Executive Summary

From time to time, individuals (typically high-income) can make after-tax contributions to traditional retirement accounts that are usually designated for pre-tax funds. No deduction is received for these contributions because the contributions have already been taxed and should not be taxed again. To avoid such double taxation, however, the after-tax contributions must be recorded properly, and those records must be adequately maintained. This is particularly important when after-tax amounts end up in Traditional IRAs.

After-tax contributions can make their way into Traditional IRAs via two separate routes, either via direct contributions of after-tax amounts or through rollovers of after-tax dollars previously held in an employer-sponsored retirement plan. Critically, while many taxpayers think that their IRA custodian is keeping track of the after-tax amounts they have in their Traditional IRA, it is, in fact, the taxpayer who is responsible for doing so. Specifically, taxpayers are required to file Form 8606, Nondeductible IRAs, to keep track of such amounts. Sometimes, for numerous reasons, taxpayers may fail to file Form 8606, which can result in basis being ‘lost’. Yet filing Form 8606 does not always capture IRA basis, as it is only required either when after-tax amounts go into the Traditional IRA (via a nondeductible contribution or a rollover of after-tax funds from employer-sponsored retirement plans) or when after-tax money is distributed from a Traditional IRA (including a Roth conversion).

Accordingly, there can be gaps between these actions with long periods of time during which Form 8606 is not required to be filed. In the interim, various events, such as changing CPAs or the death of the client, can lead to a previously filed Form 8606 being ‘forgotten’, resulting in a similar outcome to having never filed the form in the first place! One way to dramatically reduce the likelihood of properly reported basis being forgotten is by filing Form 8606 every year regardless of whether it is required. This way, a taxpayer can be sure that their cumulative IRA basis will always be available on their most recent income tax return.

In the event Form 8606 was not properly filed to begin with, basis can be reconstructed from scratch. To reconstruct nondeductible Traditional IRA contributions, taxpayers can find old Traditional IRA account statements showing contributions, past years’ Form 5498 (Individual Retirement Arrangement Contribution Information), or Form 1099-R (Quantifying And Proving Prior Years’ Nondeductible IRA Contributions) that report such amounts. Alternatively, they can also request a Wage and Income Transcript from the IRS. All of these could be used to prove that a contribution to a Traditional IRA was made. And if a contribution to a Traditional IRA was made with no deduction taken, which can be verified with copies of the relevant tax returns or by requesting Return Transcripts to the extent that such returns were otherwise unavailable, the amount is a verified nondeductible contribution!

Ultimately, the key point is that taxpayers may still be able to deduct tax-free distributions, even if they have ‘lost track’ of the basis in their Traditional IRA accounts. By turning to a multitude of resources to help identify the nature of their retirement account contributions and rollovers, financial advisors can help prevent the double taxation of after-tax contributions made to clients’ retirement accounts!

Saving for retirement in tax-preferenced retirement accounts is often one of the primary objectives for the clients of financial advisors, where most contributions made to a taxpayer’s retirement accounts are either deductible contributions to a Traditional retirement account (e.g., IRA, 401(k), 403(b), or similar), or nondeductible (after-tax) contributions made to a Roth-style account (e.g., Roth IRA, Roth 401(k), Roth 403(b), or other designated Roth account).

Occasionally, however, clients make after-tax contributions to traditional accounts that are usually designated for pre-tax funds. Such contributions have already been taxed, and should not be taxed again. Unfortunately, though, such after-tax contributions are often ‘lost’ when clients forget that these amounts were after-tax, or do not track and report them on their tax returns correctly, potentially leading to double taxation when subsequent distributions are taken and this IRA basis is not accounted for.

Accordingly, advisors can help clients keep track of such after-tax amounts, and to ‘recover’ any after-tax amounts that have previously gone ‘missing.’

Nerd Note:

Since no deduction is received when Roth IRA contributions or salary deferrals to a Designated Roth account (e.g., Roth 401(k), Roth 403(b), Roth Governmental 457(b)) are made, such contributions are, technically speaking, “nondeductible”, or “after-tax”, contributions. Nevertheless, when practitioners use the phrases “nondeductible contribution” or “after-tax contribution”, they are almost always referring to either after-tax amounts contributed to a Traditional IRA or to contributions made on the pre-tax ‘side’ of an employer-sponsored retirement plan, and not Roth amounts. Conversely, Roth contributions are typically referred to specifically as “Roth contributions”.

The Direct Creation Of IRA Basis Via Nondeductible IRA Contributions

The primary way in which basis is created within a Traditional IRA is via nondeductible (i.e., after-tax) IRA contributions. Such contributions typically occur when a taxpayer is eligible and chooses to make a contribution to their Traditional IRA, but is phased out of being able to claim a deduction for that contribution (or voluntarily chooses not to deduct the contribution, which can, in rare cases, be advantageous).

Notably, as a result of the SECURE Act, since 2020, the only requirement for taxpayers to make a Traditional IRA contribution is that they have some sort of “compensation” (prior to 2020, individuals also had to be below age 70½ at the end of the year). Typically, a taxpayer’s “compensation” will consist of some sort of earned income, such as W-2 wages or self-employment income, though other forms of income such as taxable alimony qualify as well.

But while having compensation is the only requirement to make a Traditional IRA contribution, it doesn’t guarantee that such a contribution will be deductible… even though it was made to a Traditional IRA!

More specifically, if a taxpayer and/or their spouse (if applicable) is an Active Participant in an employer-sponsored retirement plan (e.g., 401(k), 403(b), 457(b), pension, SEP IRA, SIMPLE IRA, TSP, etc.,) and has income that exceeds a specific threshold, then their ability to deduct Traditional IRA contributions is reduced or eliminated altogether. In other words, the contribution itself can still be made as long as there is earned income to contribute… but the deductibility of that contribution phases out.

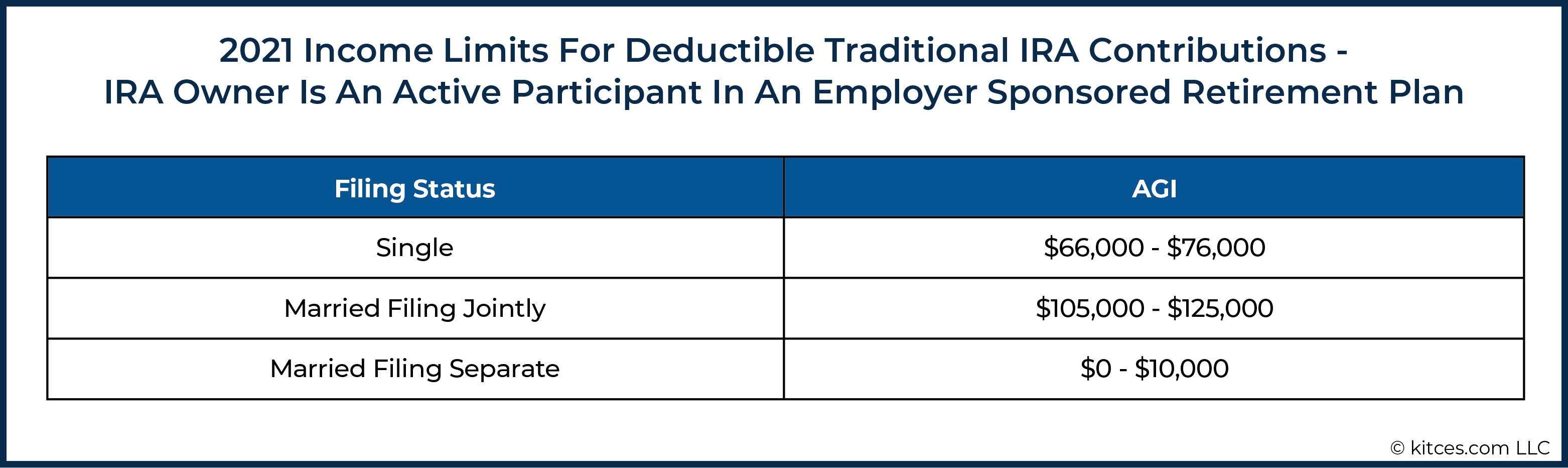

For 2021, the phaseout ranges for claiming a deduction for a contribution made to the Traditional IRA of an Active Participant are as follows:

Example #1: Albert and Minerva are married taxpayers who have AGI of $150,000 in 2021. Both are employed and are Active Participants in their respective employers’401(k) plans. Each also makes a $6,000 contribution to their Traditional IRA accounts for 2021.

Albert and Minerva have compensation for 2021, so each of their $6,000 contributions are allowable. However, since both are Active Participants in their respective employer plans, and their $150,000 income exceeds their applicable maximum phaseout amount of $125,000 for married taxpayers, they will not be able to receive a deduction attributable to those contributions.

Accordingly, both Albert and Minerva will have made nondeductible Traditional IRA contributions.

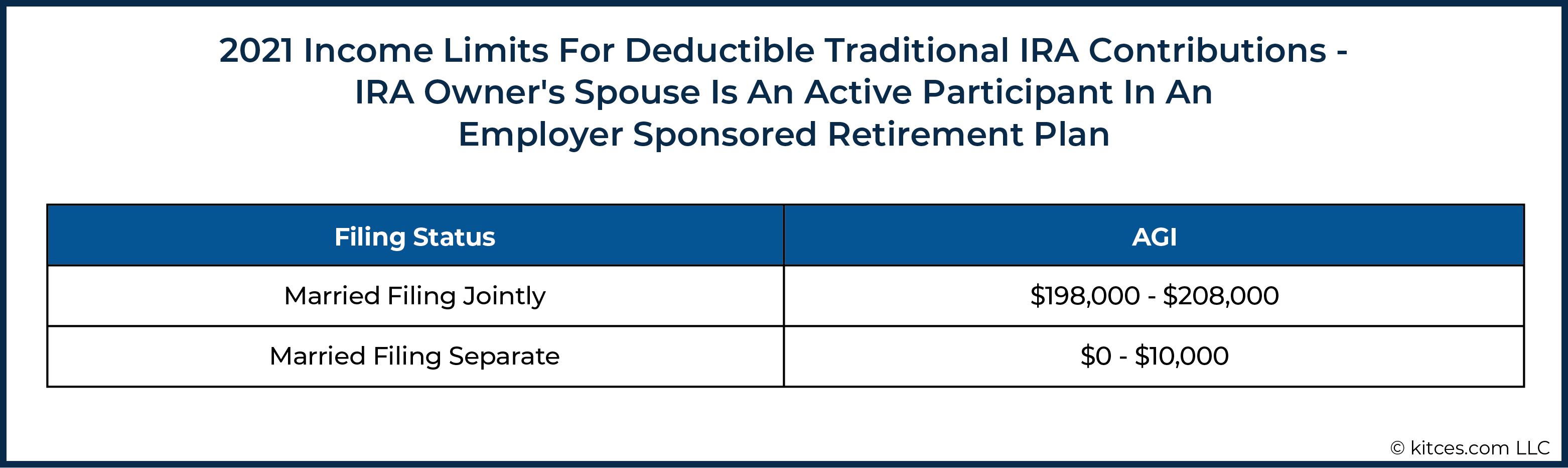

On the other hand, deductions for a contribution made to the Traditional IRA of an individual who is not an Active Participant in an employer’s plan themselves, but who is married to an Active Participant, may also be phased out, but are subject to the following, separate phaseout ranges:

Example #2: James and Lily are married taxpayers who have AGI of $150,000 in 2021. Both are employed, but only Lily is an Active Participant in an employer-sponsored retirement plan. Both James and Lily make a $6,000 contribution to their Traditional IRA for 2021.

James and Lily have compensation for 2021, so each of their $6,000 contributions are allowed. Furthermore, since James is not an Active Participant in an employer-sponsored retirement plan (but his spouse, Lily, is), and the couple’s income of $150,000 is below the threshold limit of $198,000, he is able to claim a deduction for the contribution made to his Traditional IRA.

However, since Lily is herself an Active Participant and the couple’s income of $150,000 exceeds the applicable maximum phaseout amount of $125,000, they will not be able to receive a deduction attributable to Lily’s Traditional IRA contribution.

Accordingly, for 2021, James will have a deductible Traditional IRA contribution (for being under the spousal Active Participant income limit) and Lily will have a nondeductible Traditional IRA contribution (for being over the direct Active Participant income limit).

The Indirect Creation Of IRA Basis Via Rollovers Of After-Tax Dollars In An Employer-Sponsored Retirement Plan

In addition to nondeductible contributions creating basis in a Traditional IRA, basis can also make its way into a Traditional IRA when after-tax dollars are rolled over to a Traditional IRA from an employer-sponsored retirement plan.

There are, however, several reasons why this is less likely to be the way clients may end up with after-tax dollars in their Traditional IRA accounts (as compared to making nondeductible contributions, described above).

First, while anyone with compensation can make a contribution to a Traditional IRA, only a relatively small group of taxpayers actually has the ability to make after-tax contributions to an employer-sponsored retirement plan.

This is because after-tax contributions to defined contribution plans ‘play’ on the difference between the IRC Section 402(g) salary deferral limit ($19,500 for 2021), which limits the amount an employee can elect to defer from their salary, and the 415(c) overall/annual additions limit ($58,000 for 2021), which consists of both elective deferrals (including 402(g) salary deferrals) and employer contributions.

But both limits are not applicable to all plans. SEP IRAs, for instance, don’t allow employees to contribute any of their own funds to the plan and thus the 402(g) salary deferral limit does not apply. Instead, all contributions to SEP IRAs are made by the employer, deductible to the employer, and taxable to the employee. SIMPLE IRAs are subject to separate limits on contributions and are not permitted to offer Roth options that would allow after-tax contributions. And for governmental 457(b) plans, only the 402(g) salary deferral limit applies so after-tax contributions are never made to these plans.

So, in the end, it’s primarily just traditional 401(k) and 403(b) plans that have the 402(g) salary deferral limit, and that are eligible for the higher 415(c) overall annual additions limit that makes it feasible to add after-tax contributions on top.

Example #3: Harry is a participant in the ABC, Inc. 401(k) plan, which allows after-tax contributions. In 2021, Harry maximizes his salary deferral contribution of $19,500. His employer contributes an additional $8,500 to the plan on his behalf, bringing total additions to the plan for 2021 to $28,000.

With the overall limit of annual additions for 2021 plan contributions set at $58,000 by IRC 415(c), Harry has $58,000 (overall limit) – $28,000 (total 2021 contributions made to date) = $30,000 of ‘free space’ in his ABC 401(k) for 2021.

Accordingly, Harry could make up to $30,000 of additional after-tax contributions to his 401(k) for 2021, assuming the contributions pass the requisite tests for highly compensated employees, such as the Actual Contribution Percentage (ACP) test.

Second, just because an employer-sponsored retirement plan can offer participants the opportunity to make after-tax contributions, it doesn’t mean they have to do so. In fact, to the contrary, the decision to allow plan participants to make such contributions is 100% at the plan’s discretion.

To that end, while 403(b) plans can allow for such contributions, finding such plans that choose to do so is exceedingly rare. And while the option is adopted more frequently in 401(k) plans, it is still far from what you might call “widespread” (though it has become somewhat more common in recent years as a way to accommodate those who want to do so-called “mega backdoor Roth” contributions).

Third, even when a plan does offer participants the ability to make after-tax contributions, not all participants will choose to do so. And even when they do choose to make after-tax contributions, it’s not uncommon to find high-income plan participants who are prevented from doing so because of non-discrimination testing (as even a safe-harbor plan does not exempt after-tax contributions from the Actual Contributions Percentage (ACP) test).

Finally, as a result of (somewhat) recent guidance, no new rollovers of after-tax dollars should be made from an employer-sponsored retirement plan to a Traditional IRA… because there is now a better option for those after-tax rollover dollars. In fact, the last time such rollovers should have occurred was back in 2014, when the IRS released Notice 2014-54. This release definitively addressed long-standing questions amongst practitioners over how after-tax dollars distributed from employer plans could/should be treated.

In short, the Notice clarified that if a distribution from an employer-sponsored retirement plan contained both pre- and post-tax dollars, the post-tax dollars could be split from the pre-tax dollars and sent, separately from the pre-tax dollars, to a Roth IRA as a tax-free conversion.

Given that such a conversion would ‘transform’ all future earnings from being taxable (if earned and distributed from a Traditional IRA after a rollover) to tax-free (if earned inside a Roth IRA and distributed as a Qualified Distribution) at a cost of $0 (since the dollars are after-tax in the first place and thus not taxable when Roth converted), since the release of Notice 2014-54 there is absolutely no reason to roll those funds over to a Traditional IRA.

Accordingly, over time, fewer and fewer Traditional IRA owners should find themselves with after-tax dollars in their accounts as a result of a rollover from an employer-sponsored retirement account.

Nevertheless, prior to the release of Notice 2014-54, the IRS’s position on how plan distributions consisting of both pre-tax and post-tax funds should be treated was much less clear. As a result, to ensure continued tax deferral of the full distribution (specifically the pre-tax portions), contributions were often rolled, in their entirety, to Traditional IRAs where they may still be today.

How Traditional IRA Basis Is ‘Lost’: The Case Of The Disappearing Basis

One common question asked by taxpayers who have after-tax dollars in a Traditional IRA account is, “Who keeps track of this stuff?” Oftentimes, taxpayers think that their IRA custodian is keeping track of these amounts for them.

Newsflash… they’re not.

Rather, while after-tax funds in an employer-sponsored retirement plan (e.g., a 401(k) or 403(b)) are tracked by the plan’s administrator (or at least, they should be), taxpayers are on their own when it comes to keeping track of the after-tax amounts in a Traditional IRA, including after-tax amounts rolled into a Traditional IRA from an employer-sponsored retirement plan. Specifically, taxpayers are required to file Form 8606, Nondeductible IRAs, to report nondeductible contributions to Traditional IRAs, as well as distributions of after-tax dollars, and conversions to any other IRA accounts.

With such a precisely defined way of keeping track of after-tax dollars in a taxpayer’s Traditional IRA – a dedicated IRS Form 8606 for just that purpose – one might think that it would be hard to lose track of such amounts. Unfortunately, though, for a variety of reasons, that’s not the case. Instead, ‘lost’ basis (after-tax funds) is a common problem, which often goes undetected, and can lead to double taxation of the after-tax funds!

Form 8606 Might Have Never Been Filed

One common way taxpayers lose track of after-tax funds is that they simply fail to file Form 8606 from the get-go. In such instances, the IRS may never be made aware of the after-tax dollars in a client’s Traditional IRA.

Oftentimes, the failure to file Form 8606 is due to a Cool Hand Luke problem – “What we’ve got here, is failure to communicate.”

Simply put, a client makes a nondeductible contribution to a Traditional IRA, and they never tell their CPA or other tax professional, either because they assume their tax professional already knows (but really, how would they!?) or they simply forget to tell them. Accordingly, Form 8606 is never filed.

In other cases, the taxpayer may file their own return and may not know to file Form 8606. And, of course, tax preparers are not infallible. Mistakes occasionally happen, and one of those mistakes could be a preparer’s failure to file Form 8606, even if they had all the information necessary to do so.

Filing Requirements For Form 8606 Make It Susceptible To Getting ‘Lost’

Although it’s not terribly uncommon to find a taxpayer who has never filed Form 8606 to begin with, Traditional IRA basis is ‘lost’ more frequently due to Form 8606’s own (lousy) filing requirements and the passage of time.

Because simply put, the Instructions for Form 8606 only require that it be filed for purposes of reporting after-tax amounts when one of the following events occurs:

- After-tax money goes into the Traditional IRA (via a nondeductible contribution or a rollover of after-tax funds from an employer-sponsored retirement plan); or

- After-tax money comes out of the Traditional IRA via a distribution (including a Roth conversion).

As a result of the limited filing requirements, which only trigger when money goes in or comes out of a traditional IRA with after-tax dollars, there can be many years, and in some cases, even decades, between events that require the filing of Form 8606.

Example #4: Myrtle is a single taxpayer who just turned 50 years old, and who has her sights set on retiring at 60. Accordingly, Myrtle wants to put away as much money as possible for retirement on a tax-preferenced basis each year until she retires.

Myrtle is a participant in her employer’s 401(k) plan, and after maxing out her contributions to the plan, her 2021 AGI is $150,000. She also makes the maximum contribution of $7,000 to her Traditional IRA for 2021.

However, since Myrtle is an Active Participant in an employer-sponsored retirement plan and her AGI is above the applicable phaseout threshold of $76,000 for single filers, the entire contribution to her Traditional IRA is nondeductible.

When Myrtle goes to file her 2021 tax return, she makes sure to inform her tax preparer that she made a nondeductible contribution to her Traditional IRA, thus avoiding the Cool Hand Luke problem.

Accordingly, her tax preparer properly files form 8606, reporting $7,000 of after-tax amounts in her Traditional IRA as of the end of 2021.

Assume that the same sequence of events occurs in each of the next nine years. In each year, Myrtle makes a $7,000 nondeductible contribution to her Traditional IRA, and each year, her tax preparer records the contribution properly on Form 8606. Accordingly, by the time Myrtle turned 60, Form 8606 shows cumulative after-tax amounts in her Traditional IRA of $$7,000 × 10 years = 70,000.

Suppose, now, that Myrtle has done such a great job saving for retirement that she’s able to avoid tapping into her Traditional IRA for the first 12 years of her retirement. In fact, she only begins to use her IRA funds at age 72 to take her Required Minimum Distributions (RMDs).

In this case, barring other actions requiring the filing of Form 8606 unrelated to after-tax dollars in a Traditional IRA (such as a Roth IRA conversion), Myrtle will go 12 years without ever needing to file the form!

Perhaps unsurprisingly, a lot can happen in 12 years (or 10 years, or 5 years, or even just a few years) that can result in after-tax dollars being lost to the sands of time. Some common situations that may result in ‘lost’ after-tax dollars include:

- The Taxpayer Or Their Tax Preparer Changes Software. Most tax software programs today keep track of the after-tax dollars an individual has in their Traditional IRA from one year to the next by carrying forward amounts from previous years indefinitely until there is a change via additional after-tax contributions to the account or distributions that reduce the after-tax amounts in the account.

But while familiarity with tax software (and inertia) makes sticking with the same tax preparation software from year to year the preferred choice for most (whether they be professionals or individuals preparing their own returns), occasionally, the choice is made to change software providers.

In some cases, new software might mean starting fresh and entering everything from scratch. In other cases, particularly with professional preparers, data may be pulled from an old system and imported into a new system. However, such migrations don’t always pull all the data, particularly data that did not show up on a previous year’s return. Thus, when there is no need to update Form 8606 for several years, just pulling data from just the prior year’s return (or tax return software) can miss important Traditional IRA tax-basis information.

- The Taxpayer Changed Their Professional Tax Preparer. Another common way for basis to be ‘lost’ is when a taxpayer switches tax preparers after a year in which Form 8606 did not need to be filed. Notably, when individuals change tax preparers, the new preparer generally uses the previous year’s tax return (or sometimes the previous two, or even three years) as a guide for the current year.

In most situations, this allows the new tax preparer to pick up on any relevant items from prior years that could be relevant to the current year’s return, such as net operating loss carryforwards, capital loss carryforwards, AMT credit carryforwards, etc.

Unfortunately, though, while such amounts are reported on a taxpayer’s return annually, if a taxpayer with existing after-tax funds in their Traditional IRA did not add to, or reduce, those amounts in the previous tax year (or, perhaps, for many years), Form 8606 will generally not be included with the return, leaving the new preparer unaware of such amounts.

Accordingly, unless the taxpayer, themselves, makes their new tax preparer aware of their existing after-tax amounts – which, sadly, does not occur in many situations – the after-tax amount may be ‘lost’.

The Taxpayer Dies. A final common way that basis gets ‘lost’ is when a taxpayer with basis in their existing Traditional IRA dies. In fact, this scenario may often represent the greatest threat to the loss of after-tax dollars for retirees.

At the time of the taxpayer’s death, it may be many years since the last time Form 8606 was filed and, provided they did not add to or distribute after-tax funds in their Traditional IRA in the year of death, Form 8606 may not be required to be filed for that year either.

Ask yourself this, then… How in the world will the decedent’s beneficiaries know about the basis and their inherited IRAs? In many instances, those beneficiaries will be using a different preparer than the decedent’s, so the preparer will have no idea the after-tax funds exist. Beneficiaries are also more likely to move the funds to a new financial advisor, further reducing the list of people who may have any sense or recollection of the basis that exists in their inherited account.

Ultimately, the key point is simply that, because Form 8606 does not need to be filed annually, the ‘traditional’ tax preparation process of checking the past one or several years of tax returns still may fail to capture the reporting of prior years’ after-tax contributions. Which means even if the accountant (or diligent financial advisor) asks for the past several years of tax returns to review, it’s still possible to miss after-tax dollars in a retirement account unless the question is specifically asked (e.g., “Have you ever made after-tax contributions to your retirement accounts in years past?”!

Filing Form 8606 Each Year Minimizes The Chances Of ‘Losing’ Traditional IRA Basis

As is likely evident from the scenarios outlined above, sadly, it’s not all that difficult – or all that uncommon – for taxpayers to lose track of their Traditional IRA basis. Thankfully, there’s at least one way to dramatically reduce the likelihood of such an event.

Simply stated, whenever there is basis present in a client’s Traditional IRA, they should make sure that they file Form 8606 every year.

Admittedly, in general, taxpayers are better off giving the IRS only what is required, and not voluntarily filing additional forms. Form 8606, however, is an exception to that rule.

By filing Form 8606 each year (even when it is not required), a taxpayer can be sure that as long as each year’s return is reviewed and compared against the last year’s return prior to filing (which, again, is standard practice for professional preparers), the after-tax amounts in their IRA will always be front and center. In other words, the previous year’s return will always indicate the total amount of after-tax amounts in the client’s Traditional IRA.

Re-Creating Lost IRA Basis That Wasn’t Tracked

In the event that IRA basis (i.e., the cumulative amount of prior years’ after-tax contributions) has been lost (e.g., due to a failure to consistently, or even, file Form 8606), it becomes incumbent on financial advisors to help clients reconstruct such amounts to avoid double taxation.

There are a variety of ways to go about reconstructing prior years after-tax IRA contributions and the associated IRA basis, depending upon how basis was lost and/or what sort of records the client has maintained.

Find The Last Form 8606 That Was Filed

To the extent that a taxpayer previously filed Form 8606 to report after-tax amounts in their Traditional IRA, the easiest way to identify the current total of after-tax amounts in their Traditional IRA account is to see the total reported on the last Form 8606.

Today, it’s increasingly common for tax returns to be stored digitally. Accordingly, 20 years from now, if this problem arose, it may not be all that unlikely that a taxpayer or their tax preparer would have access to copies of all returns filed for the past several years. The same is true today, though, and it’s not terribly uncommon for taxpayers to have a few years of returns available for review.

In situations where a client with basis in their Traditional IRA cannot find a tax return with Form 8606 attached, one option would be to ask the IRS for a copy of the Return Transcript for previous years. Theoretically, this transcript should indicate any amounts reported on Form 8606. Unfortunately, though, it’s not uncommon to find Return Transcripts lacking such information, even when Form 8606 was included with the return.

To the extent that a client cannot find a copy of the last Form 8606 filed, or in the event that Form 8606 was never filed, or if the IRS’ copy of the Return Transcript doesn’t contain the Form 8606 details, basis must be ‘reconstructed’ in other ways.

Reconstructing Traditional IRA Basis From ‘Scratch’

To reconstruct Traditional IRA basis from ‘scratch’, clients need to ‘prove’ that nondeductible contributions and/or rollovers of after-tax funds from employer-sponsored retirement plans went into their Traditional IRA, and that such amounts are still in the account.

So, to begin reconstructing basis, one has to ask themselves, “How can I prove to the IRS what I have contributed to my IRA over the years if it wasn’t reported on a tax return?” Thankfully, there are a number of potential options.

Find Prior Custodial Statements With Contributions

One simple option is to simply find custodial statements showing applicable contributions. To the extent a deposited amount is a current- (or prior-) year IRA contribution, it will usually be listed as such in the transaction summary. Today, many custodians often have multiple years of statements available to their customers online, making this process easier than ever before. Not all custodians, however, are as accommodating.

Reference Prior Form 5498 Filings

To the extent that such statements are unavailable or difficult to obtain, another option for taxpayers who need to quantify and/or prove prior-year Traditional IRA contributions is to reference any Form 5498s (Individual Retirement Arrangement Contribution Information) that they may have received. Form 5498 is required to be filed by IRA custodians annually, with a copy sent to taxpayers, and the information reported on the form includes contributions made to the account each year.

Unfortunately, Form 5498 is not needed by taxpayers to file their income tax returns. In fact, it’s not even sent to clients until after the April 15 filing deadline!

Nerd Note:

You might wonder why Form 5498 gets sent out so late. In short, as noted above, the form reports IRA contributions. And since contributions can be made to Traditional IRA (and Roth IRA) accounts for the prior year up to April 15, custodians don’t even have all the information they need to complete the form until that date!

Unfortunately, the odd timing of Form 5498, coupled with the fact that it is not necessary to file a tax return, means that only the most diligent record-keeping taxpayers still have them, and more often the form is simply discarded or lost.

In such situations, there’s still one more trick up the knowledgeable advisor’s ‘sleeve.’

Request Wage And Income Transcripts From The IRS

While many advisors are familiar with the ability to request a Return Transcript from the IRS, fewer advisors are familiar with the Wage and Income Transcript that is also available. This transcript, which is also available online via the IRS’s website, provides a readout of all the information reported to the IRS on various forms, such as Forms W-2, 1099, 1098, K-1, and critically, for purposes of basis reconstruction, Form 5498.

Quantifying Prior Basis Contributions From (Reconstructed) Historical Records

Once proof of contributions to a Traditional IRA that were made has been obtained, the next step in reconstructing basis is to prove that the contributions (as determined using one of the methods outlined above) were indeed non-deductible.

This one’s actually pretty easy! Just look back at prior years’ tax returns and see if there was anything reported on the IRA deduction line! To the extent a taxpayer can find a copy of a return for one or more applicable years, they can again request a copy of the Return Transcript from the IRS for that year (or years).

If a taxpayer can show that both 1) a contribution went into their IRA for an applicable year, and 2) no deduction was taken for the contribution in that year, voilà! It must be a nondeductible contribution and thus… basis found!

Quantifying And Proving Prior Years’ Rollovers Of After-Tax Amounts From Employer-Sponsored Retirement Plans

As noted earlier, basis of a taxpayer’s Traditional IRA account can also result from a rollover of after-tax amounts from employer-sponsored retirement plans. The good news here is that the after-tax amounts inside the taxpayer’s plan should have been tracked by the plan administrator. And when the taxpayer took the distribution from the plan (that was rolled over to the Traditional IRA), their Form 1099-R, Quantifying And Proving Prior Years’ Nondeductible IRA Contributions, should have indicated both the gross amount and the taxable amount of their distribution.

Accordingly, reconstructing such basis is often as easy as digging through some old tax forms to find the Form 1099-R for the year the after-tax amounts were rolled over. Of course, such forms may not have been saved by taxpayers or may have been lost or destroyed.

In such situations, the Wage and Income Transcript option can, once again, come in handy. While not foolproof, the transcript should generally reflect both the gross amount and the after-tax amount of the client’s employer-sponsored retirement plan distribution that were reported to the taxpayer.

To prove that such amounts were rolled over to an IRA account, a taxpayer can take steps similar to those described above for proving Nondeductible contributions. Specifically, IRA account statements showing the deposit amounts can be used to verify the rollover, as well as copies of Form 5498, as the form separately reports rollover contributions.

Voilà. Basis found, again.

Most money in Traditional IRAs tends to be pre-tax money. Occasionally, however, after-tax amounts find their way into Traditional IRAs via nondeductible contributions or rollovers of after-tax funds previously held in an employer-sponsored retirement plan. Such amounts represent already-taxed money, which should not be taxed again (when distributed in the future).

But what should happen and what actually happens are not always the same and, unfortunately, from time to time, taxpayers end up paying tax on the same money twice. Sometimes, this double taxation stems from failing to report the after-tax amounts held in a Traditional IRA correctly from the start. In other situations, such amounts may have never been reported to the IRS at all!

Thankfully, in both situations, advisors can help clients rectify the problem and keep their income from being taxed only once (which, for most clients, is already more than enough!).

To the extent that Form 8606 has been filed correctly in the past and after-tax amounts still exist in a client’s Traditional IRA, advisors can suggest that Form 8606 be filed every year, even when it otherwise is not required! And in situations where basis was never reported properly, advisors can work with clients to pull the relevant documents, such as old statements, tax returns, and various IRS transcripts, so that the basis amounts can be reconstructed and reported on the next Form 8606.

At the end of the day, the key point is that the hope for a (partially?) tax-free distribution doesn’t have to be lost, even if a taxpayer’s Traditional IRA basis (currently) is!