Executive Summary

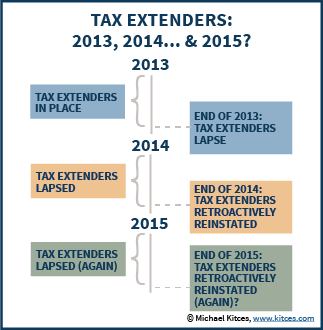

Late last night, the Senate passed H.R. 5771, known as the Tax Increase Prevention Act of 2014 or more simply as the “Tax Extenders” legislation. Having already passed the House of Representatives two weeks ago, the legislation will soon go before President Obama and should be signed into law within the next few days.

In its final form, the legislation “patches” the tax extenders for one year, retroactively reinstating a wide range of provisions that technically lapsed at the end of 2013, to now be available for the current 2014 tax year. This includes the popular rule allowed those over age 70 ½ to make a qualified charitable distribution (QCD) from an IRA, satisfying the current year’s required minimum distributions while simultaneously completing a charitable bequest and excluding the IRA distribution from income entirely for tax purposes, with just enough time left to complete a QCD before year end. However, as a temporary extension, we will find ourselves in the same boat - lapsed tax extenders, waiting for a retroactive reinstatement - again in 2015!

Notably, though, the Tax Increase Prevention Act legislation also included the Achieving A Better Life Experience Act of 2014 (also known as the ABLE Act of 2014), which will create a new Section 529-ABLE account to be used not for educational purposes but to allow for tax-free growth for a special needs beneficiary (without disqualifying the beneficiary from most Federal or state aid programs). And while the tax extenders section of the legislation is temporary – adding just one year to the life of the tax extenders – the new ABLE Act provisions as permanent, and will change the landscape of using special needs trusts and planning for special needs beneficiaries for many years to come.

Key Tax Extensions Under H.R. 5771 – The Tax Increase Prevention Act of 2014

In its final form, H.R. 5771 – also known as the Tax Increase Prevention Act of 2014 – alters and extends the expiration dates for a wide range of individual tax planning provisions that had previously expired at the end of 2013. Under the legislation, which is projected by the Joint Committee on Taxation to reduce revenue to the Federal government by approximately $42B over the next 10 years, the following provisions will now expire as of December 31st of 2014, reinstating them (retroactively) to be effective for the current 2014 tax year:

In its final form, H.R. 5771 – also known as the Tax Increase Prevention Act of 2014 – alters and extends the expiration dates for a wide range of individual tax planning provisions that had previously expired at the end of 2013. Under the legislation, which is projected by the Joint Committee on Taxation to reduce revenue to the Federal government by approximately $42B over the next 10 years, the following provisions will now expire as of December 31st of 2014, reinstating them (retroactively) to be effective for the current 2014 tax year:

- $250 schoolteacher deduction for unreimbursed expenses paid by eligible educators for books, supplies, computer and other equipment, and supplementary materials used in the classroom.

- Exclusion from gross income of discharged qualified principal residence indebtedness. Under normal tax law (IRC Section 108), the cancellation of certain indebtedness is treated as income for tax purposes (as though you received money as income to pay off the debt), and this could include debt cancelled in the short sale of real estate (where a $250,000 property is used to pay off a $300,000 mortgage, the $50,000 of debt cancelled in this underwater mortgage situation could be treated as cancellation-of-indebtedness income). With this provision extended, any short sales to resolve underwater mortgages this year can potentially avoid being treated as taxable income.

- Maximum for qualified transportation fringe benefits (e.g., transit passes and vanpooling) is excludable up to $250/month (up from $130/month without the extension), keeping it at parity with qualified parking benefits (also at $250/month).

- Deductibility of mortgage insurance premiums as (qualified residence) mortgage interest, for those who have been paying private mortgage insurance (PMI) on a mortgage issued since 2007, and who meet certain income requirements.

- Deduction for state and local sales taxes (to the extent it exceeds State and local income taxes), which is primarily useful for those who live in states like Florida, Texas, Nevada, Alaska, South Dakota, Washington, and Wyoming, which all have no state income taxes (and thus where state sales taxes are the primary deduction).

- Special rule for certain contributions of real estate for conservation purposes, which provides a significant increase in charitable tax deduction benefits for family farmers and ranchers who donate a conservative easement on their land.

- Above-the-line education deduction for qualified tuition and related expenses, although in practice the up-to-$4,000 deduction is not commonly used as most eligible taxpayers will claim the American Opportunity Tax Credit instead.

- Tax-free qualified charitable distributions that are paid directly from an IRA to a charity, for those already over age 70 ½ and up to the annual $100,000 (per taxpayer) limit.

In addition to this relatively limited list of individual tax extender provisions (and this is all the individual tax extender provisions!), the Tax Increase Prevention Act does include a wide range of business tax extenders, including the work opportunity tax credit for businesses hiring certain targeted groups of workers (including unemployed veterans, and those receiving TANF or SNAP), the 50% bonus depreciation rules, the $500,000 Section 179 expense deduction that phases out beyond $2,000,000 worth of property placed into service (up dramatically from the $25,000 and $200,000 limits, respectively, that would have applied with the current lapse), the IRC Section 1202 exclusion on gains of certain small business stock, and many many more. A wide range of extender provisions for various energy tax credits, deductions, and incentives were also included in the legislation.

Also of note in the legislation were a few permanent changes, including new inflation-indexing beginning in 2015 for a wide range of tax penalties (including the failure to file penalty, penalties imposed upon tax preparers, and failure to file business returns), and also an adjustment to Section 529 plans that allows investment allocations to be changed twice per year beginning in 2015, up from the current once-year-year rule (further discussed later in this article in the section regarding the ABLE Act of 2014).

Notably, because the legislation only retroactively reinstates the tax extenders for the current year, the rules all lapse again in just two weeks and in 2015, once again, taxpayers will be waiting to find out if the tax extenders will again be reinstated and extended. In addition, even with the retroactive fix for 2014, because many of these individual, business, and energy tax preferences are actually tax credits or deductions that would apply for dollar amounts already expended earlier this year, they will simply provide more favorable tax results for actions that were already taken. In only a relatively limited number of situations – such as qualified charitable distributions from IRAs – is there realistically enough time left in the year to actually be proactive in taking advantage of the tax extender legislation at all!

Year-End Planning With A Qualified Charitable Distribution (QCD) From An IRA

The rules for making a qualified charitable distribution (QCD) stipulate that a distribution paid from an IRA to a charity (i.e., the check from the IRA should be made payable directly to the charity) can be excluded from income as an IRA distribution. No charitable deduction can be claimed, but only because the exclusion of the IRA distribution is already effectively a “perfect” pre-tax contribution to charity.

To make a qualified charitable distribution, the IRA must be at least age 70 ½ (i.e., literally must actually be past the age of 70 years and 6 months on the date of the distribution), and the maximum QCD to a charity is $100,000 per year (per taxpayer, so a married couple can do a total of $200,000, as long as it is no more than $100,000 for each individual’s IRA, and each of them separately qualified). Any QCD paid to a charity can also satisfy the individual’s Required Minimum Distribution (RMD) obligation for his/her IRAs (but not other retirement accounts) for the current year.

With two weeks remaining in the year, there is still time for those who have not yet satisfied their 2014 RMD to make a QCD to a charity, resolving both their RMD obligation and their charitable intent. Even if the tax extender law has not yet been signed, as long as the IRA distribution is made directly to the charitable in a manner that is consistent with the law, the retroactive reinstatement of the tax extenders will make it a QCD. Similarly, it is notable that if someone already had made a direct distribution from an IRA to a charity – in anticipation of the rule being extended – it will now qualify, retroactively, as a QCD. However, if the individual’s RMD was already withdrawn for the year, there is no way to “undo” the RMD and now make a QCD instead; at best, the individual can simply donate to the charity (by cash or check), and claim a normal itemized deduction for charitable contributions that will mostly (though probably not fully) offset the taxable income from the prior IRA distribution.

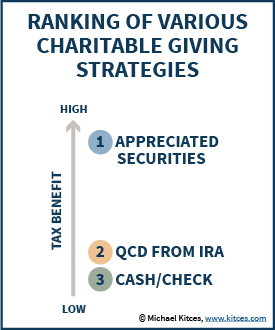

Notably, though, while making a qualified charitable distribution from an IRA to a charity is better tax treatment than donating cash or writing a check, for those who intend to make larger gifts, it is generally still far more advantageous to donate appreciated securities to a charity. The reason is that a QCD is still largely similar to taking an RMD and making a donation; in both cases, the end result is that the income that would have resulted from the IRA distribution is offset (mostly or perfectly) by the amount donated to charity. By contrast, when an RMD is taken and appreciated securities are separately donated instead, the donation from the appreciated securities (mostly) offsets the RMD, and the embedded capital gains on the appreciated securities are permanently eliminated. This “double tax benefit” of appreciated securities will generally trump qualified charitable distributions (and cash/check donations); the greater the appreciation in the underlying securities, the more beneficial it will be over a QCD.

Notably, though, while making a qualified charitable distribution from an IRA to a charity is better tax treatment than donating cash or writing a check, for those who intend to make larger gifts, it is generally still far more advantageous to donate appreciated securities to a charity. The reason is that a QCD is still largely similar to taking an RMD and making a donation; in both cases, the end result is that the income that would have resulted from the IRA distribution is offset (mostly or perfectly) by the amount donated to charity. By contrast, when an RMD is taken and appreciated securities are separately donated instead, the donation from the appreciated securities (mostly) offsets the RMD, and the embedded capital gains on the appreciated securities are permanently eliminated. This “double tax benefit” of appreciated securities will generally trump qualified charitable distributions (and cash/check donations); the greater the appreciation in the underlying securities, the more beneficial it will be over a QCD.

In addition, it is important to bear in mind that it's still better to take an RMD, pay taxes, and simply keep the rest, if there is no charitable intent in the first place; qualified charitable distributions from an IRA can be better if there was a plan to donate the money anyway, but should not be done in the absence of a charitable desire in the first place. Similarly, if the RMD was already taken and charitable giving was already completed for the year, there may be little sense to doing an additional QCD at this point (again, if there is not an actual charitable desire to do so).

On the other hand, given how late it is in the year – potentially already too late to facilitate a transfer of some types of appreciated securities by the end of December – completing a QCD at this point may be the best option available for those who do wish to make a donation, especially if the year’s RMDs have not yet been satisfied. Qualified charitable distributions can also be superior if donating appreciated securities will bump up against the annual charitable contribution limits, if the taxpayer isn’t itemizing deductions at all, or if the taxpayer is bumping up against the maximum for the phaseout of itemized deductions.

ABLE Act Of 2014 And 529-ABLE Plans For Special Needs Beneficiaries

Included as a part of the Tax Increase Prevention Act of 2014 is also the Achieving A Better Life Experience (ABLE) Act of 2014, and while the tax-extenders-section of the legislation is temporary, the ABLE Act represents a significant permanent change to the financial planning landscape for special needs beneficiaries.

The basic concept of the ABLE Act is to use the existing framework for Section 529 College Savings Plans to allow states to roll out Section 529-ABLE plans beginning in 2015, which would accept contributions that could be invested on behalf of individuals with a disability (subject to some certification requirements by a doctor, and primarily for those who became disabled before reaching age 26), be eligible for tax-free distributions when used for certain expenses for the disabled beneficiary (including education, housing, transportation, employment support, health and wellness, and more), and not disqualify the disabled individual from most state or Federal aid (e.g., Medicaid, SSI) in the process.

To the extent funds are not used for qualifying expenses for a disabled beneficiary, the growth would be taxed as ordinary income, plus a 10% penalty (similar to other non-qualified withdrawals from a Section 529 plan). Funds from a 529-ABLE account can be rolled over to another ABLE account via a 60-day rollover, for instance if the disabled beneficiary moves to another state; the designated beneficiary of the 529-ABLE account can also be changed to another (disabled) beneficiary in the same family without tax consequences (though if the new beneficiary is not disabled and/or is not also a member of the family, the rollover will be treated as a taxable distribution for non-qualified expenses). However, funds remaining in the account when the beneficiary dies will be used to repay the state for any medical assistance received under a state Medicaid plan, with only the remainder (if there is any) going to the deceased's estate or designated beneficiary (where gains will be taxable, but no 10% penalty will apply due to death).

The 529-ABLE rules (technically, a new IRC Section 529A) stipulate that any particular disabled beneficiary can have only one such account (so any/all contributions from multiple family members must be aggregated into a single account), though unlike other types of 529 accounts it appears that the disabled beneficiary will be required to use the 529-ABLE account in their resident home state (or the contracted plan of another state if the home state does not offer its own 529-ABLE).

The maximum amount in a 529-ABLE plan will still be limited to the same maximum that otherwise applies to (college-based) Section 529 plans in the state (or face a 6% excess contributions penalty) – which means its funding will be more limited than what could (potentially) be placed into a special needs trust - and as with other 529 plans, only cash can be contributed (no in-kind property contributions). In addition, contributions to 529-ABLE plans will still be subject to normal gift tax limitations (with the $14,000 annual exclusion limitation, and not eligible for gift exclusion as a transfer for education or medical expenses under IRC Section 2503(e)). Notably, contributions to 529-ABLE plans do not appear to be eligible for the 5-year-averaging rules available for gifts to 529 college savings plans, though in theory a bequest at death could fully fund a 529-ABLE plan all at once up to the state maximum. On the other hand, contributions to a 529-ABLE account may be partially or fully sheltered from a bankruptcy of the original contributor, if placed into the account at least 1 year in advance of the bankruptcy event.

The 529-ABLE plans will be subject to the ‘normal’ investment limitations and restrictions for Section 529 plans, though the new rules do provide that investment allocations can be changed twice per year, rather than the existing once-per-year changes for Section 529 plans (and in fact, the new investment-changes-twice-per-year rule will be available for both 529-ABLE and regular 529 plans beginning in 2015!).

In essence, the 529-ABLE is intended to function similar to a third-party special needs trust for a disabled beneficiary, but with far more favorable (tax-free-growth) treatment, paired with somewhat more limited annual and maximum contribution limits and potentially less favorable Medicaid-payback requirements. The funds in the new 529-ABLE plans – and the distributions from the account for qualified expenses – are designed to not be counted towards most state and Federal aid programs, though some limitations are included in the legislation (e.g., a distribution for housing expenses from a 529-ABLE account in excess of $100,000 may impact the beneficiary’s eligibility for supplemental security income [SSI]).

While final details of implementation for 529-ABLE plans still need to be worked out – this article represents just a brief review of the raw legislation itself, the IRS and Treasury have been granted 6 months to develop regulations and other supporting guidance, and of course it may be months or a year until any states have actually created any such plans to be available for disabled beneficiaries – expect to see 529-ABLE plans become a staple of special needs planning in the future.

Thank you for a great summary!

Thanks Craig!

Does anyone know if funds from an existing 529 plan can be rolled to a 529-ABLE if the beneficiary is, in fact, disabled? I have a client with son in this category.

Charlie,

I haven’t seen any potential for that yet – I can’t find any provisions allowing rollovers from 529 plans to 529A plans. But I’ll dig around a little further…

– Michael

I too would be interested to know if rollovers from 529 plans to 529a’s will be allowed. 529s were set up for twin boys, who were subsequently diagnosed as autistic. Although their 529s could conceivably be used for educational purposes, 529a’s would be far more flexible as far as qualifying expenses are concerned. Any possibility this may come to pass?

This is an interesting use of the accounts going forward

For anyone interested…529 ABLE FAQ doc states that you can roll from a Coverdell or UTMA to a 529 ABLE. I called Rep Crenshaw’s (bill sponsor) office and was told that a rollover from traditional 529 is not allowed but may be once the IRS develops their rules for this in a few months.

Charlie,

“Rolling” from an UTMA to a 529-ABLE would simply be depositing the funds of the UTMA into a 529-ABLE. It’s a liquidate account in the name of the beneficiary.

I’m not clear why/how a Coverdell could be “rolled” though, at least on a tax-free basis. I don’t see anything in the statute allowing that. Certainly, a Coverdell in the minor’s name could simply be liquidated and then transferred, but that may have tax consequences? As far as I know, it would take a (separate) Act of Congress to explicitly allow a tax-free transfer from a Coverdell to a 529-ABLE, and I don’t see any provisions for that in the recent legislation (unless it’s there and I’m just missing it).

As for IRS regulations, I guess we’ll see what they come up with in the next few months. I’m not sure if the legislation as written gives them authority to rule on 529-to-529A transfers, but if the IRS believes it has the authority, I’m sure we’ll see some kind of guidance on this!

– Michael

Section 523A(b)(2) seems to say the account is not qualified unless contributions are in cash or they are limited to the annual gift tax exclusion amount. Shouldn’t this be “and”?

(2) Cash contributions.–A program shall not be treated

as a qualified ABLE program unless it provides that no

contribution will be accepted–

“(A) unless it is in cash, or

“(B) except in the case of contributions under

subsection (c)(1)(C), if such contribution to an ABLE

account would result in aggregate contributions from

all contributors to the ABLE account for the taxable

year exceeding the amount in effect under section

2503(b) for the calendar year in which the taxable year

begins.

Thanks for the update Michael. Also good to see the IRS doing this BEFORE taxes start being filed. I helped a firm do taxes for a while, and it was a pain to tell people that we couldn’t actually process their taxes (completed in January) until Feb or March, when the gov’t agreed on extensions or revisions to tax laws. Sure wish they would decide these things in September.

.

Michael, Thank you for covering the topic, and much appreciated. In addition to creating 529A accounts, 529 college savings plans will have their number of investment changes per year increased from 1 to 2.

Best,

Paul

Paul,

Thanks for the kind words.

I mentioned the increase in the number of investment changes in the middle of the section on tax extenders – see:

“Also of note in the legislation were a few permanent changes, including new inflation-indexing beginning in 2015 for a wide range of tax penalties (including the failure to file penalty, penalties imposed upon tax preparers, and failure to file business returns), and also an adjustment to Section 529 plans that allows investment allocations to be changed twice per year beginning in 2015, up from the current once-year-year rule (further discussed later in this article in the section regarding the ABLE Act of 2014).”

Thanks again,

– Michael

Thank you, and Happy Holidays!

I took a RMD of $10,000 on Dec. 5. I would like to make a $3,000 QCD to a charity but you note this can’t be reversed. Why can’t I take advantage of the “60 day period” I would have to reverse a distribution as follows. I would return $3,000 to the IRA account then direct the fiduciary to write a check directly to the charity, all prior to year-end. Would I not then be able to satisfy the RMD with the $7,000 I kept and the $3,000 I redirected? The fiduciary says I cannot do this but why not given an individual has a 60 day period to reverse an IRA distribution?

Sam,

The problem here is that RMDs are actually not eligible to be rolled over.

Per IRC Section 408(d)(3)(D) regarding rollovers:

Denial of rollover treatment for required distributions. This paragraph [regarding the ability to do a rollover in 60 days] shall not apply to any amount to the extent such amount is required to be distributed [as a required minimum distribution].

Thus, there’s no way to “undo” the RMD once it’s done. Amounts in excess of the RMD could be rolled over (and then donated as a QCD), but not the amount of the RMD itself. So if $10k was your RMD, you’re stuck. If your RMD was “only” $6k and there was $4k excess, you could roll over up to the $4k of excess and then do a QCD with that.

– Michael

Thanks for the reply. I really don’t see this as a “rollover”, rather it is a reversal of a distribution that would be going back to the same account it came out of and then immediately directed to a qualifying charity. Seems to me I would be meeting the spirit of the extended provision if not the letter of the code section you noted. However, I know statutes are not spiritual, unless you are an IRS agent. Going forward, the thing to do is just have the fiduciary make a distribution to a qualifying charity during the year up to the amount of the rmd and then wait and see if the provision is extended once again. In those cases, the rmd’s are qualifying charitable distributions, excluded from income and not deductible. If the provision is not extended, I am in the same boat as now. The distributions are income and the contributions become itemized deductions. Right? Thanks again for your extender update and response to my question.

Sam,

Unfortunately there really is no such thing as a pure reversal of a distribution; technically, the reversal IS to do a rollover. That’s meant to be the reversal mechanic. Except in situations where rollovers are explicitly not allowed, such as RMDs. Given that an RMD is already mandatory, by definition, Congress didn’t contemplate that anyone would want/need to reverse it, and wrote the rules accordingly. :/

In terms of an approach next year, yes you’re dead-on – do the direct distribution from the IRA to the charity anyway. If the provisions are reinstated, you’ll have already done it as desired. If they’re not, you simply end out where you are now – a taxable distribution “mostly” offset by an itemized charitable deduction.

With warm regards,

– Michael

1. Can a disabled beneficiary contribute their own funds to a 529A or is it only third parties contributing on behalf of a disabled person? For instance, say that a disabled person has $100,000 in their own name or is about to receive a $100k inheritance — can that be redirected to a 529A to preserve public aid eligibility?

2. Who controls the 529A account and distributions? Generally, it wouldn’t be the disabled person, for obvious reasons (but can it be the disabled person, if appropriate?). I assume that an individual is set up as the owner (even though multiple persons can contribute) with successor owners named. Does the owner have the power to pull the money back out of the 529A in the way that a 529 owner can pull the funds back (and pay the tax/penalty on earnings)?

3. It seems like 529A is set up to be used is for a greater number of smaller expenses as opposed to 529 which are set up to pay large chunk expenses (tuition) at a later date. So will 529A be set up like a checking account to pay expenses? If so, will they really be invested long-term like 529A or will it be more short-term?

I know some of these types of questions might be difficult because it’s so new.

In anticipation of the extension of the Qualified Charitable IRA Distribution, a client had his IRA custodian issue cashier’s checks to three qualifying charities in June 2014. However, he instructed the custodian to mail the checks to him personally, then stuffed those checks into self-addressed envelopes and mailed them to the charities. Do they qualify as “direct” payments to the charities even though he had possession (but not ownership) of the checks?

Tax Increase Prevention Act will be very beneficial for the senior citizens.

Michael-

I have but one question: How the hell do you find all the time to write this information and put it together so cleanly and with all of the correct links? 🙂

Your efficiency amazes me…that or you have a great team behind you doing a lot of work as well…probably a combination.

Either way, great job as always. Thanks for all that you do for the profession!!

-Adam

Adam,

Let’s just say I didn’t spend my morning the way I originally expected to. 🙂

– Michael