Executive Summary

Historically, getting paid for financial planning – not just to implement the recommendations, but for "The Plan" itself – meant producing a voluminous physical financial plan for which the advisor would be paid. The Plan was the tangible, physical deliverable, full of in-depth analyses and culminating in the advisor’s recommendations, that substantiates the financial planning fee. The one major caveat: few clients ever actually open The Plan again after it is first presented, focusing only on the subsequent recommendations and action items… and raising the question of whether financial planning might be done far more efficiently by eschewing The Plan and just delivering a One Page Financial Plan (of core recommendations and action items) instead.

Yet the reality is that even if The Plan is never revisited by the client after the day it’s presented, that doesn’t mean it was useless to have created it in the first place. Because from the client’s perspective, The Plan is what helps to validate that the subsequent recommendations are right and to be trusted in the first place; in other words, the client may in the end focus on just the recommendations and not The Plan, but that doesn’t mean they would have trusted and acted on those recommendations in the absence of the supporting comprehensive financial plan analyses and output.

Similarly, the real challenge for many clients is not figuring out the appropriate recommendations for them to achieve the goals in their financial plan, but to identify what their goals should be – or can be, or are even possible – in the first place. Which means producing The Plan, and subsequent What-If scenarios for the plan, are an essential element of the planning process in the first place. And again something that cannot be eschewed by just focusing on the One Page Financial Plan of recommendations at the end.

Notably, this doesn’t necessarily mean that financial advisors should or need to continue producing comprehensive financial plans exactly as they have in the past. The more the advisor can establish their trust and credibility – whether through showing empathy to create rapport with the client, demonstrating good communication skills, or simply their years of experience – the less the client may rely on the advisor’s analytical plan output. And to the extent planning software can be used more interactively and collaboratively with the client, the less it’s necessary to print out the voluminous plan in the first place.

Nonetheless, the challenge remains that even if the goal of the financial advisor is not just to get paid for The Plan, but for the advisor’s own financial planning knowledge and wisdom… it’s still necessary to go through the financial planning process in crafting recommendations for clients, if only because that’s what it takes for the client to have the buy-in and trust necessary to actually follow through and implement them!

The Comprehensive Financial Plan And The Index Card Of Advice

Most professionals have heard some version of the famous allegory of the handyman and the $100 nail:

A man was frustrated by a loud creak in his floor, but couldn’t figure out how to fix it. Eventually, he contacted a handyman to come out and investigate. The handyman got down on his hands and knees, pushed on a few of the floorboards in an effort to identify the source of the squeak, pulled out a single nail, hammered it into the precisely right spot to solve the creak… and handed an invoice for $100 to the man.

The man exclaimed “$100? For a single nail!?”

And the handyman replied “No, it was $1 for the nail, and $99 to me for knowing precisely where to hammer it.”

The story of the handyman’s invoice, which has been told in many permutations over the years, is meant to illustrate the difference between the value of work (and deliverables) on their own, versus the value of the knowledge and wisdom it takes to perform that work well. Which is relevant not only to handymen and carpenters and plumbers, but also doctors, lawyers, and virtually anyone in a knowledge-based profession where experience matters… including financial planning.

In fact, the distinction between the value of the work, and the value of the knowledge that went into it, is perhaps especially relevant in the world of financial planning, where fee-for-service financial planners often get paid to provide “The Plan” (with a capital T and a capital P!), even though it’s long been observed that clients rarely ever read or refer back to the voluminous financial plan after it is produced.

Which raises the question: in the end, is the value really The Plan (the physical financial planning document), or the financial planner’s knowledge? Could a financial advisor really get paid thousands of dollars for “just” the one page of financial planning recommendations, akin to the handyman who got paid $100 for a nail (and the wisdom to know where to hammer it?)? Would clients really still pay for the financial planning recommendations on an index card, if there was no financial plan to go with it?

The Three Roles Of The Physical Financial Plan

In considering the consequences of “just” providing financial planning recommendations and not producing (the rest of) an actual physical financial plan, it’s worth considering the role that that physical financial planning document itself actually plays in the process of delivering advice.

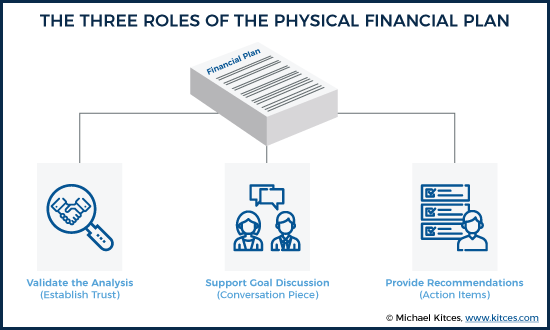

Certainly, a key aspect of the financial plan is the recommendations and actions items that it culminates with. After all, the whole point of seeking financial advice is that at some point, the advisor has to actually give advice about what to do, what needs to be changed, and what the client should implement. The recommendations and action items – whether as a standalone page (or index card), or part of the overall financial plan – are an essential component of providing “The Plan”.

Yet the reality is that while the recommendations and action items are a key part of the financial plan, they aren’t the only role that The Plan plays in the advice process.

The Financial Plan Validates The Client’s Trust

First and foremost, a key aspect of the physical financial plan is that it validates the subsequent advice and recommendations being given.

After all, without the presence of a physical financial plan, the advisor’s recommendations on a one-page financial plan would have to just be taken on faith that they are technically accurate, that the advisor properly and fully analyzed the situation, and that the action items actually reflect the best course of action. Especially since – unlike the scenario of the handyman’s invoice – there’s no immediate result to affirm that the Index Card of advice was/is actually correct.

In other words, if the handyman’s nail doesn’t actually solve the creak immediately, the handyman can’t invoice $100 for the nail, because it will be immediately obvious that the job hasn’t been done. Unfortunately, not so with financial planning, where it may be years or decades before the outcome is known. Which means the client has to trust, up front, that the advice is correct. And what better way to validate that the advisor really did the analysis properly, and that the recommendations should be trusted, than to actually show that the advisor did the analysis properly?

Thus, in practice it may be problematic to entirely eschew The Plan, even if the client never reads it again, because it helps to establish trust in the advisor’s Index Card of subsequent recommendations. Just because the client doesn’t continue to reference The Plan later doesn’t mean producing the plan was useless. Because it may have been necessary for the client to see the plan, and the work that was done, in order to trust the advisor’s recommendations enough to never need to look at The Plan again!

Or stated more simply… the physical financial plan isn’t just about the analysis of the plan itself. It is a tool for establishing the advisor’s credibility and trustworthiness, too! Which means at a minimum, advisors who don’t want to produce full plans will need to have other strategies in place to substantiate the client’s trust.

The Financial Plan As A (Crucial) Conversational Piece

The second function of a (physical) financial plan is that it helps to support financial planning conversations – not just about what the financial advisor recommends to the client and why, but about what’s possible for the client in the first place.

After all, the reality is that most of the time, if you simply ask a prospective client “What are your financial goals?” they can’t actually articulate their goals very well in the first place. At best, they may volunteer some numbers or loose goals – “I’m hoping to retire at age 65 with $1,000,000!” But deeper follow-up questions quickly reveal the looseness of the goal. Why age 65? Because that’s when most people retire at their company (and not for any bona fide personal reason). Why $1,000,000? Because it seems like a nice round number… that may or may not bear any real relationship to what they actually need to afford their retirement lifestyle (as it could have been $800,000 or $1.2M instead). In fact, often the answer to the question of “When do you want to retire, and with how much?” is “I don’t know. That’s why I hired a financial planner to figure it out!”

In other words, a key aspect of the financial planning process is “goal discovery” – to figure out what’s even possible for the client to pursue in the first place. In this context, the financial plan becomes a conversational piece about goals – starting with some baseline goal the client has stated, and then illustrating what financial planning goals are actually possible, and which are not, in turn inviting additional What-If scenarios as the client evaluates the prospective trade-offs to decide which path to pursue.

Which means without the financial plan, the client may not have enough to clearly visualize what is possible, in order to evaluate their trade-offs and choose their goals. Which makes it impossible to proceed to the final stage of making recommendations in the first place!

Moving Beyond The Physical Financial Plan?

So what does all this imply about moving beyond the physical financial plan to a One Page Financial Plan approach?

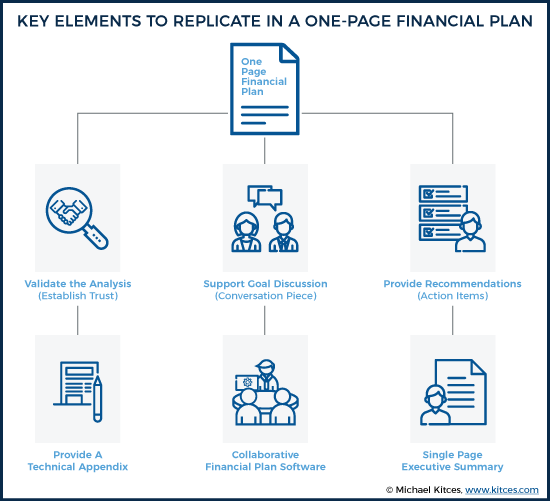

At a minimum, if the role of a physical financial plan is a combination of trust-building, conversation, and providing actual action items and recommendations, it means that just providing a one-page financial plan or the proverbial (or literal) Index Card of recommendations alone won’t be sufficient. Because it doesn’t address the other roles of the physical plan.

Instead, what it suggests is that even if the focus shifts to a one-page financial plan, the financial advisor still has to either: a) establish enough trust to validate that the plan is “right” even without “proving” it with the supporting materials; or b) at least provide the supporting plan details in the form of a technical appendix or some supplement to the one-page plan. Or viewed another way, more experienced financial advisors whose experience alone conveys greater credibility and trust may find it easier to minimize the physical financial plan, while those younger or newer advisors who are still trying to establish their credibility will likely struggle more in moving away from the physical plan. And those who have stronger communication skills and are more effective at showing empathy to build trust may find it easier to “just” deliver recommendations, compared to those who need the plan to demonstrate their expertise and credibility.

Similarly, even without the physical financial plan, it’s still necessary to have some means to facilitate a discussion about financial planning goals, trade-offs, and evaluating the possibilities in the plan. The good news in this regard is that as financial planning software becomes more collaborative in nature, and shifts from something that advisors have in their office (to do analysis) to being in their conference room instead (to use live and interactively with clients), it is increasingly feasible to use the financial planning software itself to facilitate financial planning discussions, rather than using “The Plan”. Although it does require a higher level of mastery of the financial planning software to be able to use it live and interactively with clients in the first place – who will see immediately if the advisor is making mistakes and cannot figure out how to use their own software!

Which means the construction and the delivery of the financial plan may simply need to be reshaped to a process that pushes the collaborative use of the financial planning software to the forefront, with the supporting plan details printed (later) for supplemental support (to validate the plan), and reducing the bulk of The Plan itself to little more than the recommendations and action items that emerge out of the collaborative planning session.

Or viewed another way, the physical financial plan may not be able to be fully eliminated, per se, but it can be replaced with an alternative means to address the key issues and roles that it currently fulfills.

Getting Paid For A One Page Financial Plan Requires Real Planning Knowledge

The transition of getting paid for The Plan, to getting paid for a One Page Financial Plan, is essentially about the shift from getting paid for The Plan to getting paid for the financial advisor’s planning knowledge and knowing where to apply it – akin to the handyman who is paid not for the nail, but knowing where to hammer it. With the caveat that validating the value of an intangible (and long-term) service like financial planning is far more challenging than the immediately provable outcome that a well-placed nail will quiet the creaky floorboard.

However, it’s important to recognize that this necessitates the financial advisor actually having the knowledge to impart in the first place! In other words, the reality for many advisory firms is that producing The Plan was/is a way to demonstrate at least some planning value in the absence of having any well-trained financial advisors. Because the value was literally created by the analytical capabilities of the software, not of the financial advisor, and the “advisor’s” value is giving access to the output of the software. Given the sales-based roots of financial advisors, this isn’t entirely surprising; historically, the financial advisor wasn’t paid to sell their own knowledge, because it was easier and more straightforward to simply sell The Plan as though it were a product (along with the other products that came at the time of implementation).

In other words, getting away from The Plan requires actually having the knowledge of CFP certification as a baseline, and ideally a post-CFP designation/specialization as well, to be able to demonstrate value beyond just what’s printed out in The Plan. That’s why the handyman can charge $100 for placing the nail, but the salesperson at the hardware store can only sell the $1 nail. And why a CFP certificant can charge for their financial planning advice, but a salesperson can only charge for The Plan itself.

The bottom line, though, is just to recognize that on the one hand, there is a real opportunity for value creation beyond just producing and delivering The Plan that few clients will ever read after the financial planning meeting anyway. Yet even though many experienced financial planners probably could reduce most planning recommendations to a series of simple bullet points on a one-page financial plan (or an Index Card), doing so is not necessarily sufficient to actually get paid (well) for financial advice. Instead, it’s still necessary to have a means to engage the client in meaningful conversation about their goals and trade-offs, and to establish the trust and credibility necessary to validate that the recommendations really are the result of bona fide expertise. Only then can the financial planner actually get paid not just for The Plan, but for the actual financial planning advice.

So what do you think? Do you get paid for The Plan, or your financial planning advice? Do you think you could get paid to reduce your entire financial plan to a single page of recommendations? Have you already tried it? Please share your thoughts and experiences in the Comments below!