Executive Summary

With Federal student loan debt in the United States currently exceeding $1.5 trillion, there is a huge market of borrowers who are in need of advice on managing their (potentially very sizable) debt… especially because often those with the largest student loan debts also have the highest post-graduate-school earnings (e.g., doctors, lawyers, etc.), which makes decisions about student loan repayment a very high-stakes proposition. And because of the complexity of student loans, many of these borrowers are looking for professionals with the right expertise to help them avoid heading down the wrong path. As while there are many moving parts inherent in the myriad of Federal student loan programs that impact borrowers, borrowers themselves are often unsure of how different life changes (e.g., marriage, a job change, or living in a different state) may further impact how their student loan plans will affect their financial future.

In this guest post, Ryan Frailich – Founder of Deliberate Finances in New Orleans, Louisiana – discusses how financial advisors can offer value to their clients who have significant student loan debt by acquiring the right expertise, designing a systematic student loan planning process, and developing a business model that incorporates student loan planning into their menu of services offered. After all, the reality is that a thorough student loan plan may potentially help a borrower save tens or even hundreds of thousands of dollars, leaving ample room for advisors to earn a substantive fee for the value they provide (which still amounts to a cost that is a tiny fraction of the potential debt savings). Not to mention the benefits of helping clients understand the different options available to them, how their choices may impact their student loan repayment plan, and how their career and life decisions can affect their overall student loan debt.

In order to offer their clients the most effective student loan advice, advisors need to acquire the appropriate depth of knowledge on the various student loan programs and their rules. While self-study is one option for financial advisors to obtain the subject matter expertise required to provide in-depth student loan planning services, others may wish to pursue the Certified Student Loan Professional (CSLP®) program. The CSLP is the first student loan planning designation designed to guide advisors through the process of helping clients navigate their student loans and addresses essential planning topics, including types of student loans, Public Service Loan Forgiveness, analysis of various student loan programs, and how student loan planning relates to broader financial planning topics. Once advisors acquire the requisite core knowledge, they can then work to design a repeatable process to screen and meet with clients, gather and analyze client data, and develop an in-depth student loan plan.

Depending on their firm's structure, advisors can choose to build student loan planning into their firm’s own service model, develop student loan planning as a component of ongoing comprehensive financial planning, or offer standalone student loan plans as short-term planning projects. This is often very appealing to high-income, high-debt young professionals, which can be of value for early-stage firms working to build a millennial client base.

A variety of fee models are available for advisors to consider as well, each with distinct benefits and drawbacks. Some commonly used fee models used by student loan planners include flat fees for one-time projects, fees based on the amount of student loan debt (a “debt under management” approach similar to the industry’s popular Assets Under Management approach for more affluent clientele), hourly fees, and fees as an additional expense included as part of a comprehensive financial plan. Accordingly, some advisory firms will build student loan planning to be a profitable service line unto itself, while others may focus on it as a way to profitably serve younger clients now while also planting seeds for later firm growth (as some clients who initially seek one-time project-based plans may come back as long-term comprehensive planning clients, and/or become AUM clients as their student loan debt is repaid and they become asset accumulators, especially in the case of high-debt high-income clients).

Ultimately, the key point is that student loan planning offers financial advisors a wide realm of business opportunities, either for shorter-term or longer-term engagements. For many firms, offering student loan advice can be an important differentiator to attract higher-income, upwardly mobile next-generation clients (i.e., those with high earnings but currently facing high debt burdens, where the impact of student loan advice is significant and so is the long-term client potential). Additionally, establishing expertise in the subject matter can yield client referrals (by becoming known in a niche of student loan planning), and opportunities to collaborate with other financial advisors who need student loan planning expertise – all of which can potentially turn into valuable, long-lasting relationships!

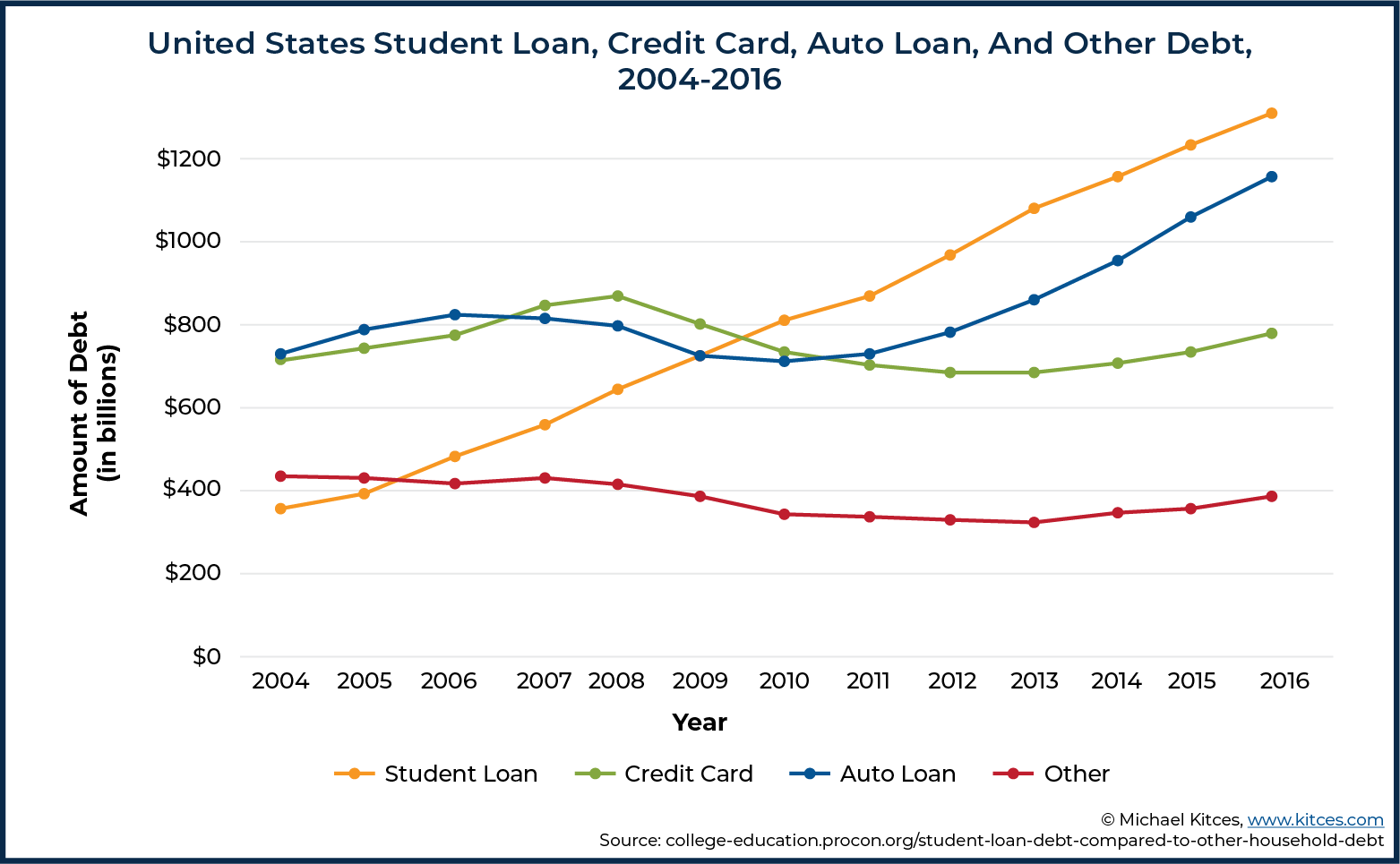

Federal student loan debt in the United States stands at over $1.5 trillion, with another $120 billion in student loans held by private lenders. There’s more student loan debt than any other form of debt, aside from mortgages, and the gap has been increasing over the past decade. With more than 40 million Americans who have student loan debt, there are many individuals in need of good advice to help them manage their debt.

For financial advisors, student loans are a topic that will continue to come up frequently for younger clients (who tend to be borrowers to get through college), which can create a profitable stream of advice fees for helping them manage that debt while planting the seeds for future firm growth. But to develop this expertise effectively, advisors must spend the time learning about student loans, building out their workflows and systems, and then scaling them up to continually make the process more efficient for a distinct kind of debt advice, unlike the traditional asset-based advice model.

For financial advisors, student loans are a topic that will continue to come up frequently for younger clients (who tend to be borrowers to get through college), which can create a profitable stream of advice fees for helping them manage that debt while planting the seeds for future firm growth. But to develop this expertise effectively, advisors must spend the time learning about student loans, building out their workflows and systems, and then scaling them up to continually make the process more efficient for a distinct kind of debt advice, unlike the traditional asset-based advice model.

Why (Paid) Student Loan Planning Is In High Demand

Given the size and scope of student loan debt, there are millions of people who are potential student loan planning clients for financial advisors. While not all borrowers have the capacity or desire to pay for student loan help, many borrowers with the highest student loan debts also have high incomes and significant wherewithal to pay for financial advice.

In fact, a study by the Urban Institute found that 34% of outstanding student loan debt is held by those in the highest income quartile. Additionally, 48% of loan debt is for graduate-level education, which is often tied to degrees (such as MDs, JDs, and MBAs) that are strongly correlated with high income levels. While the specifics of each individual’s financial situation vary, many of these borrowers are desperately looking for financial advice, not just on their student loans, but also on how their loans play a role in other aspects of their finances (e.g., being able to buy a house, get married, start a family, launch a business, and other financial planning issues).

For instance, after launching in October of 2016, Student Loan Planner has now delivered more than 4,400 student loan plans, advising on more than $1.1 billion of student loan debt. While their services focus exclusively on student loans and don’t include broader comprehensive financial planning, there is clearly a high demand for student loan advice when just one company has had that reach out to new clients in just the past four years!

In my firm, Deliberate Finances, I’ve advised on more than $5.4 million of student loan debt across 51 different households (some of which had two members who both had significant student loan debt). Almost all of these clients have come since I began focusing on this area in early 2018. As a solo advisor with no support staff, I am intentionally trying to build a small lifestyle practice and have successfully managed my client base by deepening my knowledge of student loans and creating a systematic student loan planning system. So simply put, whether you are a larger business with many staff members (as Student Loan Planner is) or a one-person shop, student loan advice can be a profitable business.

Borrowers with student loans are willing to pay for advice because student loan debt is altogether different from advising on other forms of debt. Given the complexity of Federal student loans and, in particular, the different rules on Income-Driven Repayment Plans, it’s almost never as simple as “cut spending and snowball your debt to $0.” In some cases, it may make sense to try to pay as little as possible in order to maximize student loan forgiveness, but that’s counterintuitive to borrowers (and to many planners as well!).

In an ideal world, student loan questions would all be answered for free by the loan servicers in charge of administering Federal student loans. In practice, loan servicers are notoriously difficult to work with. There have been a variety of lawsuits, both at the state and Federal level, accusing servicers of misapplying payments, pushing borrowers into costly repayment plans, or inadequately keeping records regarding payment history and forgiveness programs.

Heather Jarvis, a student loan advocate and co-founder of the CSLP® designation, summarized the problem as follows:

The interests of student loan servicing companies are not aligned with the interests of the borrowers who must rely upon them. Servicers are incentivized to process customer calls quickly and keep loans out of a delinquency status. Servicers are all too quick to suggest forbearances when Income-Driven Repayment is often better for borrowers. Also, servicers work off scripts designed to answer typical questions posed by an imaginary typical borrower. A ‘typical’ borrower may have a fairly low balance and entirely different circumstances than graduate and professional borrowers.

Acquiring Student Loan Expertise Through The Certified Student Loan Professional (CSLP) Designation

In order for financial advisors to build student loan planning into their businesses, someone at the firm needs to understand the student loan system inside and out. While this can be done via self-study and by reading the United States Education Department’s (USED) website, I strongly recommend advisors get holistic training in student loans. Because without a thorough knowledge of student loans, it’s possible to give advice that unwittingly can cost borrowers thousands compared to the other options potentially available to them.

The Certified Student Loan Professional (CSLP) designation is the first FINRA-recognized training program that specifically addresses student loan planning issues. It was founded by Heather Jarvis, mentioned above, and Jantz Hoffman, an advisor who has been advising borrowers on student loans for over a decade. The program is offered in partnership with Humboldt State University, part of the California State University system. The program is approved for CE credits for both CFPs and CPAs and, in fact, requires those who enroll in it to already have a designation such as the CFP, CPA, ChFC, CFA, or EA, and 2+ years of experience working with clients.

The CSLP program consists of a self-paced online study curriculum, with modules covering all aspects of student loan administration and repayment. Each module is focused on a specific student loan planning topic, such as “Student Loan Consolidations and Refinancing”, “Public Service Loan Forgiveness”, and “Student Loan Defaults”. Each of the modules ends with a short quiz on the topic.

After completing the study modules, advisors must then pass 6 case study modules that start with very basic cases that move into extremely complex cases with both members of a household owing hundreds of thousands in student loan debt. The case studies include calculating required repayment amounts, interest subsidies, and the impact of other financial decisions on the ultimate required student loan payment. After completing all of the modules and case studies, advisors must score 70% or higher on a test which must be completed in 2 hours or less. Advisors must also pass a short exam annually to maintain the designation. As of this writing, there are 103 people who have earned the designation and approximately 100 more who are currently in the process of doing so.

I view the CSLP designation as the most robust and efficient way to learn about student loans and to avoid potential student loan advice mistakes. By teaching an organized process that builds from the basics to the highly complex, the CSLP curriculum prepares advisors to provide accurate advice. While it’s possible to self-study in this area, I encourage anyone who wants to make student-loan planning a core part of their business to take the training. It intentionally highlights unique situations such as dual-debt households, which can be challenging to plan for.

I initially started my student loan training by taking an 8-hour in-person workshop with Heather Jarvis and Adam Minsky. While their workshop was a great beginning, I found that it was inadequate once I decided to make this a focus of my business. However, I found that the CSLP curriculum provided the foundation I needed to feel confident advising clients on their student loans.

Good Student Loan Advice Can Have A Huge Impact On A Client’s Financial Plan

Advisors who understand the different rules for student loans and how a borrower’s decisions interact with the tax, investment, and cash flow aspects of their lives are uniquely positioned to save borrowers many multiples more than the advisor may be charging in advice fees.

I have a client with a six-figure student loan debt and an income of around $60,000 – $70,000 annually. Based on her relatively low income compared to her debt balance, I projected that it would cost her less to stay on the Revised Pay as You Earn (REPAYE) plan than to pay her debt off completely. This plan limits her payment to 10% of her discretionary income each year and calls for any remaining balances to be forgiven after 25 years of payments. Even including the expected income tax due on the amount of debt forgiven (under current law), she’ll pay less in total than she would have on the Standard Payment Plan.

By following this plan, she went from paying around $750/month on student loans to $280/month and putting another $300 into an investment account to prepare for the potential tax due at forgiveness. So not only did we reduce her overall student debt burden, but we also had her saving some of her money in an investment account rather than using it all just to pay down her debt.

In this case, student loan planning was included as part of the client’s comprehensive planning services, and by restructuring these student loan payments, the client’s annual retainer fee was more than made up for!

And this client’s scenario isn’t unique. I regularly see borrowers whose total repayment obligations under different repayment options vary significantly, sometimes by hundreds of thousands of dollars. Which route a borrower takes has enormous financial implications.

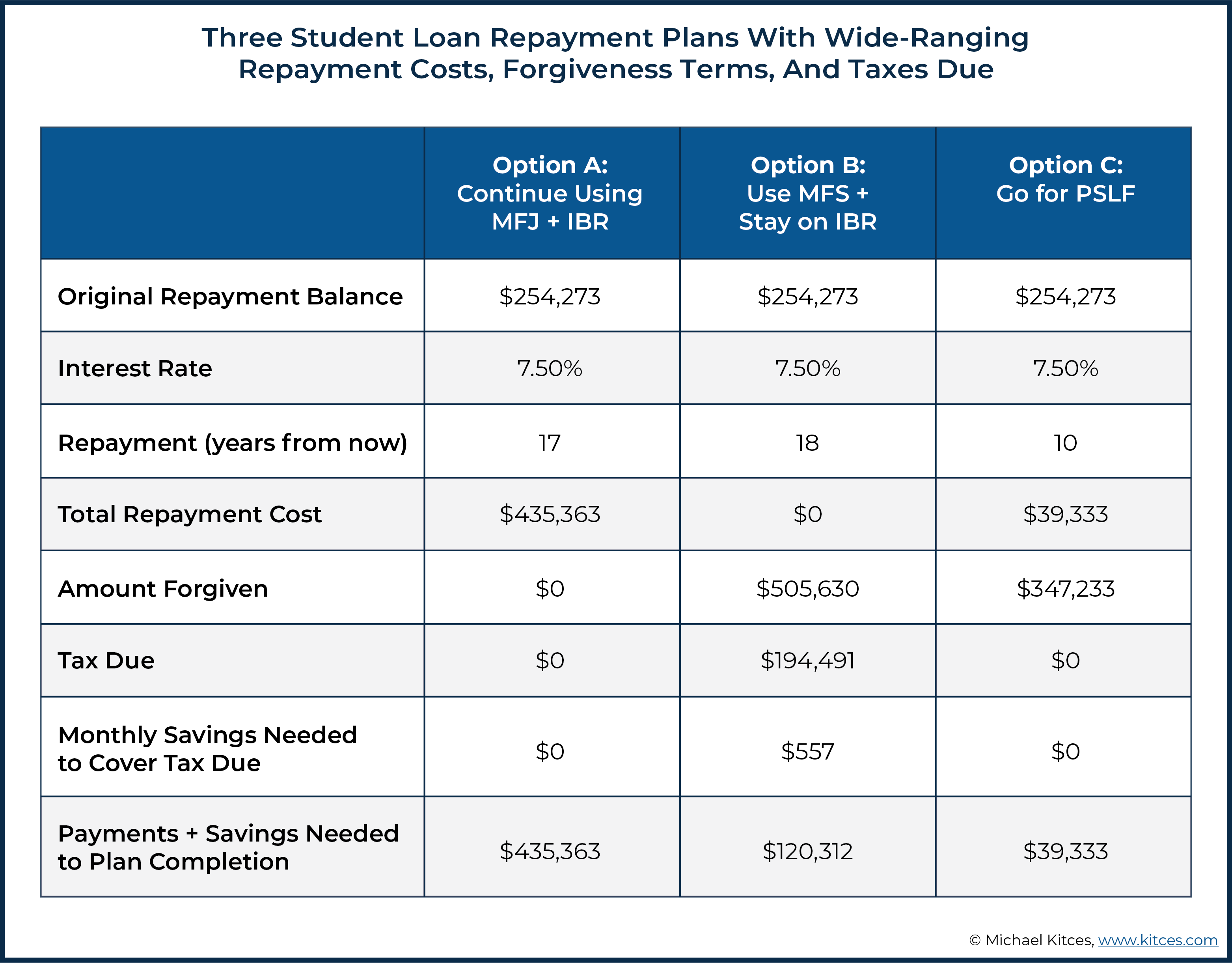

For example, in 2019, I worked on a student loan planning project for an attorney with more than $254,000 of student loan debt. She is married, but her income is so low that her required student loan payment based on her income alone would be $0 if she were to file her taxes as Married Filing Separately (MFS) and choose an Income-Based Repayment (IBR) plan. Since her income is a small fraction of her spouse’s income, using the MFS tax filing drastically lowered her Adjusted Gross Income (AGI), which in turn reduced her payment obligation to $0.

Her financial plan ultimately resulted in the three options shown below:

The ranges of outcomes with respect to repayment costs, potential forgiveness amounts, and taxes due are enormous, especially relative to the $750 fee I charged to help her formulate a plan!

Knowing about the seemingly small differences between different options, such as which repayment plans allow borrowers to use the MFS tax filing status and which do not, are things easily missed by borrowers, but that can have a huge overall impact on a client’s financial plan!

In addition to planning for the balance of the student loan debt itself, borrowers often need to make major life choices, such as whether or not to take a job or when to get married, keeping in mind how their student loans will impact their situation. Part of a good student loan plan takes borrowers through these ‘what-if’ questions so they can think through what they expect in the future and what impact their choices may have.

In the previous example, the borrower had never before considered a job in public service but began thinking about it after seeing the savings a Public Service Loan Forgiveness (PSLF) plan would provide, even relative to the IBR plan that wouldn’t require her to make any payment at all.

Building Student Loan Planning Advice Systems As A Financial Planner

Similar to any other specialized area of planning, advisors need to learn the subject material first, build a process for giving the advice, and then scale up their advice process to build their brand as an expert in the area.

My Student Loan Planning Workflow With Clients

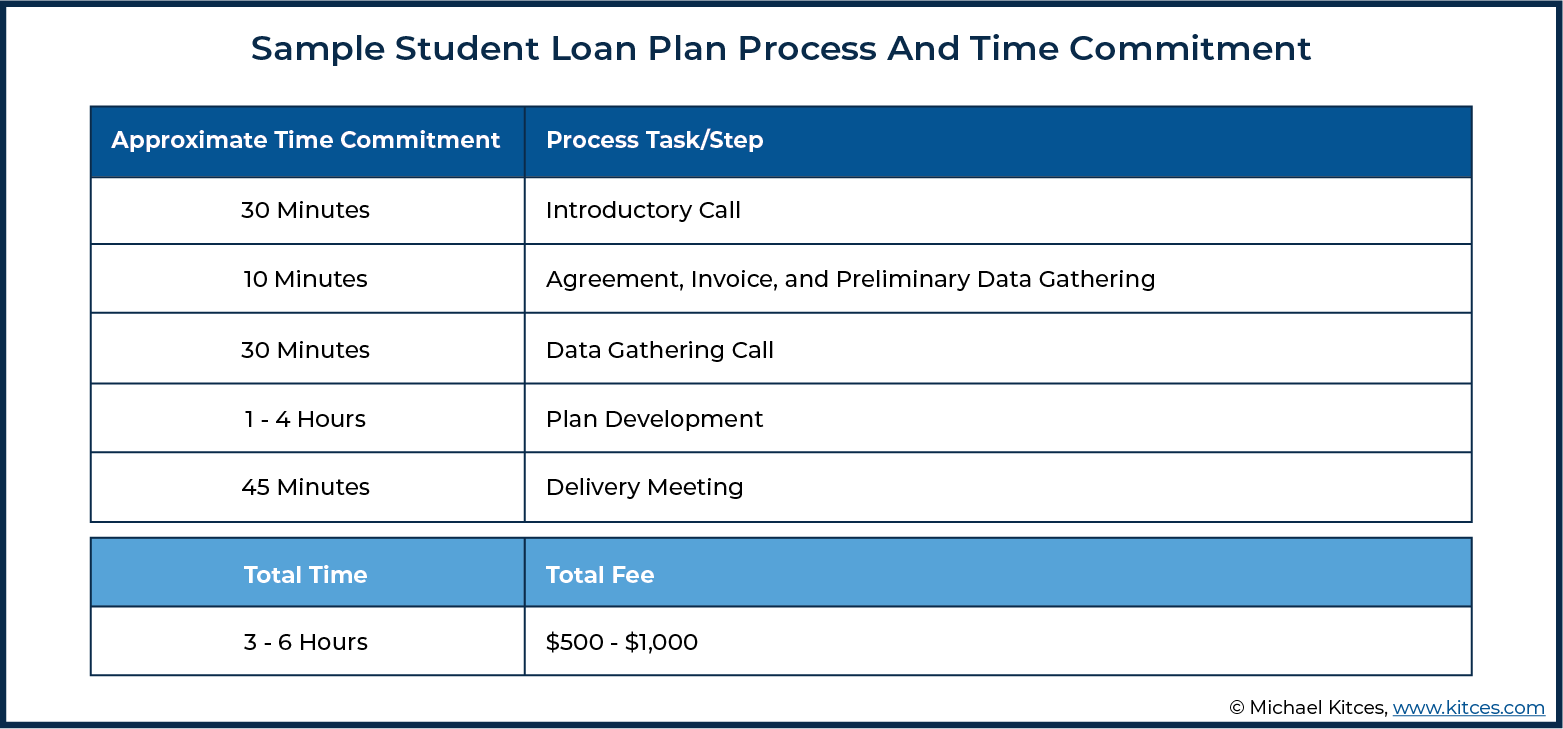

To demonstrate how a student loan project may flow, we’ll walk through my system for one-time plans focused on student loans. I follow a similar process for student loan planning within ongoing comprehensive planning, though it often happens in smaller pieces over several months as I take clients through the initial planning process, rather than as a focused, standalone module.

While I prefer to do student loan planning as part of a larger comprehensive plan, some clients aren’t ready for that financial commitment and only want advice on their loans. There are many planners who won’t do standalone student loan plans, but I’ve chosen to offer that as an option since it helps those who otherwise may be unable to afford financial advice to get help with what is often their most pressing financial issue.

Preliminary Meetings and Data Gathering

If a prospect reaches out to me, I ask them to book a free introductory call. My marketing is largely word of mouth, as I don’t have a huge web presence. Given the small nature of what I’m building, I rely on leads coming through current or former clients, other planners, XYPN, NAPFA, and CSLP Advisor search tools, and occasionally those who land on my website via an online search. After they schedule a call, I have an automated email that provides more information about my firm and sends a short survey. The introductory call helps me understand more about them and what is driving them to seek financial planning advice.

During the call, I typically allow clients to talk for the bulk of the time, as I ask just a few high-level questions. We determine if comprehensive planning is what the prospect is seeking, or if they only need help with their student loans (i.e., will this be a comprehensive planning engagement, or ‘just’ a student loan planning project).

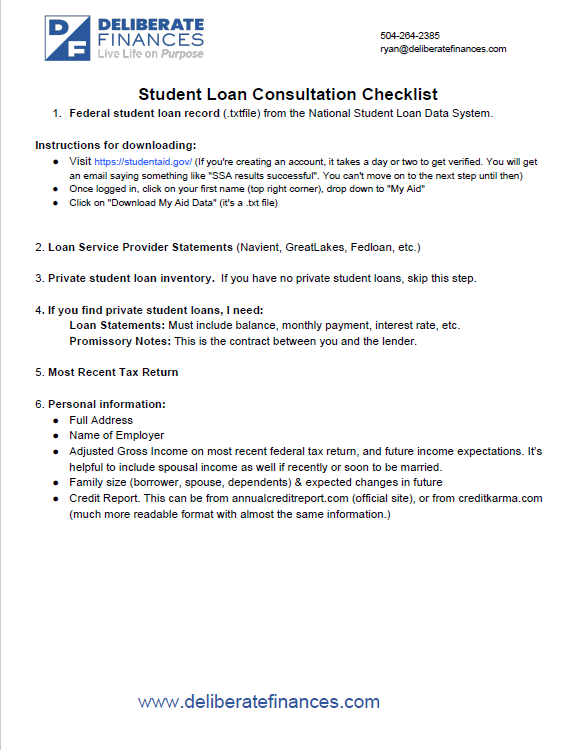

For those who decide to move forward on a student-loan-only plan, I charge 50% of the project fee upfront to ensure they’re fully committed to the project and ready to proceed. I’ve found some clients suffer from a lack of inertia in facing the reality of their student loan situation, so the 50% upfront fee acts as a commitment device to the planning process. I then have the client book a 30-minute project kickoff call. I ask them to send their basic information at least 3 days ahead of our call through this data gathering checklist:

Click to download a copy of the Student Loan Consultation Checklist

The first thing I require new clients to provide to me is a copy of their Federal student loan record, downloaded as a text file from the National Student Loan Data System, which borrowers can retrieve through the US Department of Education Federal Student Aid website. These are the instructions I give to my clients explaining how they can download their file:

-

- Visit https://studentaid.gov/ (If you’re creating an account, it takes a day or two to get verified. You will get an email saying something like “SSA results successful”. You can’t move on to the next step until then)

- Once logged in, click on your first name (top right corner), drop down to “My Aid”

- Click on “Download My Aid Data” (it’s a .txt file)

Once the client provides this text file, I upload it to LoanBuddy, which is a tool I use for some (though not all) aspects of student loan planning. There are a number of different tools available for student loan analyses; some advisors use the CSLA student loan software tool, the VIN Foundation Student Loan Repayment Simulator tool, or a macro in an Excel spreadsheet that organizes the .txt file into a readable format. Without one of these tools, this .txt file is essentially worthless, as the data is totally unorganized in the file itself. Yet, the file from the National Student Loan Data System contains far more information than a statement from loan servicers, and thus obtaining (and deciphering) it is essential to this process. Once the file is in LoanBuddy, I can see their loan balance, # of loans, the current required payment, what repayment plan they are on now, and their loan history. This helps me understand where they are starting, which helps me target my questions on the 30-minute kickoff call.

During the 30-minute project kickoff call, I try to clarify anything I have questions about after reviewing their loan information and initial data, including:

- What questions is the client trying to answer?

- Clarify any income questions, particularly about what they expect their income will be in the future.

- If they appear to be a Public Student Loan Forgiveness (PSLF) candidate, I ask for their employer benefits information, as well as how certain they are about their future career trajectory remaining in public service. Having information about their benefits is key because AGI is a critical component of student loan planning. Whether a client has a SIMPLE IRA, a 403(b) account, or a combination of a 403(b) and 457 account lets me know how much pre-tax saving could potentially be done, which in turn would lower AGI and lower the required student loan payment. Similarly, knowing about healthcare costs, availability of an HSA or FSA, etc., all drives towards the AGI calculation.

Developing The Student Loan Plan

Once I am crystal clear on what the new client is hoping to accomplish, I go to work on the plan. I use the LoanBuddy tool for some planning, though I sometimes do some of the work in Google Sheets. The tools I use will depend on the complexity of the client’s situation; if the client’s circumstances are not too complex, LoanBuddy alone can be sufficient to compare the different options available to the client.

For example, for a single client who just wants to know, “Should I stay on my current plan or privately refinance?” the analyses can all be done easily in LoanBuddy using the software’s projection tools. But for clients who want to compare several “What if I do X?” scenarios, such as switching careers, moving from private sector to public sector work (or vice versa), I find that using Google Sheets is more flexible and lets me do side-by-side comparisons more easily.

I also use Excel as a bit of a check on some of the calculations within LoanBuddy. While I think LoanBuddy is the best available tool on the market for student loans, I (and other advisors) have found some calculation errors over the years, so it’s helpful to double-check manually what the system is providing.

As I work, I gather any questions that arise and email them to the client. Once I get their answers, I complete the plan document, which is typically a 2-3 page summary of their options. I then send the client a copy of their plan via Google Docs 24-48 hours before the 45-minute plan delivery meeting and ask them to insert comments on anything they want to make sure we spend time clarifying during the meeting. Once we meet, we typically talk through the plan and any questions they may have. After the meeting, I invoice them for the second payment.

Technology Resources For Student Loan Planning

The technology resources available for student loan planning are also changing quickly, so tools and features may be available now that weren’t available just a short time before. For example, when I wrote this piece about student loan planning software solutions back in 2018, the VIN Foundation Student Debt Center required manual entry of loan data, but now you can directly upload the txt file that can be downloaded from the Federal Student Loan website.

I use RightCapital as my planning software; however, their student loan tool on its own is inadequate to give accurate student loan advice. Because it uses data feeds from loan servicers and not the NSLDS txt file, it often includes out-of-date or plainly incorrect data. This data is also incomplete. For example, it doesn’t in any way feed the number of months a borrower has already been on a given plan, so the system wouldn’t know how many credited months for PSLF a client may have and just assumes everyone starts from 0 months.

The same issues arise with those planning for longer-term forgiveness using one of the Income-Driven Repayment (IDR) plans. For instance, RightCapital has no way of knowing where along the repayment pathway someone is, so all calculations will be wrong for any borrower who isn’t just graduating from school. There’s also no record of payment history, so it’s hard to get a feel for what steps the borrower has already taken that got them to their present situation. If a borrower is just graduating and has no student loan history yet beyond having taken out the loans, the RightCapital system could work decently well. However, I’ve never had a client come to me in that situation.

I hope someday, in the future, I’ll be able to use student loan tools in an integrated manner for my clients who are comprehensive planning clients, where I already have much of their data (ages, family info, income projection, savings rates, etc.) in RightCapital. But as of this writing, none of the major financial planning software products have a thorough student loan module. I complete the student loan work outside of RightCapital using other tools such as LoanBuddy, which is able to show history from the NSLDS file and then adjust the RightCapital reports as needed once decisions are made about the strategy we are using for the student loans.

Time Management And The Importance Of Continually Improving Student Loan Planning Processes

It’s likely that the first few student loan plans you do will take many hours, but that’s an investment in learning how to do this work. Earlier in my career, when I was just beginning to tackle complicated student loan plans, the initial process would take me 4-8 hours of planning work. Now, though, most plans only take me 1-3 hours. As with most niches or specializations, once you’ve seen half a dozen examples of similar situations, finding answers to the initial “What are the options?” query becomes easy to spot.

You learn trends, such as knowing someone whose debt is greater than their annual income level is usually better off staying on an IDR plan than refinancing to a private lender. Or that if the lower-earning spouse has student loan debt, you’ll at least be considering filing taxes separately to drive down that Income-Based Repayment (IBR) or Pay As You Earn (PAYE) required monthly payment.

Click to download a copy of the Student Loan and PSLF Analysis

Once you identify the viable options available to the client, the next step is to run the calculations and place the information into a similar template to previous plans that you’ve developed, customizing for any unique pieces, and finalizing the plan. Here is an example of a student loan and repayment plan analysis I prepared. I typically deliver a 2-3 page summary of options with both the numbers and some narrative descriptions of other non-monetary factors to consider.

Once you have your process down, you can also develop a marketing strategy based on your specialized knowledge. Advisors can cite the total amount of debt they have advised on (“debt under management” instead of assets under management!?), the average debt per project, etc. For instance, Student Loan Planner highlights its client impact on their website this way:

Furthermore, your strategy can help borrowers trust that you’ll know how to analyze their unique situation. For me, when a prospect learns that I regularly speak to borrowers with six-figure debt, it often helps put them at ease.

More than once, I’ve had a prospect tell me they had been seeking out financial advisors only to be told by most that they need to “consider their wants vs. needs” and “prioritize the debt”, but those responses are woefully inadequate (and often inaccurate) to the ears of borrowers staring at a six-figure student loan balance. My personal highest balance for student loan debt was a couple with $457k in outstanding loans, though I know of planners who have seen student debt totals approaching $1,000,000!

Like all aspects of planning, my process got better over time as I adjusted my systems. While I now use templated emails to speed up each step, I still need to do a better job automating data collection. I still strive to continually adapt my process so that each project gets more efficient than the previous one.

How Financial Advisory Firms Can Build Student Loan Planning Into Their Business

There are huge benefits to advisors who specialize in student loan planning, and these benefits will only become more valuable as the cohort of borrowers with the most debt enter their prime earning years (which both lifts their earning power to pay for advice and begins their transition from debt-focused clients to potentially asset-based clients for the future).

If your firm wants to build a business serving the so-called HENRY’s (High Earners, Not Rich Yet), you’ll regularly talk to prospects who may be earning a $200,000 income but who may still be carrying a significant student loan balance. But rather than offering them a ‘slimmed down’ financial plan for their ‘simple’ situation at a reduced fee, the real opportunity is to charge advice fees for their real-world student loan complexity. The planning will just happen to center on their debt, not their investment assets.

Potential Revenue From Student Loan Planning May Start Small, But Can Establish Foundations For Valuable Relationships In The Future

For startup firms, the revenue from short-term student loan planning can be a great way to start building your practice. I started my firm in late 2016 with zero clients and zero revenue, so every dollar of revenue mattered. In 2017 and 2018, I made a total of $4,900 on 9 different student loan project plans and $1,500 from delivering workshops related to student loan planning.

While those are small numbers compared to many firm revenues, for a startup firm, it was key to staying open long enough to build up the ongoing financial planning clients that make up the bulk of my firm's revenue today. And though the $4,900 I made from project plans was from standalone student loan plans, many of my ongoing planning clients reached out to me initially because of their loan debt and ultimately selected me as their advisor, clearly because of my student loan knowledge.

I recently asked some of my clients, "What were you looking for when you were searching for a financial planner?" Below is the response from someone who had more than $110,000 of student loan debt when we began working together:

I initially decided to hire a financial planner after realizing that several years of making substantial student loan payments didn’t seem to be making a dent in my overall student loan debt. I found Ryan after having interviewed a couple of financial planners that didn’t seem well-versed in the landscape of student loan debt. When I interviewed Ryan, he seemed to understand not only my situation with student loan debt but my overall financial situation.

Of my current 44 ongoing financial planning relationships, 26 had student loan debt on the day they became clients.

I also asked Daniel Wrenne, CFP, who serves a niche of young physicians and dentists, how student loans played into building his firm. He responded with the following:

We serve young physicians, and student loans are a major financial issue for them. Naturally, it’s going to be something we focus on. For who we serve, I think it should be more of a baseline requirement than a differentiator. In other words, you shouldn’t be working with young physicians without understanding a good bit about student loans. It has helped us gain clients; people have said they chose us because "we could talk the student loan language".

How Student Loan Planning Advisors Typically Charge For Their Services

In a survey of CSLP’s, typical fees for a standalone student loan project are in the $400 – $800 range. Some will only do this work as part of comprehensive planning, but many will do a flat-fee or hourly project as well.

I typically charge $500 for an individual student loan plan and $750 for a couple, though I sometimes adjust this fee depending on any complexity revealed during the free introductory meeting. Based on a survey of other CSLP’s, my fees are in line with what many other CSLPs charge. Some may base the fee on total loan size or just have a flat fee regardless of loan size or single vs. couple, while others estimate the complexity and quote a fee based on that. Given the time involved – typically about 2.5 to 6 hours depending on the complexity of the client – this effectively amounts to a fee that averages about $100 to $200/hour for the advisor’s time and expertise. But with a great focus (and differentiated marketing advantage) than “just” offering standalone hourly advice.

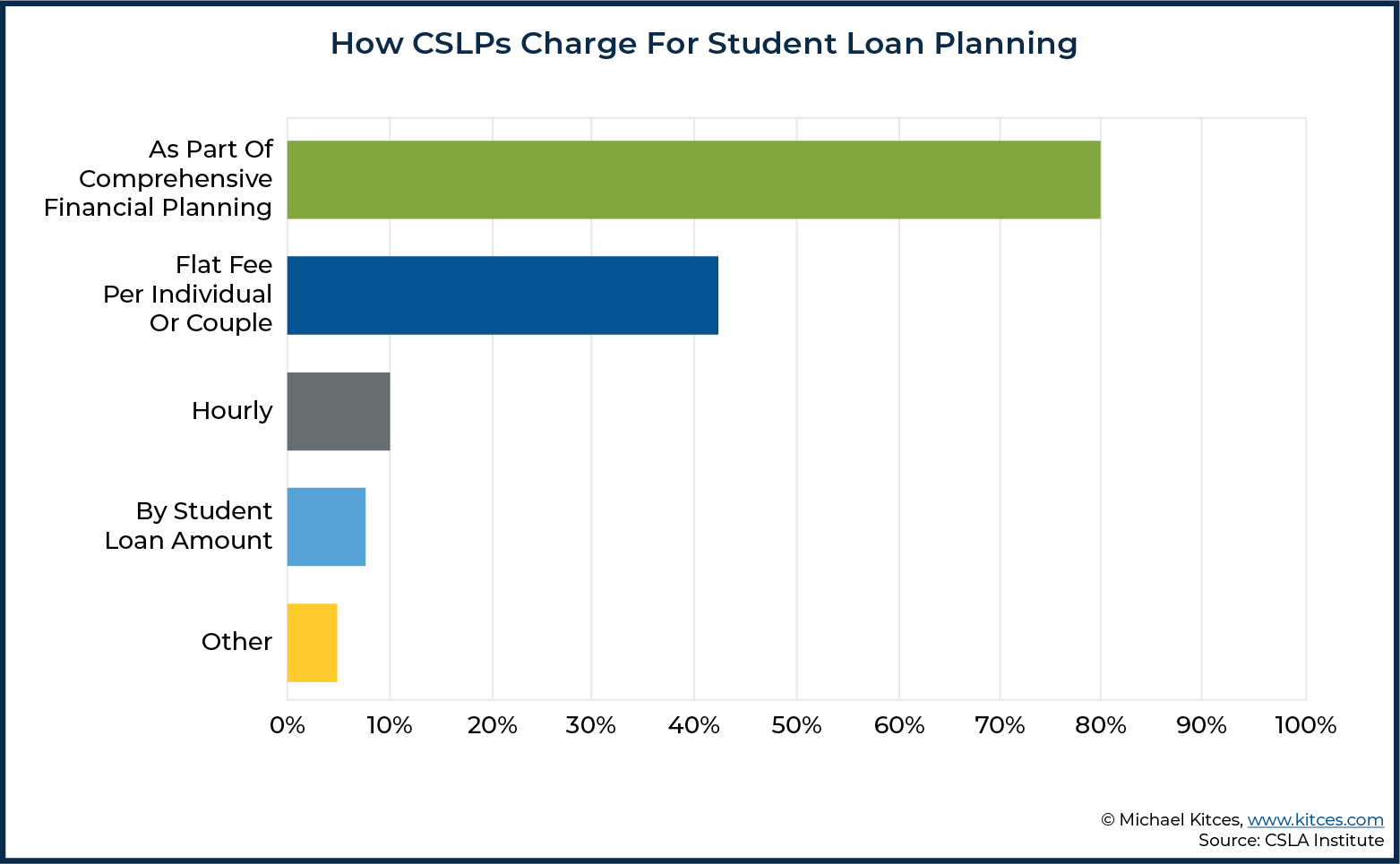

There are a variety of ways these planners have built student loan advice into their practice, as shown by the survey below, which was answered by 53 of the current 103 CSLPs.

Notably, while ongoing comprehensive planning is certainly the ideal way to work with clients given the complexity of loans (and the most appealing for advisors who try to work with clients in ongoing relationships), some clients may not be financially ready for that. On the other hand, a student loan planning engagement initially can still turn into subsequent (and more ongoing) client opportunities in the future as well.

For instance, in 2018, I completed a standalone project plan for a total fee of $600 for a client with over $250,000 of student loan debt and an annual income of under $80,000. She reached back out recently due to a sudden influx of income and has now become an ongoing financial planning client. Now I have a retainer client and recurring revenue, and it’s based on the relationship established by a standalone project plan more than 24 months ago. And the client came back because I was able to deliver meaningful value and expertise on her student loans from the very first engagement.

Establishing Expertise As A Student Loan Planner And Opportunities To Find Student Loan Planning Clients

Advisors who specialize in student loan planning can also become a trusted referral source for other professionals, including even fellow financial advisors. As while there are certainly some advisors with outstanding student loan knowledge and without the CSLP designation, the fact that only 103 professionals hold that designation is an indicator of how many advisors are not equipped to advise in this space.

In practice, I’ve gotten 9 student loan projects or ongoing financial planning clients who were referred to me by other financial planners (or, in one case, by a CPA). Several of them have remained ongoing clients of the other planner, and the client paid me directly to advise on just the student loan area of their plans. I’ve also consulted behind the scenes several times with other advisors, helping them through complex student loan cases with their clients and being paid directly for my specialized consultative role. Typically, I’ve just invoiced the advisor for an hour or two of time that we may have spent talking through their client scenario, and discussing the ramifications of different options they planned to show their client.

The key point is simply that if you have differentiated and specialized student loan expertise, tell advisors far and wide that you can help! Comment in online communities, such as the NAPFA forum or the internal XYPN community forums. When people see your explanations include terms they may only be loosely familiar with (PAYE versus REPAYE, Consolidation versus Refinancing, etc.), it can help them understand that they either need to refer their client to an expert or get some consulting help themselves.

Many planners who don’t specialize in this niche don’t want to invest the time into learning this area because the majority of their clients don’t face this problem (given the traditional advisor focus on pre-retirees and retirees who are long past the student loan phase of life). But they want to be able to help their clients (or in some cases, the children of their clients) solve these issues when they do come up, and by actively contributing to conversations in the financial planning community, you can build up a reputation as an expert to turn to.

Teaching student loan workshops is another way to establish credibility as an expert. I’ve done both advisor-facing and public-facing workshops on the topic, both of which eventually led to income based on referrals from a workshop attendee.

Another route to referrals is via your CPA connections. Because of the tax implications relating to some student loan planning, I’ve ended up getting in touch with multiple CPAs. Most of them know very little about student loans, and when I explain why filing separately may save more money in repayment than it costs in taxes, it’s eye-opening to them.

In addition, while I’ve not actually done this systematically yet, I believe there could be a lot of value in asking CPAs about who they do tax returns for that have student loans and emphasizing that I can be of help to them. As when it comes to younger clients, in particular, many have never talked about their finances with any professional other than their CPA, so having the CPA primed to give your name when the topic comes up is another potential source of referrals.

Student loan expertise is still rare enough that those who have it will be in high demand in the coming decade. Whether you are a startup firm looking to eke out revenue in the early years, or an established firm hoping to develop a new subset of clients, there are real opportunities to use student loan advice as the launching point for firm growth.