Executive Summary

It’s a long-standing principle of the tax code that expenses incurred for the production of income or management of assets (e.g., an investment advisory fee) is a cost that can be applied against the income produced – in other words, deducted as a pre-tax expense. Unfortunately, though, under the Tax Cuts and Jobs Act of 2017, the entire category of “miscellaneous itemized deductions subject to the 2%-of-AGI floor” was repealed… which included the deduction for investment advisory fees, making them no longer able to be paid directly on a pre-tax basis.

However, the ability to pay for the cost of an advisor on a pre-tax basis is still preserved in situations where the fee can be paid directly from a tax-preferenced account or product. As a result, advisory fees deducted directly from an IRA are still pre-tax, and commissions subtracted directly from the net asset value of a mutual fund (or the cash value of an annuity) are still pre-tax as well. The caveat, of course, is that registered investment advisers charging fees cannot receive commissions from mutual funds or annuities in the first place, making it effectively impossible to charge clients on a pre-tax basis.

When it comes to annuities in particular, the fundamental challenge is that even though there’s a cash value from which advisory fees could be paid – roughly akin to deducting advisory fees directly from an IRA – annuities have historically been subject to a peculiar wrinkle in the tax code: any amount received from an annuity that isn’t received as an annuity (i.e., as annuitized income payable at regular intervals for life or a period certain) will be treated as a withdrawal, and taxable to the extent that there are any gains in the annuity contract. Which includes not only traditional distributions from an annuity to the owner, but any amount paid by an annuity on behalf of its owner… effectively rendering advisory fees from an annuity to not only fail to be a pre-tax payment, but even worse to actually trigger tax consequences as a taxable distribution. Even though, again, the same advisor could receive a 1%/year commission trail from the annuity for the same net compensation without triggering a taxable event.

The key distinction is that while the IRS deems a 1% per year advisory fee that’s paid from the cash value of an annuity to be a taxable distribution to the annuity owner (who then ostensibly pays his or her advisor), any trailing commission paid to the broker who sold the annuity is instead deemed to be an expense paid by the annuity company (and deducted from the value of the annuity), and therefore is not technically a taxable distribution.

This standard treatment could be undergoing a significant shift, however, after a coalition of insurers banded together to submit a series of Private Letter Ruling (PLR) requests, asking the IRS to change its position and consider advisory fees on so-called “fee-based” annuities to be treated like any other retirement account or internal mutual fund expense ratio (i.e., as expenses paid by the account itself, rather than as a distribution to or on behalf of the owner). And, given that these contracts are specifically designed to be fee-based (and therefore RIA-supported), the IRS acquiesced and ruled that, since the payment on ongoing fees for advice are “integral to the operation of the contract,” those fees should be considered to be an expense of the annuity itself, which are authorized by the owner, withdrawn by the annuity company, and paid directly to the (registered investment) adviser.

It’s important to note that these are “only” private letter rulings, not an actual change in the tax code, and include several key stipulations that, if not followed, could make it difficult for other annuity carriers to receive similar treatment. Specifically, the PLRs stipulate that in order to receive the favorable tax treatment, annuity advisory fees can’t exceed 1.5% per year, must be paid by the annuity carrier to the RIA, should only pertain to the advice on that particular annuity, and must be explicitly authorized by the owner.

Still, while the new ruling is a major breakthrough for the annuity industry’s attempts to create more RIA-friendly annuity solutions, it remains to be seen whether fee-based annuities will gain wider adoption with advisory firms. As the reality is that there are still numerous operational and technical issues that must be addressed, including facilitating graduated advisory fee schedules (that also don’t exceed the 1.5% per year cap), integrating annuity sub-accounts into existing RIA portfolio model management tools, the ability to open new accounts at scale (for existing RIAs with a sizable base of existing clients), and being able to coordinate various distributions (leveraging an annuity’s available living benefit guarantees) amid a much more complex asset mix that includes non-annuities the advisor manages as well.

The key point, however, is that the recent PLRs from the IRS are at least a step in the right direction, bring important parity and tax law consistency between advisory fees for tax-qualified retirement accounts and advisory fees for non-qualified annuities, and provide another potential tool that advisors can use to better serve their clients… particularly in unique situations where a client specifically needs an annuity, or wants to replace an existing annuity. From a systems and practical perspective, though, there are numerous challenges that still must be addressed, particularly for larger advisory firms operating at scale, before fee-based annuities gain wider acceptance among RIAs.

Historical Treatment Of Advisory Fees Paid From A Non-Qualified Annuity – Expenses Of The Annuity Vs Expenses Of The Owner

IRC Section 72(e) stipulates that any amount received from an annuity that is not received as an annuity (i.e., as annuitized income payable at regular intervals for life or a period certain) will be treated as a withdrawal, and taxable to the extent that there are any gains in the annuity contract (i.e., to the extent the current cash value exceeds the original “investment in the contract” under IRC Section 72(e)(3)).

And notably, the taxable treatment of amounts not received as an annuity applies to any kind of actual or deemed distribution from the annuity contract to or on behalf of its owner. Thus, not only are outright withdrawals from the annuity itself treated as taxable events, but under IRC Section 72(e)(4) so are loans taken against the annuity (since it permits the owner to receive access to the value of the annuity, without being received as an annuity). And because any distribution made from an annuity for the benefit of the annuity owner is treated as a taxable distribution event, so too has it historically been interpreted that the payment of an advisor’s own advisory fees will be deemed a taxable distribution event from the annuity (as though the owner made a taxable distribution in the amount of the fees, which was then separately remitted on an after-tax basis to the advisor).

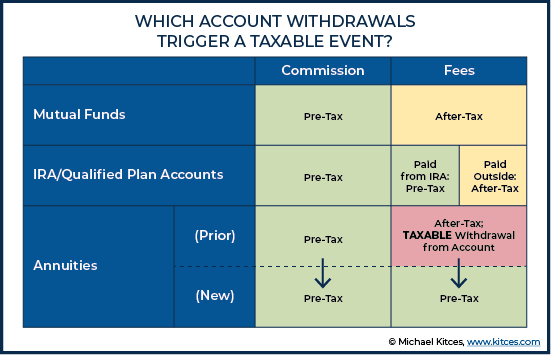

In other words, because of the broad interpretation that any amount received “not as an annuity” from a deferred annuity contract is a taxable distribution, registered investment advisers charging the traditional 1%/year advisory fees have had no way to extract their fees from their clients’ managed annuities without triggering a taxable event. Which was a substantial distinction from commission-based brokers selling annuities, who could collect a 1%/year trail to provide a substantively similar service. As in the case of a commission-based broker, the payment isn’t deemed to be a payment by the client for the broker’s advice services. It’s deemed to be an expense of the annuity company itself to compensate the broker for selling the product (i.e., it’s a marketing/sales/distribution expense of the annuity contract itself).

Thus, even though the cost to the client might amount to the same thing (either a 1% advisory fee, or a 1% commission trail), from a tax perspective the distinction was important – an annuity paying advisory fees on behalf of its owner was treated as a taxable distribution, while an annuity paying its own (commission selling) expenses of the contract to a broker (for the marketing and sale of the annuity itself) was treated as a non-taxable event and instead was simply deducted from the value of the annuity (making it implicitly pre-tax, to the extent the annuity had any gains in the first place).

In practice, this interpretation isn’t entirely unique to annuities, though. When it comes to mutual funds, commission-based expenses of the mutual fund company (to brokers for the sale of their mutual funds) are treated as expenses of the mutual fund (which are subtracted directly from the value of the fund and are implicitly pre-tax), while advisory fees must be paid directly by the investment account owner (and since the Tax Cuts and Jobs Act of 2017, are no longer deductible).

Similarly, when it comes to IRAs and other retirement accounts, Treasury Regulation 1.404(a)-3(d) has recognized that expenses of the IRA or qualified plan – which includes investment advisory fees – can be treated as an expense of the retirement account itself, and thus be paid directly from the retirement account (on an implicitly pre-tax basis) without being deemed a taxable distribution. In essence, the advisory fee is treated not as an expense of the IRA owner themselves (for which an IRA payment on their behalf would be a taxable distribution or a prohibited transaction), but instead is treated literally as a Section 212 expense of the IRA itself, for which the IRA is paying its own advisory fee. Which makes even an advisory fee permissible to pay directly from the account without triggering a taxable event, as an expense of that account. (As long as the IRA really only pays its own advisory fees, and not fees attributable to any other accounts.)

IRS Public Letter Rulings Allow Advisory Fees To Be Paid Directly From A Fee-Based Non-Qualified Annuity As An Expense Of The Annuity Itself

Given that the IRS has a long history of treating the expenses of a particular investment vehicle or account type as expenses of the account (rather than expenses of the owner that could trigger a taxable distribution if paid on his/her behalf), it was arguably only a matter of time before an annuity company would push for similar treatment that an advisory fee be permitted to be paid on behalf of an annuity for the management of that annuity. Accordingly, in 2017, a coalition of major annuity carriers came together, including Allianz, Great American, Jackson National, Nationwide, Pacific Life, and Prudential, to submit a series of Private Letter Ruling (PLR) requests that the IRS grant similar treatment for the emerging category of “fee-based” annuities (that are designed to be sold without an agent earning a selling commission, but where an independent RIA advising on the contract would ostensibly want to be paid an advisory fee, ideally without causing a tax event to the client).

And now, in a series of Private Letter Rulings issued this August, including PLRs 201945001, 201945002, 201945003, 201945004, 201945005, 201945006, 201945007, 201945008, and 201945009, the IRS has largely acquiesced to the annuity carrier requests to allow an RIA’s advisory fees for investment advice pertaining to that annuity to be paid out directly from the annuity, and without triggering a taxable event for the client… and instead, akin to how advisory fees from IRAs are handled, treating the RIA’s advisory fee for advising on the annuity contract as an expense of the annuity contract itself.

Specifically, the various annuity company PLRs requested guidance in a situation where an annuity company would issue various versions of variable, fixed indexed, and hybrid annuity contracts designed to have owners receive ongoing investment advice from a third party (properly licensed) registered investment adviser pertaining to the account owner’s risk tolerance and investment goals, the interest rates and market environment, making selections amongst the available investment options on the menu of the annuity contract, and providing guidance regarding the various other features and benefits available under the contracts.

Technically, the annuity company would then allow the annuity owner to “authorize” that the annuity company pay advisory fees directly to the investment adviser, from the annuity’s cash value (at an amount not to exceed 1.5%/year of the annuity’s cash value, and not alongside any other commissions for the annuity’s sale or servicing), for the investment advice provided pertaining to the annuity contract (and only to that annuity contract). As in other similar situations, the fee would be intended to only pay for investment advice pertaining to that annuity, and “not result in any reduction in fees related to any other asset or for any other service” (i.e., the annuity fees cannot and would not offset other fees, which could otherwise be used as a way to stuff other fees into the annuity’s pre-tax fee arrangement). Accordingly, the liability for the advisory fee would be a liability of the annuity company itself (on behalf of the contract), not the annuity owner.

Given this structure – that the annuity contract is structured to be a fee-based (RIA-supported) annuity – the IRS found that the Fees payable to the Adviser are “integral to the operation of the contract”, and that since the annuity company (via the annuity contract) is solely liable for the fees, the Fees are deemed an expense of the annuity contract itself, as the fees don’t compensate the advisor for anything other than advice to and regarding the annuity contract itself. Which means they’ll be treated as an expense of the annuity contract as the annuity company withdraws them and sends them to the advisor, not a (taxable) distribution to or on behalf of the owner.

Or stated more simply, annuity companies can now pay client-authorized advisory fees directly from an annuity contract’s cash value to the RIA advising the client on that contract, and not have the annuity’s advisory fee be treated as a taxable event. Which, notably, also implicitly makes it a pre-tax payment (as reducing the cash value without a taxable event would effectively reduce the annuity contract’s gains before those gains were otherwise recognized… at least to the extent the annuity had any gains in the first place).

Limitations Of The PLRs Allowing An Annuity’s Advisory Fees To Be Paid (Pre-Tax) From An Annuity

Notwithstanding the relatively straightforward nature of the various annuity company PLRs authorizing an annuity’s advisory fees to be paid (pre-tax) from an annuity, ultimately they are still “only” Private Letter Rulings, which technically only apply to the taxpayer who filed for and received the PLR (or in this case, the half-dozen annuity carriers who each applied for their own PLRs). The IRS is not bound to universally apply the same ruling in all instances for all annuities and all carriers, and would be within its rights to “change its mind” and stop allowing such treatment for any other annuities going forward at any point.

That being said, though, private letter rulings are generally viewed as a broader signal of the IRS’ views on an issue, and the fact that the recent PLRs on fee-based annuities are straightforward, and conform to similar practices with respect to advisory fees billed directly (and on behalf of) retirement accounts, and were approved for several different major annuity carriers all at once, suggests that these PLRs are on sound footing, and unlikely to be reversed in the foreseeable future. Which means at a minimum, other annuity carriers that want similar treatment could simply and safely submit their own PLR requests (and anticipate receiving a similar ruling). Or they could simply follow the same practices as the PLR-approved scenarios and anticipate with overwhelming likelihood that the IRS will provide them the same treatment. (As technically, there’s no requirement to have a Private Letter Ruling to affirm the tax treatment; the purpose of the PLR is just to remove any uncertainty for that particular taxpayer that the IRS might not approve it later, but getting a ‘private ruling’ upfront instead.)

However, it is important to recognize the key constraints of the private letter rulings as written – as other annuity carriers that don’t follow within the same terms will have less certainty and clarity about whether their fee-based annuity advisory-fee arrangements will be honored in a similar manner. In particular, it is notable that in the existing PLRs:

- Advisory fees are an arms-length agreement set by the advisor and the client (annuity owner), not the annuity carrier… at a maximum of 1.5%/year.

- The annuity owner must sign an Authorization with the annuity carrier to validate the Fees that will subsequently be paid by the annuity carrier to the RIA.

- Advisory fees must be paid by the annuity carrier to the RIA, and the annuity carrier must actually retain the liability to ensure the fee is paid (which ostensibly won’t be difficult given that the annuity carrier has the client’s annuity account to cover the fees, but is still notable in the event of an annuity carrier default).

- Fees should only pertain to investment advice for that particular annuity (not for other annuity contracts, nor for non-annuity investment accounts, nor other non-investment financial planning services).

Fortunately, from a practical perspective, these specifications shouldn’t be terribly difficult for most annuity carriers to manage, once the infrastructure to manage the fee payments is established (including the authorization process, fee collection and remittance procedures, and a mechanism for RIAs to set what their fees will be in the first place). But it is important to recognize that operating outside of these constraints at least places the annuity carrier back into a “grey” territory (making it more appealing for the annuity carrier to apply for its own PLR instead).

It’s also notable that these requirements for extracting advisory fees from fee-based annuities without a taxable distribution event pertains only to non-qualified annuities subject to IRC Section 72 in the first place. On the other hand, the reality is that qualified annuities (i.e., annuities held inside of tax-qualified accounts) wouldn’t need to rely on the new PLRs for fee-based annuities anyway, as extracting advisory fees from an IRA or other qualified retirement account to pay for investment management of that retirement account is already blessed by the IRS (and in such cases, the fact that the annuity is owned by an IRA is only incidental and doesn’t actually impact what is already standard treatment for advisory fees from IRAs).

Why The Annuity Advisor Fee Ruling Won’t Likely Spur Growth Of Fee-Based Contracts (Yet?)

While the annuity industry has lauded the IRS’ decision to permit an RIA’s advisory fees for fee-based annuity contracts to be paid directly from the annuity’s cash value on a pre-tax basis as a “game changer”, in reality the new tax rules alone will not likely be enough to really expand adoption into the RIA channel. As while facilitating the way an advisory firm gets paid (without triggering a tax event) is certainly an important step, arguably the biggest impediment to fee-based annuity adoption is not a fee issue, but an operational and technology systems issue first and foremost.

The issue is amplified by the fact that RIAs, with their typically-recurring-revenue AUM model, often amass over time a significantly higher number of clients that they’re working with and managing on an ongoing basis than an individual broker. Which in turn leads them to implement processes and procedures, facilitated by technology systems, to be able to deliver services efficiently to an ever-growing number of clients. Which will create significant issues for annuity carriers seeking greater adoption of fee-based annuities from RIAs (just because those RIAs can now “get paid” directly from the annuity contract).

For instance, some of the core issues likely to arise with the implementation of fee-based annuities in RIAs include:

- Need to facilitate graduated fee schedules calculated across all of the household’s accounts. It is common for RIAs to use graduated fee schedules – e.g., 1% on the first $1M, 0.8% on the next $2M, and 0.6% on everything above $3M – with holistic advisory firms calculating those fees not account-by-account, but aggregated across all of the household’s accounts. Which means client #1 with a $500,000 annuity and no other assets might be billed 1%, but client #2 with a $500,000 annuity and $1M of other assets pays a blended rate of 0.933% on that annuity contract, and client #3 with a $500,000 annuity and $3M of other assets pays a blended rate of 0.829%. Currently, graduated fee schedules aggregated across the household’s assets are calculated and billed directly via the advisor’s RIA custodian platform, or using third-party software (e.g., portfolio performance management tools like Orion). How will annuity carriers ensure that an RIA with 1,000 clients, each of whom may have a different blended fee schedule based on how their exact assets align to the advisor’s graduated fee schedule, ensure that each client pays the proper pro-rata share from the annuity contract?

- Some RIAs have fee schedules that start above 1.5% for small accounts. While the traditional “benchmark” fee for an RIA is a 1% AUM fee, in practice 1% is the median advisory fee for $500k to $1M accounts. Accordingly, an RIA fee study from Bob Veres of Inside Information showed that nearly 20% of RIAs charge a fee of 1.5% of higher for an account under $250,000, including some very large and high-profile firms. Which raises the question of whether the hard-cap maximum advisory fee of 1.5% (at least under current PLRs) may conflict for some advisory firms working with mass affluent clients (who arguably may be most in need of typical annuity guarantees) whose fee schedules start at higher levels.

- Annuity sub-accounts don’t integrate to advisor model management tools. One of the most rapid-growth technology categories for RIAs in the past decade has been “rebalancing software”, or more broadly, software that facilitates trading and managing model portfolios. It’s rebalancing software that makes it possible for RIAs to centralize trading functionality, and have just 1-2 traders support 1,000+ clients at a time, where the software determines what trades need to be made to keep clients on model (or adjust client portfolios when investment changes are made to the model), and then queues up trade files that are uploaded to RIA custodians. However, rebalancing is not feasible in/out of an annuity (as it would either be a taxable distribution, or a new contribution that may subsequently become tied up, especially for clients under age 59 ½ to whom early withdrawal penalties would then apply), nor is there any way for RIAs to do “block trades” of a large group of annuity contracts from a single centralized system. As a result, it’s virtually impossible with current technology systems for an RIA to actually integrate a fee-based annuity systematically into its model portfolio allocations for clients.

- Account opening at scale is a paperwork nightmare for an established RIA. Because annuity contracts are just that – contracts – each one must be opened and signed individually by each and every client. Which isn’t necessarily unique, as every investment account and IRA also requires individual paperwork. But if there’s one thing advisory firms dread above all else, it’s “mass re-papering” of accounts… which is effectively what would happen for an RIA to systematically roll out fee-based annuities across their client base. And with a lack of annuity application processes that link to current RIA custodial and CRM systems – both to pre-populate the data, facilitate e-signatures, and then track the progress of paperwork completion – for many/most RIAs, the prospective administrative staff cost burden of facilitating fee-based annuities may be prohibitively expensive for the firm (at least until annuity application systems better integrate more directly to RIA technology).

- RIA systems aren’t built to coordinate with the distribution limitations for annuity income guarantees. One of the primary benefits of annuities in today’s high-valuation environment is their various forms of guarantees, from living benefit riders for lifetime withdrawals to the floor-with-upside crediting formulas of fixed indexed annuities. However, most annuity guarantees have very specific provisions regarding the timing and amounts of distributions that may occur, without potentially undermining the value of those guarantees (e.g., variable annuities that allow dollar-for-dollar withdrawals up to a specified amount, and pro-rata withdrawals thereafter, where an unwitting ‘excess’ withdrawal can rapidly deplete the guaranteed benefit base). Which makes the process of facilitating withdrawals across a combination of investment accounts, retirement accounts, and fee-based annuities, exponentially more complex for RIAs (especially those with a material volume of clients trying to systematize and scale the practice). Which means at least initially, RIAs may be more likely to adopt ‘simpler’ investment-only variable annuities solely as a tax-deferral/asset location vehicle, or perhaps a fixed indexed annuity simply for the built-in risk/return profile of something on the mid-point between bonds and stocks, which don’t require the same level of retirement withdrawal coordination that RIA systems aren’t built to coordinate.

Notably, beyond the challenges that RIAs themselves face by trying to integrate fee-based annuities systematically into their firms, there’s also the challenge of how annuity carriers will coordinate RIA advisory fees with the rest of their annuity guarantees or crediting rate calculations (in the case of fixed indexed annuities). As while from a tax perspective, the extraction of the fee from the fee-based annuity will not be a taxable event, it will likely still be deemed a withdrawal for the purposes of any guarantees under the contract.

Which raises the question of whether or how fixed indexed annuity participation rates, caps, or spreads, will have to be adjusted for the advisory fee that will be withdrawn (especially since advisory fees are calculated on an ongoing quarterly basis, with graduated fee schedules, which means it may not even be knowable more than one quarter in advance what the fee will be!). And if an advisory fee is extracted from a hybrid annuity/long-term care policy, will the advisory fee withdrawals reduce the available pool of long-term care benefits?

Similarly, if a client is already withdrawing 5%/year from a variable (or fixed indexed) annuity with a guaranteed minimum withdrawal rider that provides a 5% withdrawal guarantee against the benefit base, assessing an additional 1% fee (for a total withdrawal of 6%) could be treated as an excess withdrawal that reduces the benefit base for future years. In point of fact, some annuity carriers are already looking to create a “fee corridor” approach that coordinates annuity withdrawal guarantees alongside RIA fee withdrawals of the coming generation of fee-based annuity contracts… but the exact features and structure are still to be determined.

Notwithstanding these challenges, though, there’s no question that being able to facilitate RIA advisory fees from fee-based annuities will begin to make them at least incrementally more appealing to use, if only in relatively “simple” scenarios (e.g., investment-only variable annuities as a tax deferral wrapper for asset location purposes), or in “one-off” scenarios (e.g., individual clients who specifically need an annuity, or clients with existing annuities that may be appropriate to replace). Still, though, RIAs do not run their practices in the same way that brokers do, and are more likely to try to systematize what they do for clients… in ways that makes a wide range of “one-off” annuity strategies very impractical for most firms (unless they have a very small number of ultra-high-net-worth clientele where the client/advisor ratios make such customization feasible).

On the other hand, in a world where RIA clients can no longer deduct their investment advisory fees (since the Tax Cuts and Jobs Act of 2017), the irony is that being able to pay advisory fees on an implicitly pre-tax basis from inside of an annuity may even usher in a new wave of ultra-low-cost fee-based annuities, where the tax savings on billing the advisory fee from inside the annuity is actually worth more than the cost of the annuity itself. In other words, fee-based annuities now become another type of product – alongside commission-based mutual funds and IRAs – where the tax treatment of extracting the advisory fee directly from the account/product is superior to simply billing the client to pay directly (on a purely after-tax basis), creating a bizarre tax-based tailwind specifically to try to structure advisory fees to come from annuity contracts in the future (at least to the extent permissible).

The bottom line, though, is simply to recognize that, after decades of RIAs being faced with the challenge that clients with annuities couldn’t pay their advisory fees from their annuity contracts, the latest PLRs from the IRS reverses this position 180 degrees, to the point that not only is it possible for RIAs to do so, but it may even be preferable to wrap advisory fees into annuity contracts. And the IRS shift may even usher in a similar potential for RIA-supported 529 plans to someday permit advisory fees to be paid directly from such accounts as well. Unfortunately, though, what may be feasible for tax law purposes still isn’t necessarily feasible within the real-world technology and operational constraints of RIAs, especially those that have grown beyond $100M of AUM and increasingly try to operate more systematically to scale their practices. Which means that while the shift in tax treatment of advisory fees may be a milestone in the evolution of fee-based annuities, it’s likely still only a stepping stone on the path to wider-scale adoption by RIAs.