Executive Summary

Welcome to the January 2020 issue of the Latest News in Financial Advisor #FinTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors and wealth management!

This month's edition kicks off with the big announcement that Fiserv is spinning off its 'tiny' (at least relative to Fiserv’s banking and payments business) investment services unit, valued at $880M, to a private equity firm focused on aggressively growing Fiserv’s presence in the enterprise ‘WealthTech’ space, positioning the company to become an even more direct competitor for large-broker-dealers and large-RIA enterprises with Envestnet, Fidelity, Morningstar, and Broadridge, in what may spur a heavy reinvestment cycle into more capable enterprise systems for large advisor platforms.

From there, the latest highlights also include a number of other interesting advisor technology announcements, including:

- Invesco acquires RedBlack rebalancing software as asset managers increasingly look to (vertically integrated) model marketplaces as the future of ETF distribution

- Pershing launches its own “Subscribe” fee-based annuity marketplace, integrated directly to its Managed Accounts platform, to compete against Envestnet’s own new Annuity Exchange

- Merrill Lynch abandons the ‘bring your own device’ approach of the 2010s and stakes its compliance oversight in the 2020s on brokers carrying two smartphones (personal and business)

- SEI launches a Developer Portal with new APIs in an attempt to become more of an advisor FinTech platform hub (perhaps eyeing the potential demise of TD Ameritrade’s VEO after the Schwabitrade merger closes?)

Read the analysis about these announcements in this month's column, and a discussion of more trends in advisor technology, including Envestnet announcing new enhancements to PortfolioCenter (and signaling that PortfolioCenter isn’t ‘doomed’ to be deprecated under Envestnet, and may simply become ‘Tamarac Lite” instead), Schwab launches a robo-for-retirement-income offering that overlays tax-sensitive retirement distributions on top of its robo-investments-plus-human-CFPs offering, Investor.com rolls out a new advisor-vetting platform that aims to present consumers aggregated regulatory data to spot relevant disclosures and conflicts, and Vanguard capstones its 2-year battle with TD Ameritrade over pay-to-play access by dropping stock and option trading commissions to $0 (on top of its already-free ETF trading platform) as TD Ameritrade is queued up for a sale.

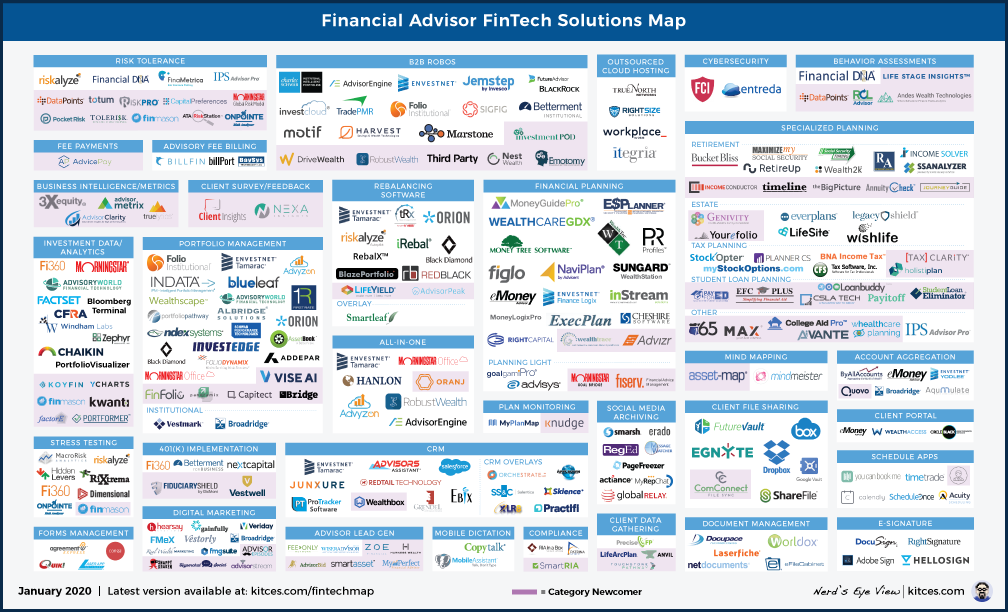

And be certain to read to the end, where we have provided an update to our popular new “Financial Advisor FinTech Solutions Map” as well.

I hope you're continuing to find this column on financial advisor technology to be helpful. Please share your comments at the end and let me know what you think!

*And for #AdvisorTech companies who want to submit their tech announcements for consideration in future issues, please submit to [email protected]!

Fiserv Spins Off Investment Services Unit Selling 60% Stake For $510M To Ramp Up Enterprise WealthTech Solutions. In the world of advisor technology, there are two separate camps of software providers. On the one side are those that sell software predominantly to independent advisors, often on an individual basis, and may then aggregate together multi-advisor firms to sell discounted “enterprise” software. On the other side are those who build first and foremost for enterprises – primarily large broker-dealers along with bank and trust companies – creating not only the software that end advisors use but also the core that the enterprise itself uses to operate (and manage and oversee) its business. In this context, Fiserv is a name not well known to most of the independent advisor community, but is actually one of the largest players in enterprise “WealthTech”, servicing 7 of the 10 largest broker-dealers (and also 9 of the top 12 retail asset managers), including the build for LPL’s ClientWorks platform and Unified Wealth Platform that services 5M accounts and nearly $1.4T in assets. The caveat, though, is that relative to Fiserv’s overall business, which is more heavily in the world of payments and banking, even a very large WealthTech business is a “small” Fiserv unit that must fight for resources within a larger organization. Accordingly, Fiserv announced this month that it is effectively spinning off its Investment Services division, selling a 60% stake to private equity firm Motive Partners for $510M (valuing the Fiserv WealthTech business line at $850M)… a very sizable transaction by AdvisorTech standards (given Fidelity bought eMoney Advisor for $250M in 2015, Envestnet bought MoneyGuidePro for $500M in 2019), though “small” by Fiserv’s scale (with a $79 billion market cap, and having bought credit and debit payment processor First Data in 2019 for $22B). From the advisor perspective, the significance of the Fiserv deal is that what was a ‘small and slow growth’ business under the Fiserv umbrella will now become a standard concern solely and fully focused on its own growth (and its Motive Partners support). Already, Fiserv has indicated it will be putting additional resources into building out its User Experience and expanding its API capabilities for more and deeper enterprise integrations, and last fall (of 2018) Fiserv also announced a new “Financial Advice Management” (i.e., financial-planning-light) solution that will likely see substantial new investment as well (especially given how “hot” financial planning software is as a category, with Morningstar’s recent launch of Goal Bridge and high-flying acquisitions of both MoneyGuidePro and Advizr in 2019). Though again, given Fiserv’s focus on the enterprise market, such solutions may still take years to trickle down to independent advisors. Still, expect to see the spin-off-and-recapitalization of Fiserv’s WealthTech unit (which reportedly will soon be rebranded as well), under the continued command of current President Cheryl Nash, increasingly competing with the likes of Envestnet, Fidelity, Morningstar, and Broadridge in the (independent) broker-dealer and perhaps the large enterprise RIA channel in 2020 and beyond.

Invesco Acquires RedBlack Rebalancing Software As Asset Managers Vertically Integrate FinTech For Model Portfolio Distribution. Back in 2015, Blackrock made waves by acquiring direct-to-consumer robo-advisor FutureAdvisor for a whopping $150M (estimated at the time to be 50X FutureAdvisor’s $3M of revenues), in what many suggested was an early peak hysteria of the robo-advisor movement. However, the reality was that even in 2015, Blackrock was not acquiring FutureAdvisor for its retail revenues, but to re-purpose the technology to automate model portfolios for advisors… with a natural default to use Blackrock’s iShares ETFs. In essence, while the industry debated whether or how many consumers would or would not adopt robo-advisors directly, from the asset manager’s perspective, a “robo-advisor” was really just another distribution channel to plug the asset manager’s products into a centrally managed account solution. Which has led in the subsequent years to a wave of asset managers acquiring robo-advisor-for-advisor or more simply “rebalancing software” for advisors, from Blackrock’s deal with FutureAdvisor (and also taking a big stake in Envestnet and its Tamarac rebalancing platform in 2018), to WisdomTree taking a stake in AdvisorEngine (nee Vanare | Nest Egg), Legg Mason acquiring Financial Guard, UBS investing into SigFig, and Invesco acquiring JemStep. And now, the news is out that Invesco is doubling down on the strategy (as Blackrock did) with another rebalancing software acquisition, buying RedBlack for an undisclosed sum. Notably, though, RedBlack did not have a very large market share in the RIA channel – reportedly only 160 RIAs and relatively flat for years – and the software is still in the process of being migrated from its original desktop/server version into the cloud. However, if Invesco wanted to acquire rebalancing software, there were virtually no alternatives remaining, as the latest Advisor FinTech map shows only Blaze Portfolio and the recent newcomer AdvisorPeak as the only remaining independent rebalancing software solutions, with more than half a dozen alternatives having been acquired or changed hands in the past half dozen years! From a broader perspective, though, Invesco’s acquisition of RedBlack, following on the heels of its recent Portfolio Pathways acquisition (for portfolio accounting and performance reporting, along with its own RebalX solution), and JemStep’s original digital onboarding solution, makes it appear that Invesco is be attempting to cobble together an entire portfolio management solution for advisors, akin to Envestnet’s Tamarac, Orion, Black Diamond, or Morningstar, in yet another bet that the future of asset management distribution is via model marketplaces (facilitated by rebalancing software to manage those models) and that therefore it’s desirable for asset managers to ‘vertically integrate’ their distribution channel by owning the model management rebalancing software itself (as even if the platform otherwise remains ‘open architecture’, there will still be an opportunity for the asset manager owner to make its funds and ETFs the default solutions to be illustrated!). From the advisor perspective, though, the real question is whether asset-manager-owned rebalancers like RedBlack or FutureAdvisor will become increasingly aggressive in pushing their own funds over time, how the ‘independent’ model marketplaces like Oranj (or more recently, 55ip) will gain market share or not, and whether advisors will eventually begin to rebuff ‘traditional’ paid rebalancing solutions like Tamarac, Orion, and Black Diamond if asset managers increasingly make model marketplaces (and the software that powers them) ‘free’ with the goal of monetizing advisors’ investment flows from clients instead?

Pershing Emulates Envestnet By Integrating Fee-Based Annuities Into Its Managed Accounts Platform As Annuities For (Hybrid) RIAs Heat Up. For decades, annuities have been a controversial product, with adherents in the brokerage and insurance channels claiming they provide ‘essential’ benefits in the form of guarantees that consumers (especially risk-averse retirees) want, and critics in the RIA channel claiming that the products are overly expensive and their benefits are simply rationalizations to justify the historically-generous commissions that they paid. The caveat, however, was that even if brokers wanted to sell lower-cost (and lower-commission) annuities, they often didn’t have such products available (and aren’t permitted to ‘choose’ to be lower cost by rebating back any of the commissions to their clients), while RIAs that may have wanted to offer annuities to their clients usually couldn’t get a no-commission version of the product. This blocking point was driven in large part by the perception of annuity companies that RIAs wouldn’t ‘sell’ their products (without any commissions or other compensation to incentivize them in the first place), notwithstanding the fact that companies like Vanguard and DFA have built their success in the advisor channels by not paying advisors compensation to sell their funds but instead trying to offer RIAs a high-quality product that RIAs will ‘want’ to sell in order to get paid advisory fees by their clients instead. Accordingly, annuity companies in recent years have been looking more towards opportunities in the RIA channel, beginning to develop new fee-based annuity products, and recently obtaining a Private Letter Ruling that will allow RIAs to sweep their advisory fees directly from a non-qualified annuity contract (without triggering a taxable distribution). However, the challenge for annuity companies is that even after clearing the can’t-pay-commissions-to-RIAs compensation hurdle, there is still little distribution infrastructure (i.e., wholesalers and marketing) to ‘sell’ no-commission annuities to advisors. Which is why it was so significant in mid-2019 when Envestnet announced the launch of their Annuity Exchange, a marketplace of fee-based annuity contracts that would allow RIAs (using Envestnet) one centralized platform through which they can find and purchase annuities for their clients (and for which Envestnet can be paid by annuity companies as a distribution partner). And now with interest in fee-based annuities for RIAs (and hybrid RIAs) heating up, now Pershing is announcing their own integration of a fee-based annuity platform (dubbed “Subscribe”) into their Managed Accounts platform, similarly allowing advisors on their platform to purchase and integrate no-commission annuities into their clients’ retirement portfolios. The significance of this announcement is not merely the fee-based annuity channel itself, but the way that annuity carriers seem to be pushing for RIA custodial and technology platforms to be the epicenter of their RIA distribution strategy, in a world where “FinTech” itself has become a distribution channel to reach advisors. Which also allows those annuity carriers to rely on their FinTech intermediaries to develop the missing technology infrastructure to support annuity contracts (e.g., coordinated trading between annuity contracts and the rest of the advisor’s client accounts, coordinated billing across all accounts in a client’s household with household-level graduated fee schedules, account opening and trading at firm-wide scale for large RIAs, and reporting systems to monitor annuity guarantees as a ‘value’ on client performance reports). From the strategy perspective, though, the most astonishing thing about the shift of an RIA (and broker-dealer) custodial platform like Pershing into the annuity exchange business is that, for years, industry commentators have wondered and mused when and whether Envestnet would try to get into the custody and clearing business, or whether it would remain satisfied being the technology and distribution layer on top of those platforms; now, however, it appears that while Envestnet is not looking to go into the custody and clearing business, more and more RIA custodian and broker-dealer clearing platforms may be looking to go into the RIA technology distribution business in the coming years instead?

SEI Announces Developer Portal As Schwabitrade Merger Raises FinTech Community Concerns About The Future Of TD Ameritrade’s VEO. While creating a product or service that customers will love is always challenging, one of the unique challenges in trying to build a successful advisor FinTech solution is the difficulty in distributing the software to advisors, in a world where it’s very time- and cost-inefficient to sell licenses to independent advisory firms one at a time, but trying to establish enough credibility to get on the radar screen of large enterprises can be even harder. In practice, most FinTech startups end out building an initial solution for independent advisors (particularly in the RIA community, where the firm owner is the Chief Compliance Officer making the decision and the advisor who will use it) to gain traction and demonstrate proof of concept and an initial product-market fit, and then pivot to enterprises to scale. Which still raises the question about the best go-to-market strategy to reach those independent advisors? For the past decade, the nearly universal answer has been: build an integration to TD Ameritrade’s VEO, whose Open Access platform that can be quickly and easily integrated to became the de facto launch strategy for most FinTech startups of the 2010s (while Schwab and Fidelity started the decade with very closed systems, and have become somewhat more ‘open’ in recent years but still often have multi-year wait lists for startups to get onto their integration roadmap). Which, in practice, was a tremendous boon to TD Ameritrade as well, attracting a disproportionate amount of advisor FinTech innovation without needing to do its own development, by simply being the most innovation-friendly open-architecture platform. Yet with the recent announcement that Schwab is looking to acquire TD Ameritrade – which has already raised concerns amongst small RIAs about whether Schwab will continue to service them, and broader concerns about whether it is too much concentration of RIA custodian market share even for larger firms – the key question in the advisor FinTech community is: will Schwab continue to maintain VEO Open Access, or eventually migrate TDA’s technology to Schwab’s much-longer-integration-roadmap OpenView Gateway instead? And if TD Ameritrade’s VEO is wound down… how will the next generation of Advisor FinTech startups go to market in the 2020s? Perhaps sensing the palpable fears amongst FinTech innovators, mega-TAMP SEI announced this month the launch of its own SEI Developer Portal to offer a wide suite of APIs for independent FinTech companies to build directly to SEI’s software (and its base of $335B of AUM, another $662B of AUA, and thousands upon thousands of financial advisors). Notably, SEI’s platform has historically has had more depth in broker-dealer channels than amongst independent RIAs – which means even building to SEI’s platform for FinTech distribution may still entail the challenging subsequent step of broker-dealer enterprise Due Diligence vetting that is difficult for FinTech startups. Nonetheless, with ambiguity emerging about the future of TD Ameritrade’s VEO in the face of the potential Schwabitrade merger, competing advisor platforms appear to be very interested in getting more of a crack at the front edge of FinTech innovation in the 2020s.

Despite Fears Of Its Post-Acquisition Demise, Envestnet Ramps Up PortfolioCenter With New Enhancements And Hosted Solution. When Envesnet acquired PortfolioCenter from Schwab last February for what was reportedly a ‘nominal’ amount, the fear amongst the industry was that Envestnet had simply acquired PortfolioCenter to ‘kill’ it and force the migration of PortfolioCenter users to its competing Tamarac platform. Yet the reality is that Tamarac itself is a portfolio performance reporting and trading platform built on top of PortfolioCenter… such that Envestnet ‘has to’ maintain the system and support the users, if only to support its own Tamarac users (which were estimated to be approximately 1,000 of the total 3,000 PortfolioCenter users at the time of purchase). In fact, Schwab was arguably doing PortfolioCenter users a ‘favor’ by selling the platform to Envestnet, which had far more incentive to actually support, maintain, and continue to enhance Portfolio is only for its own Tamarac capabilities. And sure enough, this month Envestnet announced the first series of new enhancements to PortfolioCenter, from how the system handles account transfers (now able to execute bulk transfers between accounts), to more sophisticated permissioning when doing data exports (allowing key account details to be masked when an assistant or external provider facilitates), to new summary reports to oversee the billing process and spot anomalies and errors in advance. Ultimately, none of the new enhancements are major features to attract new growth for PortfolioCenter – they are simply administrative enhancements – but that’s also the point: that Envestnet is putting resources towards enhancements that are valuable and relevant to existing users, rather than trying to wind PortfolioCenter down and force its users to Tamarac. In fact, Envestnet separately announced in November the launch of a new PortfolioCenter Hosted solution for ‘emerging’ RIAs, allowing newer RIAs to buy PortfolioCenter, have it hosted by Envestnet (though advisors ‘retain control’ over data reconciliation)… and then have the option to “seamlessly upgrade to industry-leading Tamarac Reporting, Trading, and CRM. In other words, it appears that Envestnet’s strategy for PortfolioCenter going forward is not to decommission the platform – given that it remains the chassis for Tamarac itself – but instead to offer PortfolioCenter as a basic ‘Tamarac Lite’ portfolio performance reporting solution which can then be upgraded to Tamarac’s more sophisticated reporting, trading, and other. Which means there may be a day that the separate PortfolioCenter name and brand are retired… but PortfolioCenter itself appears to be very much part of Envestnet’s longer-term future (a likely relief to PortfolioCenter users who feared whether Envestnet would shut it down), and will likely see more proactive development at Envestnet (if only because Envestnet wants those features for Tamarac) than Schwab itself was investing in PortfolioCenter in recent years?

InvestCloud Launches ‘Open CRM’ Solution To Compete Against Salesforce By Better Managing Unstructured Data For Large RIA Enterprises. When it comes to CRM systems for financial advisors, the marketplace is extremely bifurcated, with the ‘small’ end of the marketplace dominated by Wealthbox and Redtail, mid-sized firms primarily using Redtail or Junxure, and the largest firms primarily using Salesforce or Tamarac (built on Microsoft Dynamics). To some extent, these dividing lines are based on pricing (with smaller firms opting for solutions with less expensive price entry points, and larger firms being willing to pay more), but also speak heavily to required features, where smaller advisors tend to use their CRM system primarily as a ‘digital rolodex’, tracking a sales pipeline, and capturing client communication, while larger firms tend to use their CRM more as a centralized data hub for business management and reporting of the firm’s key performance indicators and financial metrics. Unfortunately, though, even the large-firm CRM systems generally only take in data from established industry vendors (via their integrations), leading to a plethora of structured data about their investment portfolios but remarkably little about the clients themselves (e.g., their social media feeds and what they’re otherwise sharing and communicating openly to the world, that their financial advisors still may not be seeing). To fill the void, InvestCloud – which makes a wide range of performance reporting, trading, and other ‘WealthTech’ apps through its InvestCloud hub – has announced a new “Open CRM” offering, aiming to compete against Salesforce (and Microsoft Dynamics) for large RIAs by doing a better job melding together a firm’s structured investment data with the ‘unstructured data’ of social media feeds (and potentially other outside data sources in the future). On the one hand, there’s arguably a lot to be said for InvestCloud’s new CRM focus, as the overwhelming majority of an advisory firm’s clients are ongoing clients for whom an ongoing relationship needs to be nurtured, where shared information on social media channels and elsewhere is absolutely relevant, and most CRM systems are still disproportionately focused on just the upfront client acquisition (i.e., sales) process in the first few months of the relationship (and not the 30 years of client relationship that may follow). On the other hand, the demand on advisor CRM systems themselves are becoming increasingly complex, not only to move beyond the ‘digital rolodex and into big data’ domain (as InvestCloud’s Open CRM aims to do), but also into the world of workflow management and business process automation… which in turn relies even more on deep domain-specific integrations to execute multi-system workflows. Which raises the question of whether InvestCloud starting ‘from scratch’, particularly in the large enterprise domain where workflow automation demands are most intense, can effectively build ‘everything’ an advisory firms needs to have its CRM drive its business processes on top of the big data capabilities it is offering… or if instead OpenCRM might itself may become an overlay of client enrichment data on top of a large enterprise workflow engine like Salesforce. Nonetheless, given the extent to which most CRM systems remain primarily about upfront sales and not ongoing relationships, there is arguably still a lot of room for competition in the world of advisor CRM!

Trizic Rebrands To ‘Harvest’ Alongside $12M Of Venture Capital To Scale Up Robo-For-Advisors In The Bank Channel. Despite their original hype, growth of most robo-advisors has been lackluster, generally a result of the difficulty in scalably acquiring enough small-dollar-amount clients in sufficient volume. These challenges in client acquisition led many robo-advisors to pivot and become robo-advisors-for-advisors solutions instead… with the caveat that independent advisors aren’t any better at getting Millennial or other clients scalably, either (and may actually be worse), while many also don’t necessarily want to introduce a new layer of potentially-costly technology on top of what they already use to service their existing clients with their broker-dealer or RIA custodian. However, when it comes to banks, the dynamics of potential ‘robo-advice’ solutions are different, as banks already have a substantial base of existing customers (to whom robo-advisor investment solutions can be cross-sold to expand wallet share), and often don’t have any investment infrastructure in place to begin with (which makes robo-advice platforms additive and not redundant). Accordingly, while robo-advisor-for-advisors solutions have largely struggled with independent advisors, Trizic – one of the early robo-for-advisors players that had a vision from the start of robo opportunities in the bank channel – is gaining traction with banks, signing on 18 bank clients since early 2018 along with 30 other non-bank customers (e.g., large RIAs and independent broker-dealers). And now, Trizic is rebranding to Harvest, and raising $12M in venture capital (on top of a $15M line of credit) to follow up on its $10M capital round last year with a vision of 1,000 banks in 5 years, in large part through a partnership with FIS (which whom CEO Drew Sievers has a relationship as FIS acquired his prior company mFoundry). Ironically, the success of direct-to-consumer robo-advisors like Betterment or Schwab Intelligent Portfolios – or even competing small-account brokerage solutions like Robinhood and Acorns – is that from the bank perspective, those are competitors that not only siphon off investable dollars, but increasingly are competing with banks for the cash that powers their core lending business as well. Which increases both the stakes and the opportunity for banks to deploy such investment solutions directly to their existing bank customers, from the ability to charge for the investment service, to being able to better capture (or retain) net interest margin profitability on customer cash. In addition, the fact that banks themselves are already engaged with their customers on smartphones – via various mobile banking apps – and have been trying to train their bank customers to work primarily through apps (and not human customer service representatives), makes various mobile-based “robo” solutions a natural fit for their existing user experience, further enhancing the adoption potential. All of which means that, while robo-advisors-for-advisors have continued to languish as a platform for independent advisors, the outlook is positive for Harvest to expand its growth in the bank channel.

Schwab Launches ‘Robo For Retirement Income’ To Replicate Advisor Value-Add For Tax-Sensitive Retirement Distribution Planning. As technology increasingly commoditizes the process of allocating and implementing a diversified investment portfolio, financial advisors have increasingly justified their value proposition in being able to service clients’ financial planning needs beyond ‘just’ the portfolio itself. After all, it’s one thing to asset-allocate the portfolio of an accumulator who is making ongoing contributions with a long open-ended time horizon to retirement; it’s another to figure out the most tax-efficient way to generate cash flows in retirement, which entails not only managing the transaction costs of liquidations themselves, the sequence of return risk in what should be liquidated when, the tax consequences of those distributions, and how to sequence the distributions from amongst various types of accounts (e.g., taxable, tax-deferred, and Roth-style tax-free accounts). Yet ultimately, taking tax-sensitive retirement withdrawals to create a “retirement paycheck” boils down to a series of ‘rules’ that most advisors follow regarding which accounts to draw from first, how to handle capital gains and RMDs, and a system to decide which assets to liquidate in up markets and down markets. In other words, the mechanics of retirement liquidation planning are fairly conducive to creating algorithms to determine how to generate liquidations from any particular client scenario. And now, that’s exactly what Schwab has done, in the launch of its new “Schwab Intelligent Income” robo-for-retirement-income solution coming in January, which will help clients figure out how much they can withdraw (or how long their planned withdrawals will last), and then facilitate generating those ongoing retirement distributions in a ‘tax-sensitive’ manner. Notably, Schwab Intelligent Income will not have a separate platform fee, though; instead, it is part of the Schwab Intelligent Portfolio Premium solution, which costs $30/month plus a one-time $300 upfront planning fee, and provides access to a CFP certificant in addition to the investment solution itself. Which means in essence, it’s simply a retirement service to be facilitated by the human CFP professionals that Schwab is already offering as part of its “premium” Intelligent Portfolios service. On the one hand, advisors may perceive this as one of the most direct threats yet in Schwab’s ‘channel conflict’ between retail and advisors, delving even further into the core value proposition that independent financial advisors offer mass affluent clients. On the other hand, robo-advisors like Personal Capital and Betterment have already rolled out their own Retirement Income solutions in recent years, and arguably true ‘retirement specialization’ of financial advisors has already been going deeper than just retirement withdrawal strategies, from coordinating the timing of Social Security payments, to planning around the costs of aging itself (e.g., whether to move into a Continuing Care Retirement Community or make home modifications), assessing Medicare and long-term care insurance, and more. And some retirees will have more complexity and planning opportunities than others, while advisors can remain on the ‘cutting’ edge with more proactive tax strategies (e.g., doing partial Roth conversions during retirement to optimize tax brackets across the retirement years). Nonetheless, the new Schwab Intelligent Income solution marks a notable turning point in the evolution of ‘robo-advisor’ competition from major brands like Schwab, given the extent to which it is delving beyond mere portfolio management alone, and that it is no longer ‘just’ about Millennials and the accumulation phase of the portfolio. Ultimately, the reality is still that consumers who really want to just delegate the retirement income planning process will likely still choose an advisor over the responsibility of trying to pick (and then be responsible for monitoring) a ‘self-directed’ solution like Schwab Intelligent Income, though with Schwab’s own recent consumer survey finding 73% of pre-retirees are comfortable using technology to manage their retirement income, and bundling the service in with their own human-CFP offering, the line between where a ‘robo-advisor’ ends and highly-scaled-technology-augmenting human advice begins is getting blurrier and blurrier.

Trust And Will Raises $6M Series A To Digitize Creation Of Estate Planning Documents And Partner With Advisors. The Economic Growth and Tax Relief Reconciliation Act (EGTRRA) of 2001 started the process of lifting the Federal estate tax exemption from the then-$675,000 threshold to $3.5M in 2009, which in turn became $5M in 2011 (after a 1-year repeal in 2010), indexed further for inflation, and was doubled again under the Tax Cuts and Jobs Act (TCJA) of 2017, culminating in a Federal estate tax exemption of $11.58M in 2020, a 17X increase that has cut the number of Federal estate tax filings by more than 95% in 20 years. In addition, EGTRRA also repealed the then-existing state estate tax credit and replaced it with a state estate tax deduction, effectively decoupling the Federal estate tax from state estate taxes and leading to a wave of states that subsequent repealed their own state estate taxes due to a lack of resources to enforce state-specific rules on their own. The significance of this, beyond simply the reduction in estate tax exposure itself, is that it drastically cut the demand for obtaining estate planning documents, as while the reality is that everyone should have a proper Will or trust in place to ensure the proper distribution of assets after death, in practice, there was nothing like “do this estate planning or you’ll face hundreds of thousands of dollars or more in estate taxes” to get people to actually do their estate planning. As a result, the marketplace for estate planning attorneys has greatly diminished over the past decade, and the few that remain have increasingly focused on the ever-narrower segment of ultra-HNW clients where estate planning is still complex enough to be a lucrative career for lawyers… and making it harder and harder for advisors to have a place to send clients who want to help their clients get their estate planning done if they have relatively ‘simple’ estate planning needs. Filling the void in the interim has been solutions like LegalZoom, though the platform doesn’t specialize in estate planning in particular and doesn’t have tools for advisors to ‘support’ the process as non-lawyer financial advisors working with their clients. Which has opened the door for new EstateTech upstart Trust And Will, which recently raised $6M in Series A funding to not only scale their direct-to-consumer LegalZoom-for-Trusts-And-Wills competitor, but is also building out a “Trust & Will For Advisors” solution that will aim to connect independent financial advisors with T&W’s own in-house lawyers through their estate planning platform. In other words, Trust & Will is not aiming to simply automate self-prepared documents – akin to LegalZoom – but to create a technology-expedited process for drafting estate planning documents… which makes it feasible both to work with consumers directly, and in partnership with advisors. Of course, from the industry perspective, diminished exposure to estate taxes has reduced how much financial planning software (and many advisors) focus on estate planning at all, beyond simply recommending that clients go get estate planning documents ‘somewhere’. But given the lack of available advisor-supported solution elsewhere, arguably Trust & Will is coming to the advisor market at the right time to scale its technology-enabled human lawyers partnership model to facilitate more client estate planning for the essential documents that every client needs?

Merrill Lynch Moves Away From Bring-Your-Own-Device And Issues 14,000 Corporate Smartphones. In the 1990s when mobile communication devices first appeared in the form of pagers, those who had to carry such devices for work would use corporate-issued pagers (as they really had little relevance for personal use). In turn, when pagers became more ‘sophisticated’ and email-accessible with the rise of the BlackBerry in the 2000s, most devices were still corporate-issued, as few had any need for “on the go” email access outside of business uses. However, when smartphones came on the scene in the 2010s, and suddenly the average person had their own for personal use – and little interest in carrying a second for-business-only device – businesses largely shifted to software platforms (e.g., Microsoft or G Suite) that could facilitate anyone using their own personal device to access “work” email and files (as the device was really just a portal to cloud-stored files or messages). The caveat of the Bring-Your-Own-Device (BYOD) approach is that it was especially challenging with respect to compliance for financial services firms, which have an obligation to oversee written communication and often want to document any/all communication, including text messages and phone calls as well. Except when text messaging and phone calls occur from a personal phone, anchored to a personal phone number (as most smartphones are not built with hardware and software to handle separate business and personal phone numbers to a single device), it gets especially difficult to track and archive “business” communication without unwittingly capturing “personal” communication as well (which most employees don’t want to share with their compliance department!). In this context, it is notable that major wirehouse Merrill Lynch announced in December a new business phone policy for all of its 14,000+ brokers… that they begin to carry two devices, and use a corporate-issued smartphone (either an Apple iPhone 11, the iPhone XR, or the Samsung S10e) for all their business communication (with Merrill paying for both the devices and the monthly plans), effectively throwing in the towel on trying to monitor and extract business communications from personal devices. From the corporate perspective, issuing and requiring two separate devices greatly simplifies the compliance oversight process, as Merrill can (and ostensibly would) have full access to ‘everything’ that happens on the device (which would/should only be used for business purposes). From the personal perspective, the obvious hassle will be the obligation for 14,000+ Merrill brokers to carry two smartphones (personal and business) from now on. Still, though, when a firm as large as Merrill Lynch can’t develop a viable alternative to smartphone monitoring for phone calls and text messages even more than a decade after smartphones arrived on the scene, it raises the question of whether the shift back to carrying a separate business devices may become increasingly common in the 2020s (as it was in the 2000s and 1990s) and the era of “everything on one [personal] smartphone” may have just been a temporary phase of the 2010s?

Investor.com Rolls Out New “Trusted Advisor” Service For Consumers To Find An Advisor. The ongoing rise of the internet has fundamentally changed the way consumers buy products and services, shifting what was once either a Yellow Pages “listing” approach (show all the available vendors in the local area, that the consumer must then contact and vet) or a referral approach (ask someone you know who they know and recommend, to avoid the time-consuming vetting process), into a platform where consumers can both look up who the available providers are and who can be trusted to provide a quality good or service. Especially since as it stands today, government-provided platforms like FINRA BrokerCheck and the Investment Adviser Public Disclosure (IAPD) are not very user-friendly, nor are the advisors listed there indexed by search engines, which is what originally opened the door to platforms like BrightScope to aggregate together the siloed and hard-to-search regulator data into a single centralized platform. Yet with BrightScope sold (primarily for its 401(k) business), the opportunity remains for a platform to aggregate together all the various regulatory data to help consumers figure out who is really a ‘trusted advisor’ or not… and then monetize the interest by selling those leads to advisory firms. In this context, a new platform dubbed Investor.com has recently launched with the goal becoming the site for consumers to vet advisors, rolling out its own proprietary “Trust Algorithm” that scans regulatory data for disputes and disclosures and assigning advisors who pass their qualifications a “trust badge”. Notably, Investor.com has a particular focus on the advisor’s fiduciary obligation, and as a result, “0% of broker-only registrants are labeled ‘trusted’” (and only 75% of investment adviser representatives earn their ‘trusted’ designation), in addition to weighing data points on a long list of conflicts of interest (from receiving 12b-1 fees or insurance compensation, proprietary investments to soft dollars) and actual disciplinary history. Ultimately, Investor.com aims to monetize the business in a similar manner to how BrightScope did – by allowing advisors to “Verify” their profile for $185/advisor (or $999/firm), which in turn lets them further customize the profile with their logo, website, and contact information (and while Investor.com notes that Verifying a profile doesn’t impact its Trust Score, it obviously hopes that advisors will want to claim and update the information on their profiles simply to make the pages convert better into actual prospects). Ultimately, it remains to be seen whether a third-party site like Investor.com can really build consumer traffic to their ‘Find An Advisor’ platform the way that lead generation competitors like Zoe Financial, SmartAsset, and FeeOnlyNetwork have, especially since they lack the more ‘niche’ oriented attraction for consumers like CFP Board’s Find A CFP Professional, NAPFA’s Fee-Only Advisor Search, Garrett Planning Network’s hourly advisor search, or XY Planning Network’s advisor-for-Gen-X-or-Millennial search. Nonetheless, with advisors increasingly struggling to grow, there is arguably more opportunity than ever for lead-generation sites that can actually convert prospects. And from the consumer perspective, the increasingly disclosure-oriented approach of regulators, across multiple different regulatory channels that advisors may be registered under, arguably has created a real need and opportunity for some platform to weave it all together for the sake of consumers themselves… as Investor.com is at least trying to do!

How A Spurned Vanguard Triggered The Drop To Zero Commissions And May Spawn The Next Wave Of Advisor FinTech Innovation. When Vanguard kicked off the New Year with an announcement that it was cutting the trading commissions on stocks and options to $0 on its brokerage platform, there was little chatter in the industry about what was largely seen as a perfunctory ‘we can check that box, too’ move by Vanguard to match the industry shift to ‘ZeroCom’ that happened in a wave this fall in response to Schwab’s high-profile move to do so. Especially since Vanguard already offered its mutual funds and virtually all ETFs on a ZeroCom basis, and it’s mutual funds and ETFs – not individual stock and option trading – that Vanguard is known for (and the kinds of investor preferences it tends to attract). Yet from the broader industry perspective, Vanguard’s own move to ZeroCom marks the capstone of a tumultuous 2-year transition that Vanguard itself largely precipitated. The starting point was in the fall of 2017 when TD Ameritrade abruptly booted most of the Vanguard ETFs from its No-Transaction-Fee (NTF) platform in lieu of State Street ETFs (after what was reportedly an unwillingness of Vanguard to pony up same NTF platform pay-to-play access fees that State Street would), which in turn caused Vanguard to respond a few months later in the summer of 2018 by making virtually all ETFs (not just its own or those of ETF providers willing to pay-to-play) free of any trading fees on its brokerage platform, led Schwab, Fidelity, and others to continuously expand their NTF ETF platforms in response with more and more free offerings, until eventually this fall Schwab (and soon the others) threw in the competitive towel and just made all ETFs (and stocks, and options) free of trading commissions. The irony of this progression is that it was TD Ameritrade who precipitated it by requiring Vanguard to pay up, and the Vanguard response to TD Ameritrade triggered an industry shift to ZeroCom that so collapsed TD Ameritrade’s own revenue that it led to the company’s own demise with a sale to Schwab! From the asset manager perspective, though, the significance of ZeroCom isn’t just that consumers can buy their funds for less, but that the elimination of trading commissions also eliminates the ability of RIA custodians to offer preferential pricing to those who pay (and less preferential trading commissions to asset managers who won’t, as was done in the past to DFA and Vanguard). However, in practice, asset managers do still have dollars allocated to pay for distribution, and the shift to ZeroCom itself is now shifting how those dollars are being spent, spurring a rise in various ‘model marketplaces’ as asset managers pay rebalancing and trading platforms in revenue-sharing dollars for assets that flow into their models (which are typically comprised at least in part by the asset manager’s own underlying ETFs or mutual funds). From the Advisor FinTech perspective, this shift is significant, because it is both triggering a wave of ‘free’ rebalancing software solutions like Oranj (that are aiming to only generate revenue from the model providers), and an acquisition frenzy of rebalancing software and ‘robo-for-advisors’ platforms that can serve as model portfolio distribution channels… but also a growing number of successful Advisor FinTech sales and exits, that in turn is spurring a new wave of venture capital and investment dollars into Advisor FinTech that is increasingly being shown as a viable and valuable market unto itself. Which means in the long run, the legacy of the shift to ZeroCom may not just be the reduced costs to consumers, and a more levelized playing field for asset managers, but also the wave the economics of asset management distribution began to flow into Advisor FinTech business models and investment opportunities. Which on the one hand, may spur a fresh new wave of Advisor FinTech innovation in the 2020s, at lower and lower costs (subsidized by the economics of investment product distribution)… but on the other hand, will raise a new series of questions and concerns for advisors vetting their FinTech platforms in the 2020s of whether their vendors’ business models are too conflicted to provide the software that advisors actually want and need (and not just what asset managers want to see sold for their own product distribution needs)?

In the meantime, we’ve updated the latest version of our Financial Advisor FinTech Solutions Map with several new companies, including highlights of the “Category Newcomers” in each area to highlight new FinTech innovation!

So what do you think? Can Investor.com actually attract enough consumer attention to help consumers figure out which advisors to trust? Will Fiserv be able to compete against and pick up enterprise market share from the likes of Envestnet and Fidelity? Is it worthwhile to stay with PortfolioCenter now that Envestnet is investing resources to enhance it further? And will FinTech companies really start building first to alternative platforms like SEI with the future of TD Ameritrade’s VEO now uncertain?

Disclosure: Michael Kitces is a co-founder of XY Planning Network, which was mentioned in this article.