Executive Summary

Passed by Congress in December 2019, the “Setting Every Community Up For Retirement Enhancement (SECURE) Act” introduced substantial updates to long-standing retirement account rules. One of the most notable changes was the removal of the ‘stretch’ provision for certain non-spouse designated beneficiaries of inherited retirement accounts and the introduction of a “10-Year Rule” requiring those beneficiaries to deplete the entire balance of their inherited retirement account within ten years after the original owner’s death.

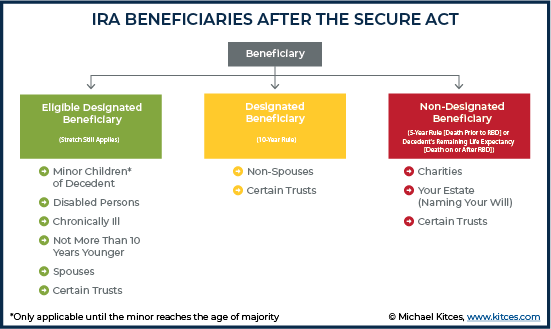

Notably, though, not all beneficiaries will be impacted by this new “10-Year Rule”. Instead, the SECURE Act identifies three distinct groups of beneficiaries: Non-Designated Beneficiaries (i.e., non-person entities such as trusts and charities), Eligible Designated Beneficiaries (i.e., individuals who are spouses of account holders, those who have a disability or chronic illness, those not more than 10 years younger than the decedent, and minor children of decedents or certain “See-Through” trusts benefiting such persons), and Non-Eligible Designated Beneficiaries (i.e., any individual or “See-Through” trust that qualifies as a Designated Beneficiary but is not an Eligible Designated Beneficiary). While Non-Designated Beneficiaries and Eligible Designated Beneficiaries are generally subject to the same rules that were in place prior to the SECURE Act (either the 5-year rule or stretching over life expectancy, respectively), Non-Eligible Designated Beneficiaries are now subject to the new 10-Year Rule, from trusts to adult children and more.

Given these substantial changes, there are many strategies that advisors can use to help their clients impacted by the new more-restrictive stretch rules, whether they be the (Non-Eligible) designated beneficiary of an inherited retirement account (trying to manage the compressed time window for distribution) or the original account owner themselves still planning for the future (to minimize the tax burden of account distributions in what is now a non-stretch world for many).

Some options available to Non-Eligible Designated Beneficiaries include spreading distributions out across a time frame for as long as possible to reduce annual income from the account, strategically timing withdrawals such that larger distributions are made in years with lower taxable income (e.g., after retirement), or simply leaving the account balance alone for as long as possible (and withdrawing everything at the end of the tenth year when required to do so).

Account owners themselves also have options to mitigate the tax impact for their heirs, including increasing the number of beneficiaries on their accounts to spread out and therefore decrease taxable income received by each beneficiary, and strategically allocating account shares based on beneficiaries’ anticipated income tax brackets to maximize the tax efficiency of those distributions. Alternatively, lifetime partial Roth conversions of tax-deferred retirement accounts can reduce (or eliminate altogether, if converting the full account) the tax burden on beneficiaries, though a careful analysis should accompany this strategy to determine how much of the original accounts should be converted to begin with (to avoid simply causing an even-higher tax burden today). Charitable Remainder Trusts can also be used to provide a potentially steady income stream for the beneficiaries (along with providing a gift to a qualified charity at the end of the trust’s term).

Ultimately, the key point is that, while Non-Eligible Designated Beneficiaries must now contend with the new SECURE Act 10-Year Rule for inherited retirement accounts, advisors can use several strategies to help clients minimize the tax impact of distributions from those accounts. Some can be implemented for the beneficiary after they inherit the account, while others can be used by the account owner themselves during their lifetime before the account transfers to the beneficiary. Although, in some cases, the best strategy may be simply to accept the 10-year rule as is, leave the account alone for as long as possible, and liquidate the inherited retirement account as required at the end of the 10-year window!

In December 2019, the passage of the Setting Every Community Up for Retirement Enhancement (SECURE) Act made several changes to the laws governing retirement accounts, but the most significant change for many financial advisors was its new rule eliminating the ‘stretch’ provision for most non-spouse designated beneficiaries.

The SECURE Act’s changes to the post-death rules for retirement account owners will impact many beneficiaries who will have to distribute funds from their inherited account(s) within 10 years after the year of the owner's death… much faster than what was previously allowed under the ‘stretch’ provision, which let beneficiaries spread distributions out based on their own lifetimes.

The SECURE Act expanded the original two basic groups of retirement account beneficiaries (Designated Beneficiaries and Non-Designated Beneficiaries) by splitting “Designated Beneficiaries” into “Eligible Designated Beneficiaries” and Designated Beneficiaries who were not Eligible Designated Beneficiaries (i.e., “Non-Eligible Designated Beneficiaries”).

While the old, pre-SECURE Act rules for Designated Beneficiaries still apply only to the newly created group of Eligible Designated Beneficiaries (i.e., they are still permitted to ‘stretch’), any Designated Beneficiary that is not an Eligible Designated Beneficiary (i.e., “Non-Eligible Designated Beneficiary”) is subject to the new 10-Year Rule. Additionally, there are no direct changes to the rules for Non-Designated Beneficiaries (i.e., they remain subject to the 5-Year Rule when death occurs prior to the decedent’s RBD, or to the decedent’s life-expectancy rule when death occurs on or after the RBD that already applied).

Understandably, the SECURE Act’s elimination of the stretch provision will also have great impact on retirement account owners. Fortunately, though, financial advisors have many strategies available to help their clients mitigate the tax impact for those affected by the new 10-Year Rule.

Strategies For Advisors to Help Non-Eligible Designated Beneficiaries Mitigate The Impact Of The New 10-Year Rule And The Death Of The Stretch

In light of the SECURE Act’s changes, one of the most common questions being asked by advisors, retirement account owners, beneficiaries, and potential future beneficiaries is “What do we do to minimize the bite of income taxes now that the stretch is gone?”

Some strategies that can help mitigate the ‘death’ of the stretch are best (or only able to be) implemented by owners of retirement accounts before they die. But regardless of the actions that an owner chooses to take (or not take during their lifetime), there are a variety of strategies that advisors can use to help their clients maximize the after-tax value of their inherited retirement accounts.

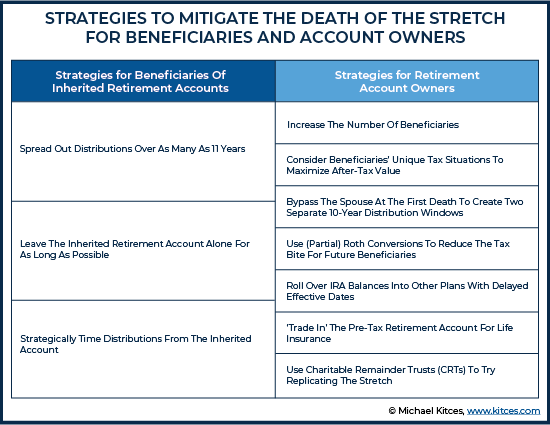

Leave The Inherited Retirement Account Alone For As Long As Possible

One tactic that an advisor can employ in light of the SECURE Act’s changes is to simply have the beneficiary leave the inherited funds alone for as long as possible.

While distributions before the tenth year after death may be taken by beneficiaries at any time, and in any amount they wish, such distributions are not required. Rather, the sole requirement is that whatever money is left in the inherited account in the 10th year after death be distributed by the end of that year.

Thus, a beneficiary could avoid taking any distributions through the first nine years after death, and only then, in the 10th and final year, distribute all the funds in the inherited account in one fell swoop. Doing so would allow a beneficiary to preserve the tax-deferred ‘wrapper’ of the inherited account for as long as possible.

Of course, such a strategy also has the potential to backfire. Big time.

If an inherited retirement account, plus any growth during the 10 years following death, is large enough to push the beneficiary into a (potentially much) higher tax bracket by having all of the income compressed into a single year (as opposed to spreading the income out over multiple years), employing a leave-it-alone-for-as-long-as-possible strategy probably doesn’t make much sense.

For example, suppose that a Non-Eligible Designated Beneficiary inherits a $250,000 IRA. If we imagine that the beneficiary is able to earn 7% per year, then using the “Rule of 72”, we can surmise that by the end of the tenth year after death, the account would be worth roughly $500,000. That $500,000 would all have to come out in the tenth year after death, creating a bump in income that would push most taxpayers into a much-higher-than-normal bracket. Simply put, that’s generally not going to be very efficient.

That’s especially true given that taking the funds out annually would have resulted in distributions of only about $35,000/year (to amortize the $250,000 plus 7% growth over the 10-year period). In other words, it’s far easier to manage (and remain in the same) tax bracket at $35,000 per year than it is with $500,000 in one year.

But while such a leave-it-alone-for-as-long-as-possible approach may not generally be the best path forward for Non-Eligible Designated Beneficiaries, there are several instances where such an approach should still be given very strong consideration.

Scenarios where delaying distributions from an inherited retirement account for as long as possible will often make sense for these beneficiaries:

- Non-Eligible Designated Beneficiaries of Roth accounts. The new 10-Year Rule for designated beneficiaries applies equally to both Roth accounts and pre-tax accounts (as while the tax treatment of the distributions may differ, the obligation to take distributions is the same).

Thus, while a Non-Eligible Designated Beneficiary of a Roth account may take distributions before the end of the tenth year after death, they don’t have to. And the longer the Roth beneficiary leaves the money in the inherited Roth account, the longer the funds in the account can continue to grow tax-free!

Accordingly, absent the need to take distributions to support living expenses before the end of the 10-year window after death, the standard operating procedure for a Roth beneficiary should be to avoid any distributions until the tenth year after death.

- Non-Eligible Designated Beneficiaries who are already in the highest income tax bracket. If a Non-Eligible Designated Beneficiary is already in the highest income tax bracket of 37%, then it likely makes sense to delay distributions from their inherited retirement account. Because regardless of how much income ends up coming out of the inherited retirement account at the end of 10 years, it can’t push the beneficiary into a higher income tax bracket for someone who’s already in the highest bracket (though there could be other, less likely impacts, such as to Medicare IRMAA or the AMT). In addition, few taxpayers benefit more from the power of tax-deferred growth in the first place than those in the highest bracket (who face the highest tax drag on ongoing growth).

Of course, high-income Non-Eligible Designated Beneficiaries looking to utilize this approach should be sure to keep an eye on Washington. If, for instance, we approach the end of 2025 and it appears that the changes to the individual income tax rates made by the Tax Cuts and Jobs Act (TCJA) will expire (sending the top rate back to 39.6%), such individuals may wish to take a distribution from their account prior to the expiration of such changes (before the tax brackets revert higher). Similarly, if Congress were to enact new legislation increasing future tax rates, accelerating distributions before such an event may, once again, make sense.

- Non-Eligible Designated Beneficiaries of small pre-tax balances. A final group of beneficiaries who may wish to delay taking distributions from their inherited retirement account for as long as possible is one that inherits smaller balances that are not likely to push them into a higher tax bracket, even after 10 years of earning. For instance, if a Non-Eligible Designated Beneficiary inherits a $15,000 IRA account, even if the account doubles over the ensuing 10 years before a distribution occurs, the resulting $30,000 distribution in year 10 may not be large enough to push the beneficiary into a materially higher bracket (and/or phase out other tax benefits).

Spread Out Distributions Over As Many As 11 Years

While waiting until the end of the 10-year period following the year of death may be a valuable approach for some individuals, many Non-Eligible Designated Beneficiaries will benefit from an approach that allows them to spread the income from their inherited account over as many years as possible. To that end, while Non-Eligible Designated Beneficiaries inheriting after the SECURE Act’s effective date are subject to the 10-Year Rule, in most cases, if desired, they may also have the option to spread distributions from the inherited retirement accounts over as many as 11 tax years.

So how can those subject to the 10-Year Rule get an 11-year period to spread distributions? Recall that ‘Year 1’ of the 10-Year Rule begins in the calendar year following the year of the retirement account owner’s death. But what about the year of death? Let’s not forget about it from a tax-planning perspective!

Notably, if death occurs early enough in the calendar year, a beneficiary should have more than enough time to be able to establish an inherited IRA and take a distribution from that account prior to the end of the year. That would allow them to take a distribution in what is, essentially, “Year 0” of the 10-Year Rule. Additional distributions can then be made over the ensuing 10 years, allowing the beneficiary to spread the income from the inherited account over 11 tax years.

Of course, the later in the calendar year that a decedent dies, the more challenging it may be to pull off this strategy. For instance, in the extreme case of death on December 31st, there is no chance that a Non-Eligible Designated Beneficiary would be able to take a “Year-0” distribution. Nevertheless, for most deaths occurring prior to December, advisors can engage in tax planning for the beneficiary with ample time to establish an inherited retirement account for the beneficiary and to coordinate a distribution prior to the end of the year.

Thus, assuming decedents will die at a roughly even rate over the course of any given year, more than 90% of Non-Eligible Designated Beneficiaries each year can be expected to have the opportunity to spread income out over as many as 11 tax years.

And while 11 years certainly isn’t the multi-decade timeframe that many such beneficiaries would have enjoyed prior to the passage of the SECURE Act, for many beneficiaries, spreading out income over those (up-to-) 11 years will still be an effective way – sometimes a surprisingly effective way – to minimize the potential risks of bumping into a higher-than-normal income tax bracket as the retirement account must be liquidated.

Example 1: On February 2, 2020, an IRA owner died, leaving his $2.5 million IRA to his two children, Jack and Jill, in equal 50% shares. Jack is married, and together with his wife, has $100,000 of taxable income. Jill is also married, and together with her husband, has $175,000 of taxable income. Both Jack and Jill would like to minimize the impact of taxes on their respective inherited IRA accounts.

Assuming that Jack and Jill are able to earn a 7% annual return, spreading out the income from their inherited IRA accounts (amortizing it) over 11 taxable years would require them to take just over $150,000 from each of their inherited IRA accounts annually. Surely this would cause them to pay tax at a significantly higher-than-normal income tax rate, right?

Actually… not so much.

First, let’s look at Jack, whose $150,000 annual IRA distribution, on top of his existing $100,000 of taxable income, will put him at $250,000 of taxable income. A quick peek at the 2020 tax brackets will show that the 22% bracket runs from $80,250 to $171,050, at which point the 24% bracket kicks in. As such, only $71,050, or nearly half of Jack’s additional $150,000 of income from the inherited IRA, would be taxed at his current income tax rate of 22%. Meanwhile, only the remaining $78,950 would be taxed at 24%, a relatively small bump up from his usual 22% rate.

Jill, meanwhile, will have a total of $325,000 of taxable income after her $150,000 inherited IRA distribution is added to her $175,000 of existing taxable income. A second peek at the 2020 tax brackets will show that the 24% bracket begins at $171,050 and ends at $326,600. Thus, despite adding $150,000 to her ‘normal’ taxable income, Jill will not see her marginal income tax rate increase at all. The entire $150,000 will be taxed at her same existing 24% tax bracket rate!

Strategically Time Distributions From The Inherited Account

Spreading the income from an inherited retirement account evenly over a 10-year (or 11-year) period can be an effective strategy when a Non-Eligible Designated Beneficiary’s income and deductions are expected to be relatively stable over that time period. But in many instances, that is not likely to be the case.

In situations where a Non-Eligible Designated Beneficiary expects significant swings in income and/or deductions, distributions from the inherited retirement account should generally be structured to coincide with periods when other income will be lower and/or when deductions will be higher.

Example 2: Bruce is a 61-year-old Non-Eligible Designated Beneficiary who inherited a $500,000 IRA from his mother on January 18, 2020. Bruce is currently employed and earns roughly $150,000 per year, but plans to retire at the age of 65.

Given the above fact pattern, it would likely make sense for Bruce to avoid (or at least minimize) distributions from his inherited IRA until the year after he retires.

For instance, he may opt to take no distributions from his inherited IRA during the first four years after his mother’s death (2021 – 2024, during which he will turn 62 – 65) and to, instead, spread the income from the inherited IRA over the final 6 years of the 10-Year Rule.

Not surprisingly, there are many scenarios where lumping taxable distributions from inherited accounts over some number of or certain specific years (as opposed to spreading them out more evenly over the 10 or 11 possible tax years) will make sense. Possible instances include when the following events will take place within the period covered by the 10-Year Rule:

- The beneficiary (or the beneficiary’s spouse) will be retiring (or ‘cutting’ back at work such that employment income is expected to drop materially);

- The beneficiary (or the beneficiary’s spouse) will be going on Medicare (Part B and Part D IRMAAs generally look at income from 2 years prior);

- A child will be applying for student aid;

- The beneficiary plans to move to a materially higher- or lower-income-tax state;

- A large charitable gift is planned;

- The disposition of a passive investment with suspended losses is expected;

- The beneficiary intends to marry (someone with modest income such that they can benefit from the lower tax rate of their married-filing-jointly tax brackets);

- The beneficiary is married to someone who is expected to pass away within the 10-year period (or is, themselves, expected to pass away and leave their inherited retirement account to their spouse); or

- The beneficiary is a child who will age out of the Kiddie Tax and have a lower income tax rate than that of their parents after that transition.

Estate Planning Strategies For Advisors To Help Account Owners Mitigate The Impact Of The New 10-Year Rule For Future Non-Eligible Designated Beneficiaries

While advisors can implement planning strategies for Non-Eligible Designated Beneficiaries (such as those described above) to minimize the impact of taxes on an inherited account, they can also help retirement account owners themselves adjust estate plans during life to account for the SECURE Act’s changes to the post-death distributions.

Notably, and perhaps not surprisingly, retirement account owners have a wider variety of planning strategies available to them to mitigate the ‘death’ of the stretch when compared to Non-Eligible Designated Beneficiaries (whose array of strategies can be summed up as different flavors of timing strategies).

Increase The Number Of Beneficiaries To Spread Out Income Subject To The 10-Year Rule

One simple strategy for advisors to use with retirement account owners in light of the SECURE Act’s changes is to increase the number of beneficiaries named on the beneficiary form. You might think of this as an “If we can’t have more years to spread the income over, then let’s have more taxpayers to spread income over instead” strategy.

Example 3: Gordon is an 80-year-old IRA owner who is reviewing his beneficiary designations in light of the SECURE Act. Currently, Gordon’s two adult children are equal beneficiaries of his $2 million IRA.

Suppose that each of Gordon’s two adult children has three adult children of their own. Instead of leaving his $2 million IRA entirely to his two children (who, given Gordon’s age, are likely in their peak earning years), he might decide to leave 5% of his IRA to each of his 6 grandchildren and 35% to each of his children (reducing each adult child’s shares, and the amount they have to fit into their tax brackets each year, by 30%).

Of course, there was nothing preventing Gordon from doing this before the SECURE Act, and he may not want to leave any of his IRA to his grandchildren. Perhaps he feels, like many individuals, that he will provide for his children, and then he will let his children provide for their children.

On the other hand, given the SECURE Act’s changes, Gordon may now prefer to see some of his IRA dollars go to other beneficiaries in order to minimize the cumulative impact of taxes on his legacy. At the very least, it’s worth a discussion.

(Nerd Note: Taxpayers who think of leaving IRA or other pre-tax retirement funds directly to young beneficiaries should remember that taxable distributions from IRAs and other retirement accounts are counted as unearned income. Thus, they may become subject to the Kiddie Tax, which after the SECURE Act, once again, is taxable at a child’s parent’s marginal tax rate. In such Kiddie Tax situations, the benefits of adding a grandchild as an additional beneficiary to spread income over an additional return may be virtually eliminated, and the dollars end out being taxed at their parents’ tax rates anyway.)

Consider Giving More Weight To Beneficiaries’ Tax Situations (And Leaving Beneficiaries Unequal Assets)

Distributions from inherited Roth accounts will generally be tax-free to beneficiaries, regardless of their own unique tax situation. As a result, heirs who are designated as equal beneficiaries of a Roth account receive equivalent after-tax value from the account.

The same, however, is not true for pre-tax retirement accounts left to beneficiaries with substantially different income tax brackets. In such instances, the greater the income tax rate of a beneficiary relative to the other heirs, the lower the after-tax value they will receive from the account relative to those heirs.

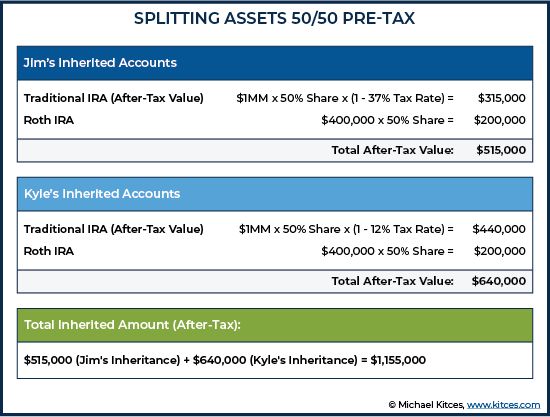

Example 4: Selina is 75 years old and is looking at revising her beneficiary designations in light of the SECURE Act’s changes. She has a $1 million Traditional IRA, and a $400,000 Roth IRA, both of which are currently left equally to her two children, Jim and Kyle.

Jim is a successful business owner and is consistently in the top 37% bracket. Kyle, on the other hand, earns a more modest living and is typically in the 12% bracket. If Selina were to die without changing her beneficiary forms, a (very) simplified analysis of the after-tax value her children would receive upon her passing might look something like this:

The total after-tax value of the inherited accounts combined is $515,000 (Jim’s accounts) + $640,000 (Kyle’s accounts) = $1,155,000.

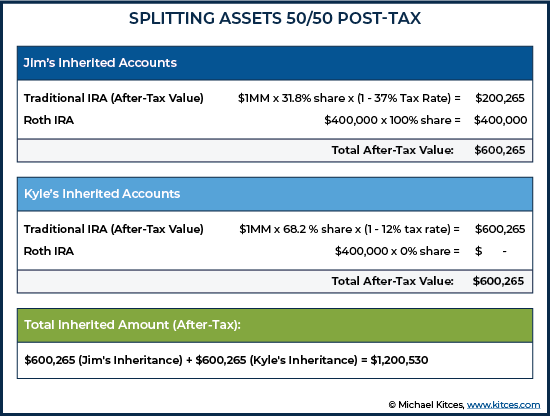

Suppose, however, that Selina decides to consider the difference in tax situations between her two children when designating her beneficiaries.

For instance, if Selina left 68.2% of her Traditional IRA to Kyle (and 31.8% to Jim), but all of her Roth IRA to Jim (with none of the Roth IRA going to Kyle), the cumulative after-tax value of Selina’s inherited accounts would be increased to $1.2MM, as follows:

Thus, the total after-tax value of the accounts here is $600,265 (Jim’s accounts) + $600,265 (Kyle’s account) = $1,200,530.

Accordingly, by altering her beneficiary designations as outlined above, Selina was able to increase the total after-tax value of her legacy!

Even though splitting assets equally among children may sound like the most equitable strategy, leaving heirs with very different nominal dollar amounts to equalize their after-tax values when there are different account types can actually increase the total wealth that they inherit.

Notably, in some situations, advisors may determine that trusts or other legal instruments are preferred to effect a similar – and perhaps even more after-tax-equal – distribution of assets upon the account owners’ passing.

For example, 100% of pre-tax retirement accounts can be left to beneficiaries in low tax brackets, 100% of Roth IRAs can be left to beneficiaries in high tax brackets, and taxable assets can be left to a trust that contains provisions requiring the trustee to use trust assets to equalize the after-tax inheritance of all beneficiaries.

On the other hand, while there is no question that a willingness to treat beneficiaries differently based on their own income tax situations can result in a greater cumulative transfer of after-tax wealth, there are downsides to this approach that must also be considered. One concern is the potential for beneficiaries to feel slighted or that they haven’t been left their fair share of (certain) assets. This can be the case even when the retirement owner’s decisions actually result in such beneficiaries benefiting on an after-tax basis since not all beneficiaries recognize how to adjust the relative value of their inheritance for the tax brackets of the other heirs.

To minimize this risk, advisors can encourage retirement account owners choosing to treat beneficiaries unequally (in order to maximize the after-tax value of their legacies) to discuss such plans with heirs during life, to avoid any hard feelings after death. Advisors can do this by helping to facilitate such meetings/discussions, which should emphasize that differences in inheritances are not indicative of different levels of love or affection and are simply being done for tax planning purposes.

Another downside to this approach is that it can add a significant amount of complexity to an estate plan. For instance, beneficiaries’ income tax situations may change, requiring beneficiary forms and/or other legal documents to be updated to maintain the after-tax parity of inheritances. Given concerns like these, many retirement account owners will avoid unequal inheritances, even when it may be financially advantageous.

Finally, it should be noted that the SECURE Act did not create the need/ability to treat beneficiaries in different income tax brackets differently in order to maximize the after-tax value of a legacy. It did, however, compress the time such beneficiaries have to distribute such assets, as well as increase the likelihood of large distributions during a beneficiary’s highest-earning years. Thus, the potential benefit that can be achieved by using such an approach has never been more valuable.

Bypass The Spouse At The First Death To Create Two Separate 10-Year Distribution Windows

Another strategy that advisors can use in order to mitigate the impact of the ‘death’ of the stretch on beneficiaries, specifically with married retirement account owners, is to leave some (or all) of the first-to-die spouse’s pre-tax retirement accounts directly to the couple’s ultimate beneficiaries, deliberately bypassing the surviving spouse.

Thus, when the first spouse dies, the portion of the account that skips the surviving spouse (who may very well have retirement assets of their own) will be inherited by the Non-Eligible Designated Beneficiary, at which point a 10-year clock to deplete the account begins. And when the second spouse dies, potentially years after the first spouse’s death, the surviving spouse’s own retirement assets (plus any portion of the first-to-die spouse’s account inherited by the surviving spouse) will subsequently be inherited by the Non-Eligible Designated Beneficiary, establishing a second 10-year clock to deplete the second account inherited from the surviving spouse.

By using this approach, the couple can give their beneficiaries as many as 20 years, provided by the 10 years following the death of each parent, over which to spread cumulative inherited retirement account distributions. This may be accomplished by either updating beneficiary designations to move up contingent beneficiaries as the primary beneficiary, or through the use of disclaimer planning.

Example 5: Oswald and Vicki are married retirement account owners who have built up a sizeable nest-egg. They currently have each other named as the primary beneficiary of their retirement accounts, and their two children as equal contingent beneficiaries. Between each spouse’s own retirement funds and the couple’s combined taxable assets, the surviving spouse (whoever it is) will have more than enough assets to support living expenses throughout the balance of their retirement years.

Given these facts, the couple may wish to revise their beneficiary designations and name their two children as each of their primary beneficiaries (or, alternatively, the survivor can just plan to execute a disclaimer upon the death of the first-to-die). By doing so, they will provide their children with two separate 10-year periods to distribute the couple’s combined retirement assets.

The ultimate benefit provided by such a strategy won’t be known right away, as it ultimately depends on how long the surviving spouse lives, after the death of the first spouse.

If, for instance, Oswald dies in 2020 and leaves his retirement account assets directly to his two children, but Vicki passes away the following year (in 2021), the change in beneficiary designations will have only ‘bought’ the couple’s children one additional year over which to distribute their cumulative inheritance (as going forward, the beneficiaries will still have to distribute most of both inheritances over the same overlapping time window).

By contrast, if Vicki survives Oswald by 10 or more calendar years, the move will have allowed the couple’s children to spread their cumulative inherited retirement assets over 20 years instead of ‘just’ 10!

When contemplating this approach, though, strong consideration should be given to both the retirement account owners’ tax rate and the beneficiaries’ tax rates. If, for example, the beneficiaries’ tax rates are higher than that of the retirement-account-owning couple, then to maximize the long-term after-tax value of the accounts, it will often make more sense for the couple to continue to leave their retirement accounts to each other at the first death. This strategy is most effective in situations where the size of the retirement accounts to bequeath is large, and the beneficiaries’ tax rates are low (and thus at risk to be driven up materially by a large retirement account inheritance).

Use (Partial) Roth Conversions To Reduce The Tax Bite For Future Beneficiaries

One straightforward way to remove the impact of higher taxes for beneficiaries as a result of the ‘death’ of the stretch is to simply eliminate the tax burden for them altogether via lifetime Roth conversions (either all at once, or more likely, systematically over time to spread out and ameliorate the tax bite).

Of course, this strategy will generally only make sense in situations where the tax rate paid on the converted amount will/would be less than the tax rate paid by the beneficiary on post-death distributions made under the 10-Year Rule. Otherwise, retirement account owners would be wise to continue to leave pre-tax retirement accounts to their beneficiaries (or at least, not to convert more for their beneficiaries’ sakes).

Having said that, when it comes to tax planning with retirement accounts, one key objective is to get distributions out of pre-tax accounts at the lowest possible rate. In the past, such distributions were able to be spread over the lifetime of the owner, as well as the life expectancy of their Non-Eligible Designated Beneficiary at the time of their death. Going forward, however, the same distributions must be distributed over only the owner’s (same) lifetime, plus ‘just’ 10 years.

Compressing the maximum potential distribution schedule, from the owner’s lifetime to just 10 years, has the potential to force dollars out of the beneficiary’s inherited retirement accounts at higher tax rates as compared to years prior to the SECURE Act’s effective date.

Logically then, this increases the chances that a beneficiary’s tax rate on distributions will be higher than that of the original retirement account owner, making Roth conversions during the lifetime of a retirement account owner more valuable to a beneficiary in a high-income tax bracket (or who is expected to be in a higher income tax bracket when accounting for distributions from their inherited account). Though, as noted earlier, in practice, it may take a very sizable retirement account (or a beneficiary with especially low tax rates prone to being increased) given the tax bracket smoothing that is possible simply by stretching out over the available 11 years.

In certain cases, beneficiaries (e.g., children) may even wish to gift non-qualified dollars upstream to retirement account owners (e.g., parents) to help pay for the tax liability on converted amounts that they expect to receive upon the retirement account owner’s death.

But just because the benefits are increased does not mean that retirement account owners should immediately and blindly turn to Roth conversions as a panacea for the ‘death’ of the stretch. In analyzing potential convert-for-beneficiaries scenarios, owners should first be sure to consider the impact of such conversions on their own chances for retirement success. If – and only if – such conversions do not have a materially negative impact on those chances, should conversions for beneficiaries generally be considered.

‘Trade In’ The Pre-Tax Retirement Account For Life Insurance

Roth conversions are one way to completely remove (at least for the Roth portion) the impact of taxes on inherited retirement account distributions. But another way to do so is to ‘trade in’ the retirement account for some other asset, like life insurance (by taking distributions from a pre-tax retirement account during the owner’s lifetime and using the after-tax amount to pay the premiums on a life insurance policy).

To that end, life insurance as a ‘solution’ to the SECURE Act ‘problem’ has been getting a lot of attention lately. For the many retirees who plan to use most of their retirement funds during their lifetime to meet living expenses, it generally is not a viable approach. But for those retirement account owners lucky enough to expect not to need some or all of the savings they’ve accumulated in retirement accounts during their lifetime, it deserves a look. In such situations, whether life insurance as a net-after-tax-wealth-transfer option makes sense (or not) depends on a variety of factors, including the retirement account owner’s age, health, the projected rate of return on such assets if they remain invested in a retirement account, and the aforementioned potential need to use the funds to meet living expenses.

Of course, the after-tax amount of any pre-tax distribution from a retirement account that is used to pay a life insurance premium could, instead, be used to pay the tax bill on a conversion of other monies in the pre-tax retirement account. Thus, any discussion or analysis of the potential benefits of ‘replacing’ a pre-tax retirement account with life insurance for heirs should also include a fair comparison with the potential benefits of a Roth conversion.

The primary advantage (some kinds of) life insurance offers over Roth conversions is that the life insurance can provide a guaranteed amount at death. Roth assets, on the other hand, offer a big edge to the beneficiary after they actually inherit, as they will have access to what could amount to several years of tax-free income. Notably, while the proceeds (death benefit) of a life insurance is income-tax-free to a beneficiary, interest, dividends, and capital gains begin to be taxable on such amounts beginning on “Day 1”. By contrast, not only is the value of a Roth account (generally) 100% tax- and penalty-free to a beneficiary at the time of inheritance, but the beneficiary will have at least an additional 10 years to allow such assets to continue compounding tax-free!

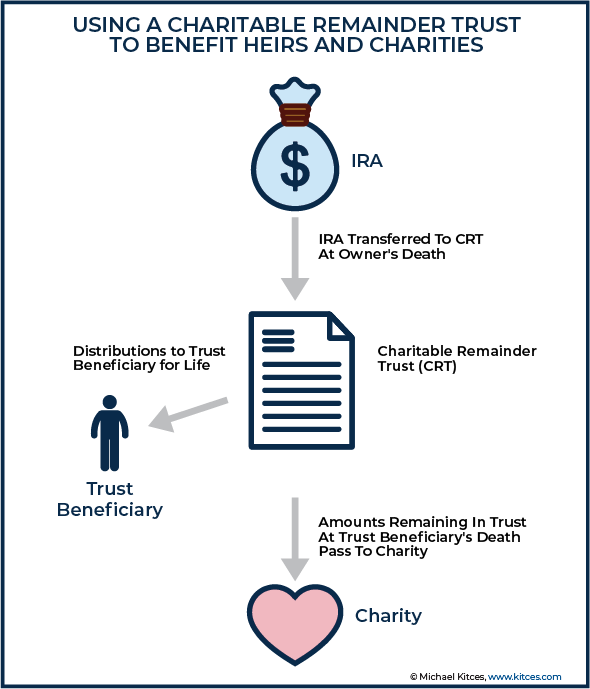

Use Charitable Remainder Trusts To Replicate Many Of The Benefits Of The ‘Stretch IRA’

For retirement account owners who still really want their beneficiaries to ‘stretch’ distributions, there may still be a way – sort of – using a Charitable Remainder Trust (CRT). As while such trusts don’t actually allow the stretch to be preserved, in many situations, they can be designed to replicate several of the biggest benefits of the stretch, including tax-deferral and a lifetime income stream.

A CRT is an irrevocable trust that is treated as a charitable entity. As such, when such a trust is named as the beneficiary of a retirement account, the entire inherited retirement account can be distributed to the trust without any tax liability at the time of distribution. Furthermore, once inside the trust, future income, interest, and capital gains earned on those dollars remain tax-deferred… at least until ultimately distributed to CRT beneficiaries. Though notably, as distributions do occur from the CRT to its lifetime beneficiaries, the income tax consequences pass along as well, with heirs being required to report all the CRT distributions that passed from the IRA into the CRT as ordinary income when ultimately received by the beneficiary out of the CRT.

In practice, once the inherited retirement funds are inside the CRT, they are distributed to the CRT beneficiaries in amounts and terms specified by the trust. Such distributions are limited per IRS rules, however, and must generally be between 5% and 50% of the trust’s assets (with the caveat that the net present value of the trust assets must equal at least 10% of the trust’s initial value upon the trust’s termination).

Furthermore, the trust can be drafted to allow distributions to continue for the life of the beneficiaries, for a term-certain period of no more than 20 years, or a combination thereof. At the end of the trust’s term (at either death of the final income beneficiary or at the end of the specified term, whichever is later), the remaining assets in the trust will pass to a qualified charity.

The sum result of these actions is a tax-deferred account that can create a lifetime stream of income to beneficiaries upon death of the retirement account owner. In other words, it’s pretty close to the stretch. But it’s not without its fair share of drawbacks.

Disregarding any costs or complexity that adding a CRT can create, the faux stretch created by CRTs also comes along with two other big drawbacks compared to the real stretch. First, CRTs remove optionality. Whereas the stretch allows a beneficiary to take distributions over their life expectancy but does not stop them from taking distributions sooner if desired/needed, the CRT essentially forces the income stream and removes access to the greater principal amount.

Additionally, whereas, upon death of the beneficiary of a retirement account, any remaining amounts will pass to the next-in-line beneficiary (the successor beneficiary who is chosen by the beneficiary) upon death of the income beneficiary of the CRT, the remaining trust assets pass to charity.

Thus, in the event a CRT beneficiary has an unexpectedly early demise, most or substantially all of the inherited retirement account may be ‘lost’ by the beneficiary’s family to charity. This risk is often mitigated with life insurance (albeit with its own cost to insure).

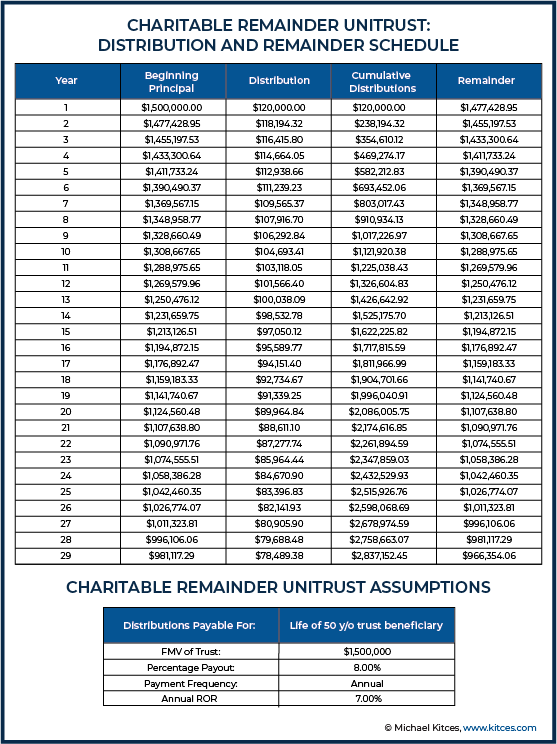

Example 6: Chris is the owner of an IRA. He has a daughter who is married and who currently has taxable income of $200,000. Chris is charitably inclined and would like to use some of his IRA money to support his favorite charity, but he would also like to see his IRA benefit his daughter while she is living. Given these goals, it may make sense for Chris to establish a Charitable Remainder Trust (CRT) to serve as the beneficiary of his IRA.

Suppose, for instance, that Chris names a Charitable Remainder Unitrust (CRUT) that will pay his daughter 8% of trust assets annually for her lifetime as the beneficiary of his IRA (as notably, the goal is still to distribute the bulk of the trust to the daughter, not necessarily to take a lower withdrawal rate that sustains the trust and shifts even more of the wealth to the charity’s remainder share). Further imagine that when Chris dies, the value of his IRA is $1.5 million and that after being transferred to the trust, the assets earn 7% annually.

Given these assumptions, Chris’ daughter would begin by receiving $1,500,000 x 8% = $120,000 in the first year, as shown in the chart below. If Chris’ daughter’s IRS-given life expectancy is age 79, she would receive a total of $2,837,152 of distributions from the CRUT during her lifetime. Furthermore, upon her death, Chris’ chosen charity (via the CRUT) would receive more than $966,000.

So how does this result compare to Chris simply leaving his IRA outright to his daughter? In this case, the CRT could actually be a reasonably compelling option.

Given the assumptions outlined above, if Chris’ daughter lived to age 79, she will have received a total of $2,837,152.45 from the CRT during her lifetime. Using a 7% discount rate, the Net Present Value (NPV) of those payments would be $1,283,208.77.

By contrast, if Chris’ daughter spread the proceeds of her $1.5 million inherited IRA evenly over the maximum 11 tax years, she would need to distribute $186,948.93 annually. The NPV of those distributions when Chris’ daughter is 79 would be $1,401,869.16.

While this amount is more than the NPV of the CRT distributions over the same time, it’s not the dramatically higher amount one might expect considering that the charity will end up with close to $1 million upon Chris’ daughter’s death. Plus, these NPVs are gross of taxes. Thus, after considering both the impact of taxes on the distributions received from the IRA and CRT at the time of distribution, and the resulting tax drag that would be created if the distributions were reinvested in a taxable account, the actual real after-tax value of the distributions to Chris’ daughter in both scenarios would be even closer.

Notably, the requirement of a CRT to designate at least an anticipated 10% of the value of the trust to a charity, and the potential for the charity to receive even more depending on the timing of death, can actually shift more value to the charity than the heirs would have lost by simply spreading over the available 11-year period and letting Uncle Sam take his slice.

Especially since the heirs still have to pay taxes on any/all IRA distributions when they do come out of the CRT to the beneficiary (as they would have by spreading out with the 10-Year Rule anyway, but now layering an additional portion that must go the charity at the end as well).

(Nerd Note: In certain situations, particularly where a smaller retirement account is involved, which does not justify the upfront (e.g., drafting) and ongoing (e.g., annual tax returns) costs of a CRT, retirement account owners may wish to explore Charitable Gift Annuities (CGAs) to see if they would serve as a more viable option. Such annuities are contracts in which, after receiving a sum of money, a charity will contractually agree to provide annuity payments back to the donor/annuitant (and potentially to a joint annuitant as well). The annuity payments can have a similar effect to CRTs by providing a lifetime income stream for beneficiaries. Notably, though, CGAs generally will not be issued by a charity, if they issue them at all, unless the annuitant is at least 60 years old (some charities impose an even later age). As such, CGAs are generally not viable strategies to provide for young heirs.)

Postpone The ‘Death’ Of The Stretch By Rolling Into Plans With Delayed Effective Dates

For a select group of retirement account owners, there may be an even easier way for advisors to help them preserve the stretch, at least for the next few years.

Because while the SECURE Act’s effective date (for purposes of the ‘death’ of the stretch) is not until January 1, 2022, for governmental plans and plans maintained pursuant to a collectively bargained agreement (i.e., union plans), owners of these retirement accounts who continue to participate in their plans can preserve the stretch for beneficiaries, through that time, by rolling outside retirement dollars into the plan. And while not all plans allow participants to roll in qualified funds from other accounts, it is not a particularly uncommon feature.

By moving all retirement funds into a governmental plan or a plan maintained pursuant to a collectively bargained agreement, retirement account owners can delay the onset of the SECURE Act’s 10-Year Rule for their Non-Eligible Designated Beneficiaries for an additional two years.

The good news… this is a super-simple way to save the stretch.

The bad news… for it to work, the owner has to die before the end of 2021!

Conversations To Review Retirement Account Beneficiaries Are A Must

The SECURE Act’s changes to the post-death distribution rules for Non-Eligible Designated Beneficiaries will have a dramatic impact on many families. Advisors, if they have not done so already, should immediately review all clients’ beneficiary designations to see which clients have named individuals or trusts that may be impacted by the SECURE Act’s changes.

Once those individuals have been identified, client contact to explain the changes is a must. Advisors should place emphasis on reaching out to those clients with shorter life expectancies, as well as those clients whose currently-named beneficiaries are most likely to experience dramatic impacts on the after-tax value of their inheritances thanks to the SECURE Act’s changes.

Such discussions with clients should focus not only on explaining the SECURE Act’s changes but also on the potential strategies that can be used to mitigate the impact of those changes. As can be plainly seen in the discussion above, there is no single one-size-fits-all strategy for clients.

Furthermore, while account owners do have a variety of potential strategies at their disposal that can help soften the blow of the ‘death’ of the stretch, each of those strategies comes with its own set of drawbacks. Thus, perhaps one of the most valuable things an advisor can do right now is to present the various SECURE-Act-mitigating options to clients and to see if there is a particular option – or set of options – that can best help the client accomplish their goals.

Alternatively, for some clients, the best decision may be to change nothing. As while the loss of the stretch and replacement with the 10-Year Rule is unfortunate, in many cases alternative strategies are even less effective than simply spreading the dollars out over the 11 years that will be available.

The most significant impact on retirement accounts by the SECURE Act is considered by many to be its replacement of the stretch provision with the 10-Year Rule for Non-Eligible Designated Beneficiaries of inherited retirement accounts. While the stretch IRA has long been an incredibly effective tool in the planner’s arsenal, it is no longer applicable for many non-spouse beneficiaries.

The good news for such Non-Eligible Designated Beneficiaries, at least, is that there are a significant number of strategies that can be used to minimize the SECURE Act’s impact. Designing distribution plans that capture income in the most tax-efficient years will be the best defense for those beneficiaries subject to the new 10-Year Rule.

But retirement account owners can also minimize the bite of the SECURE Act’s changes for beneficiaries by employing a variety of strategies, from simple solutions like increasing lifetime Roth conversions to more complex approaches involving the use of charitable trusts.

what can you do with a non-designated inherited Roth distribution by the end of 10 years? The operative word being ‘distribution.’ Is it possible to exchange the distribution of the inherited Roth with your own Roth IRA? If the distribution is only treated like cash, there’s seems to be no way around the earnings limitations associated with contributions and the loss of free compounding interest associated with a Roth.

Jeffrey,

Terrific review and examples of the many options to consider!

Jeff,

Another possibility that may make sense is to disclaim a portion of the IRA on the first to die spouse and then have multiple 10 year stretch outs. This could be beneficial for both estate/income tax purposes (depending on what the tax rate of the children is vs. single bracket of surviving spouse and when you believed the second spouse would pass away).

How was the Charitable Remainder Unitrust Distribution and Remainder Schedule computed? Can you supply the formula or the ability to download the example?

Another option, not to be overlooked, would be in the event that the beneficiaries were not maximizing their own 401(k) deferrals, using the 10/11 year distributions from the inherited IRA to effectively, if indirectly, fund maximizing their 401(k) deferrals (and possibly for their spouse as well) could be even more powerful than the old “Stretch IRA” – especially if it allowed for employer matches. Not for everyone, but it also should not be overlooked.

With very low effective federal tax rates as a Florida resident(18% on 300k), ROTH CONVERSIONS are a no brainer. Again the gov’t creates more legal and accounting work

Respectfully, I don’t believe that ROTH conversions are a “no brainer”. Many clients with high traditional IRA balances simply do NOT have the excess cash flow to pay the current taxes on the conversion. Think about someone with a $1 million traditional IRA or a couple with around $2 million. Many advisors correctly suggest ROTH conversions, but in MANY client circumstances, they just aren’t a practical solution (e.g., especially in relation to the RMD/Social Security tax trap).

Obviously, no state taxes is a huge benefit (particularly if you were in an income tax state when you got the deduction). However, the more pertinent way of looking at this is what did it cost you to do that last dollar of conversion. Therefore, your marginal tax rate of 24% (in the example you provided) is more pertinent to an effective conversion strategy.

or move to a redneck state and marry your daughter

There was a question on the bar exam: If a couple is married in Arkansas and divorced in Tennessee, are they still brother and sister?

lots of variables to consider but tax efficiency for the inherited IRA is the main issue

Leaving a ROTH IRA as a legacy is tremendous

And almost everyone feels tax rates will go up in 2026

Have you seen any good illustrations of income tax effect of larger IRA payable to trust using 5-year rule (e.g., non-see-through discretionary trust) or 10-year rule (e.g., see-through accumulation trust) (so as to inform decision regarding establishment of accumulation trust?

Ed Slott just put something out today:

“But in a shocker, IRS Publication 590-B says otherwise. Pages 11 and 12 provide an explanation and an example showing that beneficiaries would be subject to RMDs each year (as under the pre-SECURE Act rules) for years one through nine, and then the balance must be withdrawn in year 10. No one saw that coming! This doesn’t go along with the SECURE Act rules and committee reports, which seemed to indicate that the new 10-year rule would work like the old pre-SECURE Act five-year rule, with no annual distributions required.”

Potentially, this could cause some additional planning problems for big Inherited IRAs, and makes it more difficult to “time” the distributions for the heirs according to their particular tax situation each year.