Executive Summary

As the retirement research has evolved over the decades, so too have the “optimal” retirement strategies, and the entire approach to the retirement planning process itself.

In the early years, optimal retirement planning was all about determining which portfolio on the efficient frontier was best suited to achieve retirement goals. Then advisors shifted to a more goals-centric approach, where clients pursued a Maslow-style hierarchy of goals, from the “basic” essential goals of retirement (e.g., food, clothing, and shelter), to the more discretionary wants and wishes. And in recent years, retirement planning has increasingly shifted towards a more holistic “household balance sheet” approach that aims to capture all of the household’s present and future assets and liabilities, to determine if the household is fully funded (or if not, what its funded ratio is).

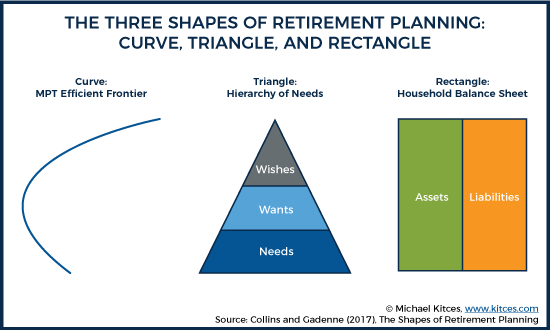

And in a recent paper, researchers Patrick Collins and Francois Gadenne note that each of these retirement modeling approaches has their own “shape” – from the curve of the efficient frontier, to the triangle of the Maslow-style hierarchy of retirement needs, to the rectangle of the household balance sheet with its assets and liabilities. And each shape leads to its own unique views on what is “best” for retirement planning, and what is considered “safe” – from cash under the curve approach (the most conservative portfolio on the efficient frontier), to the lifetime annuity under the triangle approach (guaranteeing that essential expenses are covered for life), to a laddered portfolio of TIPS bonds with the rectangle approach (aiming to perfectly match assets to liabilities and immunize the household against future changes in interest rates or inflation).

Yet ultimately, while each of the different shapes of retirement planning may prescribe different recommendations, it’s still not entirely clear which is “best”. After all, the rectangle approach may be effective to determine the household’s funded ratio and explore what’s possible, but is a poor framework for making trade-off decisions about which goals to prioritize. And while the triangle approach is better for prioritizing goals, it doesn’t necessarily produce a clear portfolio allocation the way the efficient frontier curve does.

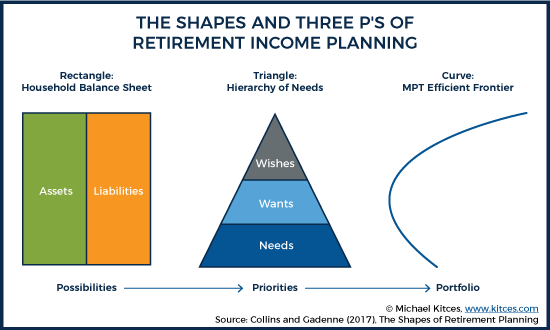

Which means in the end, the best approach for retirement planning may incorporate all three – the rectangle to explore the Possibilities, the triangle to Prioritize, and the curve to allocate the Portfolio itself!

The Evolution Of Models For Analyzing Retirement Portfolios

While his original paper was simply called “Portfolio Selection”, Harry Markowitz’s 1952 article in the Journal of Finance ultimately became the foundation of portfolio design, aptly dubbed “Modern Portfolio Theory” (MPT). Its key breakthrough (of the time) was that the investments of a portfolio shouldn’t be selected based solely on their individual return potential; instead, effective portfolio design should consider both the expected return and the risk (volatility) of the investment, and furthermore that a portfolio should be evaluated based on the overall risk of the entire portfolio (not just its component parts).

This Mean-Variance Optimization (MVO) approach to designing a portfolio was originally created to select investments on an annual basis (based on annual expected return and volatility metrics), but was ultimately adopted as an approach to fund longer-term goals like retirement as well. After all, if the MVO approach could effectively minimize risk for a given level of expected return, or maximize return for a given level of risk tolerance, then in theory buying and holding that portfolio for the long run should deliver the best path to achieving the retirement goal. The investor simply had to constrain the portfolio to a level of overall risk that was comfortable (i.e., to pick a portfolio on the efficient frontier that was consistent with risk tolerance).

However, while the MPT approach was relatively straightforward to apply to a single portfolio pursuing a single goal (ideally over a single time horizon), it was more problematic in the context of a broad range of financial planning goals, each of which might have not only different time horizons and different comfort levels with risk, but also outright different priorities. For instance, funding college for children in middle school might be a high-priority intermediate-term goal, while funding retirement is a high-priority but longer-term goal, and funding a vacation home is another longer-term goal, but one with a much lower priority. Yet Modern Portfolio Theory didn’t give an effective means to construct a portfolio that covered each of these separate goals, with their distinct time horizons and varying levels of prioritization.

Thus emerged the concept of “goals-based” financial planning, and the associated “goals-based portfolios”, where the portfolio in the aggregate may be comprised of “mini-portfolios” or “buckets”, each of which is tied to a particular goal, with an investment allocation that is appropriate for that particular goal, with that particular time horizon, and consistent with the tolerance of risk for that specific goal. Accordingly, “essential” expenses – the food, clothing, and shelter kind of needs – might be covered with a guaranteed income stream from an immediate annuity, while more flexible “discretionary” expenses might be invested via a growth portfolio, but short-to-intermediate-term needs might be invested with a series of laddered bonds that produce the requisite cash flows as needed.

Yet the problem with the goals-based planning approach is that it starts with the spending goal in mind, and then works backwards to the portfolio (or other alternative product solution), rather than looking objectively at the balance between available assets and spending goals (and other current and future liabilities) to decide whether the best path forward is to adjust the portfolio to fit the goal, or to adjust the goal to fit the portfolio. In other words, some (retirement or other) goals can’t be effectively funded, regardless of the portfolio, because the goal itself just isn’t economically feasible given the available assets. And for others, available assets may so “overfund” the goal that in reality, the investor could afford to pick new (i.e., higher) goals. None of which is necessarily captured in an approach that simply focuses on allocating investment assets to “match” goals.

Instead, the necessary retirement model is to create a “household balance sheet” that fully captures all current (and future) assets, along with current (and future spending) liabilities, to first determine whether the goal is feasible, and whether the household overall is overfunded, underfunded, or right on track. And to the extent that the household is over- or under-funded, adjustments can then be made to the “asset” side of the balance sheet (e.g., by adjusting the portfolio), or to the “liability” side of the balance sheet (e.g., by changing the spending goals). And when the value of all current and future assets (from portfolio assets and future savings, to the remaining human capital of future years of work, and illiquid “capital” like the value of Social Security benefits), along with all liabilities (from current liabilities like credit card and mortgage debt, to the “future” liability of spending goals themselves) are calculated on a present value basis, the investor gets a “pure” apples-to-apples comparison of whether the household is adequate funded or not.

In fact, in a recent paper entitled “The Shapes Of Retirement Planning: Are You A Curve, A Triangle, Or A Rectangle”, retirement researchers Patrick Collins and Francois Gadenne suggested that these three different approaches to determining the right portfolio for retirement – finding a portfolio on the Efficient Frontier using Modern Portfolio Theory, building goals-based investment buckets based on a hierarchy of goals, or allocating based on the overall “fundedness” of the entire household balance sheet after considering all assets and liabilities – form the basis of three different modeling approaches for retirement planning.

The distinctions between the models matter, because their different philosophical approaches mean that each may take substantively similar “inputs” (regarding the client’s goals and circumstances), but come up with different “outputs” (i.e., recommendations). Or viewed another way, each has its own “shape” that becomes the dominant lens through which retirement planning is viewed: the first is a “curve” (based on the efficient frontier); the second is a “triangle” (akin to Maslow’s hierarchy of needs, but applied in the context of a retirement portfolio); and the third is a “rectangle” (the assets-and-liabilities ledge format of a household balance sheet).

The Conflicting Shapes Of Retirement Planning

The fundamental challenge to these different shapes of retirement planning is that, in essence, they’re different models to analyze the possibilities, priorities, and optimal portfolios for retirement. They all take in various inputs about the client’s retirement goals and circumstances to produce some outputs, but the way those inputs are analyzed will differ… such that the “same” inputs can produce different outputs (i.e., different recommendations)!

For instance, the MPT framework focuses on an efficient frontier of portfolios that either maximize return for a given level of risk, or minimize risk for a targeted level of expected return. Finding the “right” portfolio is about matching the portfolio that best fits the required return for the client’s goal, without violating his/her risk tolerance. Yet Kahneman and Tversky’s work on prospect theory finds that people’s preferences regarding risk are impacted by where their finances stand when it comes to their goals in the first place; in other words, we experience more negative feelings about a loss than we do positive feelings about a gain, and whether something is a loss or a gain depends on where we currently stand financially.

Thus, a prospective retiree who has no wealth may look aspirationally towards accumulating $1,000,000 for retirement, while someone who already has $1.2M would be highly distressed by going down to $1M… despite the fact that they can both afford the same retirement at that point. And at the same time, the prospective retiree with no wealth who accumulates $1M experiences more happiness than the retiree who already has $1.2M and accumulates another $1M to grow the portfolio to $2.2M.

These distinctions matter, because it means the “best” portfolio with the traditional curve approach is simply the one that maximizes the risk/return tradeoff for a given level of risk, while with the “best” portfolio under the triangle approach, it may be OK to invest more conservatively after achieving enough to cover the goals (and ensure that the retiree doesn’t go backwards). Or viewed another way, the triangle approach recognizes that maximizing risk-adjusted return is not the sole goal (as it is with the curve approach).

Similarly, the MPT curve approach has limited tools to evaluate the trade-offs between using guaranteed income streams like a lifetime immediate annuity in lieu of a risk-based portfolio altogether. It takes a triangle approach to recognize that it might be a good idea to satisfy certain essential needs with guaranteed income, and then plan to fund discretionary expenses by building a “riskier” portfolio on top.

In turn, even a goals-based triangle approach struggles to recognize and plan around all of the assets that actually exist on the household balance sheet. For instance, the decision to delay Social Security can be especially effective at stabilizing the household balance sheet against low market returns or high inflation – as those factors benefit the delay of Social Security, even as they adversely affect other parts of the household balance sheet – but a goals-based framework has no effective tools to evaluate such trade-offs. By contrast, with the rectangle approach, the household balance sheet’s Social Security asset would rise in value as inflation increases, helping to offset the potential decline in the value of other fixed-income assets (and the rise in the “cost” of retirement as future spending liabilities increase with inflation). More generally, it takes a household balance sheet approach, where all assets and liabilities are discounted to a consistent present value basis, to truly understand whether the household is effectively “funded” in the first place, given all the different income and expense cash flows that may occur at different times throughout retirement.

And at the most basic level, even defining what is a “safe” investment will vary depending on the approach. After all, “safe” in the context of the curve approach – the efficient frontier of MPT – is simply a portfolio that is 100% cash. But with the triangle approach, “safe” would be a lifetime immediate annuity that covers all the essential expenses of retirement. And with a rectangle approach, “safe” would be a laddered TIPS portfolio that immunizes all future spending obligations against any changes in inflation or interest rates.

The bottom line: the shape of your retirement planning approach dramatically impacts the lens through which you evaluate what is a good or bad retirement strategy, or optimal allocation of (retirement and other) assets.

What IS The Optimal Shape Of Retirement Planning?

So given the varying retirement planning recommendations and conclusions depending on the curve, triangle, or rectangle shape to the analysis, what is the optimal shape of retirement planning?

Collins and Gadenne suggest that the rectangle approach, utilizing the household balance sheet framework, is the most comprehensive approach that allows for effective procedural prudence in the retirement planning process (an important issue in a fiduciary future). Notably, Gadenne is the Executive Director of the Retirement Income Industry Association (RIIA), which has built the curriculum of its own Retirement Management Analyst (RMA) designation around the Household Balance Sheet, which gives Gadenne some incentive to promote the rectangle approach. Though obviously, if the rectangle approach really is the most comprehensive and effective, that simply means the RMA has built around the ‘optimal’ approach.

That being said, though, it’s not entirely clear that the rectangle approach really is the most effective to formulate retirement recommendations… at least, not on its own. For instance, in calculating the household balance sheet – where all future cash inflows and outflows are discounted back to their present value – the results can be highly sensitive to the discount rate that is used in those time-value-of-money calculations. Whether or how “funded” the household is can vary significantly, with higher discount rates generally improving fundedness (as it implicitly increases assumed growth rates on assets and reduces the discounted cost of future liabilities)… yet nothing on the household balance sheet directly conveys the greater risk that is inherent in assuming a higher discount rate. More generally, there’s still very little agreement about what an “appropriate” discount rate is for analyzing various retirement strategies in the first place. Which means two advisors using the same rectangle approach may still come up with substantively different conclusions and recommendations about whether the prospective retiree is on track!

Similarly, there’s nothing about showing multiple goals on a household balance sheet that inherently prioritizes one goal over the other. The rectangle approach implicitly assumes that if the present value of all assets doesn’t add up to the present value of all liabilities, that the household is “underfunded”. But in the real world, if a prospective retiree doesn’t have enough money to retire and achieve all of their goals, saving more or earning more or working longer (to shore up the asset shortfall) aren’t the only answers. The retiree can also choose to settle for less, selectively eliminating lower-priority goals (e.g., retiring now but with a plan to take fewer vacations, or just rent instead of owning a second vacation home, or downsizing the retirement home and the associated cost of living, etc.). The rectangle approach is helpful to reflect if the current goal is feasible, but is a weak framework for prioritizing which goals to cut (or if the plan is “overfunded”, where to add to spend more).

And once the goals are selected and funded, it’s still necessary to actually allocate the assets to fund the plan, which entails some investment decisions and trade-offs. For which the rectangle approach would imply a form of asset-liability matching (e.g., liability-driven investing), though to the extent a portfolio is used (even if just for certain long-term goals), at some point an MPT-style approach to allocate the diversified portfolio still remains relevant. In other words, the rectangle approach still doesn’t eliminate the need for the curve approach; it just recognizes that the curve should be applied to allocate the portfolio at the end of the process (as those who just focus on the curve may miss the rest of the retirement picture).

Which means ultimately, the rectangle, triangle, and curve approaches all offer relevant contributions to the retirement planning process. The rectangle may help to determine whether the plan (as currently stated) is feasible and what’s possible, but the triangle approach is better for actually prioritizing goals, and the curve is still relevant when it comes time for portfolio implementation.

At a minimum, though, the Collins and Gadenne “shape” approach to retirement is an interesting way to think about different philosophical views, and different modeling approaches, when it comes to thinking about and analyzing a retirement plan, and more generally about the state of a household’s financial situation (now and in the future). For those who are interested in reading the full paper from the latest July/August issue of the IMCA Monitor, you can access it here.

So what do you think? What is the “shape” of your retirement planning process? Do you think one shape offers a more robust or relevant approach than the others? Or do you see all three working together, as the rectangle, triangle, and curve each help to evaluate Possibilities, Priorities, and the Portfolio itself? Please share your thoughts in the comments below!

The paper comes from a personal observation made in 2001 when I became the retirement client and interviewed a large number of financial professionals across the business silos: Plan Consultants and Advisors, RIAs, Registered Representatives, Licensed Agents, and Web-based services. These professionals presented different recommendations. Analyzing these recommendations showed that they were a collection of contradictory prescriptions.

One could argue that Retirement Engineering, Inc., RIIA, the CTR research project and related ventures are efforts to study the nature, the reasons, and thus the remedies for solving the contradictory prescriptions in order to make an understandable decision as a client.

The reasons for contradictory prescriptions may be a side-effect of looking at retirement planning from a product-view as contrasted with a client-view. The nature of contradictory prescriptions may come from confusing the part for the whole. At times, professionals with a product-view seemed engaged in a competition to prove that they were the smartest coercive utopian in the room. Being a natural-born skeptic, the argument from authority does not seem to be a good-enough reason for decisions. These product-focused debates felt like mental amputations that sacrificed the concrete and holistic client view at the altar of abstract product-based absolutism.

This first CTR paper presents what proved to be, personally and for other RMA Graduates, the most effective remedy for resolving the contradictory prescriptions: “Can you describe the Ideal Client for this Prescriptive Recommendation?” Do read the paper and let Patrick and I know what you think about it.

Thanks for the background Francois. I’m particularly interested in your response to Wade’s question/comment: “Isn’t the triangle approach a more detailed and comprehensive version of the rectangle approach?”

Likely best that all read the paper first in order to answer the question.

ok, here is a hint: It is a skillful professional task to determine the “best fit” between the “shape” of a retirement plan and the specifics of the client. See Table 1 in the paper for a selection of distinctions with a difference at the level of the Prescriptive Debates (and Contradictions) in the Financial Literature. The table arrays the selected debate items by Shape and by process steps (Input/Signal, Model/System, and Output/Response).

The rectangle enables scenario analysis which I believe is an important exercise to understand how well funded a retirement plan is.