Executive Summary

The essence of a unique value proposition is to answer the consumer question “what is it the value that you offer, and why should I buy it from you?” In other words, what is it that you uniquely do that can’t be gotten anywhere else, unless doing business with you? In an increasingly competitive advisory firm environment, having a clearly defined unique (and compelling!) value proposition is essential to getting clients to do business with you and not someone else.

Yet in a recent new study on advisor value propositions, Pershing Advisor Solutions finds that in reality, most advisor value propositions are not actually all that unique, nor are they necessarily delivered in a very compelling manner. Instead, advisor value propositions are rife with industry-specific jargon, and what are apparently intended as “differentiators” often describe what are little more than “table stakes” – the minimum required just to have a seat at the table and be considered a potential solution at all, but certainly not a unique and differentiated one that helps the advisor stand out from the competition.

In the past, providing customized, individualized advice solutions specific to client needs form a trusted, experienced, credentialed advisor may have been an effective way to stand out in a competitive landscape filled with “stockbrokers” and “insurance agents”. But going forward, the Pershing study results highlight that not only do advisors need to better describe the value they do provide, but they will also need to more clearly focus on how they can truly differentiate themselves beyond the minimum table stakes, whether it’s by delivering a genuinely unique client experience, providing services and solutions that really cannot be found elsewhere, or simply focusing in on a particular type of clientele that allows the firm to go deeper in its services and solutions than what any generalist can match.

From A Unique Value Proposition (UVP) To Advisor Table Stakes

In a new study entitled “What Do Top Advisors Say And What Do Investors Really Think?”, Pershing Advisor Solutions commissioned a team of “textologists” to harvest the description of advisor value propositions from the websites of the advisors listed in the Barrons Top 100 Independent Wealth Advisors list. After harvesting from the “Our Philosophy”, “Mission”, “Approach” and similar pages of 84 advisory firm websites, the team arrived at a list of the phrases and statements that advisors most commonly use to describe themselves. As the study summarized in the Word Cloud below, the most popular phrases included “Develop a solution that meets your needs”, “deliver investment management tailored to the individual” and “act in the best interests of clients”.

Source: What Do Top Advisors Say and What Do Investors Really Think? by Pershing

To evaluate how effectively advisors are actually meeting the wants and desires of high-net-worth investors, the Pershing study also worked with Harris Poll to interview 600 high-net-worth (above $1M in investable assets) individuals and ask them to share what value propositions they thought were most important, along with asking them to assess the relative importance from a list of potential value propositions. The conclusions? Consumers wanted an advisor who will “tailor solutions to meet their needs”, “work in their best interests”, and who are “experienced investment managers”.

Notably, the good news of the results from the Pershing study is that leading advisors actually are highlighting the value propositions that are most important to the consumers they’re trying to reach. The bad news, however, is that virtually all the advisors highlighted these value propositions, and most focused on little else (except for a few other commonly-cited attributes, like being independent, and giving personal/individual service) … which means while advisors may be describing relevant value propositions, they’re not describing anything unique enough to differentiate themselves from each other!

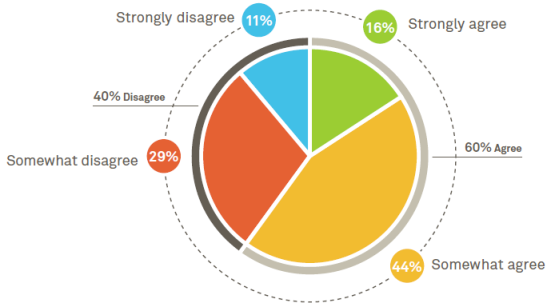

In fact, given that most of the value propositions advisors are actually using are now viewed as the just minimum expected standard from consumers – in essence, the “table stakes” just required to have a seat at the table in the first place – the results of the study paradoxically shows that advisors are doing a good job meeting consumer expectations about their value… and a terrible job explaining how their version is unique from anyone else’s! In fact, the results found that 60% of investors have difficulty distinguishing between advisors at all!

Source: What Do Top Advisors Say and What Do Investors Really Think? by Pershing

Good And Bad Words To Describe An Advisor’s (Unique) Value Proposition

Notwithstanding the similarity in the list of (unique) value propositions that Pershing found advisors commonly use to describe themselves, the study also took a deeper look at the particular words used to describe those value propositions and found some notable trends.

The first was that all else being equal, “plain beats fancy” when it comes to words of choice. For instance, consumers showed a very strong preference for the term “comprehensive” over alternatives like “holistic” or “expansive” or “360 degree view”.

The second theme was that emotionally charged words connected especially well with consumers. For instance, “unwavering” was preferable to “committed”, and similarly being “passionate” was strongly preferred over simply being “dedicated” to clients.

The third key was to avoid jargon, and to recognize that highly charged words within the industry do not necessarily have resonance with consumers. For instance, the popular “fee-only” term from the investor perspective was viewed as interchangeable with the label “no commissions”, and similarly the work “fiduciary” was actually very slightly less favored than the simpler word advocate. As noted earlier, a value proposition that communicates the advisor “acts in the best interests of clients” is a desired message from consumers; the point is not that fee-only and fiduciary are necessarily bad words, but simply that specialized words like fee-only and fiduciary to advisors may not be particularly effective marketing and their significance is lost on consumers relative to other similarly-descriptive-but-less-industry-specific alternatives.

Given these details, and their analysis of what kinds of value propositions were best received by investors, Pershing’s suggested “recipe” for formulating an effective value proposition is to capture the following four elements:

- Attributes. Characteristics of the advisor, such as the firm’s size or years of experience.

- Benefits. What the investor gains as a result of working with the advisor.

- Reason. A rational explanation of how the firm’s attributes produce the benefits for the client.

- Emotion. Language that evokes a feeling.

For instance, “effective” value proposition statements found from the Pershing study via some advisor websites included:

- We built our firm on integrity and trust, because doing what is right for you is better for our business in the long run.

- We are accountable to our clients—we say what we do, and do what we say

The key point: it’s not enough to just say “trust me” to clients (or use jargoned words or phrases like “we’re fiduciaries” alone to communicate it); instead, an effective value proposition must connect together the advisor attribute, the benefit for the client, the reason they’re connected, and done in a manner that can evoke an emotional connection or response.

What Does It Take For An Advisor Value Proposition To Actually Be Unique?

While the Pershing study focused on what kinds of key value propositions high-net-worth investors want to see, as well as the wording that is preferred (or not), applying these insights still does little more than show advisors how to communicate the “table stakes” aspect of a value proposition – the essential stuff that consumers have to hear and want to hear to work with any advisor, but not necessarily what they need to hear to work with a particular advisor. The latter requires a value proposition that doesn't just communicate the essentials in an effective manner, but one that differentiates the advisor and shows what is unique, too.

Ultimately, it seems the key to advisors truly differentiating is either to provide a far more specialized and unique service, or provide it to a far more specific and unique clientele. Even the Pershing study notes that not all value propositions are received similarly by all consumers; for instance, younger investors and those with a very high net worth value messaging about “simplicity”, but the study found affluent retirees do not necessarily appreciate simplicity (instead, the study suggests that they may have already accepted a level of complexity in their lives that cannot be entirely delegated or dismissed). Similarly, even “common” terms can reflected nuanced differences in clientele; for instance, an advisor’s focus on capital preservation and income will attract clients with a lower risk tolerance, while offering to help clients with “leaving a legacy” appeals more to those with children than without.

Arguably, though, a deeper and more substantive differentiation will require an even more specialized focus. Whether it’s working with doctors, or entrepreneurs, or upwardly mobile professional women, or teachers, or new parents, or Gen Y, moving towards serving a particular niche clientele – and then crafting a deeper, more specialized set of truly-client-centric services to deliver to them – the more narrowly defined the clientele are, the easier it is for an advisor to differentiate themselves from the competition. The end point – the advisor may talk to fewer prospects (by narrowing the potential clients to work with), but is more differentiated and more able to turn those prospects into clients.

Nonetheless, as the Pershing study highlights, even a focus on a particular niche doesn’t excuse the crucial need to communicate about the “table stakes” as well, from offering customized individualized solutions to meet client needs, the experience/capabilities of the advisor, and acting in the best interests of the client. In fact, the study’s results especially note that notwithstanding the rising focus on the fiduciary duty within the industry, advisors may still not be doing enough to establish trust with clientele (which requires more than just saying one is a fiduciary!) and communicating it effectively with language that is compelling without being complex and jargoned.

The bottom line, though, is simply this: what it takes to be compelling to prospective clients in today’s increasingly complex world requires going beyond simply the focus on being an experienced, credentialed advisor that provides customized, individuals personal financial advice and solutions to meet the needs of the client. While that may have been sufficient in the past decade or two, what was once a unique differentiator has now become the mere minimum table stakes required to have a seat at the competitive table, and it requires a deeper, more specialized focus from there to truly differentiate in the eyes of today’s advice-seeking (high-net-worth) client!

In the meantime, for those who wish to read a full copy of Pershing's "What Do Top Advisors Say And What Do Investors Really Think?" study, you can download a copy here.

Excellent article! In support of this articles material, I highly recommend Stephen Wershing’s book “Stop Asking for Referrals” to assist advisors in developing and communicating their niche to existing and potential clients. In fact, I think I heard about this book from Michael.

If you are looking for ways to differentiate, you have to find ways to make deeper connections with people. It’s not just about performance at the lowest fee with transparency anymore. There’s a type of differentiation that is rapidly growing. 90% of HNW and UHNW investors are now demanding it and they stay committed to it for longer. Younger generations want it on a wide scale, too. To find out what I’m talking about, go to @PJ_OConnor on Twitter. I tweet about this a lot. Advisors who go this route now could see rapid AUM growth in the years ahead.