Executive Summary

Celebrating its 10th year as an event, this year’s Technology Tools for Today (T3) advisor technology conference was the biggest ever, punctuated by a stream of major product launch announcements at the conference itself, and buzzing about the literally billions of dollars of merger and acquisition activity for advisor technology firms in the two weeks leading up to the conference.

The breakout categories at this year’s event included several new “Personal Financial Management” (PFM) tools for advisors to work collaboratively with their clients, including the launch of EMX Select from eMoney Advisor (which, finally, will be “unbundled” from their financial planning software!) and a new solution called “Narrator” from Advicent (maker of NaviPlan and Financial Profiles). Also highly visible at this year’s T3 conference were an onslaught of more than half a dozen new “robo-advisor-for-advisors” solutions, all seeking to bring a better technology platform for advisors to build their businesses and automate much of the onboarding and investment implementation with their clients.

Yet underlying the potential efficiency of all these new technology solutions is the ongoing challenge that for many advisors, working with smaller clients isn’t actually a matter of efficiency (which technology can solve), but a marketing problem to get a sufficient volume of those clients in the first place. And while several new technology solutions are aiming to automate more of the advisor marketing process, along with making advisor websites more engaging with a series of “self-help” tools that can get prospective clients interested in actually working with an advisor, the question remains: how many advisory firms have a good enough marketing process to actually leverage these tools in the first place?

Highlights of the T3 Technology Conference – The Rise Of Advisor FinTech

Earlier this month, over 600 people gathered at the Hilton Anatole in Dallas for the Technology Tools for Today (T3) advisor technology conference. Now celebrating its 10th year, the T3 conference itself has become the center of the world of “Advisor FinTech” – the ongoing rise of financial technology solutions specifically for advisors. Although notably, attendance remains driven heavily by the vendors themselves, who view T3 as an opportunity to form strategic alliances and partnerships, and “be seen” by the industry media and commentators; while there were a material number of advisor attendees shopping for solutions – as T3 is by far the best conference for advisors looking for technology solutions – advisor attendance was somewhat lackluster (as it has always been).

Source: Yours truly, who clearly needs a cell phone with a better camera!

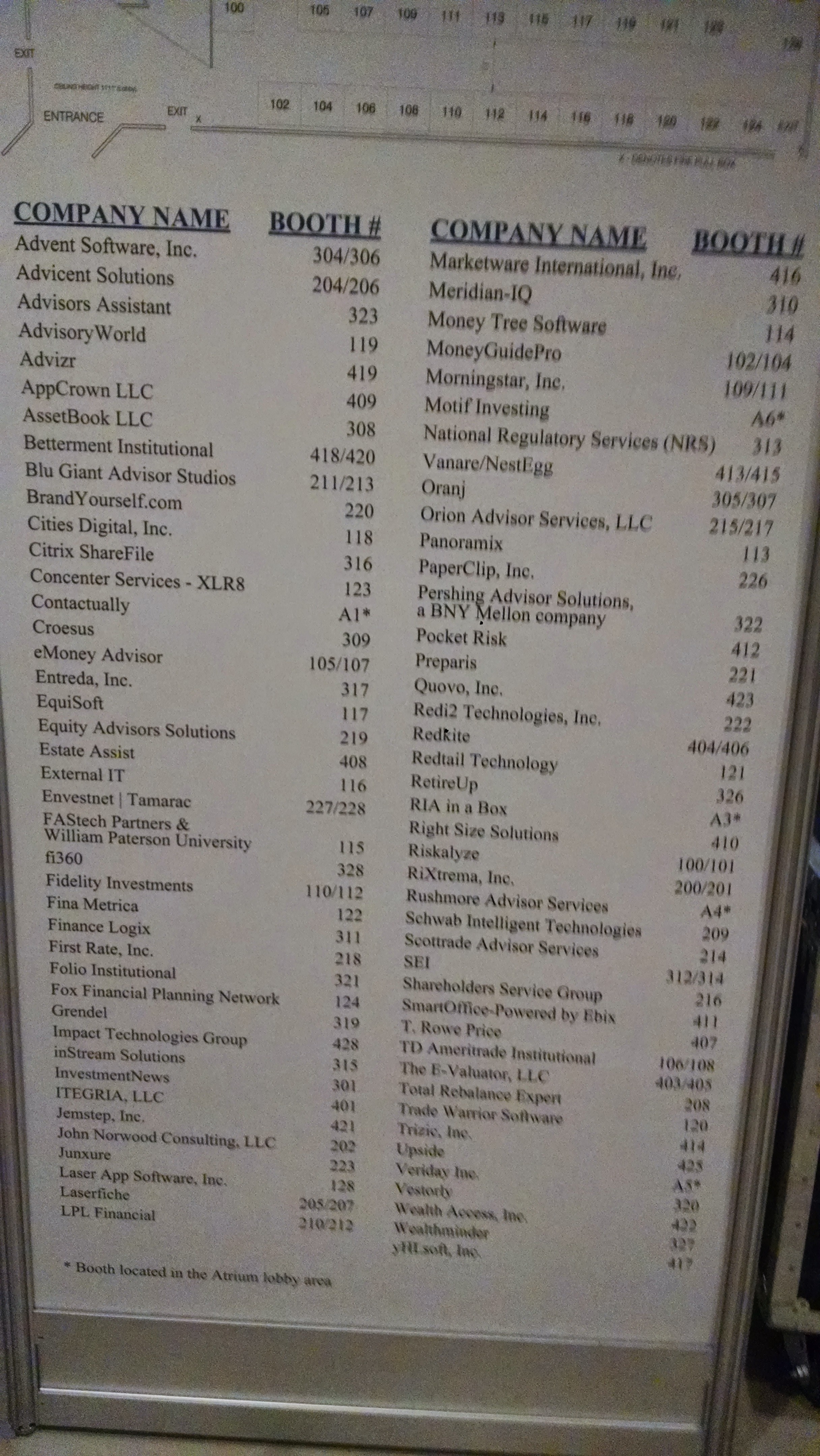

Nonetheless, in terms of advisor technology vendors themselves, this year’s exhibit hall seemed to be the largest ever – so packed that it was necessary to create an “overflow” space for additional vendors! – and also featured what was easily the widest breadth of solutions ever. In the past, technology solutions for advisors have seemed concentrated primarily around investments and asset management, with a breakdown that might have been 70% investment-related, 10% CRM, 10% financial planning software, and 10% “other”. This year, while there was still a heavy concentration of portfolio analytics and reporting tools, there was a much wider range of solutions, including multiple risk profiling and analysis tools (from the longstanding FinaMetrica, to newer providers Riskalyze and RiXtrema, and the latest newcomer Pocket Risk), to a new technology-driven compliance solution from RIA In A Box, to a new client billing solution from BillFin, a new form of digital estate planning solution aptly called Estate Assist to help clients transition their digital (and physical) assets in the event of death of disability, and entire “IT outsourcing” solutions for advisors like External IT, Entreda, ITegria, and RightSize Solutions. (Though ironically, despite the high volume of Twitter buzz on the #T32015 hashtag, there was not a single social media compliance solution exhibiting at the conference!)

Showcasing its role in the world of Advisor FinTech, the T3 conference also featured a number of big announcements, including a wide range of new product launches that happened in the days leading up to the conference or were featured at the event itself. Though overshadowing all of these product announcements were the stream of mega acquisitions that occurred in the two weeks leading up to T3, including SS&C’s acquisition of Advent for $2.7B, Fidelity’s purchase of eMoney Advisor for what was rumored to be more than $250M, and the TA Associates purchase of Northstar (including the popular Orion Advisor Services) for an unknown amount that is rumored to be in the “hundreds of millions” range.

In an environment where so much attention has been focused on the direct-to-consumer “robo-advisors” and the hundreds of millions of venture capital that have been invested into them, it was notable to see what was literally “billions” of dollars of private equity and mergers now flowing into the world of advisor technology. Suddenly, the fact that an advisor-facing tech company (or several!) can have such a large “exit” – and that private equity funds, who care most about cash flow, profits, and sustainable margins, see such value in putting their money towards technology solutions for advisors – raises the question of whether the “smart money” is betting on robo-advisors to compete against advisors, or investing into technology for advisors instead. With literally 10X the amount of money buying technology companies for advisors as is flowing into robo-advisor startups competing against them, the landscape appears to be shifting rapidly, leading to an almost palpable air of opportunity at T3.

PFM Portals and Dashboards – EMX Select and Advicent Narrator

Of the announcements at the conference that generated the most buzz, #1 was the presentation by eMoney Advisor CEO Edmond Walters announcing the release of EMX Select, an update to eMoney’s popular Personal Financial Management (PFM) client portal that will feature deeper integrations with advisor technology partners, including bi-directional data flows and single sign-on. Given the vendor integrations, it appears that EMX Select is envisioned to be both a client PFM portal, and a functional dashboard for advisors to manage their own practice.

Perhaps most notable about the launch of EMX Select, though, was Walters’ indication that EMX Select will be available separate from the eMoney Advisor financial planning software. In other words, eMoney will be unbundling its financial planning software from its PFM, and appears to be investing more heavily than ever into its PFM solution. Walters also noted that a material reason for his decision to be acquired by Fidelity was their resources to support deeper integrations and their capabilities around data management to help grow EMX Select, further supporting the idea that the Fidelity acquisition was more about PFM than financial planning software. After years of lamenting the lack of PFM tools for advisors, EMX Select may quickly become the dominating market leader in this wide-open space. And the implications for allowing advisors to become significantly more efficient and proactive in their planning process, as “financial plan updates” become irrelevant as plans are continuously updated and monitored, is significant.

Continuing the client PFM and advisor dashboard theme, Advicent Solutions (maker of financial planning software NaviPlan and Financial Profiles) debuted its new portal/dashboard offering as well. New CEO Phil Cunningham, focusing on the theme of advisors seeking ways to make themselves unique amidst the ongoing “crisis of differentiation”, announced the launch of their new offering “Narrator”, which will provide a series of FinanceLogix-style widgets (apparently pulling from financial planning software, PFM, personal finance tools/calculators, and more) that advisors (or their firms) can customize to create a dashboard of relevant information for the advisor and a unique experience for the client. Although largely targeted for enterprises right now (e.g., broker-dealers and other large firms) that would deploy the platform for dozens or hundreds or thousands of advisors, Narrator is ultimately expected to be available to independent advisors as well.

Following on last month’s announcement by MoneyGuidePro that it would be deepening its PFM offering by partnering with Yodlee (and at the conference, MGP noted it would be “PFM neutral” and would be integrating with EMX Select as well!), and the presence at T3 of new PFM solutions like Wealth Access as well, the long overdue space for advisor PFM tools is finally heating up!

Technology Platforms And The Rise Of Robo-Advisors-For-Advisors

Another notable trend of this year’s T3 conference, as predicted earlier this year, was the rapid ascent of the “robo-advisor for advisors”, with a veritable explosion of new solutions, including trend-setter (and “original” robo-advisor) Betterment Institutional (which in the days since announced a big $60 VC round in part to fuel its advisor growth), to other robo-advisor tools that started as direct-to-consumer and pivoted to advisors (including Jemstep, and Vanare/NestEgg), to solutions that launched directly for advisors from the start, like Upside Advisor and Oranj. Even existing players wanted to get in on the action, including a new joint venture called “AutoPilot” between CLS Investments and Riskalyze, and a new offering called BioniX from portfolio risk analytics provider RiXtrema.

Although the providers vary in their exact capabilities, this trend of “robo-advisors-for-advisors” generally means a set of technology tools for managing both the operations and implementation of investment management, including building/managing models (or outsourcing their creation altogether), trading and rebalancing, and also a strong online client onboarding experience (i.e., clients can complete all paperwork online/virtually) and a client portal/app/website for their use.

In point of fact, though, many of these tools and capabilities have already existed for advisors in some way or another. Rebalancing software has been around for a decade, as well as software tools to create and manage models. And while many custodians have lagged in creating a fully online onboarding experience for clients, the gap has already been closing in converting advisory firms from paper-based to paperless.

Nonetheless, the potential is that with these new tools, advisors may be able to better serve “smaller” clientele who simply could not be served profitably and effectively in the past. As these new integrated solutions for advisors become available, it becomes increasingly feasible for advisors to handle lower account minimums at a lower price point through what largely becomes a “self-service” option, supplemented by additional advisor value-adds as the client AUM and net worth grows.

Accordingly, it seems that the phenomenon of robo-advisors-for-advisors might be better dubbed “Platform 2.0”, a series of new-and-improved technology tools that build upon the existing technology, but go beyond through a combination of a superior advisor/client user experience, visual appeal, ease of use, and operational efficiency, to expand the base of clientele that advisors can serve. While the concept of the tools is not new, their 2.0 execution often puts the existing 1.0 legacy players to shame.

And notably, the trend highlights what this blog has long noted as the true threat of robo-advisors – a potential to disrupt and disintermediate existing advisor custodian and technology platforms as advisors shift from the “old” solutions to the new!

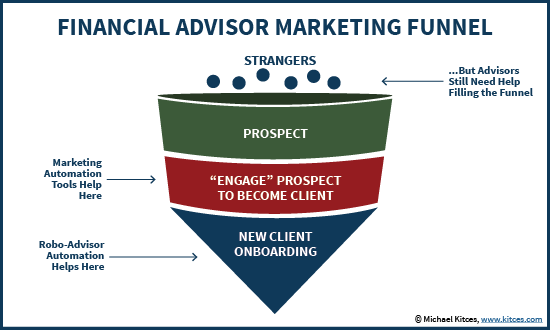

Marketing Engagement Tools And The Problem With Robo-Advisors For Advisors

While the explosion of robo-advisor Platform tools for advisors is notable – especially as many of these companies are pivoting from their lackluster results in the direct-to-consumer market to a potentially-more-lucrative advisor marketplace – their shift may indirectly highlight another key advisor issue: for most advisors, the problem is not actually the ability to manage and implement “smaller” clients more capably through technology, but their ability to get those clients in the first place.

In point of fact, this challenge isn’t actually unique to advisors. One of the great “revelations” that most direct-to-consumer robo-advisors have had to learn “the hard way” is that in a low trust industry like financial services, it’s not enough to have a low cost solution and some visually appealing technology. Consumers need time to establish a relationship with and trust a brand, which means the blocking point for most firms serving the masses is not actually the cost to service smaller clients, but the cost to acquire them (or at least, to acquire them in bulk volume), and it’s the high cost of client acquisition that leads most advisors to seek out higher net worth clientele.

In other words, financial services is not an “if you build it, they will come” industry, not when it’s robo-advisors going directly to consumers, nor when it’s (human) advisors using a robo-advisor platform to do the same. Most advisors don’t have a high volume of prospective clientele coming to their websites, where their key problem is figuring out how to accept and onboard those clients in an efficient purely digital manner (with “robo” tools).

In fact, while Upside Advisor made a splash late last year about supporting noted industry bloggers Barry Ritholtz and Josh Brown in their “robo” offering Liftoff, the reality is that Ritholtz and Brown may have actually been the best advisor clients Upside Advisor is ever going to see, with an actual high volume of website visitors that likely numbers several hundred thousand unique visitors per month. And even then, Brown recently noted that so far Liftoff is “just” seeing asset flows of $1M total after several months. While those asset flows certainly aren’t “bad” by most advisors’ standards, for the typical advisor, whose website might literally not even have 1/100th that traffic (and would be lucky to convert at the same rate), implementing robo-advisor solutions may amount to a trivial amount of revenue growth. Sure, many advisors can use these robo-solutions to handle the situation of “my client referred me a family member who’s below my minimums, but I don’t want to turn them away”, but in reality that doesn’t happen in most advisory firms with enough frequency to really add up to a material amount of new business and revenue, either.

Notably, the T3 conference did feature a number of “advisor marketing” solutions to help facilitate the process of gaining new clients, including content marketing platforms like Vestorly, the do-it-yourself initial risk analysis tool from Riskalyze, to self-guided financial planning solutions that encourage prospective clients to go deeper with a “real” advisor like the new MyMoneyGuide (from MoneyGuidePro) and newcomer WealthMinder. The common theme of these tools is that they help to engage a prospective client over time, largely through automation or “self-service” tools, until those prospects reach the point that they are interested in engaging with a human advisor for deeper services.

Yet the challenge that even these marketing engagement tools miss is that for most advisors, the problem is a lack of new prospective clients (or new “strangers” who can become prospective clients) to feed into this “marketing funnel” in the first place. In other words, automated engagement tools may help turn a stranger into a prospect and eventually move a prospect forward towards becoming a client (the “middle” of the marketing funnel), and robo-advisor-for-advisors tools may take someone who is ready to move from prospect to client and automate their onboarding process (the “bottom” of the marketing funnel). But these efficiencies at the middle and bottom of the marketing funnel still don’t answer the fundamental issue: for most advisors, there aren’t enough new strangers coming into the top of the funnel to become prospective clients in the first place!

Which means ultimately, it’s not really clear how any of the marketing engagement and robo-advisor-for-advisors tools will really work for advisors, until advisory firms figure out how to solve their marketing challenges. As it stands in today’s environment, larger advisory firms are reinvesting into marketing to solve this challenge, but most advisory firms are “stuck small” as they lack the capital to do so. In turn, while there remains a potential opportunity for a technology solution that actually helps the top-of-funnel problem – e.g., an advisor review site, or an advisor-prospect matching service – thus far, few have had much traction. The advisor review sites are doomed because of the low volume of clients that most advisors have, and the advisor matching services struggle both because it’s actually hard to “match” advisors to prospective clients when so many advisors are generalists who all do the same thing and describe their services the same way, and because even “lead generation” sites still struggle with the same high cost of client acquisition that has limited the ability of advisors to work with the middle market effectively anyway.

Nonetheless, while it remains to be seen exactly which solutions gain traction – and which advisors can actually leverage and utilize them effectively – this year’s biggest-ever T3 conference and the big acquisitions that preceded it are clearly accentuating that this may be the breakout year for Advisor FinTech. While some questioned whether the big acquisition deals mean there’s a “bubble” in Advisor FinTech, the fact that these were exits to private equity firms who see profit potential or larger players who see grow opportunities suggest that there may be plenty of room left for Advisor FinTech to grow from here. In fact, the potential for such big exits may actually inspire a new round of venture capital coming directly into the world of Advisor FinTech. Which means T3 in 2016 will definitely be an event not to be missed!

For a further round-up of articles about the T3 Advisor Technology conference, here’s some additional commentary from those who attended:

Fast Twitter Recap of T3 Dallas 2015 Conference by Craig Iskowitz

The T3 Conference: Musings on Acquisitions, Integrations, Robo-advisors, and More by Raef Lee

In A T3 Teeming With Deals, eMoney's Edmond Walters Owned Dallas by Tim Welsh

Key Insights From Day 1 of T3 Technology Conference by Steve Sanduski

Quick Recap of Day 2 at T3 Technology Conference by Steve Sanduski

As RIA Tech Grows, So Does T3 by Tim Welsh

4 Cool Tech Tools Launched at T3 by Joyce Hanson

Five Things I Took Away From T3 Conference by Marshall Smith