Executive Summary

State-Registered Investment Advisers (RIAs) are subject to numerous regulations in the state(s) where they do business, which, though they vary from state to state, generally have the goal of protecting investors from fraudulent sales practices. These rules require RIAs to file documents (such as Form ADV) with the state, maintain books and records, provide disclosures to clients, and act in the clients’ best interests whenever providing financial advice. Additionally, many (but not all) states set minimum financial requirements – in the form of minimum net capital and/or surety bond requirements – that RIA firms must maintain in order to become (and remain) licensed, to protect consumers from both the risk of fraud, and simply the consequences of negligent or inaccurate advice that could cause them harm. Because of the many differences between each state’s requirements, though, it’s important for RIA owners (especially the founders of new firms) to know their state’s particular rules and how to comply with them.

In this post, Kitces Senior Financial Planning Nerd Ben Henry-Moreland discusses how owners of state-registered RIAs can better understand their minimum net capital and surety bond requirements, and what protection they do (and don’t) provide for both clients and financial advisors themselves.

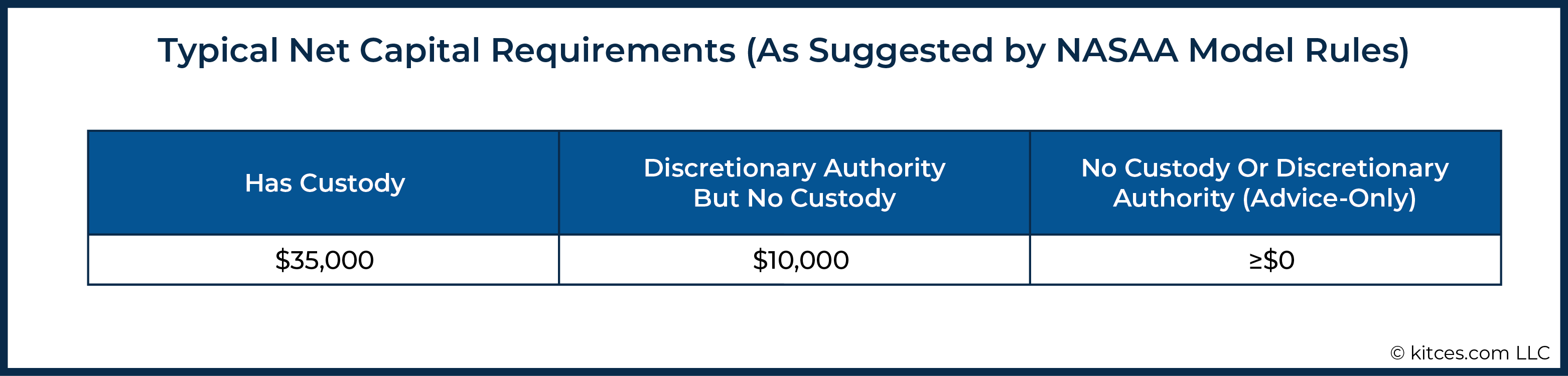

In states that set minimum net capital requirements, an RIA must hold a certain level of assets over its liabilities. This amount varies not only from state to state, but also often within states, depending on whether the RIA holds custody of client assets and/or has discretionary trading authority over client funds. In practice, states most commonly require RIAs to hold $35,000 of net capital if they have custody, $10,000 if they have discretionary trading authority (but not custody), and to have at least a $0 (i.e., positive and not-negative) net worth if they are an advice-only firm (no custody or discretion), which must be satisfied by holding cash or other marketable (i.e., liquid) investment assets.

In lieu of maintaining a certain amount of capital, though, some states permit RIAs to cover some or all of their net capital requirements with a surety bond instead. State rules for surety bonds can also vary widely, with some states requiring RIAs to hold a surety bond, others allowing firms to purchase a surety bond in lieu of maintaining the state’s net capital requirements, and some choosing not to sanction the use of surety bonds whatsoever. In states that do allow (or require) surety bonds, RIA owners need to know how surety bonds function, what the potential risks of having a surety bond may be, how their state’s surety bond and net capital bond requirements interact (and how to decide whether or not to buy a surety bond if they have a choice), and how to find the best surety bond provider to meet their needs. Though ultimately, surety bonds are appealing relative to net capital requirements because of their significantly lower cost – typically about 1% of the face amount, which means paying $100/year for a $10,000 surety bond.

While net capital and surety bond requirements provide some level of financial protection to RIA clients, that protection is minimal compared to what many clients may actually stake on their advisors’ recommendations. In practice, a legal claim by a dissatisfied client could result in a liability for the RIA that is many times greater than the state’s minimum financial requirements. Accordingly, RIA owners can protect themselves with additional layers of coverage (such as Errors & Omissions insurance) above the minimum amounts that may be required by the states in which they operate. Especially since a surety bond provider has the right to collect any client claims from the advisor, which means it does help ensure a client is made whole – similar to E&O insurance – but doesn’t actually protect the advisor’s own assets the way E&O coverage does!

The key point, though, is simply that because financial advisors are expected to give good advice, and can be held financially liable for advice that results in undesired financial outcomes for their clients, they must have the financial wherewithal available to cover any liabilities resulting from a client’s legal claims. State minimum financial requirements are one of the few ways to ensure that RIAs have assets available (or a surety bond in lieu of assets, where permitted) so clients can be compensated for any damages. But part of being a trusted professional is taking full accountability for the consequences of professional advice… which means it’s essential for the RIA to know not just how much coverage they need to secure to meet their state’s requirements (and in what form), but also how much additional coverage they may need to fully protect themselves (and their clients)!

Registered Investment Advisers (RIAs) that have under $100 million of assets under management or serve clients in fewer than 15 states are typically required to register with their home states’ securities regulators. These state-registered RIAs are subject to a suite of state-specific securities regulations collectively known as “Blue Sky Laws”. The first Blue Sky Laws were originally created over a century ago to protect investors from fraudulent stock sellers by requiring securities issuers to register with the state(s) where they do business. They have expanded in scope beyond just securities issuers throughout the 20th century to also include state-level regulation of broker-dealers selling other types of securities products in the state, and RIAs providing investment advice to those living in the state.

In general, Blue Sky Laws prohibit dishonest or unethical conduct by financial professionals, and require all RIAs doing business in a state to be registered or licensed with that state, keep accurate books and records, and provide potential clients with disclosures about their services, fees, and conflicts of interest. States also outline specific requirements for registering as an RIA, which include the filing of Form ADV, passing a competency exam (usually the Series 65 exam, or the Series 66 and Series 7 exams; though this requirement is waived by many states for holders of the CFP, CFA, or ChFC designations), and filing a statement of financial condition or balance sheet.

Additionally, many states set minimum financial requirements that RIAs must maintain in order to be registered. These requirements vary from state to state, but they usually stipulate that RIAs must hold a minimum level of net capital (also referred to as “net worth” by many states) at all times, and/or obtain a surety bond which guarantees the payment of a client’s legal claim (up to a certain amount) if the RIA is unable to do so.

Because, while most Blue Sky Laws are designed to ensure that clients of RIAs receive advice that is competent, fair, and free from conflicts of interest, they do not guarantee that clients will always receive the best advice, or that they will always be happy with the advice they receive. In some cases, the advisor may simply give incorrect advice. And no matter the intentions of the advisor, misunderstandings or unforeseen outcomes can lead a client to feel as though the advisor has failed to live up to their professional obligations. Furthermore, because clients often stake large financial decisions on the advice that advisors give, the consequences of something going wrong (through ignorant or negligent advice) can have an enormous impact on those affected.

Consequently, courts may hold advisors liable when they give advice that leads to financial harm. The outcome of such cases might be a legal judgment or settlement requiring the RIA to repay the client for advisory fees, trading costs, and/or even market losses incurred… but, in order for the client to be compensated for their losses, the RIA needs to have assets available to pay the claim.

Thus, the core purpose of minimum financial requirements is to ensure that an RIA does have the assets available to pay clients if they are ordered to do so. A legal judgment against an advisory firm with more liabilities than assets on its books could result in the firm’s bankruptcy, with clients receiving only a fraction of what they are owed. And in the case of an RIA that does go out of business, the firm would still need enough capital available to wind down its operations in an orderly way, including paying any creditors, vendors, or employees it still owes, in addition to ‘making good’ to damaged clients.

Therefore, while it may seem odd for the state to be concerned with the financial condition of private businesses, states set minimum financial requirements for RIAs to protect investors who fall victim to fraudulent or negligent advice… with the caveat that no two states’ requirements are exactly alike. In other words, by requiring firms to have a certain amount of assets available to pay clients’ legal claims (or a surety bond to cover those costs), states can ensure that RIAs are accountable – at least up to some minimum level – for the advice they give.

Which means that, for financial advisors who are starting a state-registered RIA or who are considering doing so (and even for experienced firm owners), meeting these requirements (specific to whatever state they’re in) is more than just another box to check in the initial registration or renewal process. Because complying with state regulations requires (at minimum!) enough understanding of that state’s financial requirements to know how much the RIA needs to maintain in net capital and/or surety bond coverage and knowing how to find and purchase a surety bond if needed.

While meeting state minimum net capital and bonding requirements is necessary for the sake of complying with state regulations, though, what may be even more important for the financial health of the business is for RIA owners to understand these concepts at a deeper level to help them make better business decisions and live up to their fiduciary obligations to their clients.

After all, the minimum level of protection provided by a state’s net capital or surety bond requirements may be very small compared to the actual amounts that clients stake on their advisors’ recommendations. If a client were to raise a legal claim, an RIA maintaining only their state’s minimum financial requirements may still not have the resources to fully ‘make good’ on their liability. And almost certainly wouldn’t have enough to continue the business after making good on the harm that was (even if unwittingly) caused.

Thus, for advisors to truly be accountable for the quality of the advice they give, they must understand not only what their state regulators require of them, but also what they must do in addition to those minimum requirements to fully protect themselves and their clients.

Nerd Note:

Currently, only state-registered RIAs are subject to minimum net capital and bonding requirements, as SEC-registered investment advisers (unlike broker-dealers) have no similar requirements. In 2018, the SEC put out a request for comment on areas of “enhanced investment adviser regulation” including minimum financial requirements for SEC-registered firms, suggesting that this could change eventually. However, the request was overshadowed by the SEC’s concurrent release of its Regulation Best Interest rule and the new Form CRS; as of the publication date of this article, the SEC has not released any subsequent proposals on the matter.

Minimum Net Capital Requirements For State-Registered RIAs

Unlike some RIA registration requirements (such as filing Form ADV) that are uniform throughout all 50 states (plus the District of Columbia, Puerto Rico, and the U.S. Virgin Islands), net capital and bonding requirements can differ greatly from one state to the next. The specific reasons for these differences may be as numerous as the states themselves, but the variations in requirements most likely reflect attitudes between different states’ regulators about the protection they provide to investors, versus the degree of administrative and financial burdens these requirements place on RIAs (as in the end, if the requirements are too stringent, few will be able to afford to start RIAs to serve consumers in the first place!).

NASAA Model Rules For RIA Net Capital Requirements

The North American Securities Administrators Association (NASAA), an organization of state, territorial, and provincial securities regulators from the U.S., Mexico, and Canada, created its Model Rules 202(d)-1 and 202(e)-1 in an attempt to establish some uniformity in state net worth and bonding requirements. For example, the NASAA’s Model Rule sets minimum net worth requirements of $35,000 for RIAs with custody of client assets, and $10,000 for those with only discretionary authority (where the assets themselves are held with a third-party RIA custodian, such as Schwab, Fidelity, or Pershing).

While about half of the states have fully adopted these Model Rules, the rest have either adopted only parts of the Model Rules while leaving out some sections, or else have created their own regulations entirely independent from the Model Rules.

For example, in Iowa, both minimum net capital and surety bond requirements for RIAs conform closely to the Model Rules. Its neighbor to the north, Minnesota, conforms closely to the Model Rules for its minimum net capital requirements but not for its surety bond requirements (which are unique to that state). Meanwhile, its neighbor to the west, Nebraska, does not conform to the Model Rules at all, but has its own (entirely different) set of net capital and bonding requirements.

Despite the numerous differences across states, there are some common themes when it comes to minimum financial requirements (including important areas where states often tend to have their own unique rules) that can help RIA owners navigate the process of complying with their own state’s requirements. For instance, the term “Minimum Net Capital” generally refers to the need for an RIA to hold a certain level of assets in excess of its liabilities:

The simplest and most common way for an RIA firm to hold net capital is in the form of cash in its bank account (typically a business account, covered in greater detail below). In most states, only cash or other readily marketable assets are used in calculating a firm’s net capital because the intent behind the rule is to be able to convert these assets to cash quickly in the event that it is necessary to pay client claims.

Likewise, it is common for many states to exclude certain types of assets from net capital – which might otherwise appear on a firm’s (or an individual advisor’s) balance sheet – that may not represent easily accessible funds, such as:

- Intangible assets (e.g., prepaid expenses, patents, and copyrights);

- Personal property that is not readily marketable (e.g., home, furniture, or car); and

- Loans to stockholders, officers, and partners.

Custody Vs Discretionary Authority Requirements

In most states, an RIA’s minimum net capital requirement depends on whether they have custody of client funds and/or discretionary authority to trade in client accounts. States’ definitions of “Custody” generally align with that of the SEC, as follows:

An adviser has custody of client assets…when it holds, "directly or indirectly, client funds or securities or [has] any authority to obtain possession of them."

On the other hand, the SEC says an advisor has “Discretionary Authority” when they have “the authority to decide which securities to purchase, sell, and/or retain for [their] clients.” In other words, the advisor has the authority to place trades in client accounts without first asking permission to do so, but doesn’t necessarily hold those client assets (e.g., because they’re held with a third-party RIA custodian like Schwab, Fidelity, Pershing, etc.).

Both Custody and Discretionary Authority give the RIA a certain level of direct control over client assets. In the case of Custody, the RIA has the power to withdraw assets from client accounts; and with Discretionary Authority, they have the power to make investment decisions and trade within those accounts. Both situations, therefore, carry the risk that a client will take issue with their advisor’s decision after the fact (for example, perhaps the advisor reallocated the client’s investment portfolio, which then declined in value due to market volatility) and seek restitution for any financial loss they incurred.

Consequently, a state’s minimum net capital requirements often take into consideration the additional risks involved when RIAs have (increasing levels of) control over their clients’ accounts. RIAs with custody have the greatest level of control, since they are able to transfer assets from clients’ accounts to their own, and subsequently generally have the highest minimum net capital requirements.

Example 1: Douglas owns a state-registered RIA in Portland, Maine. The firm offers bill-paying services to their high-net-worth clients, which gives them the ability to make withdrawals from client accounts (needed in order to make their bill payments). This meets the state’s definition of custody over client assets.

Maine’s minimum net capital requirement for RIAs with custody is $35,000, so Douglas’ firm will need to maintain at least $35,000 of net capital to comply with the state’s requirements.

Those with discretionary authority only (i.e., without custody), who can place trades in clients’ accounts but not withdraw funds, typically have a lower minimum net capital requirement than those with custody.

Example 2: Tricia owns a state-registered RIA in Brunswick, Maine. The firm offers investment management but does not offer any services that would trigger custody over client accounts, as all of its client assets are custodied with Schwab Institutional, with a Limited Power of Attorney (LPOA) authorization to enact trades in the client’s account.

Maine’s minimum net capital requirement for firms with only discretionary authority is $10,000, so Tricia’s firm will only need to maintain $10,000 of net capital to comply.

RIAs with neither custody nor discretionary authority (e.g., firms that only offer financial planning and investment advice, but do not offer investment management) have no direct control over client assets, and while some states have a separate minimum net capital requirement for these firms (for example, Hawaii requires RIAs without custody or discretionary authority to maintain at least $5,000 in net capital), they are often simply required to maintain a positive net worth.

It’s important to note again that the rules are state-specific and, while these themes are common to state regulations in general, any particular state can have variations not only in its top-level net capital requirements but also the specifics of its net capital computation and its definitions of custody or discretionary authority, which warrant more thorough research into that state’s laws and regulations.

Accordingly, new RIA owners who are researching their state’s net capital requirements may find it helpful to consider the following questions as a starting point as they consult their state’s website or handbook for investment advisor rules and regulations:

- Does my state have a minimum net capital requirement?

- How does my state define ‘net capital’ (or net worth), as well as the assets and liabilities that are used to compute net capital?

- Does my state have different requirements if an RIA has custody or discretionary authority, both, or neither?

- If so, how does my state define ‘custody’ and ‘discretionary authority’ for purposes of their minimum net capital requirements?

Choosing Assets To Include In Net Capital Computation

When computing their net capital, RIAs structured as a partnership or corporation (in which business assets are clearly separate from the owners’ personal assets) are restricted to including only business assets in the calculation. However, the rules are less clear for owners of solo advisory firms structured as sole proprietorships or single-member LLCs, which for tax purposes are treated as ‘disregarded entities’ indistinct from their owner.

In theory, then, a solo firm owner could include their personal assets in the net capital computation if, for instance, they didn’t want to tie up additional assets in the business. However, only personal assets that are not excluded by state regulations can be counted; thus, home equity still generally would not count toward an advisor’s net capital even as a sole proprietor, because it is typically an excluded asset type.

Thus, in practice, it makes more sense for sole proprietors and single-member LLCs to count only their business assets towards net capital. Because the funds held aside as net capital would be (by definition) subject to the legal claims of clients, keeping them within the business can help to avoid putting the owner’s personal assets at risk (and for single-member LLC owners, intermingling business and personal assets risks voiding the liability protection of the LLC, thereby subjecting all of the owner’s personal assets to clients’ claims).

It’s also notable that, while most states’ regulations require net capital to include only cash or other “marketable” assets (and most RIA firms do, in fact, hold the required amount in the form of cash in a bank account), they do not specifically require it to be held in cash. Theoretically, then, it is possible to hold stocks, bonds, or funds to satisfy the net capital requirements without committing the full amount to cash. However, this strategy runs the risk of market fluctuations dropping the RIA’s net capital below the required amount (which usually triggers a requirement to report the deficiency to state regulatory authorities).

Furthermore, holding investments as net capital adds complexity to the firm’s compliance procedures (because of the need to avoid ‘front-running’ of trades in client accounts) and tax situation (because of the investments’ potential for generating taxable income). Therefore, RIA owners considering holding net capital in the form of investments need to weigh the potential benefits versus the risks and added complexity that this strategy would present.

Another challenge that minimum net capital requirements may pose for startup RIA owners is that they literally require capital, which, when added to other startup costs, can create significant financial burdens for new firms. Consider that many states require a minimum of $10,000 of net capital for RIAs with discretionary trading authority. On top of the other startup costs for an advisory firm – website design and hosting, software, office space (or home office equipment), and compliance consulting to help the RIA meet all of the other state registration requirements, plus the owner’s own personal expenses prior to earning any revenue – keeping an additional $10,000 set aside at all times to meet the net capital requirements could be prohibitive, especially for startup firms founded with only the owner’s personal savings and with no initial source of revenue.

Fortunately, many (though not all) states have alternative ways for RIAs to meet their minimum financial requirements without actually holding aside the full amount of net capital in cash or marketable securities. In those states, RIAs are allowed (and in some cases, required) to post a surety bond – essentially a third-party guarantee for the payment of a legal claim – in lieu of some (or all) of the required net capital, reducing the level of assets required to be set aside by the firm, and potentially freeing up funds for use in other parts of the business.

Surety bonds do require an upfront cost, which depends on the creditworthiness of the RIA owner and typically starts at 1% (or $100 per $10,000) of coverage per year. The cost of posting a surety bond might be much more practical for startup RIA owners compared to the alternative of raising $10,000 or more in capital to maintain a minimum net capital requirement.

For RIA owners considering a surety bond as a potential way to reduce their net capital requirements (or who are required by state regulations to do so), it’s important to understand the mechanics, costs, and risks of surety bonds in general, as well as the specific bonding rules for the state(s) in which the RIA operates.

The Mechanics Of Surety Bonds And State RIA Bonding Requirements

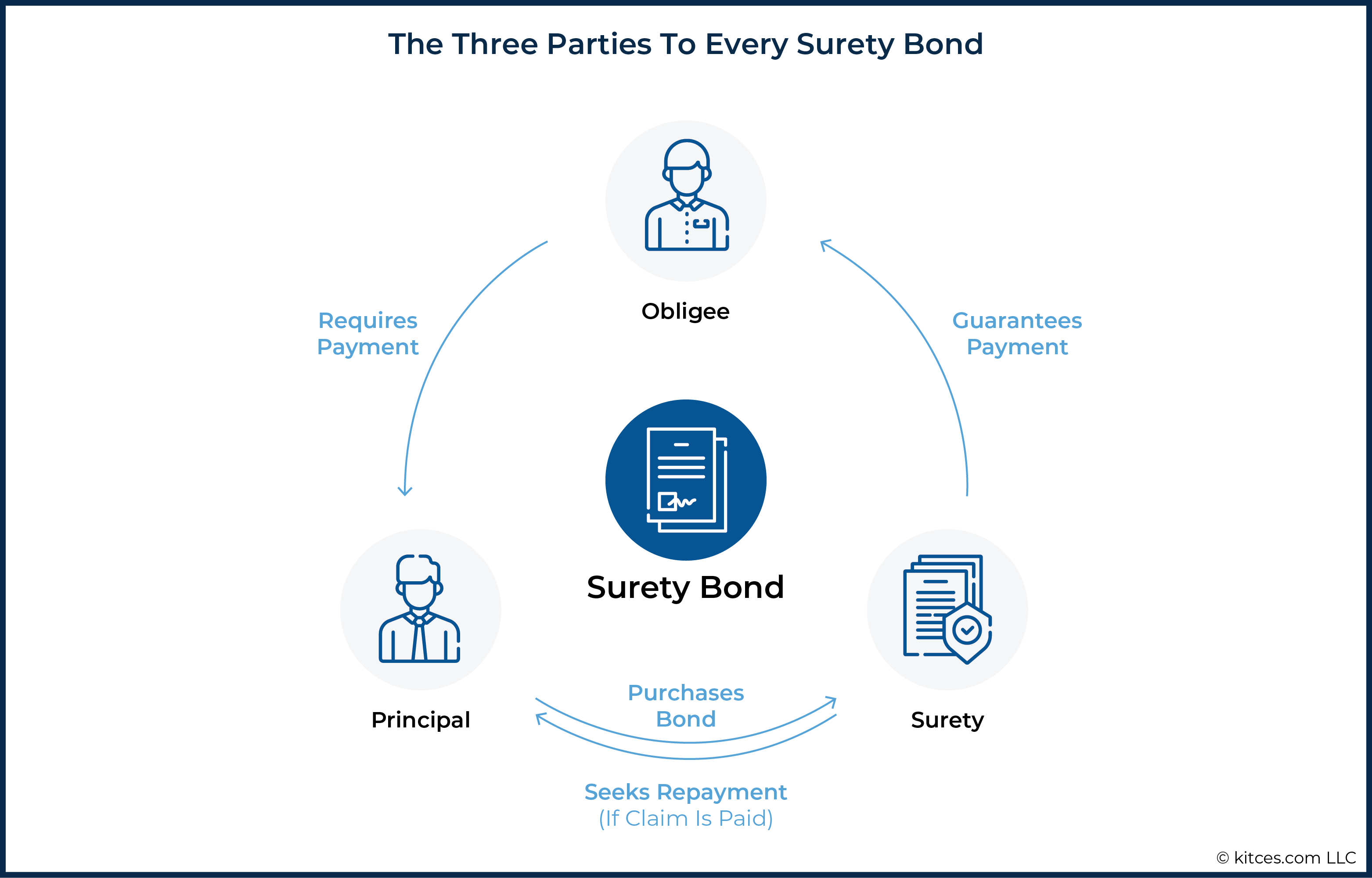

Surety bonds are used in many fields as a way for one entity to provide a guarantee to another that they will receive something that they are owed. Though called a “bond”, surety bonds bear little resemblance to the debt instrument that most advisors are familiar with.

As opposed to a government or corporate bond (which is technically an agreement between two parties – one that loans money and the other that borrows it and pays it back), a surety bond, as shown below, is agreed to by three parties: 1) the Principal (the entity that is required to make a payment of some kind), 2) the Obligee (the entity that is requiring the payment), and 3) the Surety (the entity that will make the payment if the principal is unable to). In the event the Surety must make a payment on the Principal’s behalf, they are allowed to take legal action to recover their funds from the Principal.

One common example of a surety bond in criminal law is a bail bond. Defendants in criminal cases are often required to post cash bail to the court in order to be released from jail. The cash is returned to them if they appear for their trial date, but if they fail to appear, it is forfeited. If the defendant (i.e., the Principal) lacks the funds to post bail themselves, they can pay a third party bail-bond provider (the Surety) a fee to guarantee the payment to the court (the Obligee) if the defendant fails to appear.

For RIAs, surety bonds follow the same basic structure: The RIA (the Principal) pays the bond provider (the Surety) a premium (usually amounting to 1% of the bond’s coverage per year), and if the RIA is unable to pay legal claims brought against it, the bond provider guarantees the payment. Importantly, when an RIA obtains a surety bond, the RIA’s owner generally must agree to indemnify (i.e., repay) the bond provider, pledging not only the RIA’s business assets but also the owner’s personal assets to reimburse the bond provider for any claims paid!

The state (the Obligee) holds the strings throughout the process, imposing bonding requirements on the RIA, dictating the provisions that the surety bonds must include (with many states writing the surety bond language themselves, providing a template for the RIA and the surety bond provider to sign and file), enforcing legal judgments against the RIA, and ensuring that the provider pays its claims as required.

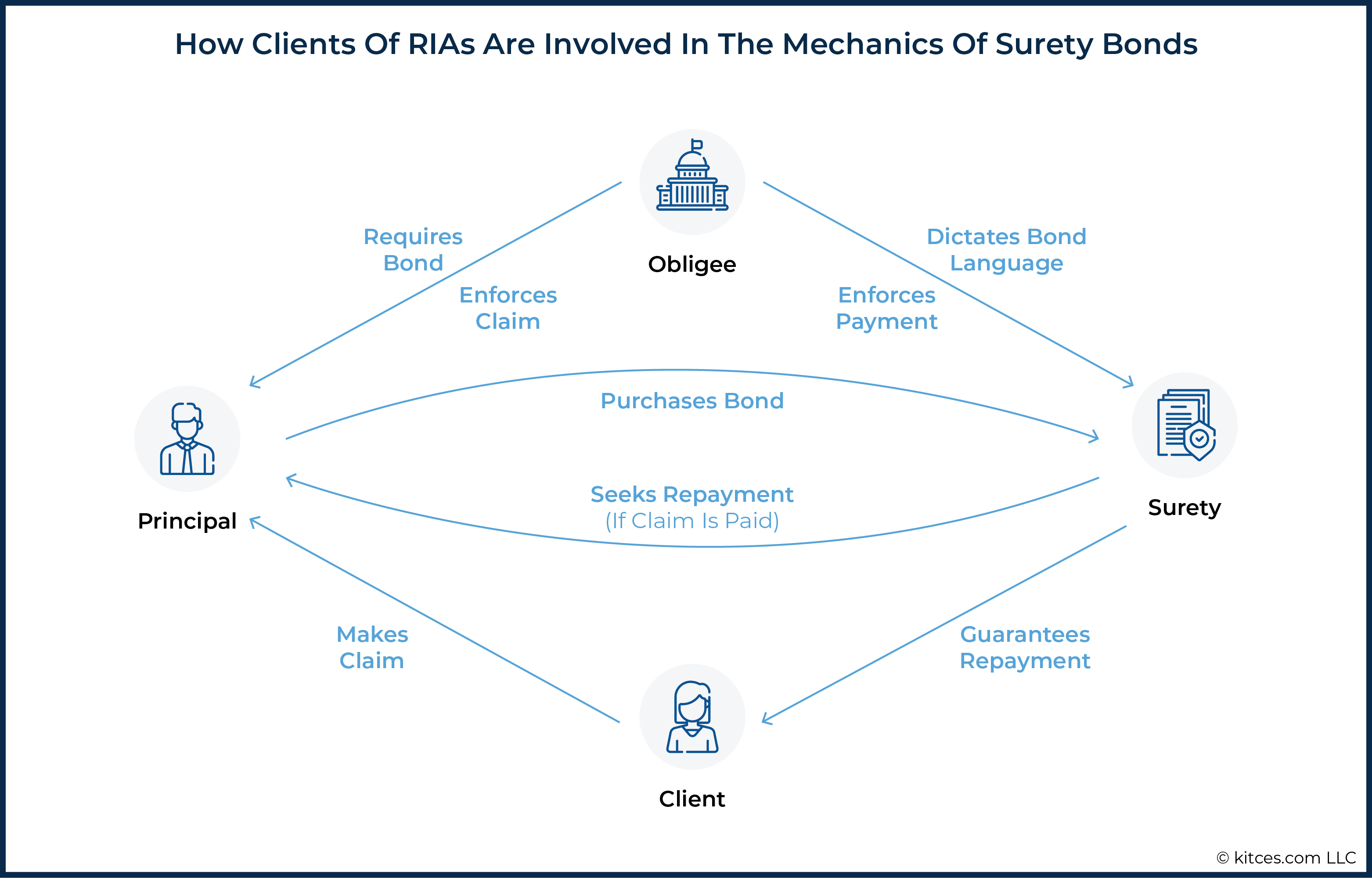

One notable difference between RIA surety bonds and other types of surety bonds (like bail bonds) is that there is a fourth party involved: the RIA’s clients, who despite not having signed onto the surety bond itself, are the ones whose interests it ultimately protects.

In this case, as shown below, the client is involved by initiating the legal claim against the RIA, and then by eventually receiving the funds paid out by the bond provider.

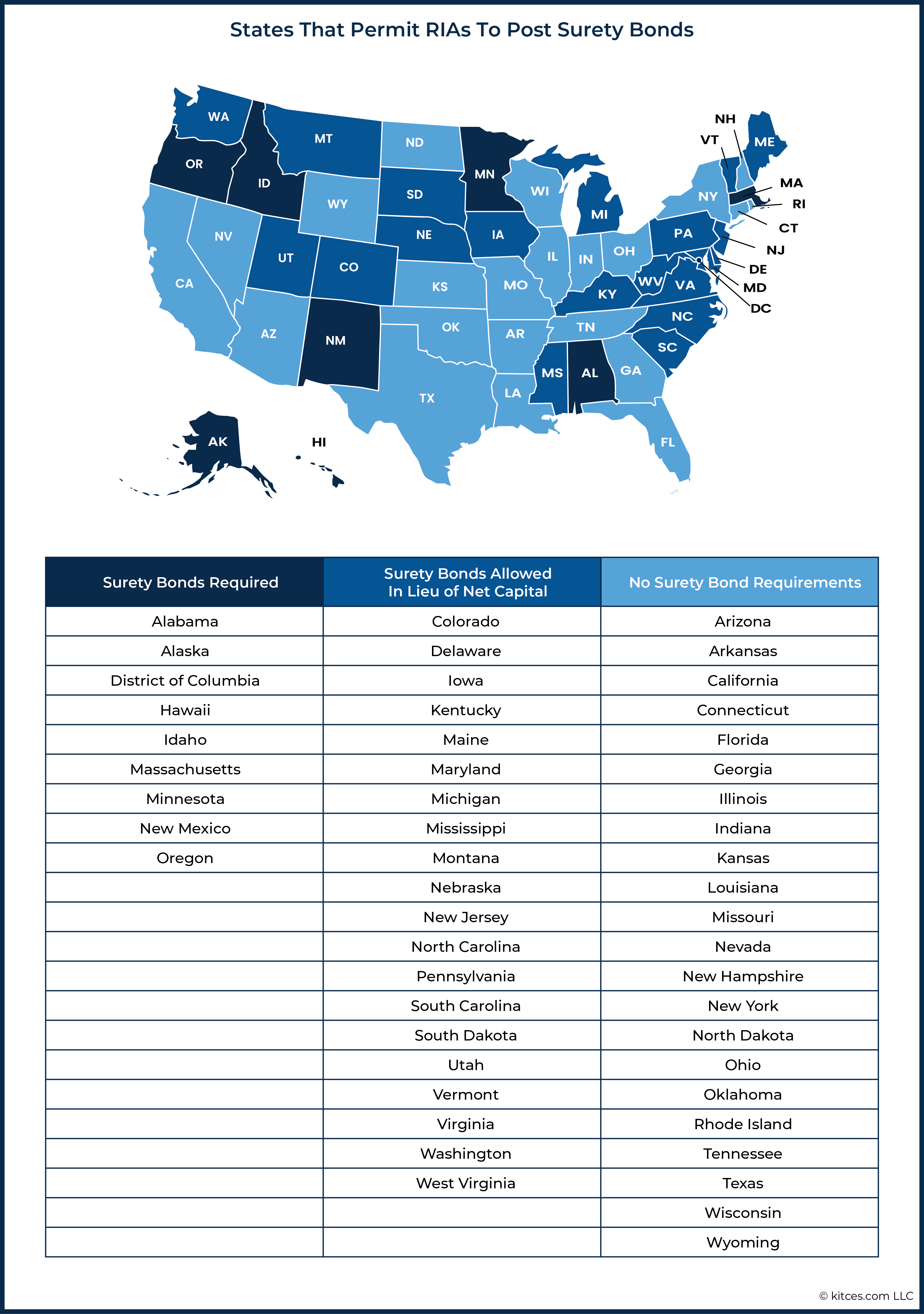

Surety Bond Requirements Can Vary Greatly Between States

Like net capital requirements, surety bond requirements also vary greatly from state to state, making it important for RIA owners to understand not only the mechanics of surety bonds in general, but also the particular rules of the state(s) where they are registered. Some states are more rigid in their regulations and require all RIAs to be bonded for a specific amount.

Example 3: Arthur owns a state-registered RIA based in Boise, Idaho.

Idaho requires all RIAs to file a $25,000 surety bond in order to register.

Therefore, Arthur must obtain a surety bond for that amount.

Other states allow RIAs to choose between maintaining a certain level of net capital or posting a surety bond, but require the bond to be in the entire equivalent amount of the net capital requirement.

Example 4: Marvin owns a state-registered RIA based in Lincoln, Nebraska.

Nebraska requires RIAs to maintain a minimum $25,000 in net capital or post a surety bond for $25,000.

Therefore, if Marvin does not want to hold aside $25,000 in net capital at all times, he will need to obtain a surety bond for the full $25,000. At standard rates, the bond would cost 1% x $25,000 (the bond’s coverage amount) = $250.

Most states, however, fall somewhere between the extremes of ‘Surety Bonds For All’ and ‘Surety Bonds For None’, allowing RIAs to partially lower their minimum net capital below the required amount, as long as they have enough surety bond coverage to make up the difference. Additionally, surety bonds are sometimes only required in certain circumstances (e.g., when an RIA has custody or discretionary authority), and often go hand in hand with the state’s minimum net capital requirements.

Example 5: Eddie owns a state-registered RIA based in Boulder, Colorado, that has discretionary authority over client accounts.

Colorado requires RIAs with discretionary authority to maintain a minimum $10,000 in net capital. Alternatively, if they do not meet the minimum net capital requirement, they must be bonded in the amount of the deficiency, rounded up to the nearest $5,000.

Therefore, since Eddie’s firm has only $7,500 in net capital, he has two choices:

- He may contribute at least $10,000 (net capital requirement) – $7,500 (current net capital available) = $2,500 of additional assets to the business to meet the minimum net capital requirement; or

- He may obtain a $5,000 surety bond to make up the $2,500 difference (as the bond must be rounded up to the nearest $5,000). At standard rates, the bond would cost 1% x $5,000 (the bond’s coverage amount) = $50.

Conversely, a handful of states (with New York and California being notable examples) have no bonding requirements at all, meaning that, without the state to act as obligee – one of the essential parties to the surety bond – RIAs would be unable to obtain a surety bond even if they wanted to (and meeting a net capital requirement would be their only option).

RIA owners, therefore, have another set of questions to answer about their state’s surety bond requirements:

- Does my state have surety bond requirements for RIAs?

- Who does my state require to have a surety bond: all RIAs, only those with custody or discretionary authority, or is it optional for everyone?

- How will my minimum net capital requirements be affected if I obtain a surety bond?

Nerd Note:

Though owners of RIAs that are registered in multiple states should be familiar with the minimum net capital and bonding requirements for all of the states in which they do business, usually the RIA is only subject to the requirements of its ‘home’ state – most states waive their requirements when an RIA’s ‘principal place of business’ is in another state, and the RIA is registered in that other state and follows its net capital and bonding requirements.

Surety Bonds Do Not Reduce Liability Risk For RIA Owners

On its surface, a surety bond might resemble an Errors & Omissions (E&O) insurance policy, a form of professional liability insurance also commonly used by RIAs, in that both involve a third party agreeing to pay a claim in the event of a judgement against the advisor… except that with a surety bond, even though the RIA owns the policy and pays the premium, the RIA would still be ultimately liable for any claims paid by the surety bond provider, as the RIA’s owner must also agree to be personally liable for any claims paid (to reimburse the surety bond provider after the fact).

In other words, unlike E&O coverage, obtaining a surety bond does not reduce the RIA’s liability risk, and for the RIA owner it may actually increase risk by pledging their personal (and not just business) assets to reimburse the bond provider. Which means that while an E&O policy can protect the RIA and its assets by paying clients’ legal claims on the RIA’s behalf (and in most cases will not seek repayment from the RIA on the claims it pays), the only parties that are actually protected by a surety bond are the RIA’s clients, who would ultimately receive any funds paid, with the RIA and its owner(s) then becoming liable to the surety provider.

The difference in coverage between E&O insurance and surety bonds is reflected in their respective costs: while E&O insurance premiums can cost $1,200–$1,500 for startup RIAs, and several thousand dollars or more for larger firms, surety bonds often cost only $100–$350 per year. However, E&O coverage typically provides at least $1 million in coverage and protects both the client and the advisor (by paying legal claims as well as lawyers’ fees and court costs), whereas a surety bond pays only the client and seeks reimbursement from the RIA.

For this reason, a surety bond should not be mistaken for a supplement to or substitute for E&O insurance, because it does nothing to protect the RIA itself. Instead, as with minimum net capital requirements, a surety bond is simply a way for the states that allow (or require) them to guarantee a minimum amount of restitution for clients harmed by negligent or fraudulent advice by ensuring that either the RIA or a bond provider will be able to make the payment.

Researching State Minimum Net Capital And Surety Bond Requirements

Fully understanding the specific minimum net capital and surety bond requirements that apply to an RIA often requires some research as, again, the requirements vary from one state to another. Usually, it is easiest to start with a basic Google search (e.g., “[state] RIA minimum net capital requirements”), which typically returns links to the state securities regulator’s website.

For some states, the regulator’s website itself will clearly describe that state’s minimum financial requirements for RIAs. For other states with less user-friendly websites, it might be necessary to do further research using the state’s laws, administrative codes, and/or regulations.

Although many states provide PDF versions of their administrative code books to download from their websites, the size and density of these documents can make research seem intimidating. However, the relevant information can often be found simply by searching the document’s text with key search terms, such as:

- “minimum financial requirements”

- “net capital”

- “surety bond”

When referring to state documentation, though, it’s very important to ensure that the requirements for RIAs are not confused with those of broker-dealers, which often have their own (typically much higher) separate net capital and bonding regulations!

Searching the internet for a state’s minimum financial requirements may return results for third-party websites, such as NASAA or compliance consultants like RIA In A Box, that aggregate information about state RIA requirements. While third-party sites can sometimes be a useful starting point for broadly understanding a state’s requirements, it’s always important to confirm the accuracy of the information provided against an official source, as they can be inaccurate, incomplete, or out-of-date.

In general, the most accurate information will be found on an official state regulator’s website, and RIA owners should rely on those sites whenever possible when researching net capital and surety bond requirements.

When RIAs Have A Choice: Deciding Whether To Maintain Net Capital Or Use A Surety Bond

By researching their state’s regulations, RIA owners can determine if they have any choice of whether or not to use a surety bond in lieu of their net capital requirement, and how much to be bonded for. In states that mandate a specific surety bond amount for all RIAs, firm owners have no other option than to obtain a bond for the required amount. But in states that do offer a choice, RIA owners can weigh the tradeoffs between holding aside the required net capital or obtaining a surety bond for some (or all) of the required amount.

For the firms that have a choice in the matter, the framework for this decision rests on three factors:

- The state’s specific net capital and bonding requirements;

- The assets the RIA has available to meet those requirements; and

- The tradeoff, or ‘opportunity cost’, of setting those assets aside as net capital compared to the cost of buying the surety bond and using the assets in other ways.

The first factor – the state’s specific net capital and bonding requirements – should be clear to the RIA owner after they have researched their state’s regulations and answered the questions outlined in the preceding sections. Specifically, the RIA owner will need to know how much they are required to maintain in net capital based on their firm’s circumstances (e.g., whether they have custody or discretionary authority over client assets), and whether they can obtain a surety bond to replace some (or all) of that net capital requirement.

The second factor in the decision – whether the RIA has the assets available to meet the minimum net capital requirement – is particularly relevant for many startup RIA owners, who may simply not have the additional funds available to meet their state’s requirements. This may be especially true during the RIA’s initial state registration process, when much of the firm’s capital (which often comes from the owner’s own personal savings) is tied up in the other costs of starting the firm. In these cases, there is really no alternative for the RIA other than to obtain a surety bond, which (assuming the state permits it) can allow the RIA to comply with the state’s minimum financial requirements without needing to raise additional funds – other than the comparatively minimal cost of the surety bond – to increase its net capital.

The Opportunity Cost Of Buying A Surety Bond Versus Holding Net Capital

The final factor in the decision is the tradeoff, or ‘opportunity cost’, between maintaining the minimum net capital amount versus obtaining a surety bond. Because when an RIA holds assets aside for the purposes of maintaining its net capital, it cannot use those assets for other purposes (e.g., to invest in other areas of the business, or to distribute them to the owner as profit).

However, obtaining a surety bond also has a cost, in the form of the ‘premium’ that the RIA pays for it. So the RIA owner must ultimately decide whether the benefits of being able to use the firm’s capital as they see fit are worth the cost of the surety bond.

In other words, if the RIA owner decides to buy a surety bond and invest the net capital that they would otherwise have needed to hold aside, the return on that investment needs to be greater than the cost of the surety bond in order to be financially worthwhile. Surety bonds vary in cost based on the provider, the RIA’s location, and the creditworthiness of the RIA and its owner, but a typical annual rate is $100 per $10,000 of coverage (or 1% of the surety bond’s face value). Therefore, however the RIA chooses to invest its additional capital after obtaining the bond, the minimum return it would need to realize on its investment would be 1%.

If the RIA were able to invest 100% of its available net capital, it is reasonable to assume it would be able to realize a return higher than 1%, making it worthwhile to obtain a surety bond rather than to hold aside net capital; however, a firm that invested 100% of its capital would then have nothing remaining to pay the overhead costs needed to run the business.

In reality, a firm already needs to set aside at least a portion of its capital for operating expenses. The only assets that are really available to invest are those in excess of this ‘operating cushion’. The breakeven point related to the opportunity cost of purchasing a surety bond can be identified by calculating the rate of return that the invested assets must realize in order to be worth the cost of purchasing the surety bond, as follows:

If the expected rate of return on the amount that can be invested if a surety bond were to be purchased is greater than this breakeven point rate of return, then purchasing the bond (and investing the available net capital) would potentially make more sense for the RIA. Thus, for RIAs with lower minimum net capital requirements, obtaining a surety bond has a higher opportunity cost because less capital can be freed up by doing so. And the less capital that is freed up, the closer the decision gets to being a toss-up, or even in favor of not obtaining a surety bond to begin with.

Example 6: Ford Financial Planning is an RIA in Ann Arbor, Michigan, with a minimum net capital requirement of $10,000.

Ford’s owner has determined that they need to set aside $9,000 at all times as a reasonable cushion to cover their operating expenses.

As an alternative to maintaining $10,000 in net capital, Firm E can buy a $10,000 surety bond for $100, allowing them to invest their excess capital elsewhere. But because they still need to set aside $9,000 for operating expenses, the amount ‘freed up’ by obtaining the surety bond is only $10,000 – $9,000 = $1,000.

Factoring in the cost of the surety bond, the return Firm E would need to realize on its investment to make the bond worthwhile is $100 ÷ ($10,000 – $9,000) = 10%.

Conversely, for firms with higher minimum net capital requirements, the opportunity cost of the surety bond decreases because more capital can be freed up for investment that would otherwise have needed to be kept on the sidelines.

In other words, for RIAs with higher net capital requirements, the lower opportunity cost means it is often preferable to obtain a surety bond and re-invest their available net capital in other ways; while for those with lower requirements, the higher opportunity cost means the RIA must invest their excess capital more effectively to be worth the price of the bond.

Example 7: Trillian Wealth is an RIA in Ames, Iowa, which has the same $9,000 operating cushion as Ford Financial Planning, but a higher minimum net capital requirement of $35,000.

Trillian’s owner can buy a $35,000 surety bond for $350, allowing her to invest the excess capital. Subtracting the operating cushion, this would ‘free up’ $35,000 - $9,000 = $26,000 to invest.

Again, factoring in the cost of the bond, the return Firm F would need to realize is $350/($35,000 – $9,000) = 1.3%.

As the examples above show, what really matters when figuring the opportunity cost of obtaining a surety bond is how much net capital will actually be ‘freed up’ after subtracting the amount held aside for operating expenses. Because, if an RIA buys a surety bond to eliminate its net capital requirement, but then needs to hold most of that capital aside anyway just to cover its overhead costs, the capital that is invested will need to realize a higher return to exceed the cost of buying the surety bond.

Choosing A Surety Bond Provider

After deciding whether to buy a surety bond and how much coverage to carry (if state regulations even allow the RIA to decide how much coverage to purchase in the first place, as some states have mandatory surety bond coverage requirements), the most difficult part of buying a surety bond can be choosing a provider.

Because an internet search for surety bond providers can produce dozens of results, and there may not be time to review each one individually, it may not be easy to decide which is the ‘right’ one for a particular RIA. And while it’s true that any licensed surety bond provider could theoretically be used, it is helpful to have a framework for narrowing down the options.

The major factors for RIAs to consider when choosing a provider are:

- whether the provider is licensed in the state where the RIA is registered;

- the amount the provider charges for the bond; and

- the provider’s overall client service and experience.

Many major carriers of small business general liability and E&O insurance (such as The Hartford and Markel Insurance Company) also sell surety bonds, making them a natural place to start for firm owners who want all of their coverage through a single company. There are also many internet-based companies that exclusively sell surety bonds, such as SuretyBonds.com and Surety Bonds Direct. The key is to pick a trustworthy provider, which can be assessed through third-party review sites like Google Reviews and TrustPilot, and by checking the provider’s Better Business Bureau page for complaints.

Though meeting a minimum net capital or surety bond requirement can be challenging for early-stage-startup-advisory-firm owners, it’s worth remembering how comparatively small the requirements are compared to the amount of client assets under management at many advisory firms. A $10,000 net capital requirement represents 1% of client assets for a firm with $1 million AUM, 0.1% at $10 million AUM, and 0.01% at the $100 million threshold where RIAs must register with the SEC.

Regulations are often crafted to protect the ‘average’ consumer, to whom the loss of a few thousand dollars can have a far greater impact than the ‘affluent’ consumer; but in reality, the consequences of an advisor giving bad advice can be many times greater than the amount of minimum net capital or surety bonding set by the state. E&O insurance, which typically carries much higher coverage limits, is a more effective way to protect the RIA’s clients (and its assets) and to show that the firm takes seriously its obligation to give good advice and be accountable for its advisors’ actions.

For RIA firm owners – particularly those in the startup phase – state registration is a complicated process requiring time-consuming decision-making and paperwork. It can be worth the extra time, however, to consider minimum net capital and surety bond requirements at a deeper level, especially for owners who have a choice between the two, because the decision can ultimately help the owner decide on the best use of their capital and how to truly protect the assets of not just the firm, but also its clients!

Because ultimately, an advisor’s value is created in what it does above and beyond the minimum requirements – certainly when it comes to the advice itself, but also in how it manages risk, makes financial decisions, and complies with regulations that protect the interests of its clients.

Many years ago I ran into trouble with these rules in Washington State after buying out a retiring partner because the loan counted against our net worth but the business value did not. Took a few try’s to find an insurance company willing to issue a large enough bond while at the same time pleading for time/mercy from State regulators to fix the issue.

Wow, that’s an interesting succession planning issue. If the loan is in the business’s name it could bring the business’s tangible net capital below the state’s minimum or even below 0, so the surety bond might need to be more than just $10k or whatever the state’s minimum net capital is. I can imagine it’s easy to miss with all the other mechanics of buying out a partner, but it seems like it would be a good idea to get the surety bond in place before the loan is funded to avoid a flap with regulators.

Interesting analysis would be for the states that require a surety bond and increase the cost of starting a RIA, whether the additional cost paid by the RIA has made the consumers of that state better off compared to states that have less stringent regulations. It clearly creates more work for state regulators as it is a line item for audit. Wouldn’t a better approach require E&O from onset and require increased coverage in E&O as AUM increases or the number of clients/complexities increases.

Locating a CDC inmate near me has always felt like a daunting task, but after reading this post, I understand the process much better. Thanks for the useful tips!