Executive Summary

Financial planning is focused heavily on establishing and working towards very big long-term goals, from saving for a child’s education to accumulating the assets to fund a multi-decade retirement.

Yet the fundamental problem of “big” goals – financial planning or otherwise – is that they can seem so big and overwhelming that it’s actually demotivating. In the extreme, the goal may feel so distant and unachievable that it simply leads the person to give up on pursuing the goal at all!

Accordingly, the reality is that to really make long-term financial planning goals achievable, the key is to break them down into smaller pieces first. As the saying goes, the way to eat an elephant is one bite at a time. And the research of behavior change and motivation is increasingly finding that the “small wins” of successfully achieving small goals may actually be the key to helping us rewire our brains to stick with the new behavior in the long-run!

Unfortunately, though, financial planning education provides little in the way of training on how to break down big goals into small ones, and most financial planning software does a poor job of helping clients to track short-term goals!

Nonetheless, in the world where the actual implementation of goals – i.e., into saving and investment accounts – is becoming increasingly commoditized, arguably it will be the process of helping clients break down big financial planning goals into smaller SMART goals that are Specific, Measurable, Achievable, Relevant, and Time-bound, and then providing them the tools to track progress and serving as an accountability partner to ensure follow-through, that may be the greatest financial planning value-add of all!

Managing Big Financial Planning Goals – How Do You Eat An Elephant?

There’s a famous saying in the world of goal setting: “How do you eat an elephant? One bite at a time.”

The point of the statement is the recognition that if you try to tackle an enormous goal all at once, it can seem overwhelming, to the point of feeling so unachievable it’s not even worth trying. Instead, if you want to be prepared to succeed in a monumental sized goal, the key is to break it down to smaller, bite-sized (literally, in the case of eating an elephant!) goals that are feasible and achievable.

In fact, a growing base of research on motivation and change finds that it’s actually the process of setting small goals, and achieving small wins, which impacts our brain chemistry in a way that propels us to completion of a long-term goal. It’s not merely that the successes in achieving our goals makes us feel good, such that we want to continue to pursue the goal to enjoy more of that good feeling. More recent research on the dopamine neurotransmitter is finding that it may actually be the basis for motivation itself – if you achieve small goals, the dopamine firing along those brain pathways reinforce the behavior into a habit, making it your new normal. In other words, small wins trigger dopamine that actually helps “rewire” your brain to keep you doing those good behaviors, which in turn keeps you on the path to long-term success in the future.

In other industries and realms of behavior change, this phenomenon is already “common knowledge” and is applied regularly. For instance, it’s no coincidence that a FitBit device encourages you to walk 10,000 steps per day. Over the span of a year, that’s actually 1,825 miles(!) of walking, but it’s virtually impossible for anyone with a New Year’s resolution to walk 1,825 miles in 2016 to keep that focus throughout the year. Instead, FitBit breaks that down to “just” 5 miles per day, and because even 5 miles feels daunting to most, breaks that down into 10,000 steps per day, and then counts each step all day long. The end result – we’re better on track to walk the entire 1,825 miles in a year, but only because we’re breaking the goal down to literally one step at a time.

Similarly, we know that losing 1 pound of weight requires us to burn about 3,500 more calories than we take in. But if you wanted to lose 25 pounds in a year, saying “I will generate an 87,500 calorie deficit this year” again feels absurd. A more realistic goal is to lose ½ a pound per week, which is just a 1,750/week calorie deficit. Breaking that down even further, a 25-pound weight loss goal is “just” giving up 250 calories per day. And 250 calories are just a few small meal adjustments (e.g., eliminate the cheese from your hamburger, get a small soft drink instead of a large, or getting thin-crust instead of pan pizza), or about 30-60 minutes of any moderate physical activity.

Breaking Financial Planning Goals Into The Smallest Goal Bits

As a recent article from Morningstar pointed out, while these techniques of creating bite-sized goals are done regularly in the world of exercise and weight loss, they’re rarely applied at all when it comes to financial planning (or financial advisors themselves!)!

Instead, financial planning tends to focus on big, long-term goals, like saving $1,000,000+ to fund a multi-decade retirement, or accumulating “just” $50,000, $100,000, or $250,000 to cover a baby’s college expenses in 18 years. Yet the problem – just as is the case for someone who plans to walk 1,825 miles this year or cut 87,500 calories from their diet in the next 365 days – is that these goals are too big, too distant, and too overwhelming to actually be effective at changing our behavior! They’re elephants, with little guidance on how to eat them.

To be fair, as financial advisors we often do break accumulation goals into more bite-sized savings elements. A $1,000,000 accumulation goal for a young investor with a 40-year time horizon can be broken down into saving $300/month and investing for an 8% return. A $100,000 college savings goal in 18 years is about $220/month at the same return assumption.

Are Savings Goals Really Spending Goals?

Yet for many households, this itself is actually still an insufficient breakdown of the goal to really be feasible for implementation, because the household may not have an available $300/month or $220/month to save in the first place. In other words, achieving an accumulation goal requires a saving goal, but achieving a saving goal may require a spending modification goal first.

So helping someone reach the long-term accumulation goal really requires setting goals for spending changes instead. Is there $100/month of “old” recurring subscriptions that could be eliminated? Is there room to trim $100/month from the restaurant budget? Could the family do one vacation via road trip instead of flying, saving $1,000+ on flights for the year.

Ultimately, then, the key for facilitating behavior change is not just breaking down a big goal into smaller ones, but ensuring that the smaller goals are small enough to actually be achievable. And for most households, the smallest unit of goals are actually not about accumulation and savings; they’re about spending and managing cash flow, which is the true financial lifeblood of the household!

The Real Relevance Of Goal Tracking And Progress

An important related issue to breaking down goals into bite-sized pieces is providing the feedback – the progress tracking – necessary to affirm that someone is on track for achieving their goal.

For instance, in the case of getting healthier, it’s not about merely having the goal to do 10,000 steps every day. It’s also about having a means to track whether you’re actually achieving that goal. In fact, when we’re trying to change our behavior or achieve a goal, that feedback is so critical, we crave it. Thus the explosive growth of FitBit and other fitness tracking devices in the first place!

Yet when it comes to financial planning, unfortunately this too is an area where advisors are often lacking – due primarily to the fact that we don’t even have good tools in order to provide that feedback to clients in the first place!

For example, many financial planning software tools don’t even have the capability of setting a goal for a client, and showing/tracking their progress towards the goal. Sure, you can create a financial plan, and then update it from time to time, and let the client see that the outcome appears to be improving. But that’s a complex process, that doesn’t provide the kind immediate feedback to really encourage the behavior. Nor ultimately does the progress move very quickly anyway. If a 44-year-old client had saved 33% of their retirement savings goal, and after a year of active saving and hard work is up to 34.5% of their accumulation goal, that isn’t actually much of a reinforcement for a year’s worth of effort!

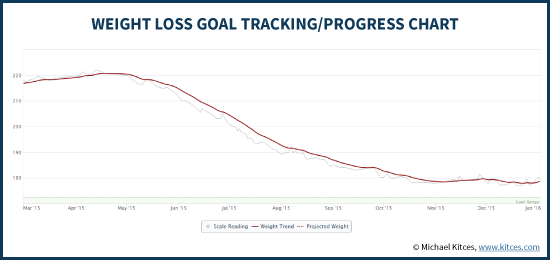

Similarly, in the health context, if the only way to find out if you were successfully losing weight was to go into the doctor for an annual physical, the feedback would not be easy and regular enough to really help. Instead, we need a scale we can step onto daily, and even a fitness tracker to give us the updates throughout the day. For instance, when I went through my own significant weight loss last year, it was the daily and weekly updates to this chart – and the sense of progress it provided – that helped to reinforce my efforts and keep me on track.

So what would relevant goal-tracking look like in the world of financial planning? As noted above, a client dashboard that just shows progress towards a (multi-decade) retirement goal is not actually very useful. Instead, once again, it arguably comes down to cash flow. This is true both because it’s the cash flow changes that actually drive the success of a savings goal in the first place, and also because over time accumulation goals are increasingly driven by uncontrollable external factors (like market returns) while cash flow goals are still under the client’s control. In other words, by focusing on cash flow goals, attention is focused on what’s controllable that can have real impact on the outcome, and the goals can be broken down into bite-sized pieces.

Setting SMART Financial Planning Goals

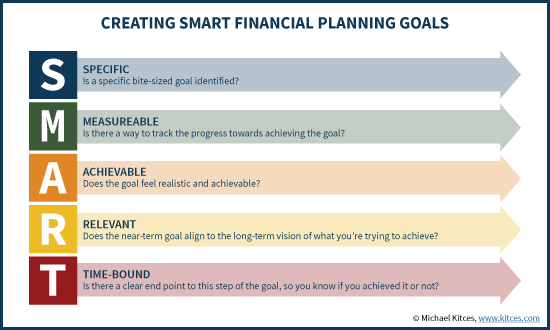

A popular acronym from the goal-setting literature is to create a “SMART” goal.

SMART stands for goals that are Specific, Measurable, Achievable, Relevant, and Time-bound (i.e., have a concrete deadline or finish). In other words, to have a good goal, you need to be very clear about what you’re trying to do, be able to measure it, ensure that it’s realistically achievable, is relevant to the long-term vision you’re trying to achieve, and has an end point (at least for that step of the goal) so you can affirm whether it was really done or not.

In this context, the purpose of the financial planner is to help clients set what these SMART goals should be in the first place. Of course, the client has to come to the table with the long-term goal (perhaps with the advisor’s help to evaluate what’s even possible in the first place), but helping to identify appropriate and realistic tactical goals to make progress – and then provide the tracking and feedback and accountability – are actually key value propositions of a financial advisor in the first place.

In other words, arguably one of the key benefits of a financial advisor is showing clients how to break down “elephant-sized” goals into “bite-sized” SMART goals that can be set, monitored and tracking, and achieved. But that requires ensuring that the goals really are set in an appropriate bite-sized manner, that the advisor (and client) have the tools to monitor and track progress, and that the advisor is ready to serve as an accountability partner to help the client stay on track! Notably, though, in a world where the implementation of the goal itself – i.e., the investment or savings account – is increasingly commoditized, this “coaching” and “goal-setting” aspect of financial planning may be one of the most significant value-adds that financial advisors can bring to the table (at least/especially when it comes to those still accumulating for retirement and other goals in the first place!).

So what do you think? Should advisors have a role in setting SMART financial planning goals for clients, and helping them break down big goals into smaller parts? As an advisor, do you feel like you have all the tools necessary to actually do this with and for your clients? Are you considering whether to change how you set action items and recommendations for clients to help them break them down into SMART bite-sized goals?

What you say is true, however it’s incredibly challenging to get compensated for financial coaching anywhere near what one can for selling product (or providing strictly investment advice). Coaching also requires a significantly larger set of interpersonal tools including empathy. The skills involved are hardly even mentioned in the CFP(r) curriculum, much less on a Series whatever exam. I have hope that commoditization of the provision/implementation of investment advice ultimately drives the ability to charge for it to zero (go robos!).

Where do real skills come in? Coaches guide clients through processes that tap motivation, foster clarity, create legitimate successes that align with the client’s real values.

Agree wholeheartedly that cash flow analysis and monitoring is the best way to communicate and track progress towards client goals. The “goals” feature in mint.com (full disclosure: I do not work for mint.com, I am just an enthusiast who is not compensated in any way for writing about my experience using the free software tool) has been a nice feature for shorter and longer term goal tracking when using mint.com as a tool to track 100% of our household accounts and transactions across three businesses and our personal expenses–all accounts (assets and liabilities) must be added as well as all transactions regularly categorized (the automation works accurately only about 80-90% of the time); and it’s nice in our marriage to keep each other accountable on our expenses by weekly reviewing and updating our categorizations as well. We call it “Money Monday Date Night,” and hey, it works for us!

We can then use mint.com to match our numerical goals to a specific account(s) that we have (Retirement accounts for retirement goals, online savings accounts for shorter term liquid goals like a home downpayment fund), which then are calculated for us whether we are “on track” or not with those familiar gamification status bars in red or green and which depend on our monthly contributions to these targeted funding accounts. The “goals” feature in mint.com is also automatically integrated into the budgeting feature as well, so total “expenses” include budgeted item estimates and actuals in addition to goal funding settings, so total “savings” are accounted for as an expense line item from the “Budgets” tab. Goals are also identified with projected month and year of completion; an obvious advantage in motivation for shorter term goals, not to mention the special “fanfare” upon actual goal achievement in the software which includes the “Mark this goal as completed?” option :).

In our financial planning practice, we’ve experimented with using mint.com along with clients and similar cash flow tracking software with some initial successes as well as simple Excel spreadsheets tracking annual expenses on a monthly basis monitored quarterly against “actual spending”. However, we know that the software that works will be the software that can be used to consistently reduce debt and increase a client’s ability to contribute to their goals regularly in relation to their increasing net worth–the data will confirm success.

The downside is that it’s been difficult to find software like mint.com (or a client’s desktop instance of Quicken, credit card spending analysis, etc) with an agnostic (not sponsored by one bank or one product) “advisor-facing” portal to organize and communicate through digitally and securely with clients and their transaction/goals/budget data. It’s also been difficult to find automated cash flow tracking software that is more consistent with categorizing transactions more accurately, we find about 5-20% of transactions are mis-categorized (this is not exclusive to only mint.com) which then can and does negatively impact the budget/goals feature accuracy if not corrected and updated since the categorization mechanism is what drives those two features. Without accuracy, the budgets and goals features become less meaningful and momentum is easily lost.

Agree with the other commenter that empathy and coaching skills are invaluable for this type of financial planning practice. Michael: do you recommend any coaching/training programs that you’d recommend for improving client relations for a CFP professional in this fashion featuring SMART goals as you’ve described?

Any potential profits lost to servicing clients completely in a fee-only fashion, and helping clients reach their financial goals (short and long term), have so far vastly been compensated in becoming enriched in the very reason I entered the CFP field which is to help people reach their financial goals successfully and develop excellent relationships with clients in order to build a business based on these values. I don’t feel that same connection in my career to any specific products or product sales more than the fee-only service aspects of the profession as described.

nice artical

Financial designing is important to business success. Without it, you just won’t understand if your business is profitable — if you’re ultimately doing things right. Below you’ll notice 10 necessary reasons why you would like to form money designing a priority for your business. If you would like facilitate making a plan, you’ll apprehend from business designing books or associate comptroller.To get more update please visit us- https://goo.gl/jghnvS

Nothing taught me this lesson so well as the weekly savings bank program that my elementary school had during the 1950’s. After depositing a $1 a week for almost three years I was rewarded with $5 from the bank.