said that enrollment in Medicare is totally separate and not required by filing and suspending. I am working and covered by an employer sponsored health plan, so would not want to lose that coverage at this time. I am past FRA and may take advantage of filing and suspending until my wife reaches FRA. Too bad Michael didn’t respond to this question with some clarification. There must be some situations where it may apply (?)

Have you seen the actuarial calculations used to make this decision? The short time frame is quite disruptive and unusual. Most of my clients are middle class using file-and-suspend to fund the survivor in the distant future. This rule is turning their reasonable margin of safety plans into barely scrape by plans. Certainly creating a lot of redesign for their planner (at no fee).

Assuming all requirements are met under the new law, if husband (age 66 and currently drawing) suspends and then dies before age 70, can wife (age 67 and currently drawing spousal benefit) draw survivor’s benefit equal to husband’s full benefit computed based on DRCs earned up to date of death?

If husband is currently receiving work record benefits and wife is receiving spousal benefits, will wife lose her spousal benefits if husband suspends his work record benefit after April 2016? Both are at FRA.

Is “suspending” the same as “delaying” as it applies to divorcees? So if one spouse is simply delaying benefits to 70, will the ex be able to get spousal benefits while the delay is occurring?

I am 61 and my husband is 63, so we will not be able to take advantage of the file-and-suspend/restricted application method of collecting SS benefits as we have planned for for several years now. Thank you Congress and Obama. My question is this–if I file at FRA, even if my husband has not filed yet, am I deemed to have filed for both my own and spousal benefits? Or can I file at 66, receive 2 years of my own benefits (smaller than my spousal benefits), then switch to spousal benefits after my husband files at age 70?

Thanks.

I still disagree with a birthdate after May 1, 1950 being the disqualifying factor in file and suspend. The legislation makes April 30, 2016 the deadline for “submission” of a request for suspension under the old rules. You can file for benefits and also submit a request for suspension up to four months before they are to take effect. Unless there is some part of the act that I’ve overlooked, anyone who is eligible to **submit** a request for suspension before April 30 can be grandfathered in – and that includes people born in May through August 1950.

Please correct me if I am wrong.

My understanding is that it is when you file for benefits not when they are set to be received so the May 1, 1950 date would be the cutoff.

I don’t follow you. What do you mean by “it is when you file for benefits?” What is the “it” you are referring to? And why does that make May 1 the cutoff?

Bottom line seems to be you need to turn age 66 by April 29, 2016 otherwise you are not grandfathered in.

POMS GN 02409.110 (https://secure.ssa.gov/poms.nsf/lnx/0202409110) states that someone must be full retirement age to request a voluntary suspension.

The fact that you can request the benefits up to four months in advance doesn’t mean you can request the suspension four months before full retirement age when POMS is pretty explicit that you must BE full retirement age at the time of the request.

If you can show anything from POMS or other Social Security administrative guidance to substantiate that they will accept and process a request for voluntary suspension four months before full retirement age, I’m all ears. But I can’t find anything to substantiate that it would be permitted.

– Michael

I don’t think that publication necessarily means that you can’t submit a request for suspension a couple of months ahead of time to take effect on your (future) FRA date when you you specify that in your benefit filing. Since I can’t think of any reason why there would have been an issue with it one way or the other before now I’m not surprised by that.

I’m curious: in the real world, are people currently prevented from combining an early request for a future benefit start date with an advance request for suspension taking effect at the same time? I hadn’t heard that, and it seems inefficient if true. To the contrary, I’ve seen references elsewhere to doing it that way – e.g., file your request for benefits online before your birthday to take effect on that date and request suspension in the “remarks” section of the online form or simultaneously send a registered letter with the request. As best I can tell there is no express reference to submitting a suspension request to be applicable on the future date of benefit start anywhere in the regs or the handbook – one way or the other.

Steve,

That book literally IS the operations manual for Social Security. If the book says they can’t process the suspension until full retirement age, then they can’t process it until full retirement age.

Perhaps in the past the SSA was flexible on this since it didn’t matter, but in a world where Congress explicitly wrote a law telling the SSA to stop processing suspension benefits under the old rules as of a certain date, I don’t see why they would have any reason or obligation to honor your strategy here.

If you can get an authorized representative of the Social Security Administration to agree to your interpretation, I’m all ears. But I don’t see how the existing Operational Manual and Social Security Act provisions would create any obligation for the SSA to permit this.

– Michael

I turn 66 on 30 Jan 2016, so I’ll be able to file & suspend as planned.

My question is: can I do the file & suspend on-line or only in-person at a SS office?

Thank you Michael for this concise summary of the effects of the new law! What Steve Condie (below) is suggesting about the actual deadline for “submission” of a request to suspend could make a difference to hundreds of people who are born in May through August of 1950 and could start the process of filing up to four months in advance of their FRA, If they submit their applications within the 180 day deadline it seems possible they too could be grandfathered in – even though their actual FRA falls outside the window. How can we get a definitive answer to this question?

Can my wife claim at her FRA on her own earnings record, and then step up to a spousal benefit when I file at 69 or 70?

I was born on August 24, 1950. My wife turned 45 on 11-3-15. Our adopted daughter was born on 6-25-13. I reach FRA of 66 on 8-24-16. My plan was to file for Social Security and submit a request to suspend within in the four month window, prior to reaching 66, and receive benefits for both my wife and daughter, until I reached 70. From then, to continue to receive benefits for all three of us, until our daughter is 16. After that, to receive benefits for my daughter and myself, until she is 18. If Steve Condie and Laura are correct, I’ll have from April 24th to April 30th to make my submission and be “grandfathered in” for file and suspend. Could anyone verify if this is correct?

I am 66 and my wife is 63. If I were to file and suspend before 4/30/16, could my wife wait until she reaches 66 in 2018 and then file for her spousal benefit, or must she also file before 4/30/16 (and thus receive a reduced amount)?

Michael, using your John and Mary examples, what if John, who is past FRA, files-and-suspends before the April 30th deadline so that he can let his own benefit build until age 70. Mary, whose own benefit will never be as large as her spousal benefit, doesn’t reach FRA until a couple of months AFTER the April 30 deadline. Will John’s filing-and-suspending do her any good? That is, when she reaches FRA in July, will she be able to begin getting the spousal benefit because John applied within the window, or was she born slightly too late? If she’s out of luck for that, can she start claiming her small benefit in July, then switch over to the spousal benefit when John begins claiming? If so, does she need to do any special paperwork to achieve that? If she’s out of luck on that one, too, does that mean their only choices are (1) for John to start receiving benefits when Mary reaches FRA in July so that she can start receiving the spousal benefit, even though they”ll get less per month than if John could wait until 70, or (2) for Mary to receive nothing until John starts at 70? Thanks!

I will be 66 before the deadline, but husband is a year younger. He intends to keep working.

Can I still File & Suspend, or File & Draw, either one—and have him file for a spousal benefit (age 65) while he waits and files on his own record at age 70 (in 2021)? Or is that option gone?

This is my question too. I’ve searched extensively and can’t find clarification on this age related question. Please, please answer.

My husband is 64 now and receiving social security, I will turn 66 in June 2016. Can I file a restricted application for a spousal benefit in June 2016 to allow my benefit to grow even though my husband will not be 66 yet?

I am a 65 yr old surving spouse receiving his benefits since age 60. I was told that when my actual social security benefits exceed those that I receive now, I could switch to my benefits. Will the new changes with 2016 budget affect that ruling?

Thank you Kathy

Michael, you state “if you’re not receiving a spousal benefit yet, but planned to file a restricted application for it in the future, you can still do so – even if your filing for restricted benefits wouldn’t have happened until as late as 2019 when today’s 62-year-olds finally reach full retirement age.” My wife and I are 62 now, will reach FRA in four years. My wife will file for her own benefits sometime in the next four years. Can I still file the Restricted Application for spousal benefits at that time, or do I have to file it now with a 2019 effective date in order to be grandfathered in? Thanks – Cliff

Cliff,

You CANNOT file a restricted application now, because you’re not full retirement age. If you tried, you’ll be deemed to have filed early for everything.

Because you are already age 62, you are grandfathered. Just go in to file a restricted application when you’re full retirement age and otherwise eligible. It’s as though the new law never existed for you when it comes to restricted application.

– Michael

Michael, I have a question about combining two strategies…. Last month a friend reached FRA and began taking a restricted application of her ex-spouse’s benefit. Since she also qualifies for file and suspend (for at least 6 more months), can she does this while collecting the ex-spouse benefit? The goal would be to to have the lump-sum retroactive benefit available as a backup.

Michael, do we need to divorce?

Mary is FRA and is collecting a $700 benefit based on FRA.

Her spouse John is 63 and plans to start collecting social security at age 70 (projected $2500 FRA / $3300 @ 70). When John turns 66 (FRA) he can file a restricted application for a spousal benefit based on Mary’s work record ($350). At that time (John FRA), will Mary’s benefit automatically be adjusted upward ($1250)? If not, would it be adjusted upward if they were divorced? If so, when should they use divorce as a strategy? Could they (do they need to) remarry @ John turning 70 to regain survivor benefits?

Just to clarify: My husband is 66 now. I am 64 (dob 9/21/51) and still working. We were planning on him to file and suspend (it sounds like he would have to do this in the next 6 months now) and I would take the spousal benefit when I turn 66 (i don’t think I can take that benefit earlier without lowering my own benefit). He then would collect his full retirement when he turns 70 and I would take mine at 70 also. Additionally we have a 24 year old disabled child currently on SSI. When could she take a benefit from him? Would file/suspend lower our disabled child’s benifits in future years, as we were trying to benefits for her for the rest of her life. BTW thank you for all of your information- very helpful!!

Michael, would you please help clarify my case so I know exactly what to do when I have my appointment with s.s. in Dec. The other day I was on hold for hours and never received an accurate answer form the agency’s personnel. I will be 65 in Feb., have been divorced for 7 years after a 35 yr. marriage,, and am single. I would like to collect a portion of my ex-spouse’s s.s. and delay collecting mine until age 70. Please advise what forms I should use and if I should do this asap. I was going to wait until I was 66, but now think I should do immediately. I really would appreciate your advice. It is difficult to understand how to proceed on my own. Thank you.

I am still confused: I am 63 and my wife is retired. We are both waiting until 66 to collect Social Security: I plan to keep working after 66 and was planning to file and suspend at 66:: Can I still do that?

No. File and suspend is gone as of April 30th of 2016, and you wouldn’t be doing a file-and-suspend until 2018. So it will not be an option for you.

if your wife starts benefits early and you want to take 50% of HER benefit at your full retirement age while delaying your own, you CAN do that because filing a restricted application for spousal benefits remains available for those born in 1953 or earlier.

– Michael

I wonder why they would do that. It seems they will actually deplete the SS trust faster that way. I will get whatever the maximum social security is at 66 (Actually Jan 1 for the year after I turn 66) and I would have done a file and suspend but kept on working. As it is I will probably still keep on working (I love what I do–it is essentially entertainment I get paid for) but take full SS at 66. Since I am the higher earner by a significant margin, 50% of my wife social is not that significant a dent in the SS fund.

If they had left file and suspend in place I would have kept on working, still contributed to my retirement accounts and delayed taking social security until 70. I would have had more money in my IRA, the Govt would get more tax money (due to RMD) from me and they would also save on Social Security.

It does not make sense financially.

In the long run Social Security’s trust fund lasts longer when people retire early. Delaying benefits is more profitable for Americans on average given today’s life expectancies (which means more damaging to Social Security’s trust fund projections). So if you decide to start your full benefits at age 66 instead of age 70 given the changes, it will improve Social Security’s financial strength. :/

– Michael

Chris, I’m a bit confused when you say… “I will get whatever the maximum social security is at 66…”. You do know that every month you delay past 66 (assuming that is your full retirement age, i.e. born before 1954) that you will get a 2/3% per month increase (8% per year) for every month that you delay past 66. Waiting to age 70 to file (or filing and suspending if you can do so before the end of April) will increase your benefit to 132% of your age 66 amount. Not only that, but since you are the higher earner, if you expect your wife to outlive you, this also increases here survivor’s benefit by 132% after your death. Claiming at 66 seems to be a poor strategy if you plan to continue working. Yes, you wife would collect spouse benefits by filing then, and you may lose that now if you can’t file and suspend before May, but waiting till 70 may still be your best long term bet.

According to Social Security I have already qualified for the maximum level benefit and my work from now on does contribute to FICA but I am already at the max, it doe snot benefit me.

One way of looking at social security is to view as a that increases by 8% per year until til I start taking it. If I wait three years I will be 2642 (or what ever the max is) if I wait till 70 I think it is around 3698 or 44376 annually.

If I cannot file and suspend: I’ll take SS at 66 I will have an additional 2642/month in income and if I( continue working I will still contribute to my Roth. The extra SS income I receive from 66-70 is 158520 (ignoring inflation). If then at 70 I start receiving the 44k roughly it would take me 16 years to make up that difference (ignoring the time value of money and inflation) and historically men in my family die very close to 70. Even the one that lived very healthy life styles don’t make it to 80. Of course at 70 1/2 I will hit the RMD (required minimum distributions) and will be forced to start withdrawing from my retirement accounts.

If “file and Suspend” is an option for me, I would do that instead.

At the age of 66 between my SS and my wife’s we will have an extra 3000/month or more extra cash which I plan to basically have fun with and probably invest for the grand babies education.

Michael, my husband is currently collecting SS as he is 69. I turn 66 in July 2016. I was going to file and suspend by SS and apply for spousal benefit. Can I still do this with the rule changes? Even if i can no longer get a spousal benefit, can I still file & suspend? Does it suspend until 70 1/2 or can I change the distribution to sooner?

Requesting a spousal benefit is NOT “file and suspend”. It is filing a Restricted Application for Spousal Benefits.

And since Restricted Application still applies for everyone born in 1953 or earlier, the new laws have zero impact on you. You can still do a restricted application for your spousal benefits next July as you planned originally.

– Michael

So Michael, if I am 65 and just started claiming ss benefits one year early can I still switch to claiming spousal when I turn FRA next august 2016 if my husband who is 66 files and suspends before the deadline in April 2016, since he has not already done so. Thanks

can I switch from collecting benefits to spousal benefits

Michael, if my husband who is 66 files and suspends within the next six months since he has not yet done so, can I change my benefits which I just started collecting early at age 65, to spousal benefits at my FRA 66, next august 2016, or should i do so now.

So Michael, if I am 65 and have already started claiming SS can I still switch to claiming a spousal when I turn FRA next august 2016 if my husband who is 66 files and suspends before the deadline in April 2016.

Michael, thanks so much for your help. Can you please clarify one thing? I am 67 and have been waiting to file at 70. My wife is 56 and I had always figured on having her taking spousal on my benefits when she gets to FRA at about 67. If I knew that taking mine now would grandfather us so she can still get my spousal at FRA, I would consider this. But do I understand this right, that it doesn’t matter about my age right now but rather her age and since she was born after 1953, then she will not be eligible no matter what I do now?

I am in the lucky group who will turn 66 in April 2016. My wife will turn 66 in May 2016. My questions is, when EXACTLY should I start the application process online to get the max benefits? Now, in a month ? Within 3 months of turning 66 ?? The day after I turn 66 ??? Thanks

Thank you Michael. This is the most comprehensive information on the ss changes. Quick question, if a wife will be 66 next year, and her husband is 62 and her own ss will be less than her spousal. As long as her husband hasn’t filed, can she take her own ss at 66, and then when her husband files at his age 70, switch to her spousal. We thought that this doesn’t count as a restricted application since he isn’t filing for another 8 years.

Michael, I just returned from my local Social Security office where I received some startling news. First the facts. I will be 66 on Nov 29 and my wife is 62. We are both retired but we both worked until retirement. The plan was to have me file and suspend until age 70 in order to maximize my benefits. Then when my wife turns 66 she will take her spousal benefit until she turns 70. However the Social Security person would not allow me to file and suspend unless my wife took the spousal benefit NOW. He even graciously checked with his supervisor who confirmed his interpretation. He also said that if I applied to file and suspend my application would be denied. One can only file and suspend if someone (e.g. a spouse) receives a benefit. Well, this runs counter to all the information I have read on multiple web sites so I phoned Social Security’s 800 number. I presented my same information, and she said the exact same thing as my local SS person.

Upon further questioning, my local SS person said SS headquarters in Maryland had not issued any new rules concerning the new law except that for now (and maybe forever) the file and suspend and restricted application strategy is no longer available to us. As of now people like me and my wife are not grandfathered in. He advised me to keep checking the SS web site for the SS administration’s interpretation of the new law as there may be grandfathering in.

Can you advise me? Thanks,

Michael J

Michael J,

I’m in a similar situation, so interested to see a reply from Michael K if he supplies one. However, in your case, it may not make much difference and here’s why: you will turn 70 within a few months of when your wife turns 66. When you turn 70, you can file for your benefits. At that time, your wife can file a restricted application for spousal benefits (because she is grandfathered in, being already 62). So once you turn 70, your wife can start to receive spousal benefits, even though you never suspended. What you would lose by not being able to file and suspend now (due to the response from the SSA that you described) is the spousal benefit that your wife could have received under the old law, for the period between the time she turns 66 and the time you turn 70. For example, if her birthday is 6 months before yours, then that would be 6 months of spousal benefits that she would lose. The key point is that it would not be 4 years of spousal benefits lost, as you may have thought when you were denied permission to file and suspend now.

In my own case, being denied the option to file and suspend now would result in a loss of 15 months of spousal benefits. So I hope the experience that you had doesn’t turn out to be the final word.

Matt

Matt, Michael,

We are in a similiar situation. My husband is 67 and waiting until he is 70 to withdraw. I will not be 66 for another year (November 2016). Our plan was for him to file and suspend before April 29, 2016 and for me to file a restricted application for spousal benefits after my 66th birthday in November of 2016 to allow my own benefit to maximize.

My understanding is that I begin taking spousal benefits prior to my FRA of 66, I will permanently reduce my benefits due to not being FRA at the time spousal benefits began. Is that your understanding?

I am the higher wage earner so I do not want to take my benefit before age 70.

MxSx,

In the absence of a reply from Michael Kitces, this amateur will respond: It is also my understanding that filing for spousal benefits prior to age 66 will permanently reduce your benefits. That was the case under the old law, and since you are over the age of 62 now, the old law would still apply to you. As I see it, the possible scenarios are:

a) The optimistic view: That Michael J’s experience with his local SS Office will not prove to be the final word, and your spouse will be able to file and suspend before April 29, 2016, while you file a restricted application for spousal benefits in Nov 2016.

b) The pessimistic view: That the SSA will not allow your spouse to file and suspend without you simultaneously filing for spousal benefits. You don’t want to do that because you want to maximize your own benefits by filing at age 70. You should still be able to file a restricted application when your spouse turns 70 and starts benefits. That would be approximately 2 years of spousal benefits instead of 4 years under the old law. Or, if you need the money in the near term and are willing to forgo some later on, your spouse could apply for benefits at any time between the time you turn 66 and the time he turns 70 and you could file for spousal benefits at the same time. The later he does this, the more delayed benefit he will accumulate, and the less spousal you will receive.

In all of these scenarios, you protect your maximum benefit at age 70, as the higher wage earner, which is important for maximizing survival benefit later on.

We need more experiences of people trying to file and suspend now so their spouses can file restricted applications later. Then we can see what our options really are between now and the end of April. We have some time to wait and see how it unfolds.

Matt

The person at the Social Security office, and the supervisor, are both WRONG. This is a very common problem. I am 67 and my wife is 65. I filed and suspended effective the date of my FRA of 66. (I actually did it several months after I reached 66, but within the six-month retroactivity window.) I was going to file and suspend when my wife reaches FRA anyway, but I did it early in order to have the option to “unsuspend” if our personal circumstances changed after the six-month retroactivity window for regular filing. I got the same misinformation you got, and the person I talked to also checked with a supervisor. You will have to very nicely but assertively insist that your application be filed even if it could be denied. Mine was not denied, and neither will yours. You will also have to smile and act nice while being berated for making the Social Security employee waste time doing something useless. Just stay in your chair and make it apparent that you are not going anywhere until your application is filed. I had been warned beforehand this was likely to happen. This is so common that it was also suggested I print the following page from the Social Security website and take it with me:

https://www.ssa.gov/planners/retire/suspend.html

I did, and I showed it to the employee, but I cannot say whether or not it made any difference. What I can say is that I successfully filed and suspended effective August 2014 even though my wife is not receiving any Social Security benefit (spousal or otherwise) and has no plans to do so until she reaches FRA in July 2016. Good luck!

Matt, Sam,

Thank you both for clarifying file and suspend. Sometime after the new year I will again visit my local Social Security office with a “nice but assertive” determination. Hopefully I will be able to successfully file and suspend whether under the old rules or the new rules.

Michael J

Michael,

My husband is 67 and waiting until he is 70 to withdraw. I will not be 66 for another year (November 2016). Our plan was for him to file and suspend before April 29, 2016 and for me to file a restricted application for spousal benefits after my 66th birthday in November of 2016 to allow my own benefit to maximize.

The posts from Matt and Michael below indicate that SSA will not allow my husband to file and suspend unless I file for a restricted benefit at the same time.

My understanding is that I begin taking spousal benefits prior to my FRA of 66, I will permanently reduce my benefits due to not being FRA at the time spousal benefits began.

I am the higher wage earner so I do not want to take my benefit before age 70.

Please advise if my husband can file and suspend before the deadline without me filing a restricted appplication at the same time.

Thank you!

I know from personal experience that your husband can indeed file and suspend without you filing any application. He may have to be assertive because many Social Security employees are not aware of this. See my answer to Michael below for more information.

I am on social security disability. I was born 5/1953. My husband (born same year) in presently receiving his ss retirement benefit having initiated this at age 62. Our plan was when I reach FRA to “withdraw” my retirement benefit instead of letting it automatically convert…and file for my retirement benefit at age 70. In the meantime the plan was for me to take my spousal benefit until then. Will this still be possible for me?

I am 67 years old and I have been receiving ss for 4 years is there anything I can do to get more money?

I am no where near 62 nor 66. Can I still file prior to April 2016 for when I turn 62?

Jack,

No, I’m afraid not.

If you’re not turning age 66 by next April, file-and-suspend is simply gone and will never be available to you.

Similarly, if you’re not at least 62 this year – i.e., you were born in 1954 or later – restricted application will simply never exist for you. The new law effectively revoked/eliminated restricted application altogether for anyone born in 1954 or later.

– Michael

I’ve read several articles that state SS funding will being drying up within the near future, and by 2032 will only be able to pay out $0.77 on the dollar to recipients. In light of these projections what advantage would be gained by deferring the filing for my benefits when I reach FRA and waiting until age 70? It seems I might actually collect less by deferring if the projections are correct. Your insights and recommendations with regard to this question are most appreciated.

Cruisewinds,

If the payments shortfall is not resolved, you’re correct that the benefits will be haircut by about 23%.

But if you take early, your early benefits are cut by 23%. If you delay, the delayed benefits are cut by 23%. So you’re cut either way. And the cuts wouldn’t apply for 15+ years. In practice, this still makes the math of delaying look pretty compelling. See https://www.kitces.com/blog/how-delaying-social-security-can-be-the-best-long-term-investment-or-annuity-money-can-buy/ for the long-term implied returns EVEN IF the cut occurs.

That being said, I’m not sure how realistic it is to plan for cuts. Politicians like getting re-elected. You don’t get re-elected by cutting benefits for what by then may be 80,000,000 senior voters.

Remember this isn’t the first time we’ve had a problem due to the imbalance of workers to retirees. We faced this 30 years ago as well. The shortfall was looming in 1983. We got within WEEKS of it happening, and then “fixed” it. For another 50 years. That was when we began adjusting the full retirement age from 65 to 67, and a number of other adjustments to extend another 50 years. Given the normal political process, I would anticipate something similar. We’ll “fix” it… sometime in the early 2030s. :/ The math isn’t hard – we know EXACTLY what to do. It’s just a matter of deciding which levers to pull to make the fix, which isn’t very politically appealing until it’s “necessary”. :/

– Michael

Thanks for your reply Michael. I am one of the fortunate few who will reach FRA in March and was leaning toward the file-and-suspend option so that we could change my wife’s current payments to spousal benefits at that time. (She had limited earnings so we started her SS at age 62, with the idea of then filing for spousal benefits when I hit FRA) Your insight regarding a potential 23% across-the-board is compelling, as well as the motivation for a political fix before the “fit-hits-the-shan” and Congress has to deal with the onslaught of angry seniors 🙂

*REPOST* I’ve read several articles that state SS funding will begin drying up

within the near future, and by 2032 will only be able to pay out $0.77

on the dollar to recipients. In light of these projections what

advantage would be gained by deferring the filing for my benefits when I

reach FRA and waiting until age 70? It seems I might actually collect

less by deferring if the projections are correct. Your insights and

recommendations with regard to this question are most appreciated.

I’m looking for information for my parents. My mother is 63, no longer working. My dad’s benefits will be at least double my mom’s. He will be FRA in September of 2016. He intends to work…pretty much forever. Can my mom file a restricted application & get her (much smaller) benefits now, and then step up to spousal benefits when my dad eventually files? Is that how it works? I had hoped they could do the file-and-suspend but it’s too late for that. Thanks.

With regards to the new File and Suspend rule – I am a divorcee (married 32 yrs), whoes X passed away before he starting drawing SS. I will reach FRA in Feb. 2017. Will I be able to fill and suspend my SS and draw off his SS until I turn 70 then draw mine?

Michael, Quite frankly I have never seen anything so confusing in my life. My local SSA office couldn’t even get it straight and we re still in a quandary about how, what and when to file. My wife is 65 (born 8/1950); I am 64 born 10/1951. We want to maximize benefits and both of us are retired but have not filed for any SS benefits except for my wife’s Medicare. I was the larger income earner and my benefit at FRA will be 44% more than my wife’s benefit at FRA. How do we maximize our lifetime SS benefit?

I am 66 today, 2/1/2016, and my wife will be 66 in July 2016. I understand that I have until 4/29/2016 to file and suspend. Can my wife wait until she reaches age 66 in July 2016 to file for her spousal benefit or must she file before 4/29/2016 to receive that spousal benefit?

Thank you.

We have a client that has filed and suspended. The spouse would like to claim 1/2 of her benefits at age 66 (in two years) but the SS office says he can’t claim 1/2 of her benefit because his benefit at age 66 will be more than 1/2 of her benefit. It would be good if he could claim1/2 of her benefit and let his benefit grow. Is this correct? Where can we find this rule?

What if Mary is 64? Can she receive benefits now without retiring now herslef? Must she wait until she is 66?

Iam 65 turning 66 in June of 2016. I will be taking SS benefits at 66. My wife is disabled and 64. When she turn 66 and disbility conferts to regular SS, can she file a restricted application and claim half my benefits and lets hers grow until age 70. Can I still collect my benefits ? There apears to be grand father and disbilty rule since we were born beore 1953?

If I 70 and my wife is 63, my understanding is that under the new rules she can claim spousal benefits when she is age 66 because I will am receiving benefits

I turned 66 in April 2016. I have not applied for retirement benefits and I never filled out a file and suspend document. I have a disabled adult son but he currently receives disability benefits under his father’s account. We were married fewer than 10 years. What would doing a file and suspend do for me and how do I do it? How would it potentially affect my disabled son? When I do reach 70, his benefits would probably increase because my benefits would be larger than those of his father. I understand that my son’s benefits are based on what my benefits would be at exactly full retirement age and he would not receive any additional benefits from my delayed retirement. Would file and suspend change this?

I would so much appreciate your advice in this matter because obviously time is of the essence!

I am turning 65 on April 6th. My own social security benefits are less than my husbands. It would clearly be to my advantage to receive half of his benefits. My husband has not filed yet for Social Security but he is already 67 – he would probably apply for benefits when he turns 70. I am getting conflicting information as to what to do. I went to the social security office in my town and they said I can’t do anything because I will not be of full retirement age for another year. My long term care rep (who has a certification for advising on social security) has said that is incorrect information: that my husband should get to social security to stop and suspend before the April 29th deadline because – if he does – I will still be able to receive 1/2 of his benefit. I would so much appreciate your opinion. Thank you.

I turn 66 in August of this year. My Monthly SS Benefit is 3-4 times higher than my wife’s Benefit. My wife turns 71 in March 2016 and is having health issues. Our plan was to use File and Suspend in August 2016 for me so she could receive a higher benefit. It appears to me that I will miss the window for File and Suspend even if I was to apply now, I’m out of luck based on timing.

Can someone please confirm. It appears my only option is to file for my wife’s Spousal Benefits 50%=about $350-400 per month. I am in good health, earning over $100k per year as an IT Project Manager and want to continue working until at least Age 68 or perhaps longer if health allows. Advice is welcomed.

Jim–has your wife filed for any benefits?

I am 66 years old DOB 10/1949. My wife is 62 DOB 4/1953

We had an office appointment with SS yesterday.

We were told by the worker and then her supervisor, that indeed I could file and suspend.

Which I did. But that my wife because she is 62 and not 66 (full retirement age) could not

file for half of my benefits. They said she could file for her benefits based on her earnings but not

based on my earnings as she was not 66. Were they correct? Can you site me to a regulation or

code?

Michael,

My husband and I have been married over 40 years and are living separately. I am planning to file for divorce soon. He is 67 years old, has never filed for his social security, and was planning to wait to age 70.

I will be 66 july 2016.

We have both been top earners for most of our careers.

He is willing to do “what is best” for me/both of us.

Is our best bet for him to ‘file and suspend’ now, and me to then file for spousal benefits on my July birthday, letting my benefits accrue? If we are still married but I have filed for divorce may I start my spousal benefits?

Is it better to wait and neither of us file until after the divorce is final (probably early 2017) and then both get “divorced spouse benefits” while our own benefits grow.

If he files and suspends, and then applies to re-instate his benefits after we divorce, does that impact my ability to continue to collect?

I and my wife are 67. We both are receiving Social Security now. Are we eligible to take advantage of this? If so, how?

Hello, my name is Miss Rosario, I’m from Bulgaria.I want to inform you

all that there is a spell caster that is genuine and real.I never

really believed in any of these things but when I was losing

Hector, I needed help and somewhere to turn badly. I found

consultant.lakuta spells and i ordered a LOVE SPELL. Several days

later, my phone rang. Hector was his old self again and wanted to

come back to me! Not only come back, the spell caster opened him up to

how much I loved and needed him. Spell Casting isn’t brainwashing, but

they opened his eyes to how much we have to share together. I

recommend anyone who is in my old situation to try it. It will bring

you wonderful surprises as well as your lover back to you. The way

things were meant to be you can contact the spell caster via email:

[email protected] he’s very nice and great. Miss Rosario and me via: +359876929306

I am 61 and my spouse is 64 and turns 65 in June 2016 but PIA is 66.

Could/Should she file a restricted application before the April deadline?

I plan to take my lower benefit at 62 and let her higher benefit delay to 70.

Thanks for any clarity.

Restricted Application has no relationship to the April deadline. The April deadline is only for File and Suspend, which you wouldn’t be eligible for at this time anyway, because neither of you are full retirement age of 66.

You will still be able to take your benefits at 62, and she will fill be able to file a restricted application at age 66, as though no change in the law ever happened. Because file and suspend doesn’t apply to you, and restricted application is grandfathered under the old rules for anyone born in 1953 or earlier (which is the case for your wife).

– Michael

I was 62 in 2015 but my wife is only 56, so I assume there is no reason to file a Restricted Application. Correct?

I am currently 64. I plan on working to age 70. My wife turns 56 in July. Do I do anything now? If I sign up and delay benefit, will my wife receive anything now, or does she have to wait until age 62?

Mr. Kitces, I have read this article over and over and it’s the best explanation I’ve read so far of divorced spouses filing for spousal benefits with the new law signed by President Obama Nov., 2015. There is one thing a co-worker and I disagree on in interpreting what you state about age of worker ex-spouse. I am a divorced spouse, have been for over 10 years and I turned 66 in August, 2016. My ex-spouse just turned 62 on April 9, 2016. As I understand it, I am grandfathered in to file a restricted application when I turn 66 (not sure the first date I can file, however), as I would like to wait until I’m 70 to collect on mine. Isn’t it correct that I can file for spousal benefits on his account for half his benefits and if his are higher, I am eligible to receive his half. My co-worker thinks I’m still not eligible because of the date he turned 62, that he had to have been 62 in April, 2015. Please advise which is correct. And if there any way for me to find out if his half is more than my whole BEFORE I file the restricted application. Thanking you in advance if you could answer this. We have looked and looked for clearer interpretation that definitely fits one or the other’s interpretation, to no avail.

I mean *turn* 66 in August

You are grandfathered into a restricted application because YOU had already reached the requisite age by the end of 2015.

Your ex-husband’s age simply determines when you are entitled to claim an ex-spouse’s benefit when you become eligible. Your eligibility itself is based on your age/birth year (including grandfathering treatment).

So yes, you will still be grandfathered into restricted application. Your husband could have turned 62 next year, you’d still be eligible and grandfathered. But you wouldn’t be able to exercise that grandfathered treatment until you there was a benefit you were entitled to, which again comes when your ex-husband turns 62.

– Michael

I began collecting social security at age 62, due to health considerations…it very little, cant live on it…can I file and collect more…born in 1942

Thank you for your article! It touches my heart deeply because I have recently went through something similar case of Bogdan .About 3 years ago my wife left me and 2 of our kids for 3years to another man. During this years of our separation I was so broken, so I finally read Bogdans comment on the internet who directed me to a spell caster Dr. Chris who helps in reuniting family again. After the casting of the love spell, My Ex-wife called me yesterday begging me to take her back, Dr. Chris has restored our marriage in a way I have NEVER expected, but I’m truly Thankful!

Contact Dr.Chris today on:[email protected]

Tel:+2348031396979

Best Regards

I turn 67 in March 2016. My wife is already 67. She was a teacher and is not eligible for Social Security benefits of her own. My social security monthly benefit is estimated to be $2,600 per month at full retirement age. Does it make sense for us to file a restricted application for spousal benefits only when I turn 67, and delay my benefits until I am 70? I plan to keep working and my annual salary is $150,000 per year. Does the spousal benefit reduce my future benefits at all? If yes, how much?

I turn 67 in March 2016. My wife is already 67. She was a teacher and is not eligible for Social Security benefits of her own. My Social Security monthly benefit is estimated to be $2,600 per month at full retirement age. Does it make sense for us to file a restricted application for spousal benefits only when I turn 67, and delay my benefits until I am 70? I plan to keep working and my annual salary is $150,000 per year. Does the spousal benefit reduce my future benefits at all? If yes, how much?

In terms of timing, what constitutes “filing” for file and suspend? I called SSA today and they made an appointment to call me on May 12th. In calling them today and them making a phone appointment, have I beat the filing date of April 29th? I am 67, my wife is 66 and we want to file and suspend for my benefits and let her file for spousal benefits.

Doug–I do not think this would constitute “filing”. Your best bet is file via the SSA web site, as Michael discussed in his article today, in order to beat the 4/29 deadline.

I was told if you call and make an appointment that later results in a Social Security event then your original contact call becomes your “Protected Filing Date”. This can be a killer (from one who knows) if you did not give up your HSA more than 180 days prior to establishing that Protected Filing Date. SSA wont tell you that until the fines and penalties begin to arrive. They are uncompassionate jerks…….

I never knew people still have powers and make things happened this way. My name is shery am from American. my boyfriend Scott left me for another girl for three months’ ever since then my life have been filled with pains, sorrow and heart break because he was my first love who dis virgin me when I was 19 years old. A friend of mine Kido Matthew told me he saw some testimonies of this Dr ozi that he can bring back lover within some few days, I laugh it out and said I am not interested but because of the love my friend had for me, she consulted the great priest on my behalf and to my greatest surprise after three days my boyfriend called me for the very first time after three months that he is missing me and that he is so sorry for every thing he made me went through. I still can’t believe it, because it highly unbelievable it just too real to be real. Thank you Dr ozi for bringing back my lover and also to my lovely friend who interceded on my behalf, for any one who might need the help of this great priest here is the email address: [email protected]

My boyfriend left me a month ago and he was leaving with another woman who is 10 years older than him,i feel like my life is completely over. I read over the internet how a spell caster have help several people to get there love back. I have been distressed for the past one month and what i need is to get him back and live with me so i decided to give it a try so i contacted the spell caster called Dr MARVIN and explain my problems to him and he cast a spell for me which i use to get my boyfriend back and now my life is complete and i am throughly greatful to this man,his contact email [email protected]

Hello, I am Theresa Williams After being in relationship with Anderson

for years, he broke up with me, I did everything possible to bring him

back but all was in vain, I wanted him back so much because of the love I

have for him, I begged him with everything, I made promises but he

refused. I explained my problem to my friend and she suggested that I

should rather contact a spell caster that could help me cast a spell to

bring him back but I am the type that never believed in spell, I had no

choice than to try it, I mailed the spell caster, and he told me there

was no problem that everything will be okay before three days, that my

ex will return to me before three days, he cast the spell and

surprisingly in the second day, it was around 4pm. My ex called me, I

was so surprised, I answered the call and all he said was that he was so

sorry for everything that happened that he wanted me to return to him,

that he loves me so much. I was so happy and went to him that was how we

started living together happily again. Since then, I have made promise

that anybody I know that have a relationship problem, I would be of help

to such person by referring him or her to the only real and powerful

spell caster who helped me with my own problem. His email: [email protected] you can email him if you need his assistance in your relationship or any other Case.

1) Love Spells

2) Lost Love Spells

3) Divorce Spells

4) Marriage Spells

5) Binding Spells

6) Breakup Spells

7) Banish a past Lover.

8.) You want to be promoted in your office

9) want to satisfy your lover

Contact this great man if you are having any problem for a lasting solution

through [email protected]

Under “Effective Date And Grandfathering Of Restricted Application”, you mention the grandfathering birth

date of Jan 1, 1954 for the full spousal benefit. Nowhere in this section did you mention the spouse who will file and suspend has to have been born no later than May 1, 1950, and submit their request to file and suspend on or before April 29, 2016.

In other words, the grandfathering date of Jan 1, 1954 is moot if the spouse filing a restricted application was born after May 1, 1950 and did not file their application prior to April 29, 2016.

If I am incorrect, please explain.

Leeteam,

Restricted Application and File-and-Suspend are completely separate and unrelated provisions. Whether you are eligible for file-and-suspend (or not) has no direct impact on being grandfathered under restricted application. At the most, the file-and-suspend deadline only matters for the OTHER spouse – the one who is NOT doing a restricted application. And for that OTHER spouse, the deadlines are already discussed in the file-and-suspend section.