Executive Summary

Cash flow is the financial lifeblood of the household. As no matter how effectively one plans for the future, with savvy tax strategies and well-diversified investment portfolios… if there’s more cash leaving the household than there is coming in every month, eventually the plan (and the money) will run out.

Unfortunately, though, remarkably few individuals have a clear understanding of where their cash is actually going from week to week and month to month throughout the year. At best, most households are aware if their available cash balance (e.g., the bank account) is rising or falling… but without knowing where exactly the money is going, there’s no way to make adjustments. Yet in practice, tracking spending to figure out where the cash is going can be so time-consuming and laborious that many households would rather stay in the dark than take the time to do the extra work.

The good news, though, is that technology tools – when combined with the ongoing shift towards “cashless” digital transactions – is making it easier than ever to track a household’s cash flow. In this guest post, Lindsay Bourkoff, Director of Financial Planning at Shrier Wealth Management, highlights the software tool that she’s found works best in planning with clients: Tiller Money.

Discovered in her process of trying to find a cash flow tracking tool for her own household, Lindsay shares how Tiller Money finds a balance between automating the download of transaction data, easy viewing and output by aggregating the data into a custom Google Sheet (rather than a proprietary software app that cannot be adapted for individual client needs), and categorization (which can be done semi-automatically, though Lindsay notes that, in practice, having clients play at least a small role in manually categorizing irregular expenses can actually help to put them in better touch with where their money is really going).

Ultimately, some advisors (and their clients) may prefer a more automated solution to fully track and categorize expenses, while others may prefer an entirely hands-on approach. But in a world where there are still remarkably few cash flow tracking and budgeting tools for financial advisors themselves, Tiller Money provides an interesting consumer-based alternative (that can still be easily adapted for financial advisors in our own practice with clients).

Before I can create an actionable, realistic financial plan for my clients, I need to know something vital: How much are they already spending, and what do they spend it on? Historically, before online banking was widespread, tracking one’s spending was quite tedious. It involved looking at banking and credit card paper statements and totaling transactions by hand. This was a painful process, with room for error.

With digital banking a fixture in most households now, though, tracking one’s spending is no longer only for those “hardcore” individuals. In fact, I believe that utilizing software that links to your bank accounts to provide up-to-date spending tracking is now essential.

But which is best? There is a multitude of personal finance apps available from Mint.com, to YNAB, or mVelopes, which can link to your financial accounts. Each of these apps can then track your spending, but each has a varying focus. And I’ve always felt that they had an inflexibility which couldn’t adapt to complex, real-world finances, or alternatively, that there were too many moving parts.

In the last year, I’ve finally found my favorite: Tiller Money. Tiller Money has helped my clients stay organized, and helped me build better and more suitable financial plans by finally understanding where their cash flow it going. In fact, I was so impressed with it, that I’m now also an avid user of Tiller Money for my own household!

Searching For A Solution That I Could Use Personally (And Recommend To Clients)

My interest in Tiller Money began as I was searching for a tool to track and manage my own personal household cash flow.

For the last 15 years, my husband and I have been downloading our expenses each month into Excel. This would require us to log on to each of our financial institution’s portals (2 credit cards, and 1 primary checking account), choose a time-period, and download that month’s transaction history. Then we would cut and paste the data into a single spreadsheet and categorize the expenses. Once categorized, we would total up each category for the period. We had tried other solutions but found our financial situation too complex, and the algorithms of the other software solutions were inflexible to handle our situation.

Tracking cash flow in Excel was a time-consuming process. I knew that getting clients to adopt it would likely not be successful; plus, it would be difficult to just explain the manual process and steps to them! After discovering Tiller, I was drawn to the automatic data feed of our transactions each day, and templates that organized our cash flow in a simple Google Drive spreadsheet stored in the cloud. I especially enjoyed how I can organize and manipulate my own data in a way that makes sense to me. Additionally, unlike other personal finance apps like Mint.com, Tiller promotes accurate data categorization because, by default, Tiller does not automatically categorize your transactions. Users must either manually categorize transactions, or they can establish well-defined auto-categorization rules using their own keywords. With Tiller, the user plays a vital role in categorizing their expenses on a regular basis. This helps to provide a greater consciousness of one’s cash flow and ultimately change spending behavior.

What Is Tiller Money?

Tiller Money (www.tillerhq.com) is a website which automatically consolidates a user’s cash flow transactions, using account aggregation to pull in the transaction data from various bank accounts and credit or debit cards, and pushing the data into Google Sheets. Once the data is there, Tiller also provides templates for individuals (and businesses) to track their spending, create budgets, and build customizable spreadsheets to manage finances.

The concept sounds simple and it is; that’s the beauty of it. There are no gimmicks, kitschy graphics, or distractions. Tiller allows you to link your various accounts (checking, savings, credit cards, etc.) through an integration with Yodlee, and then each day, the transactions are consolidated on the same Google Sheet. The user creates their own cash flow categories in one of the sheets’ tabs, and can then manually categorize transactions with a drop-down menu (although there is a plug-in option to categorize automatically using user-defined rules; more on that later!). Once categorized, the data flows into your selected template summary page.

Tiller provides more than 10 sample budgeting and tracking spreadsheet templates that a user can choose from, depending on their needs. It even includes a template that allows you to customize your own sheet from scratch. Currently, Tiller best serves individuals searching for solutions to manage their own personal finances, but they recently came out with a new template with can serve businesses too called the Tiller Simple Business Spreadsheet. This template provides a big picture overview of cash flow trends and current account balances. Because Tiller is a flexible tool and has an open architecture, businesses should be able to customize a Tiller sheet and make it work for their diverse needs.

Tiller offers a free 30-day trial, after which it costs $59 a year. The product can be canceled anytime. Currently, Tiller offers a single version of its product and does not offer a special license for financial professionals. A Tiller membership allows its users to choose up to five templates to use simultaneously. Each template can have different linked accounts, so members could use Tiller to create spreadsheets for both their business and personal cash flows in a single login (but feeding to separate Google Sheets).

One feature I enjoy is that, once a Tiller sheet has been created, it can be shared with other family members, or even one’s financial planner, to be viewed or edited. This is especially useful for financial professionals who rely on quality, reliable data to build financial plans for their clients!

Getting Started With Tiller Money

Once you sign up for Tiller Money, it will prompt you to choose a template. Tiller offers a wide range of templated spreadsheets with various purposes in mind. For those wishing to gain an understanding of their net cash flow and how it evolves each month and over the course of the year, Tiller has a spreadsheet called Tiller Monthly Budget which I personally find quite helpful. For users who want a more detailed picture of their spending only, Tiller’s Weekly Expense Tracker template provides loads of spending analytics.

More recently, Tiller-- based on user feedback -- has also recently upgraded their Tiller Budget template to include more robust budgeting features. This new Tiller Budget sheet is for users who prefer zero-sum budgeting or envelope-style budgeting (such as YNAB or mVelopes). Users can now assign a precise target budget amount for each category. As individuals’ transactions flow into the software and become categorized, Tiller keeps track whether you are over or under your budgeted amount. If you’ve spent too little in a category for the period, you can also roll over the unused dollars into the next period. Additionally, Tiller now allows users to assign a savings target.

A Review Of What It’s Like To Use Tiller Money

The operational flow of Tiller is through the use of various tabs at the bottom of their Google Sheet templates. Each tab has a different function.

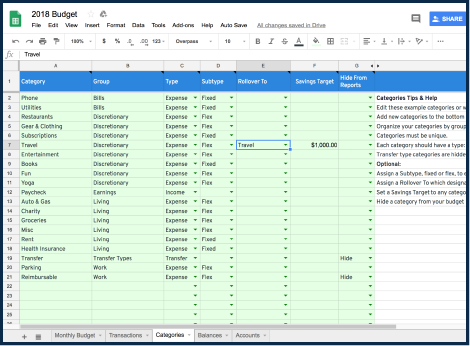

For instance, in the Tiller Monthly Budget worksheet, the primary useful tabs are Categories, Transactions, and Yearly Budget. The Categories tab is where your clients will customize the labels for their various spending categories. This is especially useful because each individual thinks about their spending in a different way, so by customizing spending labels, it allows them to develop an understanding of their cash flow which is intuitive and personal. (As an adviser, helping a client develop their categories is the first critical step to help them organize how they think about money!)

In addition to labeling the categories, users will also identify each category as one of three types: Income (i.e., inflows), Expense (i.e., outflows), or Transfer. The Transfer category is important, as some transactions are really just an internal transfer across accounts, which means it was an outflow to one account but had a matching inflow to another, and not actually a net income or expense transaction for the household. For instance, when you “withdraw” funds from a bank account to pay off a credit card, the “expense” was already recorded from the original credit card transaction itself; the payment from the bank account to the credit card is merely a transfer payment to cover that prior expense and not a new expense at that point.

TillerHQ Transaction Tracking And Expense Categorizations

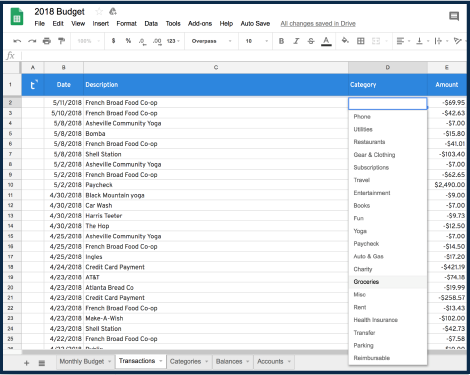

The transactions tab is where all daily transactions are found once Tiller automatically downloads them from your bank/credit cards. Notably, this means it’s not necessary to link “all” financial accounts; you only need to link spending-related accounts (e.g., primary and secondary checking accounts, and credit cards). In fact, linking savings accounts (like IRAs) or mortgages can create duplicate transactions (as they would effectively be Transfer payments from the other accounts at that point!). The transactions tab is where clients will initially categorize their spending with a drop-down menu of choices (which they personally created for themselves in the Categories tab earlier).

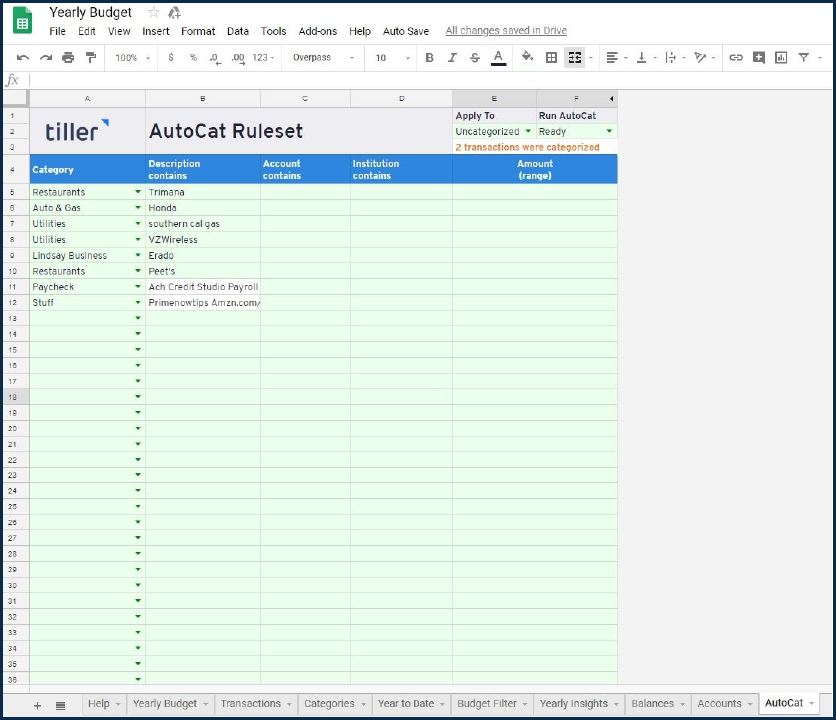

Recently, Tiller rolled out an add-on feature (plugin) called Auto-cat, which auto-categorizes the user’s expenses based on a few simple rules and makes workflows more efficient. I recently tried it out and was very impressed with the ease and accuracy of this feature. The user is in charge of building the rules for the categorization, so there are no software-based errors in categorizing your expenses. After downloading the plugin, the user sets up the auto cat rules. In the auto-cat tab, the user will type a descriptive word or two for each expense they wish auto-cat to categorize in the future. For instance, for my Honda lease, I typed in the word “Honda” in the description and in the category, I typed “Auto & Gas.” Then, every time the program identifies the word Honda, it will automatically categorize it correctly based on my rule. Auto-cat is best used for the regular and predictable monthly expenses (mortgage, utilities, car payments, tuition, student loan repayments etc.).

For expenses which are irregular or unusual (and for which auto-cat rules are not established), clients will manually categorize these expenses. For clients used to automation, this process may be tedious and slightly frustrating at first. However, I have found that manually categorizing irregular expenses allows clients to gain a mastery of their spending, and better know precisely what they are buying and where their money is going. It also ensures accuracy. In fact, I believe that it is the act of reviewing one’s expenses and manually categorizing them which is, in-and-of-itself, part of the benefit of Tiller because it forces clients to confront their spending head-on... especially when that spending is unpredictable.

TillerHQ Spending Summaries

After categorizing expenses, now it’s time to view the summaries.

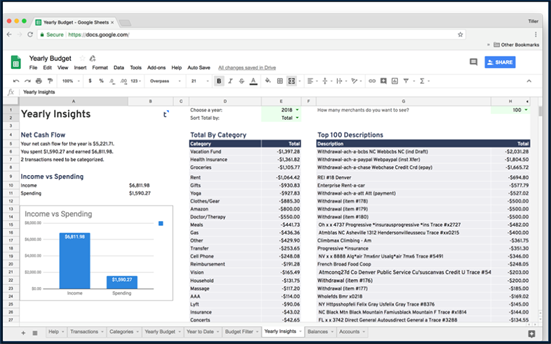

In the Tiller Monthly Budget spreadsheet, the summaries can be found in the tabs titled Yearly Budget, Year To Date, or Yearly Insights. These reports summarize the data from the other tabs. This is ultimately where most of the financial professional’s analysis will occur, as this is where all of your clients’ categorized transactions are consolidated into an organized and simple cash flow report, based on the categories that were created and how they were assigned on the Transactions tab (while excluding the Transfer payments that don’t represent net inflow or outflows from the household for budgeting purposes).

My Favorite Tiller Money Features

In the age of Amazon shopping, one of the biggest challenges for people who carefully track and categorize expenses is how to classify expenses from Amazon. For many of us, Amazon has become a one-stop-shop.

For instance, on my recent credit card statement, an Amazon charge of $104.23 was displayed. This included items for our house, kids clothing, and groceries. Tiller has the capability to address this thorny issue. On Amazon’s website, they currently provide a link which allows users to download an order history report in Excel and breaks down individual Amazon orders. This Excel data can then be cut and pasted into Tiller’s transactions, in order to categorize each individual Amazon expense (and then simply delete the original single Amazon line item on the Tiller Transactions tab). Tiller’s budget sheet will then have incorporated the specific spending data from Amazon.

Another similar feature I enjoy is Tiller’s transaction splitter. This is especially convenient for expenses such as ATM withdrawals, which may have been spent in several places. I prefer the transaction splitter for expenses with three or fewer sub-categories. Users could use transaction splitter for Amazon expenses too, but depending on how many various items you purchased, this could be time-consuming.

Lastly, I enjoy receiving Tiller’s daily digest of our spending (“Did we really go to Peet’s Coffee three times on Sunday?”), as well as communicating with Tiller’s helpful customer service team, who are available for questions over chat.

How Can You Use TillerHQ in Your Planning Practice?

For financial planners and advisers, one of the most critical elements of any retirement plan is the knowledge of the household’s actual expenses.

For younger clients building wealth, tracking spending is essential to determine how much a client is capable of saving each month or year and giving them advice on how to actually make adjustments to their spending to save more. It simply isn’t enough to tell a client to save 10% of their salary, without knowing if that is feasible given the specific circumstances of their lives. Because ultimately, if a financial planner provides a savings goal to a client that is unrealistic, the financial plan will be obsolete on day one anyway. Likewise, if a client is capable of saving more like 20%, the adviser is doing them a disservice by advising them on a “typical” 10% or 15% savings target that may be low savings for them.

Similarly, understanding a household’s spending patterns is necessary for projecting cash flow in retirement, to the extent that their current lifestyle is usually the basis for setting a lifestyle goal in retirement as well. After all, it’s not really feasible to determine the sustainability of withdrawals if there isn’t good clarity about what the spending needs (and thus the withdrawals) will likely be in the first place!

Simply put, knowing reliable spending patterns is a fundamental building block in financial plans. Yet for most of my clients, who have worked their entire lives, it is quite common to have little understanding of where one’s income is actually going. As many advisers will attest, most clients simply know that they have a certain balance of cash in their checking account and that it fluctuates month to month in a range. Over the 15 years I’ve been advising clients, I’ve found that even when clients try to estimate their own spending, those spending estimates provided by clients were usually unreliable. It is only through reliable data that we build smart, sustainable plans that have the possibility of working in the long run!

Now when working on comprehensive financial plans with clients, I try and encourage them to utilize Tiller so that both the client and I can gain a full understanding of their actual household cash flow.

How to Use Tiller Money with Clients

Over the last year, I have encouraged clients to use Tiller and even sat with them while they link their accounts and help them establish their expense and income categories in order to get started. We sit together while the client signs up for Tiller (this takes about 5 minutes), choose our desired template, and start creating categories which reflect the client’s way of thinking about their expenses. I provide the client with sample categories that I’ve used in the past as a guide, but in practice, many will choose their own categories based on what makes sense to them.

While budgeting can sometimes be a hated concept, I have found most clients are eager to start tracking their spending, gain a mastery of their cash flow and are ready to get in “financial shape.” In preparation for our subsequent meetings, I request clients send me their Tiller Sheet so I can review it, make suggestions, and refine our financial plans together. Currently, in my practice, clients pay for their own subscription of Tiller, which is completely optional.

Obtaining Consciousness of Spending – Human Engagement

In addition to providing the financial professional with quality data, in practice, I’ve found that Tiller also has had a powerful impact on my clients’ spending and cash flow consciousness by engaging them with their transactions.

Each day, Tiller sends an email with the user’s newest raw transactions and encourages users to categorize them. In the email, users are directed to a link to their personal Tiller sheets where one can categorize from there.

One critical aspect of Tiller is that it requires users to either manually categorize their own expenses, or set up specific rules for Auto-Cat. As noted earlier, the act of categorizing expenses not only ensures accurate information, but it also serves as an indispensable method to shape individuals’ spending behavior by building their own awareness of their spending as they categorize their expenses. And while categorizing or setting up auto-cat rules are initially a bit overwhelming for clients, I’ve found clients gradually get used to it and keep up with it over time.

Once initiated to Tiller, it may only take a few minutes to categorize transactions each day. I find that clients who categorize frequently, such as weekly, are most successful in this process.

In Summary

In today’s day and age where credit card bills, utilities, mortgages, and other expenses are automatically paid by online bill pay, and where paychecks are deposited automatically by direct-deposit, I have found that many clients are unsure of where their cash is actually flowing.

Tiller Money’s automatic data feed of daily transactions into a consolidated shareable Google Sheet in the cloud provides a means to make it easier to keep track. Tiller’s “requirements” to either manually categorize transactions or set up rules for auto-categorization helps people engage with their spending to create real awareness of where their money is going and eliminates artificial intelligence errors. Further, the ability to customize spreadsheets and manipulate the information to fit your personalized situation provides better control and understanding. And finally, Tiller’s subsequent and ongoing communication about user’s transactions helps to continually shape spending behavior over time, creating more conscious consumers who become more cognizant in real time about their next spending decisions.

The ease, simplicity, and customization of the software help me envision this as a method that my clients and I can adopt for many years to come!

Lindsay is a registered representative with and, and securities and advisory services offered through LPL Financial, a registered investment advisor. Member FINRA/SIPC.

The opinions expressed in this material do not necessarily reflect the views of LPL Financial and are not intended to provide specific advice or recommendations for any individual. LPL Financial is not affiliated with and does not endorse Tiller Money or any other software system or application mentioned.