Executive Summary

For most financial advisory firms that seek to grow, it takes a significant commitment of time to market to, attract, and ultimately close prospective new clients. But as advisory firms grow, the cost of that time it takes to attract clients through marketing efforts and close them through sales efforts becomes commensurately more expensive as the business owner’s own time becomes more valuable. Which can be problematic for firms that want to grow, and the cost to acquire new clients becomes more expensive as the business (and cost of that time) grows, becoming inherently less scalable the larger the business gets … unless the firm updates its marketing and sales methods to match the firm’s (newfound) size and resources.

In this guest post, Angie Herbers – Chief Executive and Senior Consultant at Herbers & Company, an independent management and growth consultancy for financial advisory firms – explains why advisory firms need to adapt the sales engagement methods that they use if they want to continue growing in a sustainable (and time-cost-effective) manner. As notably, while industry benchmarking statistics suggest that an average financial advisory firm will spend about 3% of revenue on marketing, these numbers only include direct marketing expenditures (e.g., online ads, consultant expenses, etc.), and don’t include the actual value of the advisor’s potentially-quite-costly time spent on acquiring clients (e.g., attending networking events, meeting with prospects, etc.). Furthermore, as a financial advisor’s firm grows and the advisor gains experience and expertise, their time generally becomes more valuable; thus, if they spend the same amount of time on client acquisition as they did when their time was worth less, the total cost actually spent on marketing can significantly increase!

In light of this growing premium on an advisor’s time as a part of the marketing and sales process, how should an advisor most efficiently spend their time on business development efforts? To address this, it’s important to consider the three primary processes in any financial advisory firm: A Marketing process to establish awareness that the firm exists, a Sales process to engage prospective clients, and a Client Service process, to cultivate lasting trust with clients and to give them a reason to stay with the firm. While many firms focus primarily on the Marketing or the Client Service process to address growth problems, the reality is that, more often than not, problems with growth (and time-cost-consuming nature) reside mainly in the Sales process – the stage in client acquisition that begins when a prospect schedules a first appointment, and ends with a signed contract.

For most advisory firms, there are generally three methods of engagement an advisor can use in the sales process. The best method for any firm to use will often depend on the approximate revenue of the firm. The “Do” Method involves actually doing something for the prospective client to show them what they might expect to receive from the firm and is most valuable for newer firms (generally those with less than $750,000 in annual revenues) who have not yet established a brand identity. Clients seeking these firms are looking for value and are most interested in what the firm has to offer them. The “Show” Method is less labor-intensive and involves showing samples of what the firm has to offer to the client (e.g., a sample financial plan or investment policy statement); in other words, these firms are typically well-established and can rely on their brand value with compelling stories, supported by “showing” what they offer. While this is more efficient than the “Do” Method, it does still require time to prepare samples to show a target clientele and is often more appropriate for firms with annual revenues between $750,000 and $3 million. The “Tell” Method is the most time-efficient and relies on an advisor’s own confidence in the firm to tell the client specifically how they will address the client’s needs. There is no “free work” done or samples offered because an advisor in a firm with more than $3M in annual revenue can generally rely on their firm’s brand value and the story behind the firm alone to establish trust with a new client. Which is important, because considering the high value of an advisor’s time at this level, (still) using the “Do” or “Tell” methods can be exponentially more expensive (than it may have been when the firm had less revenue and the advisor’s cost of time was less).

Ultimately, the key point is that the Sales process is a distinct step from the Marketing and Client Service processes and that, for many firms, growth problems can most effectively be addressed by adjusting how the Sales process is carried out. While newer firms with less revenue can benefit most using the “Do” method of offering free work to prove to clients they are worthy of their trust and engagement, firms with more revenue can benefit from the more efficient “Show” method of offering work samples and demonstrations to back up their firm’s brand identity, while firms with revenue generally over $3M are often the most well-established and generally have widespread brand recognition… that advisors can leverage to simply “Tell” a client why they should be engaged, ideally (and cost-effectively) ‘closing’ the deal after just one meeting!

In my 20+ years of working with independent advisory firms, I’ve come to notice that across all firms, there is one thing they have in common; it doesn’t matter if the firm has one advisor and zero clients, or if they employ one hundred advisors and manage $1 billion in assets under management.

The common thread is this: for those firms to continue growing, they need to attract and sign more clients and assets each year than they lose. It sounds simple, right? It’s a no-brainer.

But to solve this problem of finding and signing new clients each year most advisory firms have arrived at the belief that it’s solved by “more marketing”… often coupled with advisors who don’t understand marketing and who don’t do it well, but who believe if they could simply identify a way to market themselves better, they could solve their growth problems.

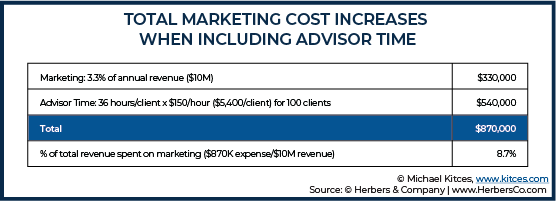

On average when new clients at Herbers & Co. begin to work with us, the amount they are spending on their marketing comes to about 3.3% of their revenues each year. But, here’s the problem with looking at these statistics in isolation: They only show you what advisors spend on things like online ads, website updates, and outsourced professionals. What they don’t consider are the ‘soft dollars’ lost when advisors have unproductive meetings with prospective clients and unnecessarily waste their time. And, they certainly are not quantifying what you are doing every day by delivering great client service that cultivates referrals.

For example, when our advisory firm clients who are having growth problems begin to work with us, we have them track the amount of time they are spending on sales and marketing. In doing so, we’ve learned that on average they are spending roughly 36 hours total to attract one client. Now, let’s say we value their time at $150 per hour spending 36 hours meeting with prospective clients and going to various work-related events to discover more of them. After all those hours spent networking and selling, an advisor only signs one new client, which is traditionally the case. The per-client acquisition cost is as high as $5,400! In fact, a recent Kitces research study on advisor marketing found that the average advisory firm spends over $3,100 in client acquisition costs… of which almost 80% is the time cost of the advisor’s hours spent in the marketing and sales process.

Now, let’s put some real math to this equation: Let’s say your firm’s annual revenue is $10 million, your average client pays $10,000 per year in fees, and you want to grow 10% next year. This means you need 100 new clients to reach your goal. You are spending 3.3% of your revenue on marketing, but each new client costs you $5,400 in advisor time.

In this scenario, your total marketing cost is now 8.7% of revenue!

Now, let’s ‘nerd out’ on this for a minute because this is what Herbers & Company has been tracking, studying, and solving for nearly twenty years.

How many of you believe your hourly worth as an advisor is $150 per hour to your firm? That may be what you take home in income, but your time to the business, better be higher for the sake of profitability.

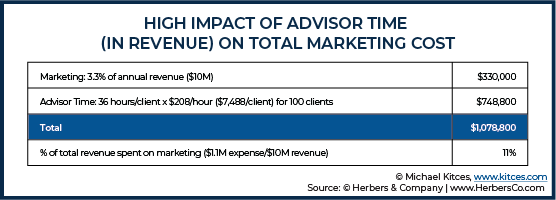

Here’s what Herbers & Company knows: On average, your firm earns $208 per hour per advisor. This is not to be confused with what you ‘pay’ in compensation to an advisor working in your firm — which, obviously, is lower. This means that if you hire one advisor, your firm can expect to generate $208 per hour per advisor in revenue (which amounts to $400,000+ of revenue per advisor across the year) in return on investment (ROI).

Now, using the scenario above, at $208 per hour instead of $150 per hour, your total acquisition cost of one new client can jump as high as $7,488 in advisor time!

In this situation, the total marketing cost based on the goal illustrated above has grown to 11% of revenue.

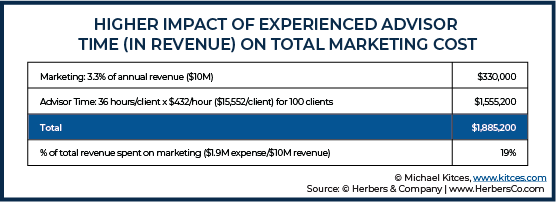

Now, here’s the real kick in the stomach. If you have experienced advisors who are very good at client service and working as a team with other advisors, you can increase what a firm earns per each advisor, up to an average of $432 per hour! This is good news!

But if advisors are still doing marketing and sales, this makes total acquisition cost of one new client jumping as high as $15,552 in advisor time! So, what is the total marketing cost now, assuming advisors are still doing a lot of the rainmaking, prospecting, and marketing as part of their job description? The cost has now grown to 19% of total revenue!

Ladies and gentlemen, contrary to popular belief (but as shown in the recent Kitces Research study on advisor marketing), most advisory firms are spending between 9% to 19% on marketing throughout the growth cycle. They just “hide” it by failing to properly account for the time cost of their advisors doing business development, including both marketing and the often-time-consuming sales process that goes along with it. And, if your advisors are great at client service and increasing their value to your firm over time, marketing and sales costs get further out of hand! It’s a Catch-22.

As we can see from our example, however, the problem with growth is not truly about an advisor’s marketing strategy, per se. The problem is in the amount of unproductive time spent meeting and seeking prospects who may or may not ultimately become clients as you build a bigger firm. In other words, when time is considered as a cost, the time efficiency – or time inefficiency – of the marketing and sales process becomes a major barrier to growth.

Stated more simply: Want to know why you aren’t growing faster? Time is the main reason why.

The Time Trap Of Inefficient Marketing And Sales

Now, I wished it stopped at time, but it doesn’t. Your time problem will only get worse if you think the problem is one that can be outgrown with more marketing. If you get too deep into that hole, you’ll start to seek acquisitions and/or mergers to solve your growth/time problem, as well. And then… fear takes hold. When the fear of no- or low-growth gets you down, you’ll either sell or merge your firm and/or layer on more marketing and sales, taking you into an even deeper whirlpool.

At this stage, you’re super vulnerable, stressed, and tired, fighting to get out. So you seek help anywhere you can get it. Sadly, some advisors will stumble into the wrong places, finding themselves talking to other advisory firms who want to acquire them and who use the promise of marketing ‘quick fixes’ to convince them.

You’re in deep now. When you realize it, you will either retreat back to being a solo advisor (How many times have you heard solo advisors are going ‘extinct’ due to large firm consolidation? Have you ever wondered why certain people are saying it?) and/or worse – drum roll please… you give up and sell your firm for less than what you are worth to a buyer who has been watching and waiting on the sidelines for you to drown, in time.

In all my years working with advisory firms, we have confirmed that most advisors don’t have a marketing problem, they have a marketing fear. The real problem is time. To solve that problem, and to get you growing again, we have to reduce cost-inefficient rainmaking time and reengineer the sales process.

Here’s what you need to do if any part of the above sounds like you. The solution is surprisingly quite simple… but only if you’re willing to get out of the rainmaking and marketing hole you’ve been stuck in for years.

How Advisors Engage Clients In The Sales Process to Transform Awareness Into Trust

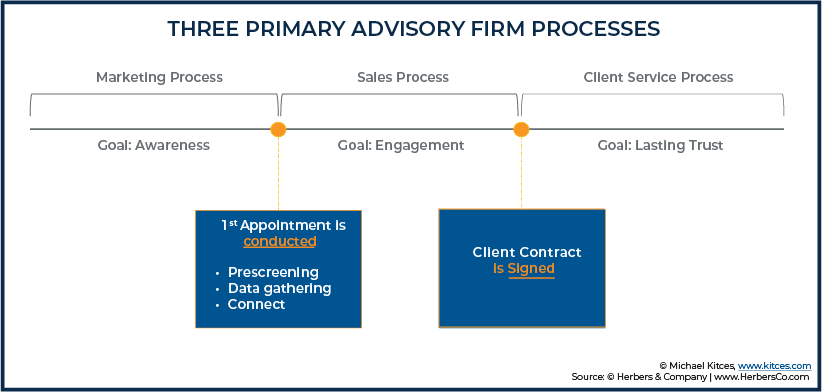

The Sales Process is one of three primary processes in every advisory firm, serving as the ultimate connector between the other two, Marketing and Client Service, because it sits in the middle, tying together what a prospective client has heard in the Marketing Process to what they will receive in the Client Service Process (Figure 1).

The Marketing Process comes right before the Sales Process, and its objective is to drive awareness to the firm, what services you provide, and how those services can make a prospective client’s life easier or less painful when it comes to their financial situation.

The Client Service Process follows the Sales Process as the last leg of the journey and is aimed at building trust with clients. Building trust goes beyond simply building engagement because trust is the ‘feeling’ experienced when you continually engage with someone and do what you say you are going to do for them.

This trust-building process is important, obviously, because when a client trusts your firm, they will stay for a long time, and they will tell others about you. Client service works on continually delivering that feeling of trust because while it is exceptionally hard to gain, it is also exceptionally easy to lose.

Throughout the growth cycle, most firms focus on either the Marketing Process or the Client Service Process, but typically growth problems reside in the Sales Process more than they do in either of the other two.

What is the true objective of a healthy Sales Process? It is to create engagement. Most people talk about engagement during the Client Service Process, but as I’ve already explained, the client service process gives you the opportunity to build deeper trust. To get to building trust in the first place, you first need to get engagement, and that happens during sales.

So, where does the Sales Process begin? It begins when someone takes action to schedule an appointment. Logically, then, your Sales Process begins with your first appointment and ends with a signed contract. That first appointment, usually for most advisory firms, follows one of three meeting types:

- Pre-Screening Appointment. This is where you get to know someone and decide if you’re both a potential fit for each other. When done right, this usually happens by phone.

- Data-Gathering Meeting. A meeting where you get beyond the surface details of a client’s feelings about their life and get detailed information about their financial situation.

- Connection Meeting. Establishing trust with the client, identifying their goals, and communicating how the advisor’s services can help them meet those goals.

During the Sales Process, your firm can engage with prospective clients in one of these three ways. The engagement method your firm uses will directly impact your ability to grow, or it may continue to bleed time and marketing dollars if you go from one meeting to the next and to the next if they don’t become a client.

Three Methods of Engagement an Advisor Can Use in the Sales Process

Designing an effective Sales Process requires advisors to understand the three main methods of engagement that can be used during this process. Too many firms try to do all three, which further eats away time and marketing dollars in sales. If you want to be effective, you need to choose just one at a time.

Before we identify which one your firm should choose, I’m first going to explain the three methods of engagement (figure 2).

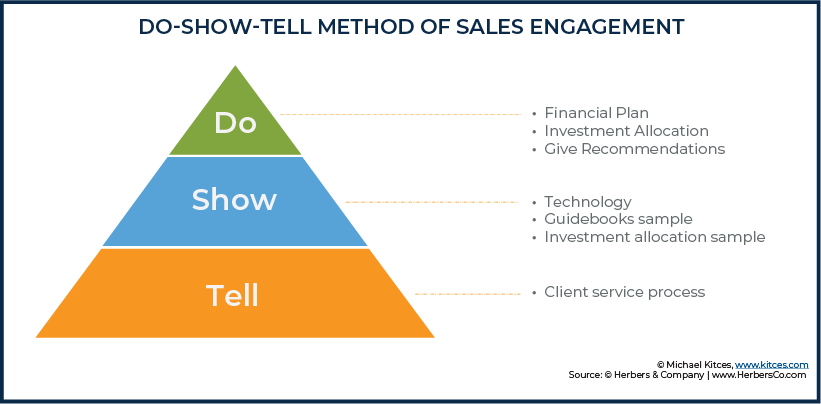

The “Do” Method

Most advisory firms that Herbers & Company has worked with and observed over the past twenty years use the “Do” method in their sales process. This method is one where you Do something (for free) for a prospective client. Typical deliverables in this “freemium” approach might include the creation of a financial plan, an investment allocation, or you give advice upfront before asking someone to work with you officially.

There are some issues with the Do method. The primary problem is that this method allows the prospect to determine if they like what you recommend or not. While it could be debated on how good that is for the prospect, it’s not good for your business in the long-term.

The deliverable you give to a client when using the Do method is commonly referred to as a “loss leader” because you’re providing work for free before someone decides to work with you. Once you’ve provided the free work and given them something they can keep, then, at that point, you’re able to ask them to sign with you.

Obviously, this method creates issues for profitability as you grow because advisors are required to do a lot of upfront work before someone commits, and there is no guarantee that the work will be rewarded with a new client.

Of the three engagement methods, the Do method is the least efficient. It eats away at profits, it’s difficult to train, and it sucks time away from more valuable business opportunities and client service. In the Do method, only an advisor can sit with a client (or spend time producing what will be delivered when sitting with the client),and spending that time with a prospect reduces the time they can spend with existing clients.

The “Show” Method

The evolution of the Do method is the “Show” method. In this sales engagement process, you get rid of any work being done for free and, instead of putting hours of work into custom deliverables, you instead Show a prospective client some aspect of what they’ll receive should they decide to become a client.

Common items to show might include a piece of technology (such as a client portal, mobile app, or financial planning software), a guidebook that demonstrates the client service journey, a sample financial plan, or a sample investment allocation and/or investment policy statement.

When advisory firms adopt the Show method of engagement, an advisor listens to a prospective client during a meeting, and then shows them what can be provided to help them achieve the goals they’ve discussed.

This method is an improvement over the Do method because an advisor is not spending any time creating free work, wasting hours and hours of marketing and sales dollars without ever having obtained a client; instead, they are simply providing prospects with the picture of a tangible result of the type of work that will be done after the client signs.

The Show method results in average operational efficiency. Some advisors will combine aspects of the Do method within Show, but Show is more difficult to achieve because it requires more pre-planning. To get to Show, advisors must create a high-quality compelling client guidebook or sample financial plan, focus on performance by showing an investment allocation, or have a piece of awesome technology they’re willing to show off.

The “Tell” Method

The “Tell” method is the holy grail of engagement methods in the sales process. In the Tell method, an advisor does zero free work, and also doesn’t show a client what will be provided in the client service phase; rather, an advisor simply describes the client service they will receive, and walks a prospect through the firm’s service model.

Many advisors we consult to move to the Tell method are initially skeptical because they’re reminded of the brokerage environment they left when they were required to ‘sell’ the prospect something without backing it up with tangible proof. In other words, they think the Tell method feels too ‘salesy’.

When done with the right intentions, however, the Tell method is the leading indicator of the confidence you have in your client service. You know what you do so well that you can articulate the journey a client will experience if they work with you. In doing so, you give them the ‘feeling’ of comfort and security.

The Tell method is not an underhanded sales technique; it is an advisory firms’ capability to communicate their value with clarity.

Comparing all three methods of engagement, Tell is the most efficient, as it requires an advisor to conduct only one true ‘sales’ meeting, which we call the “connection” meeting.

Even better, anyone in the organization can be trained to use this method; I’ve worked with a firm (and I admit this is an exceptional case) where an administrative assistant was able to conduct the sales meeting and close a prospect. Achieving the Tell method, however, requires a firm to know exactly who they are.

Choosing a Sales Engagement Method for Your Firm

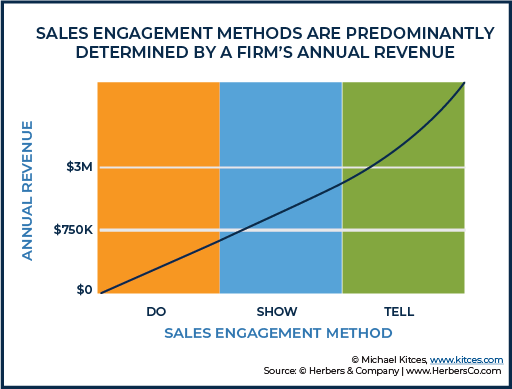

Advisors must choose one of these three methods to use within their firms, but not every firm simply gets to say, “I would like to use this method” and have it work effectively. Rather, the method a firm is able to use is predominantly determined by where the firm is in its growth stage, and the growth stage is ultimately tied to revenues.

If a firm is under $750,000 in annual revenues, the majority of clients will be more interested if the firm has something to give them. Consequently, the firm demonstrates its value as a smaller organization by using the “Do” method and giving away free work, which cultivates engagement during the sales process that would otherwise be generated in client service.

Firms in the middle of the growth process, who generate revenues between $750,000 and $3 million each year, can move on to the “Show” method. The firm’s size and brand demonstrate its ability, which means that advisors can begin to illustrate their value through “showing” a prospect the outcome of their work, instead of doing free work to credibly validate their point.

Firms generating over $3 million in revenue, can effectively implement the “Tell” method. At this point, the firm is usually big enough to illustrate its brand value and has a long and deep enough story to tell. By implementing the Tell method, a firm can maximize its efficiency and capacity to allow more room for growth, without hiring additional advisors for sales to make that growth possible.

It’s important to note here that one of the major growth problems for large firms with multi-billion in assets under management (AUM) is that they never move away from the “Do” and/or “Show” methods. This all leads to major capacity, marketing, and hiring problems that reduce the profit margin. The bottom line is that any firm operation over $3M in revenue needs to move to a “Tell” method as fast as they can before adding additional marketing.

Every advisory firm’s goal is to get to a stage where they can implement the Tell method in their sales process, and the faster a firm can get there, the better. But the problem is, most advisory firms don’t move away from the “Do” process as the firm grows. And unfortunately for these firms, the bigger you get, the more exponentially expensive the “Do” process becomes to the firm, spiraling Client Acquisition Costs higher and higher and making the firm less cost efficient as it scales!

Why Advisory Firms Don’t Improve Their Sales Process

When firms get stuck in the Do method, the work to bring on even one new client can become insurmountable. When the work to bring in a client becomes greater than the reward, these firms and their advisors begin to subconsciously (or sometimes consciously!) resist leads, because growing is simply too much work relative to the incrementally limited reward.

Other firms, however, may resist moving away from their Do method because it got them to where they are, so they fear changing it at all.

The core problem, however, is that most firms cannot articulate their client service process well enough for them to describe it in a way that engages a prospect’s feelings. As a result, they must give away free work to demonstrate what they can do. This free work, on top of serving existing clients, on top of doing marketing work, on top of trying to grow a business, inevitably takes a big toll.

Put simply, as advisory firms grow beyond one solo advisor, or a group of individual advisors working independently, into an ensemble model, they don’t understand who they are anymore and are unable to tell their story… because, well, it’s not about you anymore. It’s about your firm.

Common sales training and advice given to advisors often dictate that when advisors first meet with a prospective client, they should let the prospect do all the talking and just listen to their needs. But frankly, as we’ve learned through watching the human behavior of growing advisory firms, this advice is flat-out wrong.

No good relationship is ever built on a single story alone; there must be two stories communicated and merged for ‘true’ engagement and trust to develop. Your story, and your client’s story, must become one.

This merging of two stories into one process dramatically increases your lead rate and close ratio as you grow, without killing your time and your profit margin in the process. The relationship will build on this story, and is strengthened as a client moves through the client service process.

And, if you do this right, word of mouth marketing will take off, which is the greatest marketing of all. In consulting, we call this ‘positioning’ and/or ‘messaging’ the first step in creating great marketing.

The Tell Method’s True Benefit: A One-Meeting Close

Each step that moves your firm further from the Do method and closer to the Tell method, as you build advisory teams, shortens the firm’s sales process, strengthens advisory training, and reduces the client acquisition costs of growth.

The Do model fits the traditional sales process, and it’s also the longest with a pre-screening meeting, a data-gathering meeting to determine goals and finances, a presentation meeting to show off the work done to create a financial plan or allocation, and then a contract signing meeting to get a client to commit to the service.

But once a firm gets to the Tell method, the sales process becomes very simple and easy to train. Anyone who wants to learn more about your firm immediately gets a connection meeting. Within that meeting, a senior advisor only “tells” the prospect, sharing the story of the firm’s client service process, which is delivered in the same way by every advisor.

If that story is communicated well, it begins to cultivate a ‘feeling’ of trust in the client. Then, when the client tells their story, they can relate to your firm. Boom, the connection is created, the prospect is engaged, and you close the client relationship.

The Tell method, in fact, is designed for an advisor to create a ‘feeling’ within a client, and that feeling is the result of knowing client service really well.

Advisors who can close in one meeting and are good at ‘rainmaking’ from years of experience delivering great client service can recognize what trust between a client and advisor looks like, and know it well enough to connect to it.

But you don’t have time for every advisor in your firm to walk uphill both ways in the snow like you had to do. And, I can “tell” you (pun intended) that cultivating the feeling of trust within a client comes from good sales training to close a client in one meeting.

As anyone can see, getting to “tell” as a sales method requires a firm to put work into their people, training them on service before they can begin to expand their marketing and sales. And as you grow larger, the sales process needs to shorten as client service expands.

The goal is to transform the sales process in a way to engage prospects in the fastest way possible, taking them from awareness (marketing) to trust (client service) quickly. The very best marketing out there is to get all your advisors experienced and trained in client service, so they can “tell” too.

Don’t set yourself up to fail – in professional service industries, great client service is what markets and sells, and that’s an easy story to tell. Now, as you may have observed, much of what happens in the sales process is predicated on what happens in the client service process, and this tension begs the question: How do you create exceptional client service?

That answer is easy, too: figure out and know who you really are.