Executive Summary

Philosophically, financial advisors can have quite polarized viewpoints when it comes to the relative importance of protection and accumulation benefits of life insurance. On one end of the spectrum is a “buy term and invest the difference” philosophy that prioritizes protection above all else at the lowest cost possible. On the other end of the spectrum, the philosophy relies heavily on the accumulation aspects of life insurance, promoting insurance as a primary (if not the only) vehicle for saving for retirement. As is often the case, it is possible to go too far in either extreme.

Return Of Premium (ROP) term insurance offers a unique ‘middle ground’ strategy that might warrant more attention than it currently receives. ROP term insurance offers standard term life insurance coverage with a rider that returns all premiums paid (tax-free) in the event that an insured outlives the term of their life insurance coverage. So, for instance, if an insured buys a 30-year term policy for $1,000 per year and outlives the entire term of their policy, the full $30,000 premium paid will be returned to the policyowner tax-free.

While the mechanics of ROP term insurance are straightforward, the potential ROI from such policies is often misunderstood. A common criticism of ROP term is that a policyowner is “…just getting the money you paid toward premiums” and it is, therefore, “money that has lost out on years of compound interest.” However, this is the wrong way to think about ROP term insurance, because it is neglecting the value of the insurance that was obtained throughout the term of the policy. A fairer comparison would be to back out the cost of comparable term coverage and then treat the difference in cost between the two policies as the effective ‘investment’ that ultimately results in receiving the tax-free return of premium at the end of the policy term. And when ROP term insurance is looked at through this lens, the ROI can actually be quite attractive.

The return potential of ROP term insurance is attributed to various factors, including (a) the tax-free nature of the return of premium, (b) a form of mortality-credit-enhanced yield inherent to ROP riders (i.e., some insureds will pay for the ROP rider and pass away without receiving anything from the rider), and (c) an element of lapse-supported pricing within ROP term policies (i.e., many policyowners will purchase coverage and either intentionally or unintentionally let it lapse, resulting in premiums paid without receiving any return of premium benefit).

As a result, for those who know they want to purchase term coverage and keep it in place for the full term, adding an ROP rider is effectively an opportunity to add a side accumulation account to term coverage with some unique investment characteristics that can be quite attractive (similar to the attractiveness of mortality credits within income annuities). Some caveats to consider as well. First, since you do have to keep the coverage in force to reap the benefits, insureds may lose some flexibility to replace a policy with a cheaper alternative that may become available in the future or just let the policy lapse because they decide they no longer want the coverage. Second, the dynamics described above actually result in longer-term policies generally being cheaper than shorter-term policies, so the ROI tends to be most attractive for 30-year term policies. Third, and perhaps most important of all, the market is quite thin and at the time of writing this, there appears to only be one carrier in the market.

Ultimately, for clients who want term coverage and are willing to commit to maintaining coverage for the full term, ROP term insurance has some unique characteristics that can make it an attractive consideration. In addition to the financial benefits, the return of premium may give peace of mind to clients who are otherwise averse to carrying prudent coverage due to the ‘use-it-or-lose-it’ nature of term insurance. So although ROP term insurance may fall in an awkward middle-ground of providing both protection (primary) and accumulation (secondary) benefits that is not particularly popular among advisors, ROP term insurance may be worth a closer look!

When it comes to philosophies toward life insurance, there’s a pretty wide spectrum of views among financial advisors. At one end of the spectrum, there’s the “buy term and invest the difference” approach, where savings and insurance are viewed as entirely separate endeavors, such that it’s almost never desirable to have any savings component associated with insurance. At the other end of the spectrum is the approach that the tax preferences of life insurance can also be a direct support to savings, such that permanent cash value life insurance becomes someone’s first (and sometimes only) form of investment.

As is often the case, it’s possible to go too far in either extreme. What’s significantly under-explored, however – perhaps because it doesn’t align as neatly with either sweeping philosophical approach to insurance – is the “middle ground” of strategies that advisors could help clients implement, in which insurance has both an insurance and investment component that can be attractive on both fronts. One particular strategy that may be worth a closer look is Return Of Premium (ROP) term insurance.

The Underappreciated ROI Potential Of Return Of Premium (ROP) Term Insurance

Return Of Premium (ROP) term insurance is a form of term insurance that provides standard term coverage but, as the name implies, includes a rider that will also return all premiums (tax-free) in the event that an insured outlives (i.e., never dies and makes no claim on) the term of their life insurance coverage.

In some cases, companies may also pay out a portion of an ROP benefit if a policy is surrendered early (though not all policies will necessarily offer this and, even if they do, the surrender value is often significantly discounted relative to what would be paid out over the full term of the policy).

Like permanent insurance, an illustration can be requested to understand what, if any, surrender value is available within a term insurance policy with an ROP rider.

Example 1. Suppose John pays $1,000 per year for 30-year term coverage. He’ll pay $30,000 in premiums over the term of his policy.

If he lives through the term of his policy, he will receive $30,000 back as a tax-free benefit. John can request an illustration if he would like to know what, if any, surrender value is available earlier.

He may, for instance, start to accumulate some modest “surrender value” (not in the form of cash value build-up, but accumulated ROP eligibility) by about year 10 of the policy, but the value will often be significantly less than the premiums paid in until the full term of the policy is reached.

Unfortunately, when it comes to understanding the Return On Investment (ROI) of ROP term insurance, many people think of it all wrong. For instance, Policygenius criticizes ROP term insurance on the basis that you are “…just getting the money you paid toward premiums” and it is, therefore, “money that has lost out on years of compound interest.” In the same article, Ilya Karger, a Senior Sales Manager at Policygenius, goes on to say, “It’s like an interest-free loan to the insurance company… When you put that money in, you’re getting less money out because of inflation.” Of course, it is true that the $30,000 that comes back at the end of the term will typically have far less (inflation-adjusted) purchasing power than the $1,000/year x 30 years = $30,000 of premiums that were paid into the policy in the first place.

However, this is fundamentally the wrong way to think about ROP term insurance. With ROP term insurance, you still receive life insurance coverage throughout the term of your policy, so that value has to be accounted for. In other words, if the individual puts in $1,000/year for 30 years and gets back their $30,000 at the end, it’s not a “zero return” scenario, but instead, one where the “return” on their $30,000 was, in part, the fact that they received 30 years of term insurance (on which they happened to not have a claim, but that doesn’t mean the insurance wasn’t a worthwhile purchase along the way for the risk of untimely death it was managing).

Accordingly, a fairer comparison would be to look at the difference between buying term insurance with an ROP rider (where the $30,000 comes back) versus paying for the term insurance without an ROP rider (where those premiums are permanently gone, even if there is no death claim). Or viewed another way, it is only the difference between premiums on an ROP term policy and a comparable non-ROP term policy (i.e., the ROP rider), which should be seen as the ‘investment’ component that ultimately ‘grows’ to return all of the premiums at the end of the term.

And once the cost of the term insurance itself is backed out to figure out what the ‘savings’ component of an ROP term premium is, a rather different picture emerges.

Example 2. Suppose again that John is paying $1,000 per year for 30-years of ROP term coverage.

He’ll receive $30,000 (tax-free) at the end of his policy, but it would be wrong to say he paid in $1,000 per year and ‘only’ got $30,000 back. He got 30 years of term coverage plus $30,000 at the end of the term.

Suppose the cost of comparable term coverage without the ROP feature was $700 per year. In that case, John essentially purchased term insurance for $700 per year, and then paid in $300 per year as an ‘investment’ that would pay out $30,000 of tax-free benefit to him 30 years from now.

Once the cost of term life insurance coverage is accounted for, contrary to the negative portrayals of ROP term insurance above, the implied rate of return for ‘investing’ through an ROP term policy can actually be quite attractive (in this case, turning $300/year x 30 years = $9,000 of ROP riders into $30,000 of returned premiums at the end) – particularly when it is acknowledged that ROP term insurance is a low risk “return” to the insured (i.e., it is a contractually guaranteed return), and it is tax-free!

The ROI Of ROP Term Insurance

To take a closer look at the potentially high ROI on ROP term insurance in the real world, it’s necessary to examine the actual cost of ROP riders based on products actually available in the marketplace, relative to the actual premiums they return at the end of their specified terms.

(Editor’s Note: Product pricing examples included below are as of March 9, 2021, when this analysis was first prepared.)

Example 3: Continuing the prior example, assume that John is 30 years old, lives in Maine, and is in excellent health.

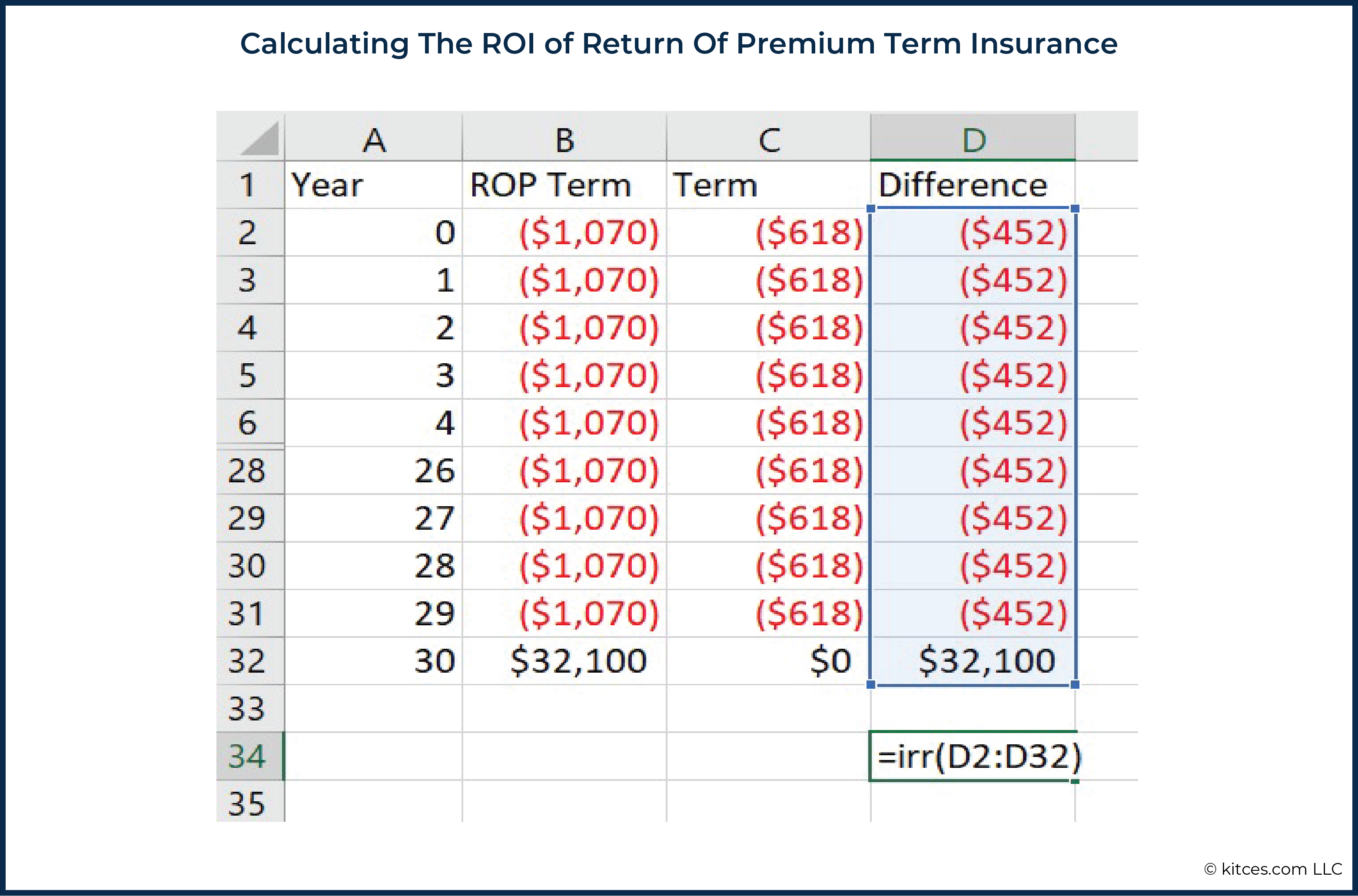

With the help of his financial advisor, John decides to look for $1,000,000 of coverage from a 30-year ROP term policy. Based on current marketplace prices, he could get that coverage for $1,070 per year.

This means that John would receive $1,070 (annual premium) × 30 years = $32,100 (tax-free) at the end of his policy. However, it would be wrong to say he paid in $1,070 per year and ‘only’ got $32,100 back because he got 30 years of term coverage plus $32,100 back at the end of the term.

The best cost of comparable standard 30-year term coverage for John without the ROP feature (through a different but comparable carrier) would be about $618 per year.

Thus, John would essentially purchase term insurance for $618 per year to get pure term coverage, and then, as an ‘investment’, would be paying in an additional $1,070 (annual premium of the ROP term policy) – $618 (annual premium of the standard term policy) = $452 each year for 30 years, for a total investment of $452 × 30 = $13,560.

Computing the ROI on the ROP term insurance rider in the above example requires the creation of a (relatively simple) table in Excel to calculate the Internal Rate of Return (with Excel’s ‘IRR’ formula), that looks like the following (Years 5 through 25 omitted):

The “Difference” column (“ROP Term” – “Term”) is used to compute the Internal Rate of Return (IRR). In Year 30, while the cash flow for the standard term policy is $0, there is a positive cash flow in the amount of all premiums paid (not just the ROP rider portion, but the entire term insurance premium) for the ROP term policy.

In cell D34, we have the formula to compute the ROI, which is simply taking the ROI of all of the differences in cash flows between the two policies [=irr(D2:D32)].

Thus, John’s ROI comes out to be 5.1%.

Recall, however, that the Return Of Premium is also tax-free. For high earners, tax-equivalent returns can be substantially higher!

Example 4: John’s Return Of Premium from Example 3 would have an ROI of 5.1%. Based on his current income level, his combined marginal state and Federal tax rates (based on existing tax brackets) is 44.15%.

Accordingly, his tax-equivalent return, then, would be 5.1% [tax-free return] ÷ (1 – 44.15% [combined marginal state and Federal tax rate]) = 9.1%.

Even at a more modest income level, the tax-equivalent return of the Return Of Premium could still be attractive.

Example 5 Continuing the prior example, instead of being in the 44.15% combined marginal state and Federal tax bracket, assume John is paying a 29.15% marginal state and Federal rate.

John’s tax-equivalent return, then, would be estimated to be 5.1% [tax-free return] ÷ (1 – 29.15% [combined marginal state and Federal tax rate]) = 7.2%.

Regardless of the tax level, the potential ROI is quite attractive for an extremely low-risk investment in an environment where high-quality 30-year corporate bonds were only paying about 3.7%.

So, to break down John’s decision a bit more, he essentially has a choice of (a) purchasing $1,000,000 of 30-year term coverage for $618/year, or (b) purchasing $1,000,000 of 30-year ROP term coverage for $1,070/year with an investment component that is paying 5.1% (before adjusting for the tax-free nature of the return!).

Choosing The Optimal Term For ROP Term Insurance

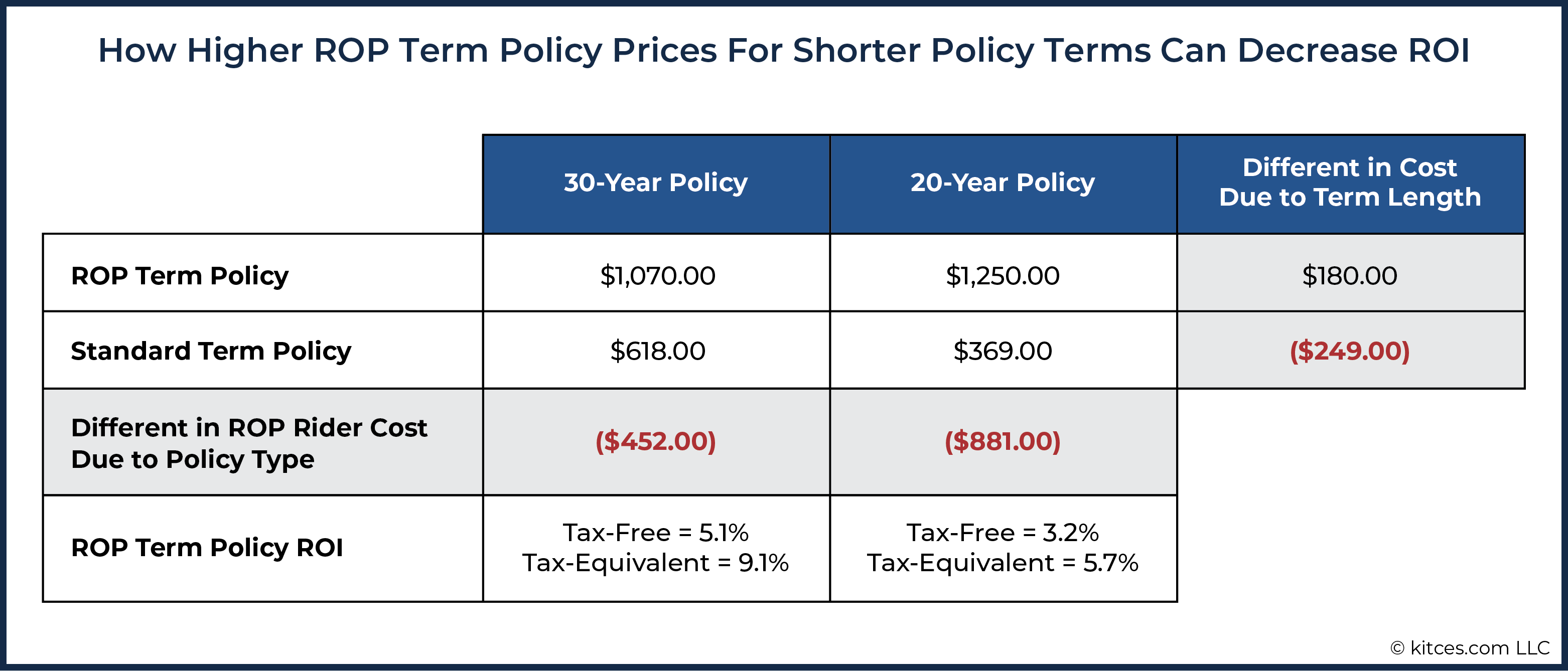

Notably, one nuance of ROP term insurance is that the pricing is often more attractive for 30-year coverage than for 20-year coverage. In other words, the insurance gets cheaper for longer periods of coverage and guarantees!

This is due to the fact that the premiums have to be returned in 30 years versus 20 years, which allows the insurance company to have more time to grow the premiums before returning them all. In other words, when the insurance company has less time to grow the ROP rider premium themselves to offset the cost of term insurance, the insurance company requires more for the ROP rider in the first place (thus increasing the cost of coverage for shorter-term ROP riders).

In addition, a 30-year term insurance policy that is actually held for all 30 years means carrying the coverage into higher-risk-of-death later years… which indirectly reduces the cost of the ROP rider because if the individual does actually die and receive a death benefit payout, the ROP rider is forfeited (because it is only designed to return premiums when the insured outlives the policy; if they die, they get the death benefit itself!).

The combination of these factors can also influence the ROI on ROP term insurance policies, and, in many cases, the ROI will actually be higher for 30-year coverage than for 20-year coverage.

Example 6: John is trying to choose whether to purchase 20-year or 30-year ROP term coverage. As before, the cost of a 30-year ROP term policy is $1,070 per year. When obtaining a current quote, though, John discovers that the cost of a 20-year ROP term policy is even higher, at $1,250 per year.

By contrast, the cost of standard term insurance itself actually declines from $618 per year to $369 per year when shifting from 30-year to 20-year term insurance.

Because the pricing difference between the 20-year ROP and Standard Term policies, in this case, is $881 per year, John would effectively be ‘investing’ $881 per year to receive a smaller ROP benefit of $1,250 (annual premium) × 20 years = $25,000, albeit received 10 years earlier than the larger $1,070 premium × 30 years = $32,100 ROP benefit in the 30-year term example above.

If we follow the same process for computing the ROI earlier in Example 3, John’s ROI falls from 5.1% to 3.2% (before adjusting for the tax-free nature of the return).

In the above example, the 20-year policy’s ROI may still be considered attractive for a low-risk, tax-free investment in the current marketplace. But the tax-adjusted return would top out at 5.7% using maximum Federal and Maine tax rates for John. This is substantially less than the maximum of 9.1% tax-equivalent return for the 30-year ROP term policy.

Other Considerations With ROP Term Insurance

Along with a favorable ROI relative to standard term insurance, another potential benefit of ROP term insurance is that, psychologically, it may be much more appealing to people seeking life insurance coverage in the first place.

As while insurance should be thought of first and foremost as providing protection, many individuals will still look at insurance and feel like they are “paying something for nothing” if they outlive their policy. Of course, this is the wrong way of looking at insurance, as someone did still get the value of coverage throughout the term of the policy, even if they never have to use it (akin to the value of still owning homeowners insurance even if the house never burns down), but this idea can be tough for some to come to grips with psychologically. ROP term coverage takes at least some of that psychological sting out, by providing a sizeable (tax-free) check at the end of a policy’s term.

However, there are some caveats to consider with ROP term insurance as well.

As noted above, ROP term policies likely work best for those who can commit to a 30-year term (and who are still young enough for 30-year term coverage to be affordable in the first place). While it still may be worth considering shorter-term policies, there are several reasons why longer-term policies can be more attractive here.

First, there’s effectively a form of mortality-credit-enhanced yield built into these ROP term insurance products. In the event that someone dies while their policy is still in effect, the insurance company will not have to pay out the ROP benefit. Of course, this individual will still receive their standard death benefit (i.e., the same death benefit they would have had purchasing pure term coverage), but they’ll have paid the extra premiums to cover the ROP rider without actually receiving any premiums back (effectively paying more in premiums for the death benefit they were going to receive anyway). Thus, similar to mortality credits in an annuity context, an ROP term rider provides an additional level of potential return to policyholders who don’t die (earning the equivalent of a bond return plus the ROP term mortality credit) than could be achieved through a comparable low-risk (non-mortality-based) investment.

Second, there’s also an element of lapse-supported pricing with ROP term policies. Since one typically does have to hold the policy for a full 30-year term to get their full ROP benefit, and since the insurance company further knows that many (if not most) won’t actually do so (whether due to accidentally letting the coverage lapse, intentionally letting go of the coverage because it turns out to no longer be needed, or because the term insurance policy is replaced with another in the future), the cost of the ROP rider can be reduced to account for forfeited ROP benefits from the number of policies that are predicted to lapse.

In other words, if 100 people buy 30-year term insurance with ROP riders, but half of them are expected to lapse the coverage before the end of the 30 years, the insurance company will have ROP rider premiums from all 100 people (at least as long as each keeps their coverage) but only ends out needing to pay out the benefit to the 50 who keep the policy. This reduces what the insurance company must charge for the ROP rider benefit and provides an additional potential boost to the ROI of ROP term coverage for those who know they can maintain coverage for the full term. As a result, ROP term coverage makes the most sense for someone who knows they can and want to maintain the coverage for the full policy term.

On the other hand, because the ROI of ROP term insurance is driven in part by those who do commit to (and actually do) keep their coverage for the entire term, a related downside challenge is that a policyholder may lose out on some flexibility in the event that they want to eliminate their ROP term policy or replace it by purchasing cheaper coverage in the future (resulting in much, if not all, of the ROP benefit being lost). This potential downside is not a major issue for anyone who is committed to the idea of keeping coverage in place for the full term, but may not be the best fit for someone who wants to save aggressively for their financial future (e.g., the FIRE approach), and then expects to drop their coverage as soon as they feel that they are financially secure enough to go without life insurance.

ROP term insurance may also not be an ideal fit for someone who currently has health or lifestyle factors that are reducing their health rating but could improve in the future. For instance, someone actively engaging in weight loss or other health changes may want to start with standard term insurance if they feel that they’ll potentially be in a position in a year or two to replace coverage with a new policy that qualifies for a better health classification during underwriting. Notably, though, some policies will allow the insured to get fresh underwriting and an improved classification on the existing policy, without re-issuance/replacement (thus preserving the ROP rider benefit), which can mitigate this risk (but should be explored in advance with the insurer if there is an expectation of a near-term improvement in health classification).

Perhaps the biggest caveat of all, however, is that the ROP term insurance market currently seems to be quite thin. At the time of writing this article, it appears that only one carrier (Assurity) is in this market. Assurity presently has an A- (Excellent) rating from A.M. Best, so the ROIs examined above don’t appear to be driven primarily by credit quality concerns (and the mortality-credit-enhanced yield and lapse-supported-pricing provide good theoretical justification for why we would expect to see some attractive ROIs for ROP policies generally), but a thin market is always less than ideal.

On the other hand, this could primarily just be driven by a lack of sales in this product area. This may be particularly true since ROP term insurance fits in a sort of awkward middle ground in terms of the polarized perspectives among so many financial advisors. ROP term neither minimizes the cost of coverage (often a primary focus for advisors of a “term and invest the difference” mindset) nor does it maximize the accumulation and growth of internal cash value in a ‘traditional’ permanent insurance product, so it ends up occupying a space that many advisors may not be paying much attention to.

Ultimately, the key point is to acknowledge that ROP term insurance may deserve a closer look from financial advisors. Both theoretically (due to mortality-credit-enhanced yield and lapse-supported-pricing), and based on the pricing that we see in the current market, ROP term insurance does provide some real upside in terms of providing insureds with both insurance protection and an attractive ROI on the tax-free Return Of Premium benefit.

Accordingly, while advisors tend to occupy space on extreme ends of the spectrum with respect to life insurance as an ‘investment’ (or not), there is some valuable middle ground that is worth exploring, and ROP term insurance is a good example of that middle ground.

Particularly for younger clients looking at 30-year coverage anyway (it wouldn’t make sense to add ROP term insurance just for accumulation purposes without needing the death benefit protection as well!) and who know they’ll want to keep coverage in place for their full term (and can afford to do so), the ability to invest in what is effectively a tax-free side account with low risk and high ROI can be quite attractive.

This enhanced return appears to be primarily driven by a combination of (a) a form of mortality-credit-enhanced return, and (b) an element of lapse-supported pricing. While these aspects are not favorable for those who may purchase insurance and decide not to keep it in force, for those who know they plan to maintain coverage, these pricing factors are a direct benefit to the policyholder. Furthermore, the psychological benefit of life insurance then becoming not a “use it or lose it” proposition may also help clients who are otherwise reluctant to carry prudent levels of insurance to do so.

While the market for ROP term insurance remains quite thin (potentially a reflection of the fact that ‘middle ground’ perspectives are just not common among advisors), perhaps after giving ROP term insurance a closer look, advisors and their clients may find that ROP term insurance is a life insurance product strategy that can provide both attractive protection (primary) and accumulation (secondary) benefits.