Executive Summary

In recent years, a growing number of retirement “bucket” strategies have been developed to tie specific portfolio allocations to specific expenditures – most commonly by tying “essential” expenses that a retiree cannot outlive to guaranteed income streams (or at least highly conservative portfolios with low withdrawal rates), while “discretionary” expenses are supported with more volatile portfolios in recognition of the fact that if the portfolio performs poorly the expenses can be cut (since they are “discretionary”).

The caveat, however, is that it’s not always easy to determine what constitutes an “essential” vs. “discretionary” expense in the first place. The classic approach is to tag the food, clothing, and shelter kinds of categories as “essential” (along with perhaps healthcare in the modern era), while travel and entertainment expenses are discretionary.

Except in practice, if a retiree lost out on such “discretionary” expenses, it would likely not only be a traumatic impact to their real-world lifestyle, but such discretionary expenses often support genuinely psychological needs (e.g., funding activities that empower social well-being). And at the same time, many classically “essential” expenses in the areas of food, clothing, and shelter, really aren’t essential at all. From the house that’s bigger than what a retiree couple truly needs to survive, to eating out at expensive restaurants instead of dining frugally at home, or buying “designer” clothes versus generic or lower-cost brands (or buying at a second-hand thrift store).

In essence, separating “essential” vs. “discretionary” expenses by looking at categories of spending doesn’t necessarily work. Instead, the better approach is perhaps to segment spending within each category into the “Core” expenses that form the nucleus of the household’s lifestyle, from the truly discretionary (and more easily adaptable) expenses within each category (from the upscale restaurants to the designer clothes). In other words, there’s a potential layer of Core vs. Adaptive expenses in every spending category.

And importantly, the distinction isn’t mere semantics. By attaching specific portfolio “buckets” to each of the Core vs. Adaptive spending types, it’s easier for retirees to actually see that their “Core” spending really is secure, while a more-volatile portfolio (with more downside risk but also more upside potential as well) is tied more directly to the expenses that are truly adaptable and flexible, while giving retirees a clear resource bucket to consume (and know when it’s exhausted). Which in turn opens up the door for retirees to decide how much they want tied to each of the associated retirement buckets.

The bottom line, though, is simply to recognize that what defines more flexible “discretionary” spending to fund wants (rather than needs) isn’t just a function of certain categories of expenses, or funding solely the expenses necessary to ensure base-level safety and survival needs. Instead, retirees can upgrade their lifestyle across any number of traditionally “essential” spending categories as well… as long as there’s a clear resource bucket to show how long that spending can be sustained, and when the retiree really may have to adapt!

(Michael’s Note: This article was inspired by a recent podcast with retirement researcher and financial planner, Jon Guyton, who discussed his version of the Core vs. Discretionary approach to segmenting retirement spending into buckets.)

Essential Vs. Discretionary And Needs Vs. Wants

A fundamental step to the process of budgeting and making responsible spending decisions is to separate “needs” from “wants.”

Needs are the “essential” kinds of expenses (the food, clothing, and shelter costs that are essential for survival, perhaps including basic transportation and healthcare in the modern era), while “wants” are viewed as more discretionary and flexible (expenditures like travel and entertainment that are certainly nice to have, but aren’t… well, essential).

From the budgeting perspective, separating needs from wants are crucial, in order to recognize that we must maintain enough cash flow to cover the essential expenses (first), and to the extent we have some extra (but still limited) resources we only then begin to allocate them to the more “optional” discretionary expenditures we want.

And from the retirement planning perspective, separating essential from discretionary expenses is similarly crucial, because it’s common to tie guaranteed (or at least ultra-conservative) assets to ensure that those essential expenses will be funded for life. While the more flexible discretionary expenses can be funded from less guaranteed and more volatile investments and asset classes (that have more upside potential to create even more discretionary spending… knowing that if it doesn’t work out, the essentials are still covered).

Yet the fundamental challenge of this approach is that, while expenses like travel and entertainment may be “discretionary” – inasmuch as they are not essential survival-level expenses – they do form the core of a household’s “lifestyle” to which they are accustomed. Which means losing out on the ability to cover those discretionary expenses in the future could still be quite traumatic to the household. Especially since those are activities that are often done socially… which means discretionary expenses often relate directly to our social commitments and support the social aspects of our overall well-being.

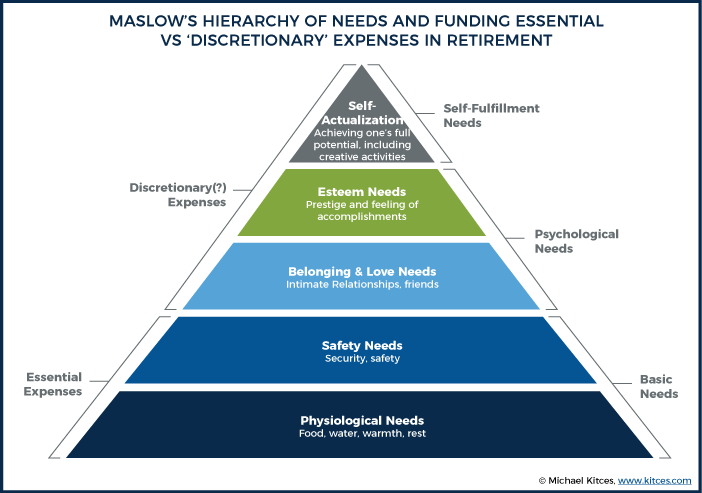

Or viewed another way, if we consider the classic Maslow hierarchy of needs, essential expenses may tie to the most “basic” needs that are essential for survival, but discretionary expenses aren’t merely optional… instead, those expenses typically just fund higher-level psychological needs instead! In other words, at least some “non-essential” discretionary spending may not support our physiological needs, but it may still be essential spending to support our psychological needs.

Furthermore, the reality is that not only are some “discretionary” expenses actually quite essential to meeting our fundamental needs for happiness and fulfillment, but not all “essential” expenses are actually essential to that endeavor, either.

For instance, while “shelter” is vital, living in a home of reasonable quality and safety doesn’t necessarily mean the current home is essential. As it may be a substantial upgrade above what is truly “necessary” for physiological safety and survival.

For those who can afford a more upscale home, of course, there’s nothing wrong with doing so. But it doesn’t necessarily mean a household’s entire expenditure in the “housing” category is really “essential” spending. For some, the “core” amount they would really need to maintain the essential housing component could be 10% less… or 25% less, or even 50% less in some cases.

Similarly, while having “food” is essential, “core” expenses may simply be buying basic groceries, while buying high-end organic groceries is really more of a discretionary expense. As is the decision to eat out frequently instead of “just” having friends over for a potluck dinner, choosing more expensive restaurants over more economical alternatives, and choosing the top-shelf alcohol and the nicer bottles of wine.

Clothing is another “essential expense” area where expenses are not always very essential. From the decision to keep buying fresh clothes when older ones were still fine, choosing to buy new clothes instead of second-hand, and the notorious cost gap between “designer” and brand name clothes versus more economical alternatives. Simply put, you may want blue jeans, but there’s a huge difference between spending $1,300 for a single pair from Gucci versus buying 3 pair for $130 at the Gap (or paying a fraction of the Gap price at a thrift store).

Simply put, at least some (though admittedly usually not all) “discretionary” spending on entertainment and travel may be essential for our personal fulfillment, while at the same time only some (and likely not all) “essential” spending is really essential in the first place.

What Is The Real Core Of “Essential” Spending?

Given that most essential expenses can include a (potentially substantial) layer of discretionary higher-cost choices on top, and that a number of traditionally-discretionary expenses are ultimately “essential” to an individual’s core lifestyle… arguably the real issue is not segmenting essential versus discretionary expenses, but instead defining a “Core” lifestyle cost, on top of which discretionary spending may be layered (in either food, clothing, or shelter areas, or in entertainment or travel or transportation).

In this context, “Core Spending” would constitute the “essentials” of the household’s entire lifestyle, recognizing that most people simply do not want to go backwards on their current lifestyle… but may still have a number of areas where they recognize they spend more than they truly need to because they can afford to do so.

Because spending more than the necessary Core is fine as long as one can afford to do so. But in the context of retirement planning, clarifying Core versus the Discretionary expenses that stack on top is crucial to understand how much the household really needs in order to fund their retirement expenses, and how much risk the household can and should take in a portfolio to satisfy those spending goals.

The key distinction, though, is that segmenting a household’s (retirement or other) budget into Core versus non-Core expenses means not splitting up household spending into essential versus discretionary spending categories, but separating out the Core expenses within each category instead.

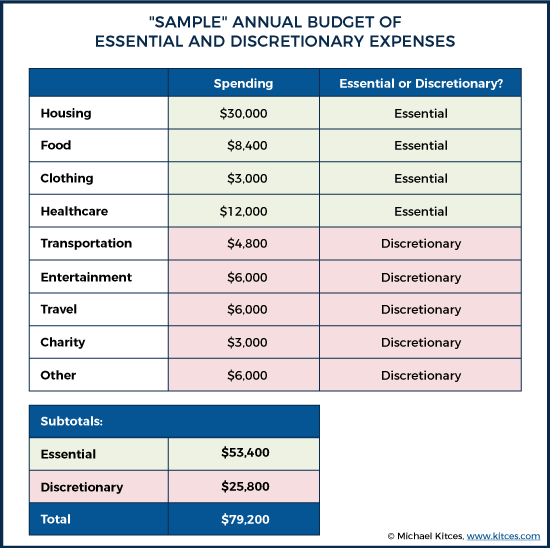

For instance, imagine a relatively affluent retired couple, that is living on almost $80,000/year of spending. Almost 40% of their budget ($2,500/month) covers the home they’ve lived in for the past 25 years (including the mortgage and property taxes, along with home furnishings), and they spend $1,000/month on healthcare (Medicare Part B and Part D, plus a Medigap supplemental policy for each of them), about $700/month on food, and $3,000/year on clothing, all of which forms a core of about $53,000/year in “essential” expenses. On top of this, they spend roughly $500/month on entertainment, another $400/month on their car payments, $6,000/year for vacation travel, donate $3,000/year to charities, and spend about $500/month of other miscellaneous expenses, bringing up their discretionary total to almost $26,000/year.

The challenge, though, as noted earlier, is that many of these “essential” expenses may not be totally essential – for instance, most retired couples ”can” survive on far less than $700/month for food – while other more discretionary expenses are still fairly essential (as some level of transportation is necessary, and eliminating the travel and entertainment budget to $0 could severely impair the couple’s social connections).

And from a more practical perspective, if the retiring couple’s advisor created a portfolio strategy that secured essential expenses but had a material risk of failing to sustain the couple’s discretionary expenses, this would likely not be deemed an “acceptable” retirement plan… because the couple literally can’t envision having those travel, entertainment, and other “discretionary” expenses really go all the way to zero.

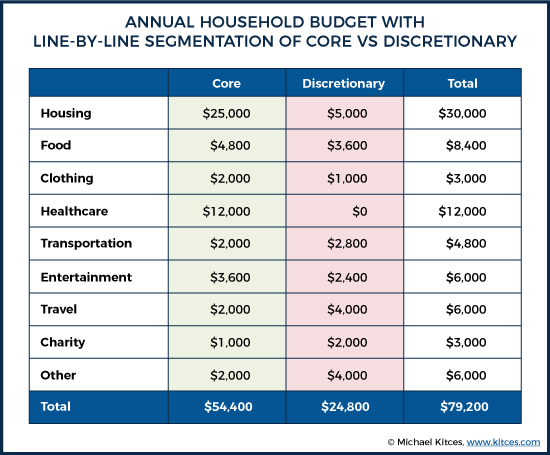

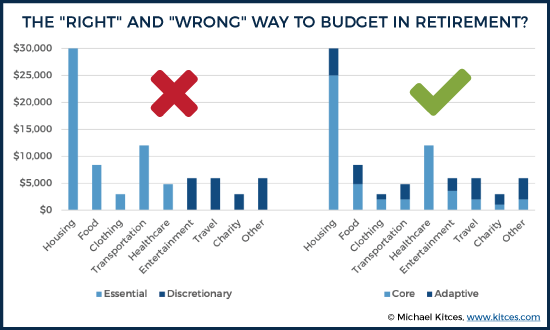

So what’s the alternative? Rather than segmenting each category of spending into essential versus discretionary tiers, segment the spending within each category into the “core” level of spending that would sustain the household, versus the discretionary spending they would like to do on top, but realistically could live without.

For instance, the couple might decide that they are unwilling to move out of their home, but they could scale back on the landscaping and home furnishings budget. And that they could trim their food and entertainment budgets by about 40% if they had to, trim back to 1 car (they hardly drive the second one anyway), dial down to just one vacation a year to see the grandchildren, and trim most other spending categories as well. (Except healthcare, as their Medicare Part B and Part D and Medigap supplemental policy premiums are entirely fixed, and they can’t control their out-of-pocket expenses any further if/when a health event does occur.)

Notably, in the end, the relative breakdown of how much constitutes “discretionary” spending is actually substantively similar, with about 2/3rds of the couple’s spending ($54,000/year) as “Core” and the other 1/3rd ($25,000/year) as “Discretionary.” But unlike the prior budget, this is one that, if necessary, the couple actually could adapt do. Because they wouldn’t be required to entirely eliminate categories of spending that can’t realistically be eliminated without drastically altering their lifestyle. Instead, their retirement plan simply reflects the ability (and an actual viable plan) to “scale back” if/as needed.

Fixed Versus Adaptive Expenses (Until Spending Declines With Age)

Once expenses are segmented into a “Core” that is relatively unchanging and a discretionary portion that is more flexible, another interesting phenomenon emerges… many of the expenses that retirees ultimately label as “discretionary” above the Core are expenses that tend to decrease with age anyway!

In fact, recent retirement research has increasingly documented that retiree spending tends to naturally decline – at least in real-dollar terms – throughout retirement, as even with a moderate rise in healthcare expenses in later years, “discretionary” spending tends to decline in a manner that more than offsets rising healthcare costs. And it’s not because retirees eliminate entire categories of “discretionary” expenses in retirement. Instead, it’s because their previously-scaled-up “discretionary” lifestyle dials back towards a lower-cost Core as age (and sometimes, health-related events) reduce the retiree’s activity levels.

Thus, just as is reflected in a typical allocation of spending between Core and Discretionary, retirees in their later years tend to reduce their transportation costs (consolidating from two cars down to one, and eventually often one to only ad-hoc or public transportation when driving is no longer safe), reduce their travel and dining out (as health limits mobility), and reduce their expenses on a wide range of other more-typically-discretionary expenses from clothing to entertainment.

Which means those non-Core “discretionary” expenses aren’t just discretionary; they’re also the more “Adaptive” expenses that tend to decline with age and natural lifestyle shifts as well.

In turn, this makes it feasible to once again develop retirement portfolios and pair retirement assets to the nature of the expense… not by tying one portfolio to essential-category expenses and another to the “discretionary”-category expenses (that would be traumatic to actually lose), but instead by tying one portfolio allocation to Core expenses and another to those that are naturally more “Adaptive”… and more likely to wind down on their own anyway.

Of course, for many retirees, a significant portion of retirement spending – and particularly Core expenses – may already be covered by Social Security. Which arguably is a plus, as it more directly ties the most “essential and Core” expenses to a stable and lifetime-guaranteed income stream, while the portfolio itself remains tied to the already-naturally-adaptive expenses left over.

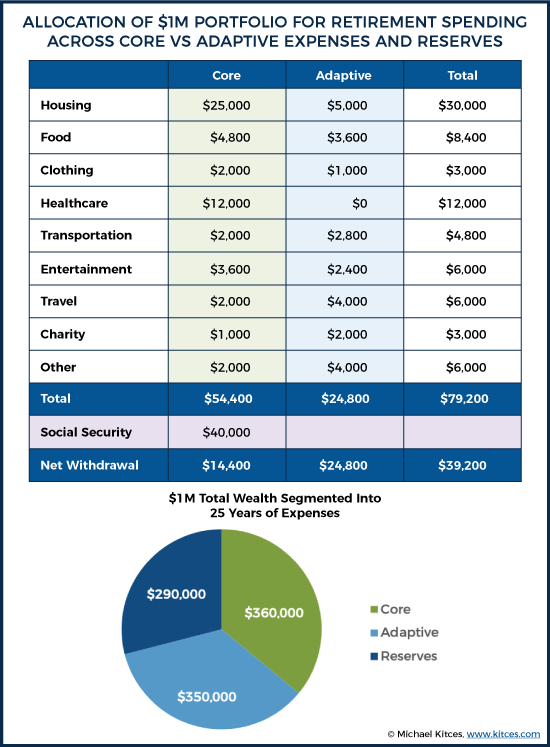

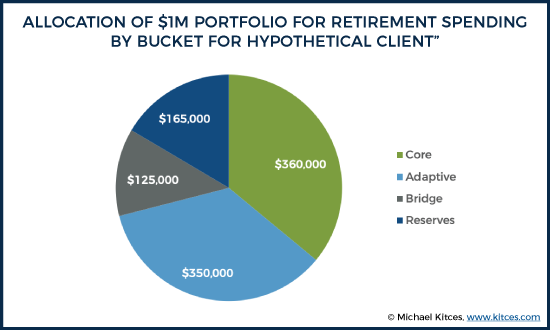

Thus, for instance, continuing the prior example, the retiring couple may already be anticipating $40,000/year of Social Security benefits, which means their portfolio “only” needs to sustain a net of about $15,000/year of Core expenses. At a 4% initial withdrawal rate (conservatively chosen given that they “must” continue for what could be a 30-year time horizon), which would necessitate a roughly-$360,000 allocation. In the meantime, the “adaptive” expenses that will naturally wind down over time only need to continue for the next 20 years, and are more flexible in the first place, which means the couple may accept a 7% initial withdrawal rate (since it’s OK and even anticipated that this portion of the portfolio will be spent down over time), receiving another $350,000 allocation.

Accordingly, if the retiree had a $1,000,000 portfolio, approximately $360,000 would end out in the “Core” portfolio, the next $350,000 would be allocated to the Adaptive portfolio, and the last $290,000 could simply be held as long-term “Reserves” for future use.

Of course, a key caveat of the preceding example is that, depending on exactly when the retiree couple actually retires, the Social Security benefits that cover the bulk of their Core expenses might not actually be available right away to cover those expenses.

For instance, if the couple was retiring at age 65 (as Medicare becomes available), but plans to only take the lower-income spouse’s $1,250/month benefit while delaying the other spouse’s benefit for 5 years until it rises to $2,100/month (with delayed retirement credits), then the couple needs another approximately-$125,000 (at a pace of $25,000/year for the next 5 years) to “bridge” spending needs until the rest of those Social Security payments begin.

As a result, the couple would allocate $125,000 of their “reserves” to a bridge portfolio (which must be allocated differently, and likely ultra-conservatively, given the very short time horizon), with the remainder then available to either continue holding as reserves

Allocating Retirement Portfolios Across Core, Adaptive, And Bridge Buckets

Ultimately, the reason it’s so important to “properly” categorize retirement expenses is to ensure that retirement assets are allocated properly to cover them, and that withdrawal rates from those assets are reasonable given both the time horizon involved and the relative flexibility or adaptive nature of the expenses (or not).

Thus, as noted earlier, “Core” expenses might be tied to guaranteed income streams (e.g., Social Security, a pension, or an inflation-adjusted immediate annuity), or at the most an appropriately conservative safe withdrawal rate from a long-term portfolio. While discretionary expenses might be tapped with a substantially higher withdrawal rate and a more growth-oriented portfolio, given that expenses can be reduced if necessary, may naturally reduce over time, but can also enjoy the upside potential of a favorable sequence of returns that would allow an even greater lifestyle instead. And bridge expenses, which will generally be the most short-term and fixed in nature, would be allocated to the most conservative (e.g., fixed-income) investments appropriate for the shorter-term time horizon.

Similarly, to the extent that not all the retirement portfolio is needed for those three buckets, available “Reserves” can simply be held in reserve or can be re-allocated to one of the other buckets to lift spending.

For instance, a retiree that finds themselves with a substantial excess “reserves” could also simply chose to allocate it to their Adaptive bucket, and actually spend it by increasing their more flexible lifestyle expenses since they can afford to do so (and have the health and energy to be able to enjoy it). Alternatively, the retiree could also allocate the reserves to their Core expenses, lifting up their Core lifestyle in the first place (e.g., buying a nicer retirement home for their new primary residence).

However, because the withdrawal rate will – by necessity – be lower with the Core bucket than the Adaptive, the same dollars allocated out of Reserves won’t have the same spending impact. Moving $100,000 of Reserves to the Core portfolio increases spending by just $4,000/year. Allocating it to the Adaptive bucket would lift it by $7,000/year (albeit for a shorter period of time).

The bottom line, though, is simply to recognize that carving up spending into classic “essential vs. discretionary” budgets fails to align to a retiree’s real-world lifestyle goals, where whole categories of “discretionary” expenses aren’t really discretionary. Or at least, while they may be from a pure subsistence/lifestyle perspective (the retiree will “live” without those expenses), losing all access to most discretionary spending categories entirely would be so traumatic to one’s lifestyle that no one would ever want to proactively plan for such an outcome in the first place (any more than they'd risk the rest of their essential expenses).

On the other hand, when carving up spending within each category into Core vs. Adaptive expenses, it becomes clearer where retirees really do have spending flexibility to cut back… either out of necessity if portfolio performance is poor, or simply naturally due to time and age and the natural slowing of retirement spending that tends to occur in the later years.

And in turn, clarifying the relative amount of Core vs. Adaptive spending also makes it easier to determine how much in retirement assets should be allocated to each bucket, how the buckets themselves should be invested, and whether the retiree actually has “more than enough” and could allocate some additional reserves to support even higher spending.

Arguably, though, as Guyton himself notes, perhaps the greatest benefit to a clear separation of Core vs. Adaptive expenses, and the creation of separate buckets to support each, is simply that it makes clear to retirees themselves exactly how much room they have left to spend, or not, and allows them to see more directly the impact that market volatility may have on their Adaptive spending (but not their Core)? In other words, labeling expenses as “Core” (across essential and discretionary) expenses and “Adaptive” on top isn’t just a matter of semantics; clear words and labels help retirees to stay on board with the plan, too.