Executive Summary

(Note: For an updated discussion of the final 2017 GOP Tax Plan, see Individual Tax Planning Under The Tax Cuts And Jobs Act Of 2017.)

With the Republican clean sweep of both the White House and both houses of Congress, momentum is building for 2017 to be a major year of tax reform, both for corporations, and for the individuals that financial advisors work with.

Accordingly, in today’s blog post, we delve in depth into both the likelihood of individual tax reform itself, and the details of the proposals from both President Trump, and the House Republicans. In fact, a deeper look reveals significant differences in both the style of tax reform between the President and House GOP proposals, as well as the deficits they imply – which itself could actually prove a stumbling block to getting legislation passed.

Nonetheless, both proposals would drastically simplify the tax brackets, from the current 7 tiers of tax rates, down to just three: 12%, 25%, and a top rate of 33% that kicks in at $225,000 (for married couples, or $112,500 for individuals). Both proposals would still keep preferential rates for capital gains and qualified dividends, although President Trump would retain the current 3 brackets (0%, 15%, and 20%), while the House GOP would simply make the rates 50% of the ordinary tax bracket (which means investment income would be taxed at 6%, 12.5%, and 16.5%).

However, when it comes to deductions, the proposals diverge substantially, with the House GOP suggesting the elimination of virtually all individual tax deductions except the mortgage and charitable deductions (paired with an expanded standard deduction), while President Trump would keep all the current itemized deduction rules, but cap itemized deductions (at $100,000 for individuals, or $200,000 for married couples) while also expanding the standard deduction even more (so only a moderate subset of people between the standard deduction and the cap would ever itemize at all).

Given all these differences, it remains to be seen whether individual tax reform will really happen in 2017, and whether key parts are compromised or delayed to accomplish corporate tax reform instead. In addition, despite now being the minority party in both the House and Senate, the Democrats still retain the ability to filibuster legislation, which will further limit the ability of Republicans to engage in permanent tax reform without compromising some concessions to Democrats. Or alternatively, the Republicans could ultimately pass individual tax reform as budget reconciliation legislation… which, under the Byrd rule, would have to sunset by December 31st of 2026, setting up a reprise of President Bush’s infamous sunset provision on his signature 2001 tax reform!

Individual Income Tax Reform – Are We “Due” In 2017?

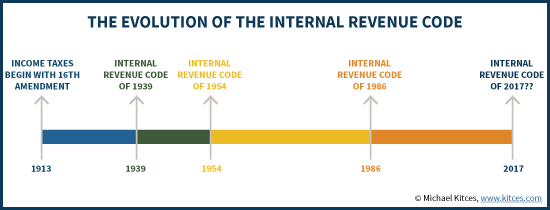

The current individual income tax system originated with the 16th Amendment to the Constitution, adopted in 1913, granting the Federal government to levy a tax on income (to supplement the existing Federal revenue from tariffs and excise taxes). The initial income tax rate started at 1% on the first $20,000 (in 1913 dollars), and rose as high as 7% on incomes over $500,000. In today’s dollars, that would be 1% on the first $463,000, and the 7% bracket would kick in at $11.5M.

Over the first few decades, Congress simply amended the tax system by adjusting and assessing new taxes in a series of seventeen Internal Revenue Acts, but in 1939 the series of tax rules were codified into the first formal Internal Revenue Code of 1939, and 15 years later in 1954 it was updated in the first wide-sweeping tax reform – a process of cleaning up what had been a generation’s worth of complex tax layers.

The Internal Revenue Code of 1954 remained the primary framework of the income tax system, but became increasingly complex – a combination of high tax rates (with top rates as high as 91% in 1954), combined with a wide range of tax deductions and shelters (so expansive that many high-income individuals still paid little or no taxes, which in turn led to the creation of the Alternative Minimum Tax). By the 1980s, another generation’s worth of complexity spurred the desire for a fresh round of tax reform, with the Tax Reform Act of 1986 eliminating a wide swath of deductions in exchange for drastically simplifying and reducing the tax rates (and bringing the top tax bracket down to 28%).

In essence, the income tax code has a steady pattern of growing complexity that tends to spur a once-every-generation desire to reform and simplify the process again. In this context, it is not entirely surprising that Congress is again considering tax reform – as 2017 will be 31 years out from the Tax Reform Act of 1986, which in turn was 32 years out from the Internal Revenue Code of 1954! Ironically, it might have happened even sooner, if the advent of the computer and tools like TurboTax hadn’t made modern tax filing so much “easier” for individuals and their accountants!

Tax Reform Proposals From President Trump And The Republicans

While tax reform has been bandied around for several years, the clean sweep of the Republicans in the House and the Senate, combined with Donald Trump’s victory in the Presidential election, suggests a high likelihood that tax reform could actually pass in 2017. Accordingly, it’s worthwhile to look in detail at the current legislative proposals, to understand what might be coming next year.

Technically, although Republicans swept the White House and Congress, the individual income tax proposals from President Trump are not fully aligned with the current “Better Way for Tax Reform” proposal from House Republicans (via the House Ways and Means Committee). Though since his campaign speech in August at the Detroit Economic Club, President Trump’s tax reform proposals have converged closer to the House GOP version.

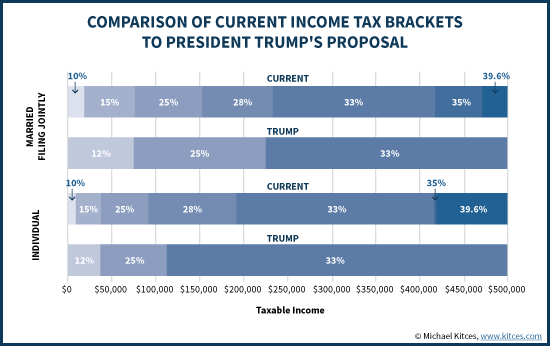

Proposed 2017 House GOP And Trump Tax Brackets

While President Trump’s original tax plan called for three tax brackets – 10%, 20%, and 25% – his current proposal would have a slightly different series of three brackets, with rates at 12%, 25%, and 33%. This is identical to the House GOP plan.

Notably, though, the House GOP plan is silent on where, exactly, the thresholds would come for each tax bracket, while President Trump’s tax brackets proposal would set the 12% bracket for married couples at the first $75,000 of income, the 25% from there up to $225,000, and the 33% bracket for all income over $225,000. (For individuals, the brackets would simply be 50% of these amounts.)

Notably, these thresholds are very similar to where the 2017 tax brackets are already projected, which include a 15% bracket up to $75,900, a 25% (and 28%) bracket that extends to $233,350, and then top rates (at 33%, and then rising to 35% and 39.6%) above that threshold. However, the shift would be somewhat more significant for individuals, where the end of the 15% bracket and beginning of the 25% bracket is already at $37,950 (similar to the $37,500 under President Trump’s proposal), but the 33% bracket currently doesn’t kick in until $191,650 today (whereas it would begin at $112,500 under the new system).

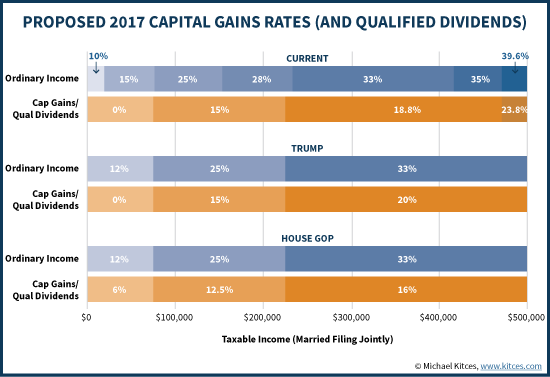

Proposed 2017 Capital Gains Rates (And Qualified Dividends)

Under President Trump’s proposal, the current 3-tier capital gains tax structure, with 0%, 15%, and 20% rates, would remain in place (and continue to apply to qualified dividends as well). The three capital gains rates would correspond directly to the 3 individual income tax brackets – thus, those paying 12% ordinary income rates would pay 0% capital gains, those in the 25% bracket would get the 15% capital gains rate, and those in the top 33% bracket would get the 20% rate. In addition, the 3.8% Medicare surtax on net investment income would be repealed.

By contrast, the House GOP proposal would simply allow all individuals to exclude 50% of their investment income – including both capital gains, qualified dividends, and even interest income – and then tax it at ordinary income rates. The fact that 50% of the income is excluded effectively means that all these types of investment income are taxed at half the ordinary income tax rates, which would mean capital gains (and qualified dividend, and interest) tax rates of 6%, 12.5%, and 16.5%. The House GOP proposal would also repeal the 3.8% Medicare surtax.

Notably, the House GOP version that treats bond interest as “investment income” eligible for preferential rates would be a significant tax savings on bond interest compared to today (and also to President Trump’s plan, which would continue to tax bond interest as ordinary income).

Proposed 2017 Standard Deduction, Personal Exemption, and Itemized Deduction Changes

When it comes to the treatment of deductions, President Trump’s proposals diverge even further from the House GOP.

The original proposal from President Trump would keep all itemized deductions, but enact a more aggressive version of the Pease limitation (phasing out many deductions at higher income levels). But perhaps given the reality that the Pease limitation is really just an income surtax, the current proposal shifts to simply capping itemized deductions at $200,000 (for married couples, or $100,000 for individuals). In addition, President Trump would consolidate the standard deduction and personal exemptions into a single, larger standard deduction of $15,000 for individuals, and $30,000 for married couples.

By contrast, the House GOP plan would keep the mortgage and charitable deductions (along with some incentives for retirement accounts and college savings), but eliminate virtually all other deductions altogether. In addition, the standard deduction and personal exemptions would again be combined into a larger standard deduction – in this case, $12,000 for individuals, $18,000 for individuals with a child, and $24,000 for married couples – which effectively means that those with a significant mortgage and /or a lot of charitable giving would itemize to claim those two deductions, but everyone else would just claim the standard deduction.

Notably, such limitations on deductions (under either proposal), combined with the lower tax brackets, would also render the Alternative Minimum Tax (AMT) a moot point, and thus the AMT would be repealed under both proposals.

Proposed New Above-The-Line Tax Deductions And Preferential Accounts For Families

In addition to President Trump’s proposed changes to the income tax brackets, capital gains, and the standard and itemized deductions, he has also proposed several new tax breaks that would apply specifically for families supporting dependents – either children or adult parents.

The first would be an above-the-line deduction for child care expenses, available for up to four children. The deduction would only be available for kids under age 13, and would be capped at the average cost of child care in the state for a child of that age. In addition, the deduction would apply for both third-party child care facilities, and the implied (average) cost of child care would still be deductible if care is provided by stay-at-home parents or (unpaid) relatives serving as caretakers.

This above-the-line deduction – effectively, an exclusion from income for a significant portion of child care expenses – would phase out at income levels above $250,000 for individuals, or $500,000 for married couples, but become available as a refundable credit for those with little or no income tax liability (through the Earned Income Tax Credit [EITC] system).

A similar above-the-line deduction would be available for “elder care” expenses for a dependent parent living in the home. The deduction for eldercare expenses would have a dollar cap of $5,000/year, though.

In addition, President Trump has also proposed a new Dependent Care Savings Account (DCSA). Similar to Health Savings Accounts, contributions would be tax-deductible (up to a $2,000/year limit from all sources), and growth would be tax-free (with no “use-it-or-lose-it” requirements). Ostensibly, tax-free growth could only be spent for related expenses, which would include expenditures to foster child development (e.g., after-school enrichment programs or even school tuition) or to support expenses for dependent parents (e.g., for in-home nursing or long-term care). To further encourage contributions, low-income households (eligible for the EITC) would be able to get an up-to-50% match (with a maximum of $1,000/year) by requesting to have their EITC credit directly deposited into the account.

Notably, these new tax deductions and credits, and tax-preferenced accounts, are unique to President Trump’s proposals, and are not included in the House GOP plan. In fact, the House GOP plan explicitly notes an intended goal to simplify (e.g., consolidate) the number of different types of retirement, college, and other tax-preferenced accounts, as opposed to creating new ones.

Assessing The Political Feasibility Of Income Tax Reform

Notwithstanding the fact that the Republicans control both the White House and both houses of Congress, it’s crucial to recognize that tax reform in 2017 is still not a “done deal” at all.

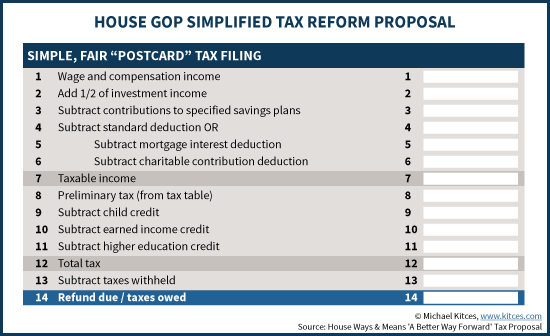

The first is that while both President Trump and the House GOP plan are represented as “tax reform”, in reality the President’s proposals do not really fit the classic tax reform mold of simplification. While the tax brackets themselves are simplified – from 7 brackets down to 3 – the proposal to keep special tax rates for long-term capital gains and qualified dividends, along with keeping the current complexity of itemized deductions (albeit with a cap), and the introduction of new above-the-line deductions (for child and dependent care) and new tax-preferenced accounts (with the DCSA), would ultimately maintain or even add to the complexity. By contrast, the House GOP tax reform aims to truly simplify the tax system, down to the point that many individual tax returns could effectively be filed on a postcard. In other words, it’s not clear that the House Republicans will acquiesce to pass President Trump’s version of “tax reform” over their own, and some compromise may be necessary.

In addition, it’s important to note that President Trump’s proposals are projected to create a substantial increase in the Federal deficit, even under “dynamic scoring” methods that consider the potential that positive economic growth (as a result of the tax cuts) could partially offset the economic impact. By contrast, the House Republicans have generally indicated a goal of keeping their tax reforms revenue neutral (at least on a dynamic scoring basis). Which means that even President Trump’s own Republican party may not be willing to vote in favor of his proposals as they currently stand, necessitating some further compromises. And of course, current reform proposals are looking at both corporate tax reform and individual tax reform, and it’s not clear whether some of the President’s individual tax proposals might have to be compromised to win corporate tax reform concessions.

And of course, there’s still the reality that while the Republicans do have a majority in both the Senate and House of Representatives, they do not have the infamous 60 votes required to avoid a filibuster, which means the Senate Democrats still have the potential to block substantive permanent tax reform. Which means the President and Congressional Republicans may still need to engage in further compromises to actually get legislation passed, whether on individual tax reform, corporate tax reform, or perhaps conceding their attempt to repeal the estate tax. Alternatively, the Republicans could aim to pass the legislation under the budget reconciliation rules, which can be accomplished with a simple majority vote. However, under the so-called “Byrd” rule for budget reconciliations, proposals that have a negative impact on revenue beyond 10 years must sunset at the end of that time period, which means if Republicans seek to accomplish tax reform this way, there’s a good chance that it will be scheduled to sunset on December 31st of 2026! (In point of fact, President Bush’s 2001 tax reform legislation also had a sunset provision at the end of 2010, for this exact same reason!)

The bottom line is simply to recognize that even with the Republicans holding the White House and both houses of Congress, and some similarities at a high level about how to reform the tax code (e.g., consolidating to three tax brackets), substantial disagreements still remain, both within the Republican party and between parties, that may need to be compromised. In addition, while the Democrats are now the House and Senate minority, they are not powerless in their ability to negotiate and try to extract at least some promises. Which means, ultimately, it remains to be seen whether tax reform can truly happen in 2017 or not!

So what do you think? Are we "due" for tax reform in 2017? Will President-Elect Trump and the House GOP be able to come to a compromise on reforms? Will Republicans be willing to further compromise in order to satisfy Democrats? Please share your thoughts in the comments below!

I’m all for simplification of the tax code and filing. Much less enthusiastic about cutting taxes for anyone given our budget problems. Trump would certainly modify the “postcard return” with at least one more line — Business Losses. As usual the devil is in the details. The current 1040 can be viewed as Total Income less adjustments = AGI less deduction = Taxable income. Apply tax rates. Subtract off credits. So really the postcard return is just a summary of the 1040 with various schedules still needed to support it.

Paul,

The point of the tax reform “postcard return” is that it literally would be that simple for the 1040 itself. Nearly 100 lines would consolidate down to barely a dozen. (You’d obviously still need supporting Schedules for some of the line items.)

That’s a key difference between the two – Trump’s version would not do much to consolidate line items, while the House GOP one would. That will be a point of negotiation/discussion within the party…

– Michael

I think, in reality, that the postcard is only for certain taxpayers – similar to the 1040EZ – but applicable to a slightly larger number of taxpayers. Anyone with income NOT from wages (W2 income) and investments will be using a longer form. Postcard is more a gimmick than a reality.

Anne,

Yes, ultimately income from businesses will ostensibly still require business schedules (Schedule C, Schedule E, etc.), and investment income still has to be at least itemized somewhere (currently Schedules B and D, and likely still?).

Nonetheless, the postcard version would actually be sufficient for a VERY large swath of taxpayers. And it’s worth noting that even if the supporting schedules feed up to it, the process actually would still be drastically simpler than the current two-pages-packed-full Form 1040.

We’ll see whether it happens… 🙂

– Michael

I would say less than half of the tax clients that I see would be able to use that form, unless, of course, they added lines that Schedules C, E, F, etc would actually flow TO. As written it doesn’t work. “Very large swath” is a bit of an exaggeration.

I’m all for tax reform; I just wish people with actual knowledge of the tax code and the broad lives of Americans were involved in it, rather than those in Congress.

You may clients who don’t reflect the reality of many taxpayers.

Bear in mind that most financial advisors work with the top 10%-20% of households or so.

Our clients are NOT typical/average Americans, and should not be viewed as representative of how tax reform impacts most Americans.

Remember, median HOUSEHOLD income across the country is about $52,000/year… THAT is the ‘typical’ middle-of-the-road (by definition) taxpayer.

– Michael

$52k is probably a little higher than the average income of my tax clients. Many are self-employed (including farmers). Many have rental income and/or royalty income (I live in a natural resources area). Many are retired with SS/RR, pension, and/or tax-free bond income. So that’s why that postcard looks to me like the authors are a little too ignorant of the complexity of the tax code.

But, of course, what concerns me the most, as a caring human being, is that lower and middle income households will be hurt by these tax changes while wealthy households will benefit (sometimes greatly). What’s good for me personally as a taxpayer is not as important to me as protecting the vulnerable.

I wasn’t aware of the potential for an above-the-line deduction for child care provided by a SAH parent. Similar to the post-AGI child tax credit I guess, but interesting.

Seen/heard anything about self-employment taxes? Sure would like those to go down. 🙂

Hey michael

thx for the post.

do you have any insights into what retirement items would remain deductible under the House plan or what happens to carried interest. Also Trump’s $200,000 limit on itemized deductions – it’s not clear to me – do you get to deduct up to $200,000 from income or do folks with over $200,000 in income lose the deductions?

thank you for any further insights!

DRC,

In terms of retirement items being deductible, the House plan has generally said it wants to ‘consolidate’ the number of retirement account types, but we don’t know beyond that.

As for carried interest, Trump has said he would convert it to ordinary income treatment. The House GOP plan hasn’t taken a clear position (that I’m aware of, at least).

In terms of the itemized deduction cap, it appears to be a proposal to cap the actual dollar amount OF itemized deductions. Not simply reapplying the Pease limitation phaseout at a lower income threshold.

– Michael

thanks – very helpful!

Michael,

Any thoughts/information about what happens with home sale gain exemptions?

Thanks,

David

No proposed changes to the exemption itself. And to the extent the income is exempted, it never hits your tax return in the first place, and thus the exempted gain wholly outside the scope of these proposals.

– Michael

1) Munis – I take it nothing is happening here

2) Exemptions – Will this go away and be considered part of the standard deduction?

3) SS Income – Will this be simplified?

Harvesting losses, accelerating deductible investment fees, and making your January mortgage payment in December appear to be the right strategies if your itemized deductions are below the 24K or 30K thresholds. Worst case, you should essentially “break even” over 2 years on tax benefits.

JC,

Currently no substantive proposals I’ve seen to change Muni treatment, or the taxability of Social Security income.

Personal exemptions would be wrapped into the (new, higher) standard deduction.

– Michael

So the GOP plan eliminates refundable credits? Overall, it seems to increase the burden on lower and middle income households while giving a nice boost to upper income households. Or am I missing something?

One thing I do like is that these plans discourage large families. It’s about time we address the population growth issue.

The worst idea is eliminating the Medicare surtax. Gotta wonder (worry) what their plan is for Medicare!

I think Trump, who is a Republican in name only, will find that even a “sweep” will not end the deadlock in Washington. Compromise has become a dirty word. Plus Democrats, if wise, will adopt the Republican obstructionist policy.

@Michael_Kitces:disqus,

Any thoughts on what would likely happen to the credit for prior year minimum tax (https://www.irs.gov/uac/form-8801-credit-for-prior-year-minimum-tax-individuals-estates-and-trusts)?

I’m likely to incur significant deferral AMT in 2016 which I would likely be able to recoup in 2017 and 2018. If the AMT is eliminated, do you think the credit for prior year minimum tax would still be available, or will that potential credit be lost?

Joshua,

My gut offhand is that the AMT credit carryforward would still be allowed, as technically it’s a credit against your REGULAR tax liability (it just happens to be sourced from a prior-year AMT liability). If we eliminated the AMT tax line, the credit would/should still be there. It’s also logical to keep it, simply because eliminating it would cause a situation of double-taxation (as avoiding double-taxation of gains is the very reason WHY it exists in the first place).

There’s nothing to guarantee it sticks around. Congress can change the rules any way they want. But I would view it as an odds-on bet that it sticks around, even through AMT reform.

– Michael

What about the Adoption Tax Credit? Where does Trump stand on somethingg so valuable to so many.

What happened to the idea floating around a few years back about exempting some annuity income from taxation to encourage annuitization?

The proposals are not that far apart, and you have to remember the name of Trump’s book, The Art of the Deal.

The final vote on Steve Mnuchin as Treasury Secretary is scheduled for 7 PM Today!

I see a compromise, a deal, being made within a month, probably a couple weeks!

It looks like minor modifications to me (not reform). I am not impacted but it looks like I will just continue to have an incentive to stay under $75000 in earnings. No biggy for the working class. Looks like nothing but a lot of smoke and mirrors behind this big dog and pony show. I haven’t had a raise since 2008 and last year my out of pocket for Insurance and deductibles was half my income because I have to file as an individual and do not qualify for Obama care. I was hoping maybe a reduction in my income tax rate would help me with the huge inflation rate I am suffering with all the insurance, RE Tax and other big cost of living increases.

A side note to the not-passed AHCA. One of the last minute changes was to make the repeal of the Medicare Surtax and the NIIT retroactive to January 1, 2017. This probably sends a signal. One also has to wonder whether repeal of these taxes, independent of any health care legislation, will be in the tax reform package.

Not uncommon for tax cuts to occur retroactively to the beginning of the year. A similar effect happened with several of President Bush’s tax cut provisions in 2001 and 2003.

The challenge at this point is that repealing the NIIT in health care reform was important, because it meant a no-NIIT baseline for tax reform. Without AHCA, repealing the NIIT will be part of the CBO scoring on tax reform, which will make it ‘more expensive’ and harder to get done. That was a part of why tax reform was initially scheduled to come after health care reform.

– Michael

Removing personal exemption and increasing standard deduction will only serve to increase taxes on middle class itemizers with between 17400 and about 40k or so in deductions. And also penalize itemizers who donate large sums to non profits. Not a good move as it changes virtually nothing as far as IRS revenue, and penalizes modest itemizers and big philantropists and charities.

It will only encourage tax fraud and fudging deductible expenses for those who are being penalized for modest deductions.

If they really are removing the personal (and family) exemptions, this would actually REDUCE fraud, since a lot of fraud develops from improper claims of “dependents”. As far as charitable donations go, it is always more beneficial to invest in your company (or yourself), than to donate money. If anyone donates *because of* the deductions, they are doing it wrong, and this is actually doing them a favor. The only reason charitable donations may actually surpass re-investing would be if you hit threshold limits, and need the charitable donations to funnel the money through a foundation and back to your company, which… is further fraud that would be reduced by this plan! 😀

You have made a sweeping overgeneralization. Fraud happens in all tax situations. Claiming additional personal exemptions for dependents will be one of the if not the most difficult pathway since you will need a valid SS number. The issue may come up in custody cases at most. Furthermore, the measure is clearly regressive as households with children spend more of their income on goods. Taking that money away to streamline to some kind of one size fits all reform (and appease some strongly opinionated childless couples who believe its somehow unfair to allow personal exemptions for children) will effectively take money from the families thereby reducing consumer spending substantially. Kills two birds with one stone by also punishing already existing families in addition to providing financial incentive to stay childless.

Give seniors on social security a break and stop taxing up 85% of social security received.

I’ll drink to that. You work all your life paying into SS and then they take out $109. monthly for medicare insurance and then tax a portion of the gross amount at 50% or 85% counted as income depending on your AGI. You plan, you save, you put money away for retirement and then the government punishes you for being successful. Those who lay on their ass and don’t plan or save get zero tax. SS started out being a tax-free old age benefit and then Congress decided to tax it at 50% and then later upped it to 85%. What is next … 100%? What we have here is a tax on a tax where the government is paying itself through your account.

This is a “back door” means test and the threshold was not indexed for inflation. Thanks to Greenspan, Reagan and Clinton. Further, They raise the standard deduction and Remove Individual exemptions The incomes under $100K get little if any tax relief and in some cases pay more.

SSI is only taxed if they receive other income, meaning they are not solely reliant on that SSI. Also, it’s not taxed at that rate. Which means 15% will ALWAYS be tax free. Even if the *maximum* of 85% is taxed, it is only taxed at their applicable tax rate. Knowledge is power.

We seem to forget that when “we the people” entered into SS agreement with our first paychecks back in the 1970 early 1980s, all SS income received by current recipients was NOT subject to federal taxation. It was no until the 1980s that SS became federally taxable in chunks which eventually led to current taxation of up to 85 percent of your SS income…

Being in one of the highest state taxed areas, I think state tax should still be a reduction

Since state tax is accounted for in itemized deductions, you should follow updates on that aspect of the reform. It sounds like the standard deduction is going to be increased to a point where itemizing won’t be necessary for a majority of individuals anymore.

Michael

What do you think will happen to spousal support as a deduction? Thanks

It’s not really a deduction as much as it is an adjustment to income. Since the payee must claim this income, the payor can reduce their income by the same amount. I imagine this will remain the same, since this is just a way to calculate your taxable income.

Long Term Capital Gains – As far as I can tell, the current proposal would continue with Zero Percent on Qualified Dividends and LTCG for those in the new 10% tax bracket having an AGI of $75,000 or less. To the best of my knowledge, the actual From & To income amounts for the 10-25-35 percent brackets have not yet been specified. Also it is yet to be seen if the proposed tax modifications will be passed by Congress.

just in case you need a system programmer to help you fix you credit score or clear any collections on your score,or you need help to reduce your tax rate i can help you also to hack to reduce the rate of your tax and which means you will start paying lower tax rate just contact me on the mail above,i am highly at your service any time

Great…as an individual making about $115K in a high-cost state, I’m screwed by Trump’s plan as it raises my tax rate from 28% to 33%. What’s the incentive to work hard to move forward and earn more? None! May as well find a way to suck off the government.

Take a 2k paycut and go under the bracket so you pay less in taxes

I am all for having only 4 kids to be used as exemptions. People are having too many kids, and are using the system for their advantage, and it will hopefully help with population control.?

Ask us how you can reduce your corporate and personal liabilities through Safe Harbor … Contact a

Financial Advisor today about your retirement plan.

After reviewing the proposed tax reform, it looks like I will paying more and correct me if I am wrong.

Scenario under the current tax code:

Married Gross Income: $ 55000

Less Exemptions 8100

Less Itemized Deduction 30,000

Taxable Income $16,900

Tax (10%)

“Standard deduction” goes to $24,000 plus child tax credits

Standard deduction goes to $24K but that doesn’t help someone who itemizes. We lose out because we no longer have an exemption. The American dream to own a home has gone to pot. Guess Trump found a way to burst that housing bubble. No incentive to go out and buy a home when you wind up paying more in taxes.

After reviewing the proposed tax reform, it looks like I will be paying more but correct me if I am wrong.

Scenario under the current tax code:

Married Gross Income: $ 55000

Less Exemptions 8100

Less Itemized Deduction 30,000

Taxable Income $16,900

Tax (10%) $ 1690.00

Under the proposed tax reform:

Married Gross Income $ 55000

Itemized Deduction 30000 (exemptions are eliminated)

Taxable Income 25000

Tax (12%) $ 3,000

With the proposed tax reform I will be paying $ 1,310 more than the existing tax code

How about a GEOMETRIC TAX CODE.

Homostasius is not a GREEK G_D

How about a GEOMETRIC TAX CODE ?

Stop treating US like were as daft as a ….. member of the federal government.

Seniors with $45k income and above are getting totally screwed… Social Security as taxable income needs to be stopped with the current proposal. Most states don’t tax SS income… Why would Fed tax SS?… That’s double or triple taxation on seniors!