Executive Summary

While there are an ever-growing number of advisory firms operating on the AUM model and offering “wealth management” services, there is still a significant gap between those that are ultimately still investment-centric, and the firms that are truly focused on financial planning first.

The significance of this difference in the culture of an advisory firm is that it impacts not only the depth of its investment vs financial planning services, but that it also shapes the technology decisions of the firm. Because the investment-centric firm is typically built around its portfolio accounting software as its core, while the financial-planning-centric firm uses its financial planning and CRM software as the hub of the business.

Yet despite the substantively different technology needs of the two firms, the overwhelming majority of advisor technology is still being developed for investment-centric firms, with at best only a token nod towards financial planning goals – even though, ironically, the financial-planning-centric software solutions often command a premium price in the marketplace!

Nonetheless, as the commoditization of investment management continues to drive more firms towards offering comprehensive financial planning services, the technology shift is beginning, from the rise of Turnkey Financial Planning Platform (TFPP) technology solutions, to the rising demand of planning-centric firms for a more financial-planning-centric client experience. Will advisor technology solutions step up to fill the void?

Investments Vs Financial Planning: What Is Your Firm’s Culture?

Arguably the biggest trend in financial planning over the past 15 years has been the explosion of the AUM business model. Whether it’s investment management firms that had always done AUM but more recently added financial planning services and became “wealth managers”, or financial planners that evolved from product-based financial planning or standalone planning fees into the AUM model as a way to get paid for financial planning, the convergence of AUM and financial planning has defined the rise of most of today’s largest financial planning firms.

Yet even amongst the wide range of firms on the AUM model that say they “do” financial planning, there’s very little consistency in what “doing” financial planning really means. In some firms, offering financial planning means they will use software to analyze the client’s situation and create The Plan, to be provided to the client up front and then updated as needed and requested, while client meetings focus on investment management and portfolio updates. In other firms, financial planning is a more continuous and ongoing experience, where every client meeting starts out with a status check on financial planning action items that are currently underway, and a conversation about the investment portfolio is just a brief check-in at the end.

Viewed another way, the essence of this distinction is that while many firms may have a strategy of doing investment management and financial planning, they differ in whether their culture is financial-planning-centric or investment-management-centric. Which matters, because while two firms may have a similar business model and state they provide similar services, it’s the firm’s culture – what they do even when no one is looking – that guides everything from how they really deliver those investment and financial planning services, what’s on the agenda for every client meeting, to what technology the firm will rely upon in order to serve their clients well.

What Is The Center Of Your Advisor Technology Stack?

From the technology perspective, one of the notable challenges in executing an advisory firm is that whether it is investment-centric or financial-planning-centric, most firms on the AUM model end out using the same core advisor technology stack, focused around CRM, portfolio accounting, and financial planning software, with ancillary add-ons to support those three core areas.

However, while the technology stack may be similar across firms, its central focus may actually be quite different, driven by the underlying culture of the firm.

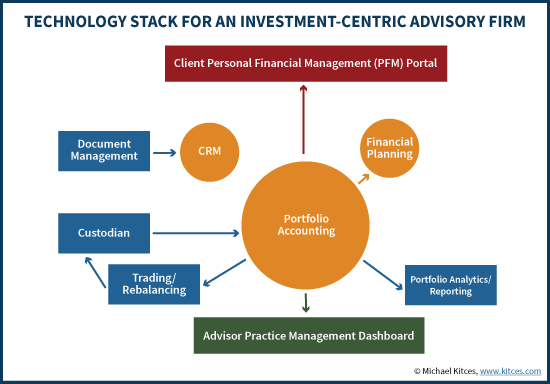

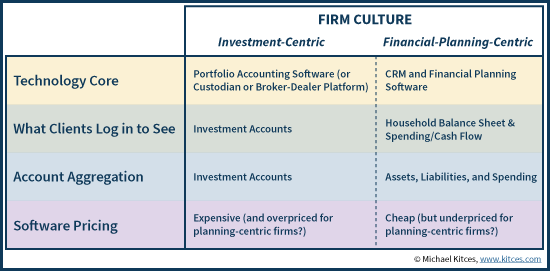

The technology center of an investment-centric firm is typically the portfolio accounting software, and supporting trading platform. This is the software that tracks and monitors the portfolios themselves, and manages the rebalancing and trading activity, which in turn form the center of the (investment-centric) firm’s core value proposition. The CRM software sits off to the side (with relevant portfolio-accounting data perhaps pushed into it), and the financial planning software is simply used as needed (perhaps with the investment account balances updating automatically into the planning software from the portfolio accounting software). Clients interface with the firm through a website or portal that reflects the account balances and performance of the managed accounts.

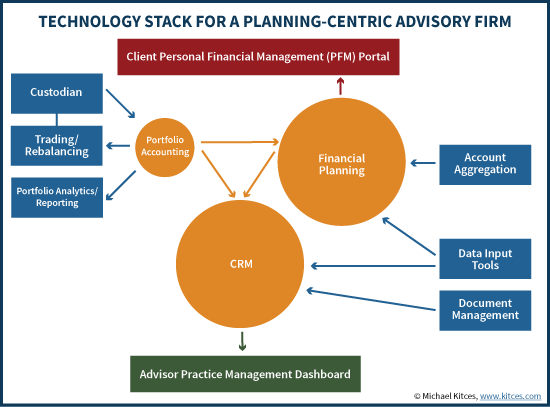

On the other hand, the technology center of a financial-planning-centric firm is typically different. The “center of gravity” shifts from the portfolio accounting software, to the financial planning software and CRM systems, and typically includes more supporting software tools to go along with it (including account aggregation and data input tools), as the sheer amount of data to manage (pertaining to financial planning) goes far beyond what is “just” in the portfolio accounting software platform alone. The flow and integration of data is more complex, and the CRM often becomes the ‘hub’ of financial planning activity, with all data pushed into (and through) it. The client’s interface is now driven by the planning software (showing the status of the plan), rather than the portfolio accounting software (just showing the investment accounts).

And perhaps most significant, from the perspective of the advisor, is that the advisor’s view into the business is materially different between an investment-centric and a planning-centric firm. In an investment-centric firm, the dashboard of the financial advisor – the first software he/she logs into every morning to see the status of the business and “what needs to be done” in terms of client trades, recent performance, and account balances – is typically driven by the portfolio accounting software. In a planning-centric firm, it’s driven by the CRM (or the financial planning software itself) to see the latest financial planning relationship issues that need to be addressed.

The Technology Divide Between Investment And Financial Planning Firms

The reason cultural differences in investment- versus financial-planning-centric firms matters from a technology perspective is that, when the difference in culture is reflected in a materially different design of the advisor technology stack, it suddenly means that some software or platforms may be a better or worse fit than others for the firm.

For instance, an investment-centric firm may use its CRM primarily to “just” record client communication and transactional information, but not necessarily to manage an ongoing financial planning relationship. As a result, a relatively “simple” CRM system is sufficient to capture the key contact information, and perhaps record simple points of communication and correspondence. Conversely, for financial-planning-centric firms, an in-depth CRM that can handle complex financial planning workflows and ongoing relationship needs becomes crucial. In this context, it’s thus no surprising to see that Junxure CRM has long had a strong positioning amongst financial planning firms (because it was built by a financial planner, for use in planning-centric firms), while others have struggled (to the point that Salesforce decided to build its own Financial Services Cloud solution to better support client relationships).

Similarly, because planning-centric firms need more effective management of financial planning data, eMoney Advisor’s financial-planning-centric portal allowed it to harness significant market share of financial advisors, despite being priced nearly 3 times the cost of its typical competitors. While investment-centric firms simply want to gather client data up front and deliver a printed financial plan output may choose a less expensive financial planning software alternative, planning-centric firms want to craft a financial-planning-centric experience, where clients log into their client portal and immediately see their financial plan, including their household balance sheet and cash flow tracking (not just their investment accounts!), continuously updated with relevant financial planning data, and with a dashboard that allows the advisor to manage the financial planning needs of the entire client base. By contrast, the investment-centric firm typically has clients log into a portal that "just" summarizes investment accounts.

The Software Gap For Financial-Planning-Centric Firms

Ultimately, the issue that arises from the technology needs of investment-centric vs planning-centric advisory firms is that most of the industry has focused on technology for investment-centric firms, despite the irony that financial-planning-centric firms are often willing (or forced but able to) pay more for good solutions!

This gap can be seen in the fact that at any event that has software solutions for financial advisors – particularly tech-centric events like the T3 Advisor Technology conference – the number of software solutions that do portfolio analysis and reporting typically outnumber the financial planning software providers by a 3:1 or 5:1 margin.

Similarly, the pricing of advisor software in today’s environment is clearly reflective of investment-centric firms. An advisor who has 100 clients, at typical industry technology pricing, could pay as much as $15,000 for a portfolio accounting solution (e.g., Orion Advisor Services), but just $1,200/year for financial planning software (e.g., MoneyGuidePro). A larger advisory firm with a dozen advisors and 1,000 clients might pay $15,000 for financial planning software licenses, but only because portfolio accounting software could be $75,000 to $150,000/year or more for that many clients and accounts. (One can only wonder what financial planning software might be capable of if it, too, was priced at $75,000 to $150,000/year!)

Even a look at the recent “robo-advisors-for-advisors” movement of better technology for advisors to onboard and execute for clients is focused around facilitating the input of investment information and the ability to process paperwork to open investment accounts and transfer investment portfolios. Thus we have an explosion of “robo” technology for investment advisors, from Jemstep to Vanare to Oranj to Autopilot to Schwab’s Institutional Intelligent Portfolios, and more. In the meantime, the only third-party "robo" software to come out in years that offers technology to facilitate the onboarding and data input of financial planning clients is PreciseFP.

Ironically, though, the complexity of delivering on a quality financial-planning-centric relationship actually commands a premium price in the software landscape for financial advisors. Planning-centric Junxure CRM charges $65/month/user, while the more broad-based Redtail CRM is $99/month for up to 15 users. eMoney Advisor offers a combination of financial planning software and holistic financial planning dashboard and account aggregation for $324/month, while MoneyGuidePro focuses on just producing and delivering a financial plan and charges just 1/3rd the price ($108/month). And there’s so much demand for a quality holistic data input process that PreciseFP is able to charge firms $59/month just to gather data that gets pushed into other financial planning software and CRM!

Notably, the difference in needs between investment-centric versus financial-planning-centric firms is also beginning to shape the design of turnkey advisor platforms as well. While the past decade has been dominated by the rise of the Turnkey Asset Management Platform (TAMP), which brings together a consolidated suite of technology solutions on a single platform for investment-centric firms, now we’re beginning to see the rise of Turnkey Financial Planning Platform (TFPP) solutions instead – providers that offer a consolidated suite of technology solutions on a single platform for financial-planning-centric firms instead. Our own XY Planning Network bundled technology solution was created in this mold (to support a particular kind of financial planning firm serving a particular type of clientele), and United Capital’s new FinLife Partners platform (which Joe Duran has dubbed a Turnkey Advice and Planning Platform [TAPP]) is similarly built around their financial-planning-centric Salesforce-CRM-based technology platform.

Which means ultimately, we may be at just the front end of the next wave of advisor technology innovation – a shift from software solutions for investment-centric firms, to deeper solutions that are relevant for financial-planning-centric firms, who have more complex needs but are willing to pay a higher price point, because the planning software doesn't just support product sales but actually facilitates an ongoing financial planning value-add (not to mention achieving operational efficiencies). And the trend may only accelerate further, as the ongoing commoditization of pure investment management services drives more and more firms towards financial planning – and for some, manages to shift their entire culture to become more financial-planning-centric, which will compel them to find different technology solutions.

So what do you think? Is yours an investment-centric or a financial-planning-centric advisory firm? When you meet with clients, is financial planning or a portfolio review at the top of the agenda? When your clients log into the firm’s website or portal, what do clients see first?

At the heart of this discussion is what configuration of financial services comprise continuous, comprehensive counsel necessary for expert standing in advisory services. This goes beyond statutory duty to encompass professional standing in advisory services incorporating budgeting, cash flow analytics, etc.. The data that drives this level of counsel is largely not tracked by broker centric (investment centric) firms and give Advisors a huge edge in the depth and breadth of counsel, yet brokers would be extremely well se4rved by this capability. The resolution revolves around trading desk. There are actually a few brokerage firms exploring how they might eliminate trade execution cost/commission sales to align with the fiduciary construct which treat trade execution as a cost center to be minimized in the client’s best interest, rather than a profit center in the b/d’s best interest. Advisors would gain the ultimate in differentiation relative to brokers. Cost would be streamlined and compensation would be based on rendering very specifically defined financial services for an ongoing fee. This development may scare product focused brokerage/custody firms, would be far less expensive and afford a far superior level of counsel as trade execution becomes a commodity service (which even today can be obtained for free in high end advisory services applications like CALPERS, Betterment Institutional, Private Trust Banks, Large Institutional Consultants, etc.). This might be a bit prescient, but is where things are headed. A new business model is emerging that is faster, better, cheaper and in the client’s best interest. The free market at its best.

SCW

Hi Michael, I enjoyed your column. I don’t think investment advice and financial planning advice can be delivered separately. This is my economics training coming through. Economics tells us that people want to have a smooth living standard with limited downside living standard risk. The is what my company’s ESPlannerPro software is designed to deliver. It doesn’t take spending targets as given and consider the chances of making those targets. Instead, it adjusts the spending targets to the performance of the portfolio. We’ve incoporated this in our software for years and have produced, for years, the risk-return tradeoff measured in terms of the risk of the household’s living standard being low or high in the future and the average level of the household’s living standard. My best, Larry

Larry,

Thanks for commenting.

The point here is not necessarily to talk about investment and financial planning advice being delivered ‘separately’. As you’ll note, both graphics of investment-centric and planning-centric firms have tools for both in there somewhere.

But in practice, there’s still a significant difference between investment-centric and planning-centric software, both from the advisor’s process and the client’s experience.

For instance, an investment-centric firm may have tools for how an investment portfolio fits into your financial plan (the intersection of the two), but that doesn’t necessarily mean it has the tools to do the rest of the financial planning analysis, such as when it’s better to liquidate the portfolio to either pay down student loan debt or bridge retirement income while delaying Social Security (to pick two random planning-centric-but-not-investment-centric examples).

In the current software landscape, many advisors use similar tools to do ‘both’, but the evolution that’s emerging is that the needs of truly investment-centric firms are quite different than the needs of truly planning-centric firms (both for the advisor and for the client). Which creates significant opportunity for new and better software solutions that change the landscape for adoption.

– Michael

It has been disappointing to see what is out there for a financial-planning-centric “solopreneur”. I have a technology background, and am thankful b/c I’ve had to cobble together what I need in many instances!

I’ve evaluated every CRM under the sun, either through their website-listed Features, a free trial, or even purchasing and using. I’ve started using Contactually for CRM (it’s ability to automatically link Exchange-based emails from clients, along with its ability to set up Buckets of people so nobody falls through the cracks and its Kanban-inspired Programs). So many are either too expensive for 1 advisor (*ahem* SugarCRM and Microsoft Dynamics), have no/limited workflow management and email templates (VTiger and the now-dead Outlook Business Contact Manager), aren’t customizable enough (Redtail or Insightly), or have a UI that is too painful for me to use (PlanPlus).

MoneyGuidePro has made a lot of advancements over the years, and they have aced out eMoney (man that was some painful data entry back in the day), Financial Profiles, and many others.

Portfolio design and maintenance, billing and expense tracking, client service management, financial planning, social media interaction and archiving, email, project management, knowledge repository (OneNote), calendar and tasks – it’s a lot to coordinate for just 1 advisor!

Maybe I’m too particular in wanting a system that works how I work instead of completely changing my workflow to cater to the software development teams. Maybe by remaining a sole proprietor I’m keeping my budget too low to enjoy the Orions and Junxures of the world. I’ve lived in the software development world and I know how hard it can be.

The firm that can deliver what I need would have an extremely loyal, willing to refer, willing to pay client. Too bad they are fictional!

Elliott Weir

III Financial

Junxure is worth it!

Great insight, Michael. Adding to your comments, I believe it’s easier for financial planning firm to migrate into investment management than the other way around. Adding financial planning software to an existing investment company and saying the company now does financial planning doesn’t attract much business because it doesn’t change the company’s investment centric culture or its goal of attracting AUM.

As an aside, a difficult issue is when you’re using a fairly comprehensive planning program and someone comes out with an outstanding new program on a discrete subject – say Social Security claiming or order of liquidation. This would be a great additional feature to clamp on to the existing package – even at an additional charge. But it’s hard to justify spending the money and the brain damage to subscribe to an entirely new piece of software.

The financial planning chart you have makes the assumption they are still involved in the account management. A third chart option would be financial planning only firms that don’t do any investment management and can cut out those expenses as well.