Executive Summary

The Tax Cuts and Jobs Act of 2017 made substantive changes to the Internal Revenue Code and in the process, created several new provisions, including “Qualified Opportunity Funds” (QOFs), which were designed to encourage taxpayers to invest in certain low-income (and also newly created) “Qualified Opportunity Zones” (QOZs) by offering some particularly unique (and potentially potent) tax benefits. Specifically, by investing into a QOF, a taxpayer gains the ability to defer taxes from the sale of any asset (including intangible assets like stocks), as long as the portion of the proceeds attributable to the capital gains on the asset that’s been sold are reinvested into a QOF within 180 days. Moreover, the portions of those deferred capital gains reinvested into the QOF are eligible for potentially two partial basis increases (once after five years and again after seven years), and if the investors hold the QOF for at least ten years, then all of the tax attributable to the gains of the QOF, itself, are completely eliminated if the QOF is sold.

Of course, such tremendous tax benefits don’t come without potentially prohibitive caveats, and there are many when it comes to QOFs. Specifically, capital gains on the sale of an asset that aren’t reinvested (on a timely basis) into a QOF by December 31, 2019 (a little over 4 months from the date this article was published) won’t be eligible for all of the available basis increases. Moreover, any still-deferred gain will become taxable either when the QOF is sold, or at the end of 2026 (whichever comes sooner).

Older potential QOF investors, or those with predictably shorter life expectancies, should also be aware of the disadvantages to beneficiaries who inherit a QOF. Typically, assets originally purchased with non-retirement funds receive a “step-up” in basis upon the death of the owner, giving the beneficiary the opportunity to sell the asset with little to no tax consequence. However, the gains that were originally reinvested into a QOF do not receive a step-up in basis, but instead, become income in respect to a decedent (IRD). Which means that QOFs tend to make poor estate planning vehicles, particularly when compared to other potential options. Plus, given the forced inclusion of any still-deferred gain at the end of 2026 and the extremely illiquid nature of QOFs, a beneficiary with limited other financial resources could find themselves between the proverbial “rock” and “hard place."

Ultimately, the key point is that for many older investors (or younger investors with shorter life expectancies), there may be better alternatives than a QOF, especially when considering the potential benefits, or lack thereof, for their heirs. Some of these include, not selling the asset in the first place (and waiting instead to simply bequest an appreciated asset, which will eventually receive a step-up in basis), maintaining the eligibility for a step-up in basis by using a 1031 exchange (but only in the case of real property), or making use of a charitable trust. Although QOFs do offer several unique and useful tax benefits that can’t be found in any other vehicle, older investors, in particular, should look carefully at more mainstream gain management strategies before going down the QOF road.

Why Opportunity Zone Funds Make Lousy Estate Planning Vehicles

In December of 2017, the Tax Cuts and Jobs Act (TCJA) made dramatic changes to the Internal Revenue Code, the likes of which had not been seen in more than 30 years. The law repealed some parts of the Tax Code, modified others, and created a substantial number of new provisions of the Internal Revenue Code (IRC) as well.

Among the newly created provisions of the IRC are “Qualified Opportunity Funds” (QOFs). These funds, by virtue of their numerous potential tax benefits, have received a significant amount of coverage in the financial media since their creation. In addition, commercially available QOFs are now being heavily marketed by some companies. Thus, investors are becoming increasingly aware of QOFs as an investment option.

But while QOFs may present an incredible opportunity for some investors looking to liquidate assets with existing gain, older investors in particular may wish to think twice before selling appreciated assets and reinvesting the proceeds into such funds. Because simply put, QOFs make rather poor estate planning vehicles when compared to other options.

What Are Qualified Opportunity Funds?

In addition to QOFs, “Qualified Opportunity Zones” (QOZs) are a new entrant into the tax-planning parlance created by the TCJA.

QOZs are low-income (as defined by IRC Section 45D(e)) census tracts (and a limited number of certain contiguous [connected] census tracts) that have been specially nominated as such by the state, the District of Columbia, or the U.S. territory in which they are located. The “final” list of over 8,700 zones was published by the IRS on July 9, 2018, in IRS Notice 2018-48 (there were two additional zones in Puerto Rico added in July 2019), and a downloadable and sortable spreadsheet of the zones is maintained by the Treasury Department’s Community Development Financial Institutions Fund.

In turn, Qualified Opportunity Funds (QOFs) are partnerships or corporations that are created to invest (primarily) in businesses and tangible property located within QOZs. These funds represent the latest efforts by Congress to encourage growth and development of low-income areas by providing various tax breaks.

Qualified Opportunity Funds Offer Substantial Tax Benefits (For Reinvested Gain)

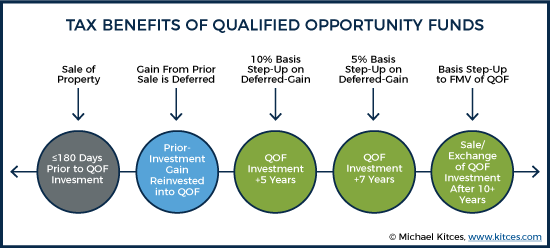

There are three primary tax benefits associated with QOF investments made with timely reinvested gains from the sale of previous investments: tax-deferral of existing gain; basis step-ups of existing gain; and tax-free gain of the QOF investment, itself. Notably, however, these benefits are only available to the extent that gains are timely (more on this below) reinvested into a QOF.

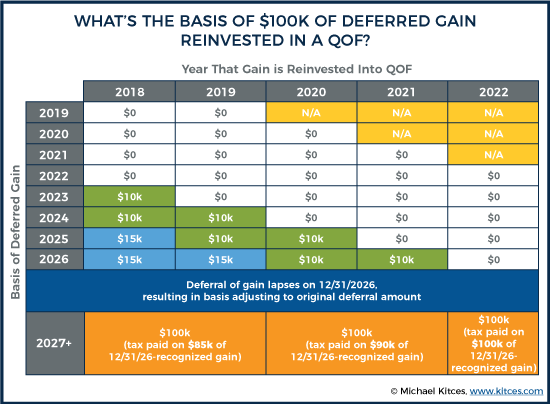

Under IRC Section 1400Z-2(a)(1)(A), gain that is reinvested into a QOF within 180 days of the sale or exchange creating such gain may be deferred (such deferral is an election to be made by a taxpayer). And per IRC Section 1400Z-2(b)(1), that deferral lasts until the earlier of December 31, 2026, or the date on which the QOF is sold or exchanged. Thus, absent any further changes to the rules by Congress, the latest the gain reinvested into a QOF can remain tax-deferred is 2026.

Example #1: On January 26, 2019 Paula sold a building for $2.4 million. At the time, her adjusted basis in the building was $1.4 million. In an effort to minimize the tax impact from her sale, Paula reinvested only the $1 million of gain into a QOF on March 31, 2019 (she invested the proceeds consisting of her return of basis elsewhere). Since her gain was reinvested within 180 days of the sale, Paula can defer the $1 million gain until December 31, 2026, or until she sells or exchanges the QOF, whichever comes first.

The second major tax benefit afforded to QOF investments made with timely reinvested gain is a series of basis step-ups. More specifically, IRC Section 1400Z-2(b)(2)(B)(iii) calls for a basis increase equal to 10% of the still-deferred gain after a QOF has been held for five years, effectively turning 10% of the tax-deferred gain into a tax-free gain. IRC Section 1400Z-2(b)(2)(B)(iv) calls for an additional basis increase of 5% of the still-deferred gain after the QOF has been held for an additional two years (a total of seven years). Thus, the tax liability on up to a maximum of 15% of the reinvested gain can be “erased” via the combination of these step-ups.

Example #2: On March 31, 2019, the gain that Paula reinvested into the QOF has an initial basis of $0. If she holds the QOF for five years, through March 31, 2024, her basis will increase to $100,000 (10% of $1 million). If she continues to hold the QOF for an additional two years, through March 31, 2026, her basis will increase to $150,000 (15% of $1 million).

But there’s a catch. As noted, the step-ups only benefit reinvested gain that is still deferred. But as also noted earlier, the latest that deferred gain reinvested into a QOF must become taxable is on December 31, 2026 (at least, if the current rules do in fact lapse then). Thus, to meet the seven-year requirement needed to get the second step-up (of 5%), an individual must make their QOF investment by December 31, 2019!

QOF investments made after that date won’t be eligible for the 5% step-up, but investments made between January 1, 2020 and December 31, 2021 will still be eligible to receive the 10% step-up after five years. Any gain reinvested into a QOF after that time, though, will not be eligible for any basis increases.

The third and final major tax benefit available when gain is timely reinvested in a QOF is the potential for all “gain on gain growth” of the QOF, itself, to be tax free. Per IRC Section 1400Z-2(c), this benefit is only available to QOF investors who have held their investment for ten years or longer. But if such an investor does meet the 10-year requirement, then the investor’s basis in the QOF will be equal to the fair market value of the QOF on the date the QOF is sold or exchanged (assuming that only the prior-investment gain was originally reinvested into the QOF).

Example #3: Paula decides that she will keep her QOF investment, which she purchased on March 31, 2019, until 2030. On December 31, 2026, the deferral of her $1 million gain will lapse, and she will owe tax on $850,000 ($1 million – $150,000 from the 10% step up in 2024, and the additional 5% step-up in 2026) of capital gains. At that point, her new adjusted basis will increase to $1 million, the amount of the gain originally deferred.

On January 1, 2030, when Paula plans to sell her QOF investment, she will owe no capital gains tax because, since she had held the QOF for ten years, her basis will adjust on the date of sale to the fair market value of the QOF.

Finally, it’s worth reiterating that, perhaps somewhat oddly, each of the above-referenced potential QOF-related tax breaks is only available when gain from the sale of a prior investment is timely reinvested into a QOF. By contrast, investments attributable to basis receive none of the same tax benefits. (Thankfully, though, any basis from the sale generating the to-be-reinvested-in-a-QOF gain can be “split” out from the gain, “pocketed” tax free.)

Tax Treatment of Qualified Opportunity Funds Upon Death

While QOFs can offer investors a slew of tax benefits, they aren’t nearly as attractive, from a tax perspective, to beneficiaries.

More specifically, when a beneficiary inherits a capital asset purchased with non-retirement funds, they generally receive a “step-up” in basis upon death of the owner. This “step-up” makes the beneficiary’s basis in the property equal to the fair market value on the previous owner’s date of death. Thus, a beneficiary is generally able to sell such an asset with little to no income tax consequences (shortly) after acquiring the asset.

Deferred gain that is reinvested in a QOF, however, is not eligible for a subsequent step-up in basis upon the death of a QOF owner. Instead, it becomes income in respect of a decedent (IRD) by means of IRC Section 1400Z-2(e)(3), which states:

“In the case of a decedent, amounts recognized under this section shall, if not properly includible in the gross income of the decedent, be includible in gross income as provided by section 691.”

As such, if a beneficiary inherits a QOF, with regard to any still-deferred reinvested gain, the beneficiary will essentially “step into the shoes” of the original owner, and will owe income tax on that still-deferred gain in the same manner, and at the same time, as if the owner were still living. Thus, any beneficiary inheriting a QOF prior to December 31, 2026 will, at best, only be able to retain the deferral on reinvested gain until that date (since that is when the QOF owner would have been required to recognize any still-deferred gain, had they lived)… but not receive a step-up in basis as the beneficiary would with any other inherited property.

Notably, though, it would appear that the beneficiary would get a step-up in basis for any gain attributable to the QOF investment itself (i.e., the gain-on-timely-reinvested-gain), though there is still some uncertainty regarding the issue.

In fairness, taken together, these rules don’t make QOFs a poor choice for older investors who must later sell the asset, or who are 100% committed to doing so regardless of the tax consequences for themselves or their heirs. Rather, as discussed in greater depth below, it’s more that in many situations, QOFs are just less attractive than other options, at least from a tax perspective, if the QOF is an asset anticipated to be bequeathed to heirs.

Example #4: Paula, who reinvested $1 million of gains from a building sale into a QOF on March 31, 2019, has died on August 2, 2024. Upon her passing, Connor, Paula’s son, inherited her QOF which, on the date of her death, was fairly valued at $1.15 million ($150,000 gain in the $1 million of gains that had been reinvested into the QOF). Since Paula died after owning her QOF for five years (but not seven), prior to her passing, she would have received a basis increase equal to 10% of her initial investment in the QOF ($100,000). That basis would be carried over to Connor. And in addition (it seems as though) Connor would receive a step-up in basis of $150,000 for the gain of the QOF, itself, since Paula’s investment. Which would bring Connor’s total cost basis to $100,000 + $150,000 = $250,000.

That, however, leaves Connor with $1.15 million - $250,000 = $900,000 of still-deferred gain at the time of his inheritance. If Connor holds the QOF until the 7-year mark (counting Paula’s holding period) is reached, he will be eligible for an additional $50,000 increase in basis (5% of the initial gain timely reinvested), but that’s the best Connor can do.

Thus, in a best case scenario, Connor will ultimately have to pay tax on $850,000 of long-term capital gains, even though any other appreciated property Connor might have inherited would have no capital gains at all. And as noted above, that tax bill will arrive no later than December 31, 2026.

(Note: Beneficiaries of very affluent decedents, whose estates were subject to Federal estate tax, will have the impact of the recognized capital gains partially ameliorated due to the fact that an IRD deduction will offset some of the gain.)

Some Good News For QOFs: Death Is Not An “Inclusion Event”

Although the lack of a step-up in basis on reinvested gain is a significant downside of QOFs from an estate planning perspective, the good news at least is that the IRS has proposed that death will not result in previously deferred QOF gains to be included in an investor’s income. In other words, QOF gains can at least transcend death and carry over to the beneficiary, rather than simply being due at the death of the original owner.

The reason that QOF gain can at least carry over to a beneficiary is that, as discussed earlier, timely reinvested gain can be deferred until the earlier of December 31, 2026, or when the QOF is “sold or exchanged”. But in limiting the language in IRC Section 1400Z-2(b)(1) to “sold or exchanged”, Congress ignored the potential for QOFs to “change hands” via other methods, such as by gift, charitable contribution… or by bequest upon the (QOF) owner’s death.

As is often the case, the IRS was left to fill in these gaps via Treasury regulations, which they did by creating the concept of an “inclusion event”. An inclusion event is merely an action that has the effect of treating a QOF as if it were “sold or exchanged”, thus ending the tax deferral of gain (and triggering any other QOF tax consequences that may apply upon disposition).

In a Proposed Regulation published on May 1, 2019, the IRS provided taxpayers with a nonexclusive list of situations that qualify as inclusion events. The general rule provided by the proposal is that any receipt of property (from the QOF) treated as a distribution for Federal income tax purposes, or any transfer that reduces the QOF owner’s equity interest in the QOF, will be considered an inclusion event.

Normally, the bequest of a QOF would be a transfer that reduces the decedent’s (or the decedent’s estate’s) equity interest in a QOF. Nevertheless, under Proposed Regulation 1.1400Z2(b)-1(c)(4), the IRS explicitly provided an exception to the general inclusion event rules for transfers made on account of a QOF owner’s death. Specific examples of death-related transactions that are excluded from general inclusion events are a decedent’s QOF transferring to their estate, the estate distributing the QOF to beneficiaries, and a jointly held QOF passing to the other joint owner(s) by operation of law. So, while gifting or selling a QOF immediately ends its tax deferral period, bequeathing a QOF to a beneficiary will not. A beneficiary who inherits a QOF will be able to continue deferring taxes on the QOF gain until an inclusion event takes place (such as a sale or exchange), or until December 31, 2026 – whichever comes first.

The Illiquidity Of Qualified Opportunity Zone Funds May Create Tax Issues For Beneficiaries

Example #4 above, in which Connor inherits a QOF with still-deferred gain, raises an interesting question… “What happens if a beneficiary of a QOF investment has limited financial resources outside of the QOF and December 31, 2026 comes around?” Since December 31, 2026 is the absolute latest date that gain reinvested in a QOF can remain deferred, a beneficiary who inherits a QOF must have a plan for paying the tax liability on the to-be-recognized amount, even if the QOF itself is not liquid at that time!

And chances are, limited liquidity is going to be the case. By virtue of their very nature of investing into long-term not-very-liquid real estate (and often real estate that wasn’t attracting many other investors, thus why it needed QOF tax incentives to get any investment at all), QOFs will typically be highly illiquid investments. Plus, since one of the “core three” tax benefits of investing in a QOF is the tax-free “gain on gain” growth of the QOF (which is only available after an investor has owned a QOF for 10 years), these investments are generally intended to have lifecycles of a decade or longer.

Example #5: Recall Paula, from our previous examples, who sold a building for $2.4 million and timely reinvested her $1 million gain on the sale into a QOF. Further recall that Connor, her son, was the beneficiary of Paula’s QOF upon her passing in 2024, and at best, is slated to owe long-term capital gains on $850,000 of IRD on December 31, 2026.

Perhaps in addition to the QOF, Connor also inherited $1 million or so of other, liquid assets. If so, assuming Connor continues to hold the QOF through December 31, 2026, he can “save” some or all of those liquid assets to cover the tax bill that will be owed on the forcibly-recognized gain.

What if, however, Paula left her liquid assets to other beneficiaries? Or what if Paula spent through most of her liquid assets during the final years of her life and there was little other than the QOF to pass on? If Connor isn’t independently wealthy, himself, how is he going to cover the tax bill on $850,000 of gain!?

Note that this issue is not shared with other common items of IRD, like IRAs and other retirement accounts. While such assets are IRD and thus, subject to income tax, that income tax bill is only triggered as the beneficiary receives distributions from those accounts. Thus, a beneficiary can account for taxes when the distribution is made, by either withholding taxes from the distribution directly, or simply “putting aside” some of the distribution for the forthcoming tax bill.

This is not the case, however, for a beneficiary inheriting a QOF. Come December 31, 2026 (at the latest), that beneficiary is going to have taxable income, even if they have not received so much as a dime in actual “spendable” money from the inherited QOF asset.

Thus, for beneficiaries with no other way to pay the tax bill, the only option may be to consider selling the QOF on a likely-thinly-traded secondary market. In such instances, a desperate beneficiary forced to sell may only be able to get a fraction of the QOF’s “true value”.

Other Estate Planning Challenges Created By QOFs

You might be thinking that it would still be appealing to roll gains into a QOF, and to just try to dispose of the QOF by some other means before death… but that won’t work, because as noted earlier, while death is not an inclusion event, almost any OTHER type of pre-death estate planning strategy WOULD be! Gifting an interest in a QOF to a child (or other individual) would, for example, be an inclusion event and result in the immediate taxation of any still-deferred gain.

This could be particularly problematic for high-net-worth QOF investors if the current $11.4 million (in 2019, adjusted for inflation) unified estate/gift tax exemption were to be reduced, either as scheduled at the end of 2026, or potentially sooner via Congressional action (which would likely require that Democrats control the House, Senate, and White House, as Republicans would be unlikely to support any such proposal).

Because in either case, if it appears that a decrease in the unified exemption amount is imminent, high-net-worth individuals, bolstered by the IRS’s recent guidance that such amounts will not be subject to a “clawback”, will likely look to gift assets out of their estate prior to the scheduled reduction to maximize the current exemption amount (similar to planning that took place towards the end of 2012 when it looked like the $5 million exemption was going to go back to $1 million, even though the $5 million exemption was ultimately extended by the American Taxpayer Relief Act (ATRA) in January of 2013). Except when it comes to QOFs, affluent investors can’t gift them to reduce their taxable estate… at least, not without immediately triggering the QOF gain, due to the inclusion event rules.

In addition, the Proposed Regulations make clear that the inclusion rules apply to “gifts” made to both taxable and tax-exempt donees. As a result, any charitable contribution of a QOF, including a transfer of the investment to a charitable trust(!), will result in an inclusion event for that owner. And while a deduction for a charitable contribution may, indeed, offset most of the impact on a QOF owner’s taxable income (i.e., the inclusion event triggers QOF gains, but then the charitable contribution produces a deduction to largely offset those gains), that charitable contribution would not do anything to reduce the inclusion event’s impact on a taxpayer’s adjusted gross income (AGI), on which many income-sensitive benefits (i.e., credits, deductions, etc.) and costs (i.e., Medicare Part B/D premiums, the 3.8% Obamacare surtax, etc.) are based.

And perhaps even more concerning for some QOF owners is that there appears to be no exception to the inclusion event rules for gifts made to a spouse! Thus, such intra-couple spousal transfers, which are commonly made for estate planning and Medicaid planning purposes to shift assets or equalize estates, cannot be completed without triggering the income tax on any still-deferred gain.

How Other Tax Deferral Strategies Offer Superior Estate Planning Benefits

While QOFs offer some attractive benefits, because a “full” step-up-in-basis-upon-death is not one of those benefits, older investors should first give at least some consideration to other tax-deferral approaches that offer better tax benefits for heirs after their death. Some alternate options may make more sense than investing in a QOF, and are discussed below.

Simply Skip The QOF Opportunity And Wait For A Step-Up in Basis

One obvious “strategy” is to do nothing...not out of laziness, but by choice. While an individual may wish to sell an appreciated asset because they believe a better investment option exists elsewhere (or they just no longer believe in the merits of their current investment), in some cases it may pay to hold on to the investment anyway, allowing heirs to receive a step-up in basis at death.

Certainly, it’s important not to let “the tax tail wag the investment dog”, but at the same time, it’s also foolish to look only at the potential gross return of an investment without evaluating the tax consequences of making it (or changing it) in the first place. To that end, and while each situation must be evaluated based on its own unique set of facts and circumstances, the following general statements can be used to help guide an investor with appreciated assets towards the best decision.

- The higher an individual’s tax rate, the more holding an asset until death makes sense rather than changing and deferring gain into a QOF opportunity.

- The greater the built-up gain in an investment, the more holding an asset until death makes sense.

- The older the individual and/or the shorter an individual’s life expectancy, the more holding an asset until death makes sense.

- The smaller the gap between the expected return of the new investment and the expected return of the old investment, the more holding an asset until death makes sense.

Use A 1031 Exchange To Keep The Step-Up “In Play” For Sales Of Real Investment Property

Another potential strategy for older investors looking to sell highly appreciated business or investment property is the use of a 1031 exchange. A 1031 exchange, named after the IRC Section 1031 that authorizes it, is a special transaction that allows an investor to sell one investment and replace it with another “like-kind” investment while continuing to defer gain.

Notably, though, the deferral of gain via a 1031 exchange offers two key benefits as compared to the reinvestment of gain in a QOF. First, there is no end date on the continued deferral of gain provided via a 1031 exchange. Thus, unlike a QOF, which forces recognition of any previously unrecognized gain by December 31, 2026, the 1031 exchange can indefinitely defer the gain on a previously sold investment.

Second, and of even greater importance in the context of estate planning, a 1031 exchange does not create IRD for a beneficiary if the owner of the exchanged property dies. Rather, the beneficiary receives a full step-up in basis on the property. From the beneficiary’s perspective, it would be as if the exchange had never occurred, with the same step-up that would have been available on the original asset.

It should be noted, however, that since the passing of the TCJA, the 1031 exchange is only available for sales/purchases of like-kind real property. Thus, an investor with highly appreciated stock, or cryptocurrency, cannot use a 1031 exchange to defer the gains on the sale of such investments.

Use A Charitable Lead Trust In Lieu Of A QOF

For owners of highly appreciated investments who also have a charitable streak, the use of a charitable trust may provide a superior tax minimization and estate planning alternative to the use of a QOF. Such trusts might include charitable remainder trusts (for owners primarily looking to enjoy income from their investment during their lifetime), or, in the case of individuals of an advanced age primarily concerned about providing for beneficiaries, a charitable lead trust.

Charitable trusts offer the potential benefit of an upfront tax deduction that can alleviate the impact of taxes on other income. Further, once the asset to be sold is moved into the trust, the trust can sell the asset, and replace it with just about any other type of investment, providing the trustee with maximum flexibility.

Qualified Opportunity Funds are an interesting new arrow in the quiver of the tax and financial planner. They provide a trio of tax benefits that an individual likely cannot replicate via any other available investment and, therefore, deserve strong consideration from individuals selling assets with significant gain.

But QOFs are not the end-all and be-all for individuals holding assets with significant gains -- other options must be considered. Perhaps nowhere is this truer than for investors nearing the end of their life expectancy.

The loss of a step-up in basis on reinvested gain for the original QOF owner, combined with a forced tax bill on a likely illiquid asset for a potentially unsuspecting or ill-prepared beneficiary, tends to make QOFs a rather poor investment vehicle to own at death. And that’s to say nothing of the other estate planning challenges created by the inclusion events outlined in the IRS’ proposed regulations. As such, older investors, in particular, should carefully evaluate other potential gain management strategies, including simply “holding tight” and doing nothing (and waiting for a step-up in basis), before making the leap to become a QOF investor.

https://youtu.be/SybLY3BhquI

Thanks for an interesting article. Since the IRS has proposed that death is not an inclusion event, would an effective estate strategy for a charitably inclined QOF owner be designating a 501c3 charity as the QOF beneficiary? Would a DAF be an allowed 501c3 beneficiary? Thanks.