Executive Summary

The sustainability of retirement cash flows from a portfolio depends in no small part on the returns generated by that portfolio – in particular, the real returns, given the pernicious impact of inflation over a multi-decade retirement.

In today’s high-valuation environment, many retirement projections are being done with reduced long-term return assumptions… with the caveat that while many advisors agree on the need to project lower returns, there is little agreement on how much lower it should be.

A look at the available market data suggests that realistically, it would be appropriate to reduce equity return assumptions by about 100bps (or 1 percentage point) over the next 30 years, to reflect the current valuation environment. Ironically, the reduction is not greater, because 30 years is such a long time that even if returns are bad for a period of time, there are enough subsequent years to recover as well.

In point of fact, though, it turns out that market valuation is even more predictive of 15-year returns, and that today’s high P/E ratios imply that between now and 2030, market returns could be reduced by as much as 400bps. On the other hand, because market valuations (and the associated returns) tend to move in cycles, this also implies that in the 2030s and 2040s, market returns could be as much as 400bps above the long-term average as well.

Ultimately, then, the ideal way to adjust return assumptions in a retirement plan in today’s environment may not be to reduce long-term returns at all, but instead to do projections with a “regime-based” approach to return assumptions. This would entail projecting a period of much lower returns, followed by a subsequent period of higher returns, in a manner that more accurately reflects the impact of market valuation on returns – and better accounts for the sequence-of-return risk along the way as well!

Impact Of Market Valuation On Long-Term Equity Returns

As Benjamin Graham famously said, “in the short run, the market is a voting machine but in the long run, it is a weighing machine.” The fundamental point that the father of value investing was trying to make: while in the short term market prices generally move based on the market psychology of what’s popular (and not necessarily based on what the investment is “really” worth), in the long run markets eventually weigh an investment based on its underlying value.

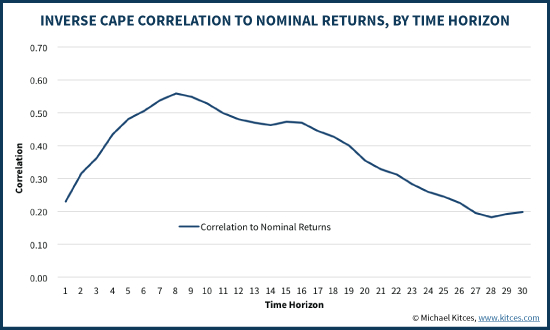

And as the data reveals, this phenomenon really is true; in the short run, market returns exhibit little relationship with their underlying market valuation (the correlation between returns and valuation is low). Over longer term time periods, though, market valuation actually exhibits a remarkably high correlation with subsequent compounded market returns! For instance, the chart below shows the correlation between the overall P/E levels of the market (based on the Shiller CAPE) and subsequent returns of various time periods. The longer the time horizon, the better the correlation between market valuation and the returns that follow.

On the other hand, the data also reveals that in the ultra long term (e.g., 20+ years), market valuation actually becomes less predictive of equity returns. In other words, while market valuation is predictive for long(er) term market returns, eventually so much time has passed – and so much has changed – that the starting valuation is just no longer predictive of how markets grow and compound 20-30 years later. In fact, valuation is even less predictive of 30-year returns than it is in predicting 12-month returns!

Shiller CAPE And Real Equity Returns

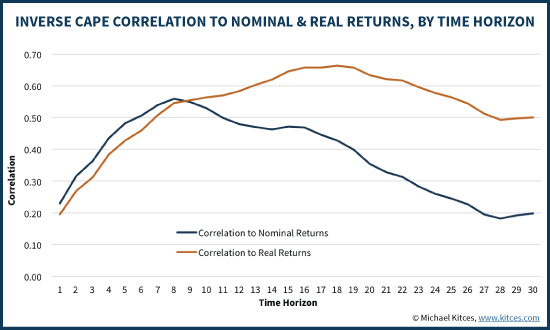

Of course, the caveat to the chart above is that in the end, it’s not just about nominal investment returns to fuel long-term retirement spending, but real investment returns. After all, if the whole point of having equities for growth in the portfolio is to allow the portfolio to maintain spending power, it’s necessary for the equities to actually generate a favorable real rate of return.

Ironically, though, as it turns out, market valuation measures like Shiller CAPE are actually even more predictive of real market returns than it is just nominal returns! Or viewed another way, one of the reasons why long-term nominal returns are not well predicted by market valuation alone is that inflation confounds the picture. Yet since the ultimate goal is to project based on real returns anyway, using market valuation to predict real returns is just even more predictive!

As the chart reveals, there is a correlation of almost 0.50 between the Shiller P/E ratio at the beginning of a time period, and the 30-year average annual real compound return that follows from the initial market valuation starting point.

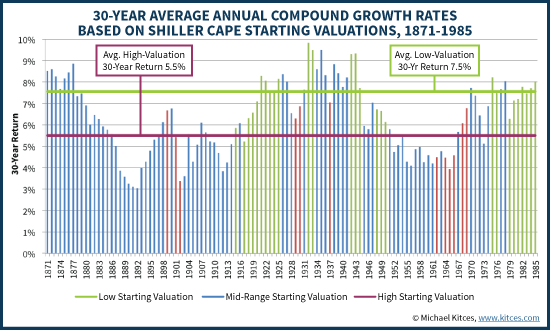

In addition, the data reveals that the predictive relationship holds up in both higher valuation environments, and lower ones. For instance, the chart below shows the 30-year average annual compound growth rates for every starting year going back to 1871; time periods with starting valuations in the top 20% (a Shiller CAPE above 22) are colored red, while those with starting valuations in the bottom 20% (Shiller CAPE below 12) are green, and the rest (somewhere in the “muddled middle” 60%) are blue. Overall, the average 30-year real return is 6.3%, but while there is some variance of returns from high and low starting valuations, overall as expected the average of the high valuation zones is only 5.5%, while the lower valuation zones produced a 7.5% average return.

Notably, these results also suggest that even at valuation extremes, it would not be appropriate to adjust long-term equity returns by more than about 1% (or 100bps) in either direction. Which means even in today’s high valuation environment, where the Shiller CAPE is about 25.9, at the most it would only be appropriate to reduce long-term returns by 100bps.

30-Year Returns Are Comprised Of 15-Year Secular Bull and Bear Market Cycles

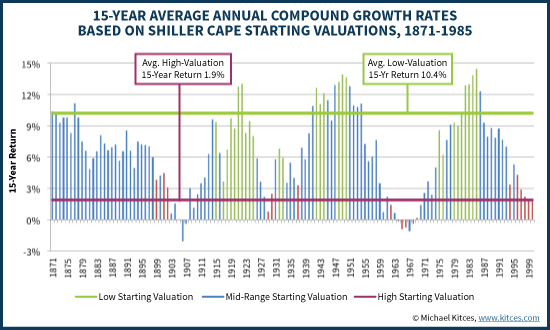

One important caveat to using market valuation to project 30-year return expectations is that, as noted earlier, while there is a significant correlation between Shiller CAPE and subsequent market returns, the peak correlation is actually after the first 15 years, and falls thereafter.

Over that first 15-year period, though, valuation is even more predictive of returns. For instance, the chart below shows the rolling 15-year real returns on equities, again segmented by whether the starting valuation was high, low, or in the middle. While over 30 years, market valuation suggests that the long-term return should only be changed about 100bps above or below the overall average, on a 15-year basis low-valuation environments have an average real return of 10.4% while high-valuation environments average only 1.9%!

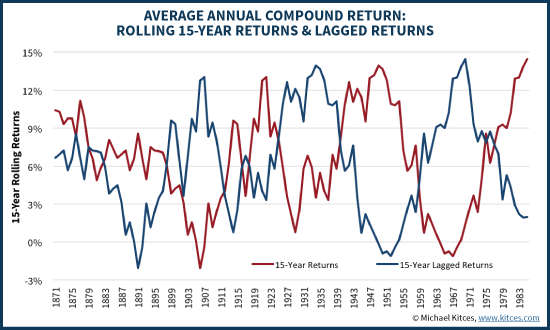

On the other hand, while market valuation is more predictive of the first 15-year period than the whole 30-year period, it turns out that the subsequent 15 years aren’t entirely “random” either. In fact, because markets tend to move in cycles, especially poor 15-year returns in one period end out being predictive of good 15-year returns in the subsequent period.

The chart above shows, for any given starting year, the average annual compound return in the first 15 years (red line), and the average annual compound return for the second (subsequent) 15 years (blue line). For instance, the first data point in red is, starting in 1871, the 15-year average annual compound equity return from 1871 to 1885 (15 years inclusive), while the blue line is the subsequent 15-year return from 1886 to 1900 (or the 15-year-lagged 15-year returns).

What the chart reveals is that bad 15-year returns in the market tend to be followed by good 15-year returns. The lines move in nearly perfect opposition to each other. Thus, there’s actually a 0.67 correlation between market valuation and subsequent 15 year returns, but there’s also an inverse -0.32 correlation between market valuation and the 15-year-lagged 15-year returns that follow!

In other words, high valuation actually predicts good future returns beginning in 15+ years, albeit only at a “cost” of bad 15-year returns between now and then. In today’s context of high market valuation, this implies below-average returns between now and 2030, but unusually high above-average returns in the 2030s and 2040s!

Regime-Based Equity Return Expectations For Retirement Projections

The key point of cyclical market returns is that just looking at market valuation to adjust (or in today’s environment, reduce) long-term returns actually misses out on an even more meaningful relationship between starting market valuation and alternating 15-year cycles that tend to follow. While market valuation extremes indicate 30-year returns may deviate by +/- 100bps, the valuation extremes indicate that 15-year returns may deviate by a whopping +/- 400bps (and tend to alternative)!

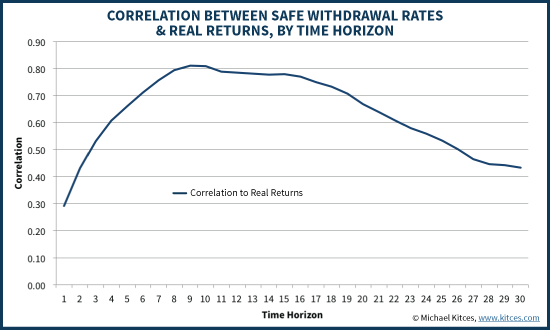

And the fact that market valuation predicts 15-year market cycles so effectively is especially important given that, for retirees, the sequence of returns early in retirement has a significant impact on the long-term sustainability of the retirement withdrawals. After all, the safe withdrawal rate is actually far more correlated to 15-year real returns that it is to 30-year real returns!

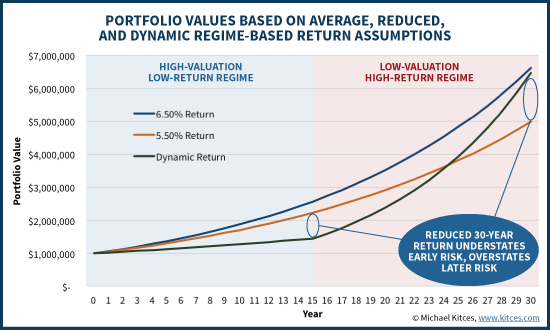

The significance of this dynamic is that it actually illustrates a significant “gap” in today’s retirement planning software. What the data suggests in a high-valuation environment today is that a “good” solution would be to reduce the long-term equity return by 100bps, but a “better” solution would be to illustrate 15 years of significantly below average real returns (e.g. reduced by 400bps), followed by 15 years of significantly above average real returns (increased by 400bps above the average!).

In other words, the optimal way to adjust retirement projections for extreme levels of high market valuation is not to reduce long-term returns by a little, but to reduce “intermediate” term returns by a lot for the current low-return “regime”, followed by a subsequent period of significantly higher returns (as the first 15 years of low returns amidst any level of ongoing economic growth eventually results in a low return environment). Doing so is superior because it more properly matches the true risk of high-valuation environments: exacerbated exposure to sequence of return risk, as valuation extremes trigger an especially high likelihood of a bad decade of returns, which is especially problematic for retirees sensitive to the first decade’s worth of returns!

Sadly, though, today’s financial planning software packages are incapable of modeling regime-based retirement projections – not because it’s impossible, or even difficult, to program, but simply because it’s not be programmed to do so. Hopefully that will change soon!

So what do you think? What equity return assumptions are you using for retirement projections? Are you reducing returns in today's environment? If so, by how much? Please share in the comments below!