Executive Summary

Welcome to the December 2018 issue of the Latest News in Financial Advisor #FinTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors and wealth management!

This month's edition kicks off with the big news that Blackrock is taking a whopping $123M stake in Envestnet as the company doubles down on the strategy of using technology as a distribution channel after its $150M acquisition of FutureAdvisor just 3 years ago… and raising the question of both what other asset managers may acquire FinTech companies for distribution in the coming years, and what Envestnet itself may invest into and acquire with its newfound cash.

From there, the latest highlights also include a number of interesting advisor technology announcements, including:

- E*Trade ramps up its competitive push into the (large) RIA custodial space with new account aggregation tools and an advisor referral program,

- RightCapital becomes a real financial planning software contender with enterprises as a Commonwealth deal takes the company beyond its independent RIA roots,

- Stonecastle launches an FDIC-insured cash management solution for RIAs to compete with MaxMyInterest as cash yields start to matter again, and

- United Capital partners with Medicare BackOffice as “real” retirement planning increasingly expands beyond just retirement portfolio management.

Read the analysis about these announcements in this month's column, and a discussion of more trends in advisor technology, including a signal that Investopedia’s Advisor Insights may be shutting down, a Vestorly pivot away from content marketing into trying to license its content curation engine instead, Smartasset ramping up its financial advisor directory for consumers (but without learning the lessons of BrightScope from years ago), Morningstar fighting back against Riskalyze and Blackrock’s Aladdin, and TD Ameritrade announcing the finalists for its first “Innovation Quest” FinTech competition.

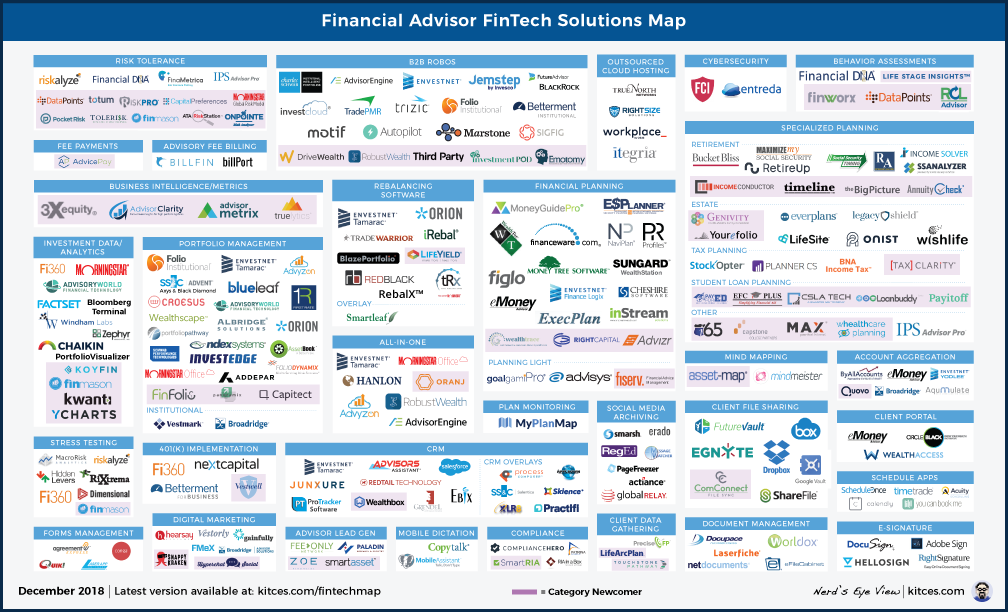

And be certain to read to the end, where we have provided an update to our popular new “Financial Advisor FinTech Solutions Map” as well!

I hope you're continuing to find this new column on financial advisor technology to be helpful! Please share your comments at the end and let me know what you think!

*And for #AdvisorTech companies who want to submit their tech announcements for consideration in future issues, please submit to TechNews@kitces.com!

Blackrock Doubles Down On The Future Technology As A Distribution Channel For Asset Managers With $123M Stake In Envestnet. From the consumer perspective, the rise of the robo-advisor movement raised the question of whether it’s better to get a diversified portfolio from a human advisor or a robo-advisor, and highlighted the extent to which the industry’s legacy technology and (still-)paper-driven process had fallen behind the capabilities of modern technology tools. However, from the perspective of ETF manufacturers (and mutual fund managers more generally), the rise of the robo-advisor movement represented a potential shift in the distribution of products, where “robo” advisors could be a distribution channel (for their products to be used in managed accounts) just as there are various human advisor distribution channels (e.g., RIAs, wirehouses, IBDs, banks, etc.). Accordingly, within just a few years, Schwab launched its Intelligent Portfolios platform as a way to distribute its proprietary ETFs, the rebalancing software platforms began to launch “model marketplaces” and cut deals with asset managers to include their model portfolios, and Blackrock bought B2C-turned-B2B robo-advisor FutureAdvisor to have its own “robo-for-advisors” platform through which it could distribute its ETFs in Blackrock-designed default model portfolios. And now, Blackrock is doubling down on the strategy of using technology as a distribution channel 3 years later, taking a whopping $123M stake in Envestnet to build its suite of Digital Wealth tools – including FutureAdvisor, its iRetire planning tools, and the Blackrock Advisor Center – more directly into Envestnet, in the hopes that advisor adoption of the Blackrock software through Envestnet will lead to advisor adoption of Blackrock’s ETFs and other products in their client portfolios. The deal comes about after an initial integration of Blackrock’s iRetire solution to Envestnet led to “unexpectedly” high adoption (and ostensibly, unexpectedly favorable asset flows to Blackrock as iShares portfolios are often shown by default in iRetire-recommended retirement solutions for clients). Ultimately, the Blackrock deal should cement the emerging approach of treating technology as a distribution channel, and may spawn copycat deals for other asset managers to acquire technology companies (just as other asset managers bought or invested into robo-advisors after Blackrock bought FutureAdvisor, and in the previous generation of product distribution insurance companies bought broker-dealers to support distribution), though doing so may also begin to accentuate the risks of newfound conflicts of interest in technology and finding the balance between “open architecture” platforms and just how aggressively a particular asset manager’s products are pushed or not (e.g., Envestnet maintains it will remain open architecture, but iShares will likely still be the default products recommended in Blackrock-software-created portfolios through Envestnet?), and whether advisors will need to better scrutinize the integrity of the recommendations their software queues up. In the meantime, the question from many is what Envestnet itself will do with its cash, with recent analyst predictions that Envestnet may also go on a(nother) FinTech acquisition binge in 2019 as it seeks to expand the reach and capabilities of its own platform (to make it an ever-more-appealing distribution channel to even more asset managers?).

Trust Company Of America Ramps Up RIA Custodian Competition With New Account Aggregation Tool And Pending Advisor Referral Program Rollout. The independent RIA custodian landscape is dominated by the “Big 3” of Schwab, Fidelity, and TD Ameritrade, followed by up-and-comer Pershing Advisor Solutions, and then a number of much-smaller “niche” RIA custodians like SSG for “smaller” RIAs under $100M, TradePMR for those who want an all-in-one tech platform, Millenium Trust Company for RIAs that do a lot of alternatives, and Trust Company Of America for RIAs running model portfolios (or operating as model-based TAMPs for other RIAs). But last year, E*Trade announced that it was acquiring Trust Company of America in a massive $275M deal, it what appeared to be a play for the online retail brokerage firm to pivot into the RIA channel. And now, a year later, the new “TCA by E*Trade” platform is beginning to ramp up, with announcements this month of a new account aggregation portal for advisors dubbed “CompleteView,” where clients can link their outside investment and bank accounts to see a holistic view of their financial household, which may be appealing to advisory firms that have not fully invested into financial planning software but want to begin to take a more holistic approach with clients. Perhaps even more notable, though, was TCA by E*Trade’s second November announcement, that it will be rolling out a new referral program that will send retail E*Trade clients to RIAs on the TCA – an opportunity promising enough to lure even Edelman Financial Engines to a new custodial relationship with TCA. Though ultimately, what’s really notable is not merely that E*Trade is looking to monetize some of its more delegation-oriented retail accounts with its affiliated RIAs – a strategy long-since deployed by the Schwab, Fidelity, and TD Ameritrade retail divisions as well – but that it signals a substantial commitment by E*Trade to scale up the appeal of its RIA platform. And with E*Trade’s size and scale – as one of the largest discount online brokerage firms in the country – not to mention the custodial growth potential of landing Edelman’s firm (and likely other large RIAs to follow), the potential exists for TCA to gain the necessary resources to continue to roll out increasingly competitive technology solutions for RIAs and provide new level of competitive pressures on the technology offerings of today’s RIA custodians. Stay tuned for more TCA by E*Trade technology announcements in 2019?

Advisor Group [Finally] Shows The Real Promise Of “Robo” Tools For Advisors. The first era of robo-advisors ran from 2012 to 2015, as direct-to-consumer platforms like Betterment and Wealthfront revealed how far the financial services industry had lagged in creating efficient client-centric onboarding processes for investment accounts. And when Schwab and Vanguard pivoted into their own competing services in 2015, with the eye-popping success of billions of dollars into their new managed accounts in under a year, the second era of robo-advisors began as industry incumbents went all-in on acquiring, building, or partnering to develop their own “robo” solutions. Yet the reality is that most consumers don’t just voluntarily “opt” themselves into a robo-advisor, and the actual segment of self-directed robo-advisor consumers is still minuscule relative to the total size of the asset management industry; and even worse for broker-dealer incumbents in particular, their own brokers didn’t want to use and “sell” a robo-advisor solution that implied they themselves added no value and were redundant to the equation. For advisors that can and do add value on top of what a more digitized and efficient account-opening process can provide, though, equipping them with “robo” tools still has the potential to drastically improve the back office efficiency of advisory firms. And in this context, it is notable that major independent broker-dealer Advisor Group (with subsidiary IBDs Royal Alliance, FSC Securities, SagePoint Financial, and Woodbury Financial) has just announced the rollout of its new and aptly named “Equipt” onboarding system. Announced last year as being built on top of the robo-advisor-for-advisors Jemstep Pro, Equipt aims to create a “robo-like” digital onboarding process for advisors, making it feasible to open everything from simple IRAs to complex advisory accounts (and for dual-registered advisors, to open both brokerage and advisory accounts) via a single platform, while providing the advisor flexibility to decide where and how data is entered (and whether the advisor or client are responsible for it). The end result: an estimated 50%(!) decrease in the time to open up investment accounts for clients by fully digitizing the previously- (and still for many firms, currently-)paper-intensive process, and a solution that Advisor Group in its very naming of “Equipt” emphasizes equipping the advisor for efficiency while dropping the “robo” moniker altogether. Notably, Advisor Group suggests that it has been able to leapfrog rival broker-dealers in the rollout because their own back-office systems do not have the “technology debt” overhang of others that still rely on legacy mainframe technology… though given that the rollout was originally announced for Q4 of 2017 and has arrived a full year later, it appears that even more modern IBD technology systems are still struggling to integrate to and overlay digital onboarding processes on what are often still even-more-old-school custody and clearing platforms that underlie them.

StoneCastle Launches Competitor To MaxMyInterest As FDIC-Insured Cash Management For RIAs Heats Up. For nearly 10 years, there has been remarkably little focus from advisors and their clients on cash… for the simple reason that after the financial crisis, the Fed dropped interest rates so low that most cash accounts literally yielded 0%, or at least so close to 0% that investors just didn’t care. Cash was trash. But now as the Fed has begun to raise rates, and cash can at least generate some yield, there is a growing interest in cash management solutions… especially since not all banks, money markets, and financial institutions have been increasing their cash yields evenly, which has made it especially profitable to “shop around” for yield. And unlike managing cash, the last time yields were compelling – nearly a decade ago – the growth of online banking and digital account opening and transfer capabilities makes it easier than ever to move cash around and shop for yield. Or to even automate the process. In this context, a few years ago MaxMyInterest launched a “MaxForAdvisors” service for financial advisors specifically designed to automatically move and shift client cash amongst 5 different online banks, automating the process of maximizing bank yield. And now, in an effort to one-up the competition, a “newcomer” to the advisor channel (previously focused solely on institutions) called StoneCastle has launched “FICA For Advisors” (short for “Federally Insured Cash Account”), that similarly aims to automatically route and transfer client cash across dozens of different online banks to shop for maximal yield. In fact, while MaxMyInterest focuses on “just” 5 of the most popular (and typically highest-yielding) online banks, StoneCastle is offering access to nearly 800(!) banks, which means clients who spread accounts amongst all of them can obtain as much as $25M of FDIC insurance per person (albeit one $250,000 limit at a time, and with each account providing its own cash yield). And while MaxMyInterest transfers out and allocates cash directly to the various online banks, StoneCastle routes them all through a single centralized brokerage account with US Bank (which means one statement and one Form 1099-INT at the end of the year). In addition, Stonecastle has thus far managed to offer slightly higher yields, reportedly as high as 2.22% (compared to MaxMyInterest’s 2.06%), ostensibly by leveraging their bulk bargaining power given StoneCastle’s institutional relationships. The caveat, though, is that StoneCastle has not built connections to the most popular RIA custodians Schwab, Fidelity, and TD Ameritrade (though they do have a connection to Pershing Advisor Solutions), which may limit how “automated” and efficient the process really is thus far compared to MaxMyInterest. On the other hand, if market volatility continues to rise, and advisor allocations to cash rise, there may soon be even more interest from RIAs as investors rotate from “cash is trash” to “cash is king”… especially when RIA custodians themselves continue to face rising scrutiny about their own paltry cash yields on related-bank sweep accounts.

RightCapital Financial Planning Software Becomes A Real Contender For Enterprises With Big Commonwealth Deal. While financial planning software has more than a dozen solutions competing for advisors’ attention, the “big 3” by advisor count and market share have long been NaviPlan, MoneyGuidePro, and eMoney Advisor, with the latter two gaining the bulk of growth in recent years. And because no financial planning software has very effective export or migration tools, switching costs to change providers are extremely high, causing most advisors to become entrenched in their existing vendors where years or even decades of historical plans for clients have accumulated… and making it especially hard for new solutions to break into the market. The problem is especially severe in the enterprise marketplace for financial planning software, where banks and broker-dealers are often tied up into long multi-year contracts, and making a transition to a new software involves not only transitioning data and retraining hundreds or thousands of advisors, but also rebuilding what is often an additional proprietary layer of deployment features on top. As a result, to the extent that new financial planning software companies come to market at all, most start in the smaller independent RIA community (where there are more new forms being formed and the ability to convince a firm to switch is still a much lower barrier than a major enterprise), and then try to “pivot” upmarket to enterprises after they gain initial traction. And so it is especially notable that industry-trend-setting independent broker-dealer Commonwealth Financial – a firm that is “notorious” for having very high demands and expectations on enterprise vendors to integrate deeply into Commonwealth’s Client360 platform – announced last month that it was partnering with newer financial planning “upstart” RightCapital, officially marking the transition of the company from a strong player in the independent RIA channel (where its software user ratings were already on par with eMoney and MoneyGuidePro) to a real contender for enterprises. In fact, it’s notable that RightCapital won the deal despite MoneyGuidePro already having a relationship with Commonwealth… raising the question of whether MoneyGuidePro’s insistence on focusing only on interactive planning tools for client meetings themselves and not an additional layer of account-aggregation-based client portal capabilities (and the integration potential that creates) may finally begin to take a toll on its enterprise market share for the future-looking firms most focused on holistic (year-round) financial planning engagement with clients? At a minimum, though, look for RightCapital to increasingly have a seat at the table in enterprise financial planning software proposals in the future… and the additional capabilities the company may add in the coming years as it gains traction, market share, and scale?

Investopedia Advisor Insights Suspends New Content Submissions From Advisors As Yet Another Advisor Q&A Platform Struggles? For most financial advisors, the greatest struggle of digital marketing is figuring out how to create their own original content that can showcase their expertise and establish credibility. For a few who are more skilled writers (or at least are able to communicate effectively in writing), though, the challenge is not creating the content, but figuring out how to get it seen by prospects. Which in turn has led in recent years to the rise of not only using various social media platforms for content distribution, but also the rise of numerous advisor publishing and “Q&A” sites that will showcase the content advisors create on platforms that have existing readership, starting with early players like AdviceIQ, then shifting to consumer Q&A sites like NerdWallet’s Ask An Advisor, and more recently with the launch of Investopedia Advisor Insights. The problem, however, is that relying on social media platforms like Facebook and LinkedIn to publish content leaves advisors at the mercy of those platforms making unfavorable changes to their algorithms (as both have done repeatedly in recent years), and using third-party content distribution platforms may provide the reach but leave advisors no effective means to actual capture a lead’s contact information or develop the ongoing presence necessary to establish trust and turn a reader into a client (as most people who browse to a free personal finance website for information via a Google search aren’t likely to follow through and hire the advisor who wrote it when by definition the consumer was searching for free content answers in the first place). As a result of the limited success advisors were (or rather, weren’t) having, AdviceIQ was ultimately shut down and sold to Financial Media Exchange, NerdWallet eventually shut down its Ask An Advisor platform… and now Investopedia Advisor Insights has announced that it is no longer accepting advisor article submissions as their editorial team “reassesses the Advisor Insights content strategy.” The problem for advisors, though, is not merely that these platform shifts compel them to start over again, but that their content itself will live on with those platforms (or in the case of AdviceIQ, became part of the FMeX library that other advisors can now use to market to their clients). Which means the advisors are left both without a marketing platform and stuck competing in the future against their own original content hosted on other platforms! Which is why our Nerd’s Eye View blog has repeatedly cautioned advisors not to build their content and expertise on “borrowed land” (i.e., other social media or publishing sites), and explicitly urged advisors not to adopt Investopedia’s Advisor Insights when it launched in 2016. On the plus side, at least what should hopefully be a shift away from advisors giving away their content to third-party platforms will create an opportunity for more and better advisor technology solutions to build great websites and support the distribution of their content from their own platforms, instead?

Vestorly Woes Highlight Problems With Advisors Using Third-Party Marketing Content? The explosive rise of digital marketing automation platforms like Hubspot and MailChimp in recent years has spawned a series of niche advisor technology companies looking to replicate the success of the model in the financial services industry, from early entrants Vestorly and FMG Suite to the more recent AdvisorStream and Snappy Kraken. But after raising $12.6M of Series A funds back in 2016 to scale up its financial advisor marketing automation tools, Vestorly has now announced that co-founder Justin Wisz has departed, and co-founder and new CEO Ralph Pahlmeyer has stated a plan to shift the entire Vestorly model away from providing marketing automation tools for advisors and instead is looking to third-party license the content curation engine it created to feed its original marketing platform instead, noting that the basic tools of marketing automation have become commoditized and Vestorly’s unique value proposition is its ability to sort a wide range of third-party content by the probability that consumers will actually open and read it. In other words, Vestorly is aiming to license its content curation tools to other marketing automation platforms – with an initial deal with Hootsuite already announced – to help those other platforms determine the “right” third-party content for advisors to share that clients will be most likely to open, click on, and read. Yet ultimately, Vestorly’s decision to pivot away from its marketing automation core suggests that the company was having trouble producing real results for advisors and/or differentiating the value of their content curation engine over its competitors in the first place… which raises the question of whether licensing its content curation engine to other firms will produce any better results for advisors. As in the end, the fundamental challenge is that “just” curating third-party content – even well-selected third-party content using Vestorly’s algorithms – still won’t necessarily produce any new client results for financial advisors themselves, until/unless the advisors also produce at least some of their own original content that actually demonstrates their expertise and establishes credibility with prospects (as yours truly cautioned about Vestorly years ago). Still, though, to the extent that even advisory firms that produce some of their own content to showcase their expertise may want to fill it in with third-party curated content, there is arguably room to leverage Vestorly’s content curation capabilities as complementary. Though whether there’s really much appetite for it in the financial advisor marketplace with a limited number of B2B competitors that Vestorly can sell to in the first place, and whether Vestorly’s curation is really that much better than what other platforms (or advisors themselves) can select in content to send their clients more simply or directly, remains to be seen. At a minimum, though, Vestorly’s woes are an ominous warning sign for their other advisor marketing automation competitors that advisors are done with the honeymoon phase of digital marketing promises, and are now starting to vote with their feet for what solutions are really producing results (or not)… even as newcomer competitors like Snappy Kraken and AdvisorStream are aiming to step up and fill the void.

Snappy Kraken Adds Exclusivity To Its Third-Party Content For Financial Advisor Marketing. With the rise of marketing automation platforms for advisors, two challenges have arisen: the first is whether or how advisors can convert prospects to clients using (only) third-party “canned” content that is curated for them; and the second is that even if a platform is successful in converting clients, eventually more advisors buy in the same platform and process, and prospects may start seeing the same marketing emails and campaigns from multiple advisors at once. In this context, Snappy Kraken announced this month a new offering it has dubbed “Exclusive Content Rights,” which will grant financial advisors an exclusive license to use Snappy-Kraken-generated marketing content in a particular geographic region, to avoid the risk that an advisor’s prospects see the same marketing content from other advisors as well. Of course, that does potentially limit Snappy Kraken’s total market size in the long run. But Snappy Kraken appears to be aiming to offer a more “premium” solution at a higher cost ($559/month, albeit heavily discounted in December as a part of the launch of their new Exclusive Content program) that doesn’t necessitate having an extremely large volume of advisors. And when financial advisors generally have the bulk of their clientele within one metropolitan area (and often within just a few miles of their offices in crowded high-traffic areas), there is arguably still ample room for Snappy Kraken to create its own custom content and license it across a relatively large number of geographic regions, one advisor at a time. Or alternatively, to eventually create a second (and different) set of custom marketing campaigns to license to a second (and different) set of financial advisors in overlapping geographic regions (without violating the promise of exclusive custom content to the first set of advisors). The caveat, though, is that it’s not entirely clear that having overlapping marketing content in a single geographic region is actually a problem for financial advisors in the first place, in a world where advisors in the aggregate still only serve a small percentage of the total population, and advisors tend to see each others’ potentially overlapping marketing (by following each other on social media) more often than prospects necessarily sign up for and see multiple advisor mailing lists (with duplicative advisor marketing content) at the same time. And of course, the challenge still remains that at some point, advisors need to demonstrate their own expertise and credibility beyond “just” using third-party content – even professionally-produced and exclusively-licensed third-party content – though if Snappy Kraken’s custom exclusively-licensed content is targeted enough to particular types of advisors and their value proposition, it should have the potential to generate bona fide quality leads for financial advisors.

SmartAsset Expands New Advisor Directory But Fails To Learn From BrightScope’s Mistakes? When BrightScope first launched its “Advisor Pages” service in 2011, its goal was to help clean up the industry by making it easier for consumers to find good advisors – and to spot bad ones – by aggregating publicly available regulatory data from the SEC’s IAPD and FINRA’s BrokerCheck databases into a single location. However, with 300,000+ financial advisors, the only feasible way to do so was to scrape not-always-clean regulatory data itself, ultimately leading to a backlash when occasionally-incorrect data was posted, which was only compounded by the fact that advisors initially had to pay an additional fee to add additional (and more accurate) data to their profiles (which the firm eventually allowed for free). However, with BrightScope being sold to Strategic Insight last year (and primarily for their 401(k) data business, not Advisor Pages), financial technology company SmartAsset announced earlier this year the launch of a new BrightScope-esque Advisor Pages matchmaking directory with an initial launch of 10,000 profiles. And now, SmartAsset is accelerating the rollout, ramping up to 50,000 advisors profiles already (and aiming for 100,000 by the end of December) on a new SmartAdvisorMatch.com website. Yet despite the furor that overtook BrightScope in its early years for posting not-always-accurate information about advisors and then providing insufficient means to update and correct it, SmartAdvisorMatch provides no direct means for advisors to submit corrections short of submitting an email request to SmartAsset for them to call the advisor about it (and potentially try to upsell SmartAdvisor’s paid lead generation services?), despite readily apparent errors like our local Columbia, Maryland advisor listings also showing advisors from Columbia, Missouri and advisors from Columbia, South Carolina as well (while the Columbia, Missouri listings show advisors from Columbia, Maryland). And unfortunately, SmartAdvisorMatch has no actual directory of advisors by name, nor any way for advisors to search for themselves, except for searching by geographic location (which, as noted above, is wrong for some advisors and would potentially make them unfindable even to themselves). Perhaps even more controversial to some, though, is that SmartAdvisorMatch appears to only and exclusively list brokers registered with FINRA to sell products, and not any standalone RIAs actually registered to get paid for giving advice (despite being heavily funded by RIA aggregator Focus Financial in its recent $28M Series C round). Nonetheless, in a world where FINRA’s own BrokerCheck pages are not indexed to search engines and make it difficult to easily find out information about an advisor’s regulatory history (notwithstanding FINRA’s own recent national ads encouraging consumers to use BrokerCheck), arguably there is still room in the industry for someone to make a consumer-centric platform that effectively aggregates appropriate regulatory data in an easily-findable format… but hopefully in a manner that is friendly to advisors who want to be certain consumers get the right information, too?

United Capital Goes Deeper On Real Retirement Planning With Medicare BackOffice Partnership. The ongoing shift of the advisory industry into the assets-under-management (AUM) model, from the growth of RIAs to the rise of fee-based accounts in broker-dealers, is leading more and more financial advisors to focus on retirement planning – as the more that advisors focus on managing portfolios as a part of their financial planning services, the more they tend to “go where the money is,” which is baby boomers (and their Silent Generation parents) who are transitioning into or already in retirement and still hold the overwhelming majority of investable assets to manage in the first place. However, for many financial advisors, “retirement planning” is still little more than running retirement planning accumulation and decumulation projections in financial planning software, and then reverting back to managing the retirement portfolio… and not addressing the real concerns of retirees, which aren’t just about generating retirement income from their available retirement assets (though that certainly matters). In fact, a recent major PwC study of Baby Boomers found that their biggest fear about retirement isn’t actually running out of money before the end of retirement, but how they’re going to handle their health care costs in retirement. Which means “specializing” in retirees in the future will increasingly involve providing solutions in areas like Medicare planning as well, given not only the complexity of the upfront Medicare enrollment process but also the ongoing annual review process during the annual Open Enrollment Period (especially for Part D prescription drug plans). And so it is perhaps not entirely surprising that United Capital announced this month a new partnership with Medicare BackOffice for support on all Medicare-related inquiries from United Capital clients. What’s even more notable, though, is that United Capital decided not to simply train up their advisors on Medicare planning, but instead chose to partner with a third-party provider to help clients through the Medicare enrollment and annual review process, allowing each company to maintain its respective focus. Which in turn raises interesting questions about whether the future of Medicare planning amongst financial advisors will eventually be “insourced” – with in-firm advisor expertise and better financial planning and other software tools for support, akin to how advisors have increasingly gone deeper on Social Security planning – or if the future is more of an outsourcing model akin to how financial advisors refer out estate planning, tax accounting, and other more specialized services to third-party providers. Either way, though, the United Capital decision highlights the perceived need and value of Medicare planning itself for retirees as a means to both provide value to clients and differentiate in an increasingly crowded advisor marketplace for retirees.

Morningstar Expands Its Global Risk Modeling Tools In Squeeze Between Between Riskalyze And Aladdin. The success of Riskalyze in turning “risk tolerance” software from a regulatory due diligence compliance requirement into a proactive tool to be used in prospecting for new clients and illustrating risk with existing clients has spawned a spate of competitors in recent years, from Tolerisk and RiskPro and Pocket Risk to Totum Risk and Capital Preferences. Last year, Riskalyze expanded further into ongoing risk modeling by launching Scenarios, its take on interactive stress testing of client portfolios akin to alternatives like Hidden Levers and RiXtrema. And Riskalyze’s pivot into the model marketplace business in 2017 and becoming a technology distribution channel for asset managers, in turn, amplified the then-emerging trend of leveraging advisor technology itself as a distribution channel for investment products. Accordingly, over the past 18 months, Blackrock has been expanding access to Aladdin, its own scenario- and risk-modeling tools for portfolios, to the independent advisor community as a means of leveraging the distribution channel, putting the squeeze on Morningstar’s own positioning as the standard investment portfolio analytics providers for advisors. And now, Morningstar is expanding its own tools in response, with a series of major updates to its “Global Risk Model” tools, including more forward-looking advanced scenario capabilities (e.g., the impact on the portfolio if oil prices spike, or the Fed raises rates, or a trade war emerges) on top of their existing risk analytics launched back in 2016, to fight back against the two-fronts encroachment of Riskalyze coming up the tech chain and Blackrock coming down the asset manager distribution chain. At a minimum, though, the convergence on scenario-based stress-test analyses is an affirmation to early players like Hidden Levers that pioneered the approach in the advisor channel, and emphasizes the way that technology is turning risk tolerance from an abstract measure into a far more concrete way to illustrate and facilitate conversations with clients. In the meantime, Morningstar’s own solution of the software is reportedly still in beta, with a full release available through Morningstar Office Cloud in 2019.

TD Ameritrade Announces “Innovation Quest” Finalists For Its First-Ever Advisor FinTech Competition. Earlier this year, TD Ameritrade announced the launch of its own FinTech competition, dubbed “Innovation Quest,” to support the development of new technology for RIAs, building on the popularity and success of the XYPN FinTech competition it sponsored in 2016, and offering $25,000 to each of 3 finalists (and another $25,000 to the winner), who will have an opportunity to present and compete to be the winning entry at TDA’s annual LINC conference in February of 2019. And now, TD Ameritrade has announced its finalists (from a reported field of a whopping 135 submissions!). The first is Emotomy, a startup that initially competes in the category of “robo-advisor-for-advisors” digital advice platforms (with the usual suite of paperless onboarding, risk tolerance questionnaires, trading tools, and portfolio rebalancing), and has now developed a monitoring tool that tries to identify when client accounts are at risk of leaving (ostensibly based on their engagement behavior with the client portal) to prompt the advisor to engage with clients preemptively and “save” the relationship. The second is iMar Learning Solutions, which submitted a financial literacy application that advisors can use with their clients (or more realistically, with children or other family members of clients). And the third is Dynamic Wealth Solutions, an independent advisory firm that is trying to develop a voice-activated assistant support tool for advisors dubbed “RIA Genie.” Notably, though, Innovation Quest included a somewhat controversial requirement of FinTech entrants – a “right of first negotiation” clause for TD Ameritrade that the companies cannot develop, integrate, license, sell, or be acquired by anyone else without first giving TD Ameritrade the opportunity to do so. On the one hand, TD Ameritrade is still a large enough platform that companies could still potentially have success “just” developing for the RIA base at TD Ameritrade; on the other hand, though, the “right of first negotiation” clause has a huge 4-year time window attached to it, which could eventually limit companies from making a timely pivot away from TD Ameritrade if it proves necessary to do so, and/or limit their access to investor capital from funders that are concerned about being limited to “just” TD Ameritrade’s addressable market and platform viability. At the least, it’s somewhat bizarre for a company that has otherwise been so dedicated to open architecture to require such a closed development agreement for its own FinTech competition.

In the meantime, we’ve updated the latest version of our Financial Advisor FinTech Solutions Map with several new companies, including highlights of the “Category Newcomers” in each area to highlight new FinTech innovation!

So what do you think? Does the shift of asset managers into the Advisor Technology marketplace create problematic new conflicts of interest, or just spur investment into more and better technology solutions? Would you like more and better cash management solutions for clients, or is cash still not worth managing? Were you a user of NerdWallet’s Ask An Advisor or Investopedia’s Advisor Insights, and if so what will you do now? Please share your thoughts in the comments below!

Disclosure: Michael Kitces is a co-founder of XY Planning Network, which was mentioned in this article.

Leave a Reply