Executive Summary

The typical client meetings conducted as a part of the financial planning process are challenging. It starts with data gathering, but clients can’t easily produce the needed data to analyze the situation. Clients are asked about their goals, but often articulate ones that will just result in a plan that “fails”. And the whole process culminates in a physical printed plan output that most advisors agree is rarely read by clients anyway.

Even worse, from the client’s perspective – since they don’t see much of the behind-the-scenes work that happens – financial planning is little more than providing data to the advisor, and getting printed planning software output in response. As though a financial advisor does little more than software data entry!

So in a world where the goal is to get clients to actually value each meeting of the financial planning process – rather than simply having it be a data-gathering-for-software-output experience – how could each meeting in the financial planning process be reimagined to be more relevant, more collaborative, more interactive, and more immediately and tangibly valuable?

Getting Compensated For The Typical Financial Planning Process?

The recent “2015 Trends In Financial Planning” study from the FPA’s Research & Practice Institute interviewed over 750 financial planners to understand how financial planning is delivered today.

The results of the study indicated the “typical” financial planning process is:

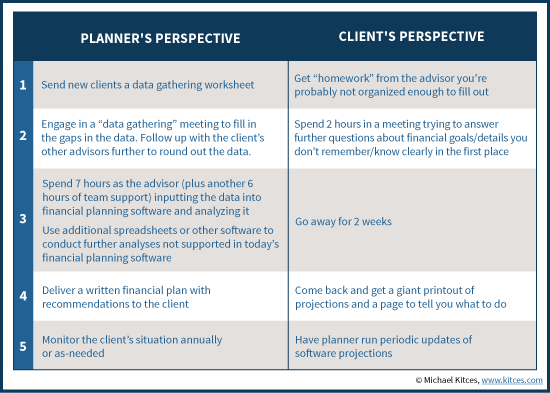

1) Send new clients a data gathering worksheet

2) Engage in a “data gathering” meeting to fill in the gaps in the data. Follow up with the client’s other advisors further to round out the data.

3a) Spend seven hours as the advisor (plus another six hours of team support) inputting the data into financial planning software and analyzing it

3b) Use additional spreadsheets or other software to conduct further analyses not supported in today’s financial planning software

4) Produce a paper report printout of the plan and deliver it to the client

5) Monitor the client’s situation annually or as-needed

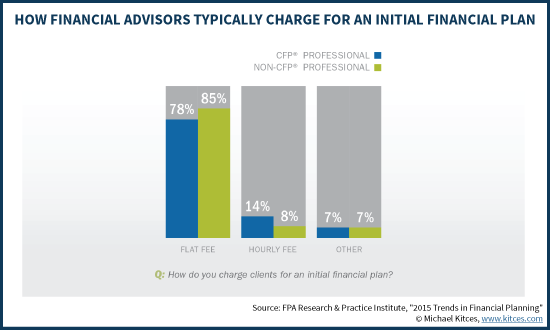

The financial outcome of this process for the advisor – after nearly 20 hours of cumulative work between the data gathering meeting, software analysis, and presentation of the financial plan report – is a flat financial planning fee averaging around $2,000 to $3,000 (which amounts to just over $100/hour for the advisor’s time). And in 1/3rd of those cases, the fee is further discounted if the client chooses to implement. If the planner even charges for financial planning at all.

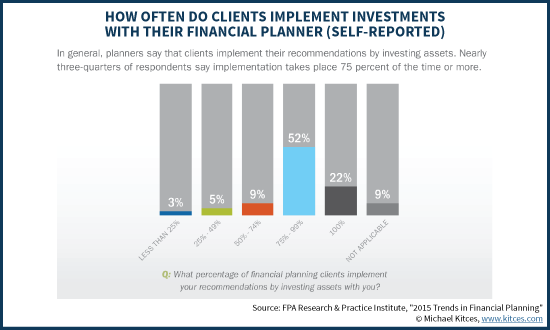

Ironically, even though it’s so challenging to get paid for financial planning, a whopping 75% of advisors still report that clients who received financial planning are more profitable. Though clearly this is not driven solely by the financial planning fees paid. Instead, it seems to be driven by the fact that the overwhelming majority of clients who go through the financial planning process end out implementing investment strategies with the advisor beyond just the planning fee!

In other words, it’s still the case that most financial planning is at least partially paid for ‘indirectly’ through investment management or product sales as a part of the implementation process!

Is The Typical Financial Planning Process Even Worth Paying For?

While from the advisor’s perspective, the typical financial planning process often feels laborious and time-intensive (and a struggle to get paid for the time it takes), it’s notable that the client’s experience may be even worse! After all, much of what happens in financial planning is ultimately behind the scenes from the client’s point of view.

Which means that when it comes to the client’s perspective and interactions, the financial planning process is:

1) Receive “homework” that you’re probably not organized enough to fill out from the advisor

2) Spend two hours in a meeting trying to answer further questions about financial goals/details you don’t remember/know clearly in the first place

3) Go away for two weeks

4) Come back and get a giant printout of projections and a page to tell you what to do

5) Go through the process again to get updated software projections as “needed”

In other words, from the client’s perspective, financial planning amounts to little more than trying to give an advisor a bunch of data, and having the advisor come back with a printed report. Or viewed another way, the financial planner is operating as little more than a glorified data entry device to put the client data in and get the software output in return!

Accordingly, then, it is perhaps no surprise that it continues to be a struggle for most financial advisors to get paid on a standalone basis for financial planning. Ironically, in many situations the planner isn’t even substantively getting paid for his/her own advice – it’s literally nothing more than the sale of the financial planning software output! In other situations, the planner perhaps adds something to the process when conducting the analysis and crafting the recommendations, but from the client’s perspective the bulk of the experience still centers around providing data to the planner and getting a printed report in return.

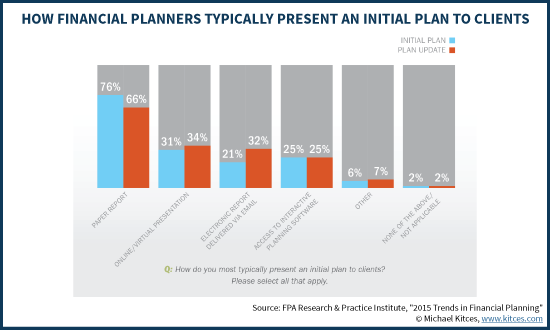

To say the least, the meetings that the client attends are not exactly a central part of the value (even that’s the primary experience of the client!). In fact, the experience tends to be remarkably one-sided, with the advisor asking the client lots of data questions in the first meeting, telling the client what to do in the last meeting, but not necessarily really engaging the client along the way at all. In fact, the FPA study notes, only 25% of financial plan presentations involve any kind of client experience where the planning software is actually used interactively and collaboratively!

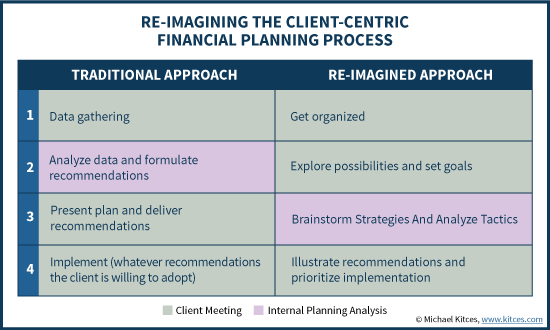

Reimagining A Client-Centric Financial Planning Process

In a world where the “value” of many financial planners ultimately boils down to little more than doing the data entry and “work” necessary to operate financial planning software, it should be no surprise that few clients are willing to pay for it, and many/most who do are very affluent (where their time is so valuable they’re willing to pay an advisor to take the data, input it, and operate the software for them!). And in point of fact, as more and more direct-to-consumer software solutions become available, it may only be a matter of time before consumers really can do the software part themselves, making this aspect of the financial planning process wholly irrelevant and value-less!

So if we were going to re-imagine the financial planning process to be more useful and relevant from the client’s perspective, what would it look like?

Get Organized

The starting point would be to recognize that most people aren’t particularly financially organized in the first place. Those who are already highly organized are probably more likely to be self-directed in their financial strategies and behaviors in the first place. While some clients might already be well organized, for most the first step of the process would simply be helping them to get organized, so it’s even possible for them to take the next step in the financial planning process.

Notably, this might also be an opportunity for us, as advisors, to gather data from them – in the process of helping them to sort out their own financial lives – but from a client-centric perspective, the first meeting should be a “Get Organized” meeting!

This could include both helping the client to get physically organized (e.g., providing them an actual personal organizing file system), using online tools to help (e.g., signing up the client for a personal financial management [PFM] software tool), and helping the client to visually construct a full picture of their financial situation (e.g., with mind-mapping tools).

Explore Possibilities And Set Goals

Once the client is actually organized and has an understanding of their current financial situation, it’s time to help the client imagine what possibilities the future could hold. In other words, just as few clients are really already financially organized, even fewer have any idea what their financial goals really are. So going immediately from gathering financial data to gathering goals is useless.

So the second meeting of the planning process, from the client perspective, would be to “Explore The Possibilities” using financial planning software interactively to understate what could be, and what the tradeoffs may entail in pursuing various alternative scenarios. That allows the client to even figure out what the goals realistically could and should be. And contingency plans can be formed about what would realistically need to be done to stay on track if a problem arose.

Brainstorm Strategies And Analyze Tactics

The fact that this “extra” meeting occurred – already beginning to use financial planning software – in order to explore possibilities and set realistic goals before beginning the “analysis” stage now makes the job of the financial planner far easier to brainstorm appropriate financial planning strategies and analyze specific tactics to consider. No longer is there a risk of analyzing the data and constructing plan recommendations that turn out not to be viable because at the plan presentation meeting, it turns out “the plan” doesn’t work, and/or the client doesn’t want to proceed until looking at more/alternative scenarios.

Instead, it’s already known that the current goals are at least “somewhat” realistic and feasible. It’s just a matter of crafting recommendations about the best way to get there, and what tools and techniques would be implemented to do it - which is where the planner’s expertise is highly relevant, whether it’s suggesting portfolio changes or a new insurance policy, shifting savings to a retirement account or engaging in a Roth conversion.

Illustrate Recommendations And Prioritize Implementation

The next and final meeting is where the crafted recommendations - specific tactics and action items - can be illustrated to the client, to show how each recommendation further improves the path towards achieving the stated goals (and provides the opportunity for the goals to be tweaked further, given the positive impact of the advisor-recommended tactics).

Notably, there really is no need to present a formal “plan” at this point, since the output of the typical financial plan was already explored interactively in the second meeting. And in point of fact, in this meeting the financial planning software tools would likely be used interactively again, to educate the client and illustrate before/after outcomes of the specific financial planning recommendations. This provides the client an opportunity to understand exactly how each recommendation would work and the benefit of the tactic, decide whether/which ones to proceed with, and to prioritize which recommendations will be implemented first (since clients cannot possibly implement every recommendation all at once!).

The goal by the end of the meeting is for the client to be committed to taking action on the top 1-2 recommendations that can be executed in the coming months (and then engage in the next meeting to decide what to tackle next!).

A Three-Meeting Financial Planning Process

Ultimately, this three-meeting planning process – Get Organized, Explore Possibilities And Set Goals, and then Illustrate Recommendations and Prioritize Implementation – may seem very similar to the “traditional” financial planning approach of gathering data, presenting a plan, and following up for implementation. But there are important differences. Planning software is used collaboratively up front to explore possibilities and set the goals, rather than “asking” for the goals and presenting a plan to show how they will turn out (without knowing whether the plan to be presented will even be viable in the first place). Analysis only occurs after the advisor and client collaboratively plan around potential scenarios. And because the plan is already known to “work” from the beginning, the focus of the final meeting is not on presenting “the plan” to see whether it works, but to present (and illustrate) the recommendations and why/how they help, and determining which to implement first/next.

Ultimately, though, the fundamental point is simply that creating value in the financial planning process must move beyond just gathering client data up front and providing the output of financial planning software at the end. It diminishes financial planning to being little more than just glorified data entry – no wonder few clients will pay for it! – and isn’t even a very effective process for actually helping clients to identify their financial goals and how to achieve them. Instead, a truly client-centric financial planning process actually guides clients through a process to get financially organized, explore the possibilities to set realistic and achievable goals, and then formulate the tactics to best reach those goals – while recognizing what clients need to really help them make progress along the way!

So what do you think? Is it time to re-imagine the financial planning meeting process? Is the value you provide to clients in the output of the software, the analysis you do behind the scenes, or the interactive experience you give them in the meeting itself?

Personally love the idea. I am a bit skeptical from the client point of view though. Maybe I am just working with a certain segment of people but I have found numerous times that a lot of client’s don’t really care to stay organized financially. I have spoken to many about the benefits and advantages of different services that can help in that area and most seem excited and do it…but only for a while. Eventually they slip back to not tracking things, not organizing things, etc. In a weird way I have found that a lot of people want us to do data entry for them when to comes to financial planning. Since a lot of people end up doing tedious task’s in their career’s or personal life I have found financial tedious projects always get put on the back burner under the guise of “I’ll do it next weekend/month” or “Were fine right now money wise” etc.

As always, I am sure I could improve my delivery and chat’s when it comes to this topic and maybe that would increase the usage rate for client’s but so far it seems to be a very challenging activity to get client’s to stay on top of. Not to mention that if/when many do stop staying organized, it becomes a sense of embarrassment for them if ever brought up. Almost like a parent giving a child the “disappointed” treatment.

Will stay on track on this topic as I do love the idea and maybe just need to spend more time on figuring out how to implement something like this.

Keep up the great blog!

Hey Michael,

I agree with what you are saying here. My experience has been that there is a strong relationship between those people that are not very organized, but wish they were, and those that want financial planning. In other words, they want us to organize their lives!

So if we have a way to integrate their investments, bill paying, etc., and if we help them set their goals, if we organize their insurance in terms of what, where, how and to whom, and finally have a way to track their progress that shows if they are on track or not, then I think that is of great value.

My number one goal for each of my clients is “financial peace.” That comes from 1) Helping to get them organized and on track 2) Having a way to easily keep them organized, at least on the important things 3) Showing them that they are making progress. 4) Showing you really care and put them first. This takes time but, once they trust you, it means a ton to them.

That last point is most important. For example, I actually encourage my clients to buy rental real estate to help supplement their current and retirement income. Yep, it takes money out of my management but, if they are up for being a landlord, I thinks it is the right thing to do. Once we can tangibly show we put them first, then trust comes.

Perhaps I am rambling, but your post struck a chord with me regarding how my clients too don’t stay as organized as I would like and as focused as they should be. But I feel that is what I am here for.

It will be interesting to see if the next generation of advisors (who didn’t have to come in the agency system way) who are more planning centric may turn this process on its head. In a more planning forward approach rather than an investment management or product sales approach, I perceive this to be less and less of a disconnect between process/experience for our clients.

That being said – I really look at it as a Phase 1 and Phase 2 Planning. Phase 1 is getting the fundamental blocking and tackling done from a financial planning perspective (Is net worth going up or down? Budgeting? Building for first home/retirement/education/specific family goals? Are you a good steward for the resources available to you? Are you employing your resources in a way that isn’t antithetical to what you want in life?) Phase 2 engages the flourishing version of life for clients once the blocking and tackling is done. Then the tables/projections are merely supporting material for the plan, but not the plan itself.

Unfortunately though – software doesn’t move at the speed of simplicity or complexity in the vagaries of life. And while the tools are great in terms of maintain valuable financial tests for clients at the current time or TVM projections for the future, I don’t feel like the software holds the value of the planning process. So much more of the value of the communication with clients comes from the knowledge and experience stuck in the planner’s noggin rather than merely vomiting volumes of tables/projections (which often has a fine patina of dust on it at my next client meeting).

Bravo! My thoughts exactly.

Thanks Garnet! 🙂

– Michael

Michael, Thanks for focusing on this concept of customer-centric financial planning.

I love this idea.

I’m not a planner – I’m the client who doesn’t trust financial advisors. 🙂

Here’s why: I worked with an advisor (CFA) several years ago to lay out some goals and help me figure out a plan. I actually do have my financial life very organized and could lay out a clear budget with all my income and expenses. I’m self-employed, but have a relatively steady income. I was able to share a pretty detailed monthly and annual budget. The planner gathered my info and goals, just as you described. During that meeting, I made it clear to him what my income was and my preference to include long term investment real estate in my plan. Then he went away and created a plan. Which he walked me through in print a couple weeks later.

In it, he had allocated all of my investment portfolio to stocks and bonds, even wanting to sell my investment property to re-invest that principal. He allocated a large portion of my monthly income to the strategies – so much that I would not have been able to pay my mortgage, health insurance and groceries, let alone other “insignificant” budget items like water, heat and electricity.

From my perspective, this supposed financial plan was just a thinly veiled sales pitch and an effort to take over as much of my assets as possible to generate more fees. The real estate wouldn’t make him money, therefore, it was a bad financial strategy (in spite of the profit it generates monthly).

I would have happily taken part in an interactive planning session with him, had it been offered. As it was, I walked away and refused to pay for the plan he had developed, because it was useless to me.

I’m sure most planners are not that bad, but hopefully, hearing about this experience from a customer’s point of view will prove helpful to someone. Financial planning should be interactive, in my opinion.

I concur with many of your comments. I too am mostly a consumer of financial planning services. I am dealing with one planning that followed the scenario described above. In fact, they reviewed some information but said it hadn’t passed compliance review. So they had to come to review it again. The second they came to review, they assumed I could claim both my late wife’s and my social security in retirement. Other assumptions were “off” from what we discussed. The plan still didn’t place their compliance review.

They came back with a another review, still passing their compliance reviews and offered up the big binder, with lots of pages… We reviewed the executive summary, but they quickly wanted to move to their proposal to manage all of my assets, even though I indicated I would be splitting my assets across several managers. The assets included a structured product, that would guarantee me not to lose money. I asked them, of the major part of the binder of financial reports, what should I look at? They said it was necessary… When I reviewed in depth, I knew they hadn’t incorporated latest financial statements that had assets transferring names, they didn’t factor into a scenario that I should see an option with FRA instead of just early retirement at 62.

They even have a tool that was touted by my estate attorney, and another wealth management company – the tool is eMoney (which has been discussed here several times over the past year). I find that eMoney is not better than Yodlee and maybe even Mint. It has poor “AI” — a description that includes “TRANSFER” automatically becomes income. And far too many transactions are captured in the category of Veterinary. You enter detailed budget information and it doesn’t show on the Overview of Spending.

It’s been a week since I asked for recommendations regarding how much down payment should I put on a condo, after several months ago they preliminary plans said I could well afford to pay cash. They have a lot of reports, but the reports from the tool that I want to see, I can’t see them – they are not in the reports pull down for the client. I guess only the advisor can pull those options — it has to do with cash flow in retirement. And when does Investment Income only include rentals from properties? There was nothing modeled about Investment Income from the Financial Portfolio, only that assets values always go up, and that to meet the level of expenses (mostly additional charitable contributions, I could withdraw from asset balances.)

After working with the transactions and reallocating assets, I had to remind them that everything I knew about was in the tool. Even my last call to review my comments about the tool, and what was lacking, and my comments about the plan, or even the investments were done in conference call only, with no option to use the tool collaboratively. Yet it’s a selling point to eMoney.

eMoney has financial priorities, but is the tool geared to help work across those priorities? I don’t think so. In fact while it is nice face in asset aggregation, it suffers the same problem other aggregators do — It can’t allocate properly funds from Oppenheimer that almost describe the fund, placing them in “uncategorized” or something like that (e.g. Oppenheimer Real Estate, or International, and Discovery – how easy is to say Real Estate is Real Estate????? International is broadly International?)

Having just reviewed my assets with four planning and wealth management organizations, as well as filing for a mortgage, I have been told I am very well organized.

Basically in the case of the financial planning, they are part of an Insurance Company, and unfortunately, their investment mix tilts toward a foundation of insurance / annuity products. When I questioned their recommendation about “buying” a life insurance policy, instead of the policy I have today, they said, there option was an option, it didn’t have to be for the amount of the policy or the annual premium.

That’s because most asset managers just use the financial plan as marketing bait. The trick is to find planners that actually do financial planning. It’s definitely a subset of the financial services world out there and I suspect that more and more will be incorporating some of Michael’s ideas in there process.

“Planning” just to do ‘planning’… doesn’t help anyone. One must define priorities and the extent of the problem. Until one defines the problem that the client WANTS to solve… what’s the point of gathering all the data and going through all that work?

Using a client-facing financial simulator is far more helpful. It allows the advisor to showcase their knowledge of the various factors that affect one’s total financial plan. That’s why I use RetirementView from Torrid Technologies. I know, it doesn’t have a monte-carlo analysis and it doesn’t allow you to vary returns from year to year (straight-line calculations only)… but it’s great to show clients the gap in their retirement planning and illustrate what they can do about it. The software allows me to be on the side of the client while the program tells the client the truth, based on the given assumptions. It’s far more interactive and helps me to ‘activate’ my prospective client’s interest… rather than just collecting a ton of data to spit out a report.

We’ve been using the approach outlined here for about 18 months and clients, for the most part, love it. The second meeting is very important, and clients usually become very engaged. Also, the concept of a Monte Carlo Analysis, and how risk and reward and portfolio choices are related, is so much easier for them to understand when they can see the changes in outcome take place as we adjust variables. Lastly, the third meeting, which I usually call “Implementation,” is much more focused because at the end of the second meeting we’ve already agreed on the scenario we want to run with – I’m not usually surprising the client by telling them, “hey, you should consider a Roth conversion,” or “maybe that whole life policy isn’t doing you a lot of good.” Instead, we’ve covered that together in discussions at meeting 2, and meeting three is putting it into action.

David,

Yeah, to me one of the big virtues of this approach is that many of the ‘tactics’ get explored and modeled (prospectively) in the midst of meeting 2, and affirmed then as to whether or not they make sense. So by the time meeting #3 rolls around, the implementation phase is far more focused and expedited, because it’s not reviewing “new” recommendations but simply prioritizing the execution of the ones already discussed (at least usually).

– Michael

Agree on the most of the process and love that you reminded people that looking at processes from the client’s perspective is the right way to go.

So often people take processes too far and while they might be efficient they are not effective or client-service oriented.

I also think it important that after every meeting with a client an advisor asks the same questions most coaches ask. We learned that these questions up the value rate. 🙂

Something like “what’s one thing you’re taking away from our meeting that you’ve found to be of value. (Listen, write it down, don’t comment on it other than to say “thank you”.)

What’s something you’re going to do in the next week regarding your goals.

It’s good learning for the advisor (to see what each client appreciates) PLUS good to keep track of it for the client (to show them growth in the future).

Naming each part of a process (actually any process) into 1-3 memorable words is a great way to go with processes. It’s more understandable when staff knows that the next step is “send Welcome Kit”. And if the advisor and staff use those same words with clients, chances are that the clients will use similar words when someone asks them “so what did they do”.

So it might be:

Client Onboarding

(process that takes place once they agree to be a client)

1) Thank you letter – Short, sweet, and handwritten, to a new clients signed by all staff.

2) Welcome Kit Binder – include articles of interest with sections for their financial materials, and only 1 checklist of “Important Financial Materials” =the ones you may want them to find. The binder should not include forms to complete, which should be mailed/emailed/gathered online. This is more like an organizing gift.

3) Welcome Kit Call — Your assistant calls them to let them know that you’ve sent them a Welcome Kit in the mail. They should get it in “x” days or call the office.

4) Discovery Meeting (get to know clients better. Where are they now, what’s each of their short and long term visions, some organizing)

etc. etc.

Michael, great to see you Thursday and hope you made it home safely before the storm!

Totally concur with your post. Two years ago we went to a very process driven onboarding system consisting of 3 meetings. I wouldn’t change it for anything. Meeting #1 Preview Meeting… the 45-60 min where we show the prospect our mind mapping. If they engage us it’ll be a for a flat fee for the “Insight Assessment”, this consists of two meetings. The fee for the assessment will be between $3K to $7.5. Then Meeting #2 is “Discovery” (or explore possibilities), we do an internal peer analysis which leads to Meeting #3 which is “Presentation” (which is a combo of your #3 & #4). At this point the Assessment is completed and we move into a retainer/AUM combo.

As you know Gary and I very biased on this but we strongly feel mind maps are essential for the client experience.

Keep up the great work and hope to see you soon again. Rob

Michael, as a Financial Planner, I have been using some wonderful software from Torrid Technologies called RetirementView, which helps greatly with a more “client centric” approach to planning and meeting with clients. I absolutely love it and rely heavily on it. Check it out!

David Braun

I’m a fee-only financial planner and try my best to make the actual planning work I do as interactive as possible. I use MGPro and leverage the client portal heavily. During my in-person meetings with clients I often have one screen with the portal and one with “my” information. I sometimes let the client drive on their side as we go through everything, and then I can update on my side and refresh the portal in real time. We’re talking about their plan the whole time and reviewing/evaluating variables as we go. In my experience this engages clients in the process and makes those in-person meetings the primary “deliverable” versus the fake leather binder full of stuff most people simple do not read. I couch planning to clients as an ongoing, changing process that I want to open up to them as much as possible.

That’s awesome Tahoediver! Glad to hear you’re finding this approach really does help to more fully engage your clients in the process! 🙂

– Michael

Hi Michael, long time reader, first time commenter…I always look forward to, and enjoy, reading your blog posts.

I have been in financial services for the better part of 40 years. Over my career I have held many positions. Although I may have started out selling a product for a commission, I have always put the needs of the client first. A cliché, I know, but true.

For the past 20 years my focus has been on comprehensive financial planning as both a financial advisor and a software designer/developer. Ten years ago I realized that the “generally accepted process” for delivering a financial plan was not practical. Clients were not properly engaged and I was not adequately compensated for my time. After much soul-searching I realized the problem was not me or the client, it was the software.

So, here is my financial planning software manifesto:

1. Financial planning software is NOT a financial plan: To use a Harley-Davidson motor cycle analogy, “It’s not the destination that matters, it’s the journey.” The plan should address the needs of the client and support implementation of the recommendations made.

2. It must be client facing: I do not have the time to do anything more than once, so the client needs to be present when preparing the analysis.

3. Real-time data entry taking no more than 15 minutes: To do this the amount of information gathered in the first meeting would need to be minimized. The 80/20 principal states that 80% of our productivity comes from 20% of our efforts. This is also true for financial planning in that 80% of a financial plan comes from 20% of the client’s information.

4. No “what-if” scenarios: To eliminate the need for what-if scenarios, the system has to automate all routine elements of the financial analysis. Implementing strategies to minimize tax and maximize returns would be done with intelligent algorithms instead of manual data changes. In simple terms, the system would need to automate the calculations that any competent advisor would perform, but without requiring input from the advisor.

5. It should provide simple answers to common questions: “How much can I spend?” “When can I retire?” “How much do I need to save?” and, “What rate of return do I need?” In any situation, no matter what the outcome of the analysis, an intelligent algorithm should automatically provide the above answers.

6. No shortcuts in business logic: The analysis must be robust and accurate, providing proper tax calculations and flexible assumptions that can be controlled by the advisor.

In 2010 I felt so strongly that advisors needed to spend more time interacting with clients and less time on computers crunching numbers that I decided to create the software that lived up to these principles. Creating my own vision of the software I needed was the “simplest solution” to my problem, so I decided to call it The Razor after Occam’s Razor.

Available to Canadians since 2012, and soon to be available in the US, The Razor embraces simplicity and automation, without sacrificing precision.

– Dave Faulkner

This manifesto has already been implemented since 1993… the one the original… RetirementView by Torrid Technologies. And yes I work there and work with advisors every day teaching them how to do robust accurate retirement planning “live” and “in living color”….

If a client isn’t willing to put in the time to gather information pertinent to the meeting than they aren’t engaged in the process and probably aren’t good clients in the first place. We want clients who are nice, value and act on our advice and are willing to pay for the advice. Not everyone meets this criteria. As long as the questionnaire is clear, concise and well organized it shouldn’t be a problem to complete. I also believe a client’s time is valuable. Having 3 meetings just doesn’t make sense for most busy and successful people. I believe meeting 2 and 3 can be combined. Hopefully, you’ve discussed many of the client’s financial planning objectives in the “get to know you” first meeting. Once you receive the questionnaire, any specific questions for more information can be answered via a telephone call. Most good planners can begin to form recommendations from the data and have worked through many what if retirement scenarios before the second meeting. I agree with you on making the second meeting interactive. Working through the plan on the computer with the client showing what changes to saving rates, inflation, rates of return, gifting, etc. do to the plan. In addition, educating the client is key. A discussion of estate planning 101 is a big area where this can be done. Most clients have no idea about what their estate plan looks like. They get a huge binder of stuff and put it away in their safe deposit box. Having a discussion about the coordination of wills, trusts, asset titling, beneficiary designations goes a huge way to showing your expertise. It also almost always leads to referrals to CPAs or Attorneys in your network to help build your relationship with these important professionals. Specific recommendations on things like life insurance, disability insurance, LTC, etc. should be dealt with in a separate meeting after you have commitment from the client to move forward.

Hello Michael, Great thoughts for re-engineering the financial planning process. I’m wondering if some “behavioral finance” can be thrown in the mix. I, too, find the data gathering to be tedious for a client and for myself, mostly with following up in order to get information in a timely manner. Getting part of the upfront fee for the engagement helps. I’m wondering though if an additional economic incentive might help. For example, taking $75 or so off the last payment installment if all the initial information gathering stage is complete say by 20 days. Saves clients some money and saves me some time from having to chase things down.

About to launch my own sure-to-be-mostly-virtual RIA, I am ruminating on the How of implementing the Getting Organized meeting with a client. I like the idea. But all the discussion around software tools (from what I can see in the older article linked to in this blog post, and from this blog post itself) seems to end in “Nothing good enough exists yet.” So, how do I help my (future) remote clients to get organized? What is the virtual equivalent of the file box? It seems like it’d be so much more viscerally gratifying to organize physical papers, but then again, if I’m targeting women in the high tech industry, I highly doubt much of their life revolves around physical papers. Thanks for the continued thoughtfulness.

I have been searching & trying to find the right tools to help my clients in the Getting Organized session. I need a software where I can input my clients income and all their bills, debt, and everything they are using their money on a data report to show my clients where their money is going so we can eliminate unnecessary things and allocate that money toward building them a investment portfolio to begin accumulating them wealth to secure them assets to be able to plan for their retirement. With your experience and knowledge, can you recommend some software platforms & tools that can help me at this stage as help build a portfolio tailored to their risk & investment strategy?

Melissa,

There are a few tools in the advisor space to at least help do this.

The first is eMoney Advisor, which through their eMx platform can do account aggregation to bring in client spending and cash flow details. Others in this space include FinanceLogix (though I’m not sure how much detail they give on cash flow vs just assets/investment accounts), WealthAccess, and a coming new product called Narrator Clients from Advicent.

You might also check out some standalone budgeting tools like YNAB.

I hope that helps a little?

– Michael

Michael, thank you for your insight, not only on this topic, but on everything else you cover as well! I think this approach makes so much sense, especially with the instant gratification required by so many people in today’s world. We’d like to think most people make their finances a priority and are willing to do the work to get a quality financial plan, but too often that’s not the case. Anyways, my question for you is, how do you envision broaching the topic of planning for a fee, and do you believe the “Get Organized” meeting is part of that fee, or simply a way of building rapport and creating value early on? I’m sure it could go a number of different ways, but am curious to get your thoughts on how you see that part of the process going. Thanks in advance for your time!