Executive Summary

From the moment the Roth IRA was created in the late 1990s, it has been a popular vehicle to generate future tax-free growth and income, whether by contributing to the account on an ongoing basis, or even doing a Roth conversion of an existing IRA or other pre-tax retirement account.

Yet the caveat is that the decision to contribute or convert to a Roth IRA incurs an immediate tax liability. And in the extreme, a large Roth conversion can generate so much taxable income that it actually drives up the IRA owner’s tax bracket to the point that the transaction becomes wealth destructive!

Fortunately, though, the decision to do a Roth conversion doesn’t have to be “all or none” – and in fact, not only is a “partial” Roth conversion permitted, but in practice it’s often the optimal strategy, allowing retirement account owners to convert just enough to fill the lower tax brackets, without causing “too much” income that would trigger the top tax brackets.

In fact, the Roth recharacterization rules make it feasible to precisely fill the bottom tax brackets, but not a dollar more, by converting more than enough to fill the lower tax brackets each year, and then doing a partial recharacterization to back into the optimal partial Roth conversion amount after the year is over!

How To Do A Partial Roth IRA Conversion – It Doesn’t Have To Be All Or None!

Beginning in 1998, taxpayers have been permitted to both contribute to a Roth IRA (subject to income limits), and to convert existing assets in a traditional pre-tax IRA to a Roth. In 2006, under the Pension Protection Act (and the subsequent IRS Notice 2008-30), the Roth rules were further expanded to allow conversions of pre-tax 401(k) plans directly to a Roth IRA. And in 2010, delayed provisions from the Tax Increase Prevention And Reconciliation Act of 2005 finally took effect, eliminating Roth conversion income limits altogether, allowing anyone with a pre-tax retirement account – IRA or 401(k) (or any other employer retirement plan) – to convert to a Roth IRA (or even intra-plan to a Roth 401(k)).

Notably, though, while the Roth conversion rules are often discussed as though an entire IRA or other pre-tax retirement account might be converted, the reality is that IRC Section 408A(d)(3) simply stipulates that whatever dollar amounts are distributed to a pre-tax IRA and rolled into a Roth will be treated as taxable as a Roth conversion. There’s no minimum or maximum regarding how much must be converted. In other words, a Roth conversion doesn’t have to be all or none; it’s up to the investor/taxpayer to decide whether to convert everything, or to simply do a “partial Roth conversion” instead.

Similarly, under the Roth recharacterization rules of Treasury Regulation 1.408A-5, any Roth conversion amounts that are rolled back to a pre-tax IRA (in a timely manner by the following-year-October 15th deadline) are no longer taxed as a Roth conversion. Yet again, there’s no requirement that a recharacterization be all or none; instead, the account owner can recharacterize as little or as much as desired (with the caveat that all amounts recharacterized must share in a pro-rata portion of any gains or losses, unless the Roth conversion was done to separate accounts in the first place). Thus, even a pre-tax retirement account that is fully converted to a Roth can end out being a partial Roth conversion, if partially unwound via a partial recharacterization!

The fundamental point: Roth conversions really don’t have to be an all-or-none transaction, and can either be done as a partial Roth conversion on a prospective basis, or partially recharacterized after the fact to create the same result. And in practice, doing a partial Roth conversion – or rather, a series of them – is often the best way to maximize the long-term value of a pre-tax retirement account!

Using Partial Roth Conversions To Fill Lower Tax Brackets

The virtue of doing a Roth conversion is that once converted, subsequent growth in the account can be spent tax-free as a qualified Roth distribution in the future. The caveat, of course, is that doing the Roth conversion forces the value of the account to be reported as income today, triggering an immediate tax liability. To come out ahead, the current tax rate at the time of conversion must be lower than what the marginal tax rate would be in the future.

Yet given that a Roth conversion itself is income for tax purposes, a large single-year Roth conversion can become self-defeating; because tax brackets are progressive (the higher the income, the higher the tax rate), if enough dollars are converted at once, so much income is created that the taxpayer is driven into the top tax brackets. Which ironically means there really is such thing as doing “too much” of a Roth conversion, where the effort to create a large tax-free account all at once with a huge conversion drives up tax rates to the point of making it less desirable (or outright destructive!) in the long run to have done so!

Example 1. Jeremy and Linda’s current combined income after deductions is $60,000, putting them in the 15% tax bracket. They have a $500,000 IRA that they are considering whether to convert to a Roth IRA to avoid what is anticipated to be a 28% marginal tax rate in the future when their RMDs begin. If they convert the entire account, though, their taxable income will be increased to $560,000, driving them up into the top tax bracket of 39.6%. Which means a Roth conversion that may have been appealing initially (converting at 15% to avoid a future 28% rate) becomes very unappealing by the end (as the last ~$100,000 crosses into the 39.6% tax bracket today, just to avoid a lower 28% rate in the future!).

In this context, the partial Roth conversion suddenly becomes appealing. Converting the entire account may drive the couple’s marginal tax rate into the top 39.6% bracket, which is so high that they probably would have been better off just leaving the money as a pre-tax IRA and spending it in the future at a lower rate! A partial Roth conversion, on the other hand, allows the couple to create just enough income to be subject to the lower tax brackets, while stopping before they reach the upper brackets.

Example 2. Continuing the prior example, Jeremy and Linda could convert as much as $14,900 and still remain within the 15% tax bracket (which tops out at $74,900 for a married couple in 2015). Alternatively, the couple might choose to convert as much as $91,200, filling up the remainder of the 15% bracket and all of the 25% bracket (which ends at $151,200 for married couples filing jointly), but stopping before they ever actually hit the 28% bracket today. Thus, the couple is avoiding the top tax brackets today, while also avoiding an anticipated future 28% tax bracket for those converted dollars paid at 15% or 25% now!

The end result of the strategy is that the couple can convert exactly enough to ensure that their IRA is subject to the lower tax brackets today, but only those lower and more favorable tax rates. Of course, given that there’s only so much room to convert until the higher brackets are reached, this means the bulk of the couple’s IRA may remain in pre-tax form. Yet given a multi-year – or even a multi-decade – time horizon before they need to spend/use all the money, this isn’t necessarily a problem. It simply means the couple will repeat the partial Roth conversion systematically each year in the future as well, continuing to whittle down the size of the pre-tax IRA (and grow the size of the Roth IRA), while ensuring each year that the conversions are modest enough to avoid ever hitting the top tax brackets.

Ultimately, then, the goal of partial Roth conversions is to find a balance, where the converted amount is low enough to avoid top tax rates today, but not so little that the remaining retirement account balance plus compounding growth causes it to be exposed to top tax brackets in the future, either.

Identifying Low Tax Rate Opportunities For Partial Roth Conversions

Clearly, one challenge to the strategy of Roth conversions is that the benefits are highly dependent on what future marginal tax rates turn out to be, in a world where we don’t necessarily know that outcome for certain as of today. Projecting future wealth and known future income streams can be a good starting point for estimating a future marginal tax rate (e.g., what will tax rates be for the retiree who already has Social Security benefits, portfolio interest and dividends, real estate or other passive income sources, and/or Required Minimum Distributions [RMDs]), but clearly some uncertainty remains, not the least because Congress could just outright change the tax laws between now and then (although even higher tax rates in the future is not a guarantee that Roth conversions are a good idea today!).

Nonetheless, we can know what the marginal tax rate will be for this year, and in practice there are many situations where that tax bracket is low enough that we can be virtually certain it is favorable compared to almost any likely future.

For instance, if someone experiences a layoff that leaves them without employment income for most of the year, his/her tax bracket may be just 10% or 15%, a rate that’s hard to beat in any foreseeable future as long as there’s any income tax system. In the extreme, if deductible household expenditures (e.g., property taxes, charitable giving, the deductible portion of advisory fees, etc.) continue while there’s no income for the year, taxable income could even be negative, which means the partial Roth conversion would be tax-free just absorbing the otherwise-unusable deductions (which are permanently lost if not offset against negative income in the same tax year!).

Similarly, a business owner that experiences a significant (pass-through and otherwise deductible) business loss might have an ‘unusually low’ income year where a partial Roth conversion can benefit at the low rate. Alternatively, a household that has an unusually large amount of deductions (e.g., for a significant charitable contribution, or perhaps paying a large outstanding state tax liability balance from the prior year?). And notably, because deductions are applied against ordinary income first and capital gains second, someone with high total income due to capital gains could still be eligible for low tax rates on a partial Roth conversion (although this can still phase out the benefits of 0% long-term capital gains tax rates), and/or have their deductions apply favorably to shelter further partial Roth conversions.

Systematically Repeating Partial Roth Conversions Of An Existing IRA

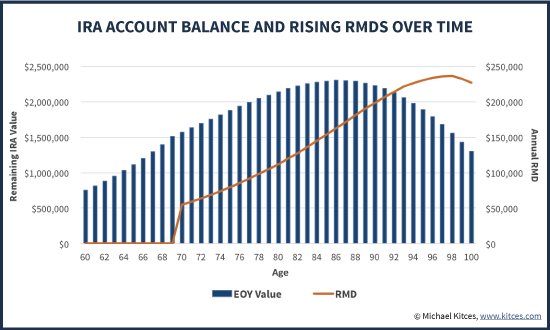

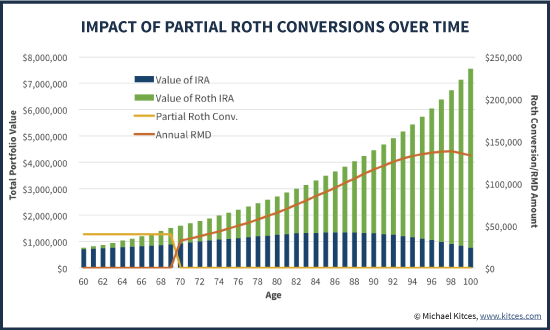

For those transitioning into retirement, the years after wages and employment income end, but before Required Minimum Distribution (RMD) obligations kick in, can also be especially appealing for timing partial Roth conversions. For instance, a retiree in their early 60s might do a partial Roth conversion each year throughout their 60s, whittling down the size of a pre-tax IRA over time, such that by the time RMDs actually begin at age 70 ½, there isn’t much of a pre-tax IRA left!

Example 3. Betsy is a single 60-year-old female who recently retired with a $20,000/year Social Security survivorship payment and a $40,000/year survivorship pension from her deceased husband. Betsy also has a $200,000 brokerage account, and a substantial $700,000 IRA (the combined value of her original IRA, and a spousal rollover from her deceased husband’s 401(k)). In a decade when her RMDs begin, Betsy will face RMDs of upwards of $50,000/year (with an 8% growth rate in the IRA between now and then), propelling her into the 28% tax bracket even after her moderate deductions; by her 80s, the RMDs are projected to be more than $100,000/year, topping out the 28% rate and approaching the 33% bracket!

To manage the exposure, Betsy decides to do a partial Roth conversion of $40,000 each year for the next 10 years, which after her deductions just barely fills up her current 25% tax bracket, but stops short of the 28% tax rate. Repeated each year, this gives Betsy the opportunity to significantly whittle down her overall IRA exposure; in fact at this pace, her pre-tax IRA will still only be about $900,000 by the time her RMDs begin, which will produce RMDs of barely $35,000, allowing her to remain in the 25% tax bracket! In the meantime, Betsy will have accumulated a tax-free Roth IRA projected to have grown over $700,000 by age 70 ½!

The end result – by doing systematic partial Roth conversions for several years in a row, it’s possible to remain in (and fully utilize) the lower tax brackets, while avoiding higher tax rates today, and whittling down pre-tax retirement accounts to the point that RMDs won’t be subject to higher tax rates in the future, either!

Filling The Lower Tax Brackets – Using Roth Recharacterizations To Avoid Losing Them

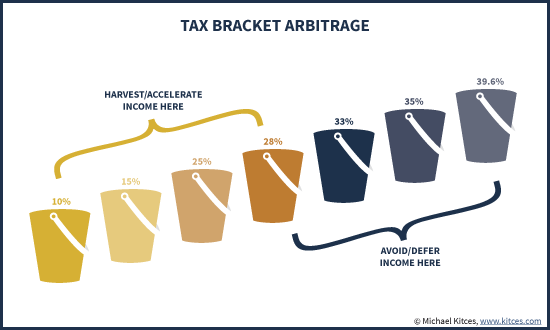

The key aspect of the systematic partial Roth conversion is that deferring “too much” income – by accumulating and compounding an IRA and never withdrawing or converting it – drives someone into top tax brackets, and there’s no way to go back after the fact and use lower tax brackets that may have been available in prior years. In essence, a low tax bracket available today is “lost” forever if not actually used in the current tax year. Which means for those who are already facing top tax rates, it makes sense to defer or avoid income, but for those eligible for lower tax brackets, it’s an opportunity to harvest income, accelerating future income into today’s lower marginal tax rate.

And notably, since the opportunity to fill low tax brackets is a “use it or lose it” scenario – because taxable events must actually occur in the current tax year to count in those income buckets – December 31st becomes a firm deadline for any annual low-tax-bucket-filling strategies.

Unfortunately, deciding how much income to create before the end of the year can be challenging, because sometimes you don’t know what income (and deductions) will end out being until the very end of the year, leaving little or no time to do the calculations and the ‘last minute’ conversion.

In this regard, the particular strategy of doing Roth conversions with a planned recharacterization becomes appealing. Because the Roth recharacterization rules allow a Roth conversion to be undone in the following tax year (as late as October 15th), those who aren’t certain how much to convert to fill the bottom tax brackets can simply convert more than enough now, and then recharacterize the excess later!

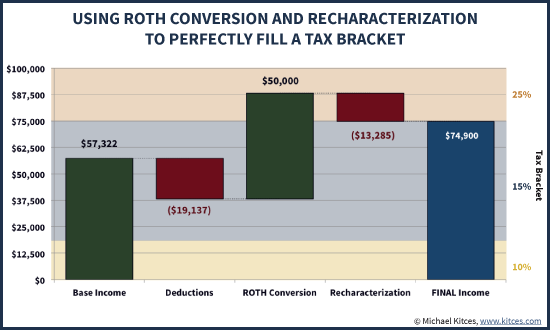

Example 4. Donald and Donna are retired and have approximately $50,000 of current income and $15,000 of deductions, and want to do a Roth conversion to fill their 15% tax bracket (which ends at $74,900 of taxable income). However, their nearly $1,000,000 portfolio in a taxable account holds several mutual funds that could make end-of-year capital gains and dividend distributions, and they’re not certain how much (if any) will be distributed until very late in the year.

To avoid the risk that the distributions will be small enough to allow room for a Roth conversion but come so late in the year there’s no time to do one, Donald and Donna do a partial Roth conversion, now, of $50,000, which would be sufficient to fill their 15% tax bracket even if total distributions from their investments turn out to be $0.

After the close of the tax year, it turns out that Donald and Donna have total income of exactly $57,322 and total deductions of $19,137. Their taxable income is $38,185, which means they could have converted exactly $36,715 of their IRA and still remained within the 15% tax bracket. Accordingly, they recharacterize $13,285 of their $50,000 Roth conversion (plus or minus the pro-rata share of any gains/losses from that $13,285 conversion), which results in a taxable Roth conversion of $50,000 - $13,285 = $36,715, the exact dollar amount they wanted to convert.

The end result of this strategy is that even in situations where there is uncertainty about exactly how much to convert, the precise amount of the desired partial Roth conversion can still be accomplished, by converting more than enough up front, and then recharacterizing the excess afterwards! Or in the extreme, the couple could convert even more investments, across multiple asset classes, into separate accounts, and then recharacterize everything except the account that is up the most, in the exact (original) dollar amount desired to fill the appropriate tax bracket(s)!

Carefully Evaluate True Marginal Tax Rates For Potential Partial Roth IRA Conversions

Of course, the caveat to all of this is that it’s still necessary to determine the ideal tax bracket, or amount of income, to partially convert to a Roth in the first place. Ultimately, this is driven not only by an estimate of the future marginal tax rate when the funds will be withdrawn (or if the IRA will be unused and bequeathed to the next generation, the marginal tax rate of the IRA beneficiaries instead!), but also the marginal tax rate today, including the impact of all the various income-related factors that can drive up marginal tax rates, from the impact of PEP and Pease, to the phase-in of taxable Social Security benefits, to Medicare Part B and Part D premium surcharges, AMT exposure, and more. In other words, just because someone is in the 25% tax bracket doesn’t necessarily mean he/she is really subject to a 25% marginal tax rate, as it could be much worse!

It’s also important to recognize and remember that Roth conversions will themselves impact future tax rates, as the diminishment of a pre-tax IRA reduces future tax exposure! For IRA accounts that are projected to be large – where RMDs can propel the IRA owner into the top tax brackets – a partial Roth conversion is appealing to benefit from lower tax brackets today and avoid the higher ones in the future. But notably, if the entire IRA is converted to a Roth, it eliminates all future tax exposure, which means the future marginal tax rate may become so low that the last IRA dollars weren’t going to be taxable anyway! In other words, the greater the (partial) Roth conversion, the less need there is to convert the remainder!

The bottom line, though, is simply this: the availability of low tax brackets is an opportunity that should be utilized before it is lost, and the partial Roth conversion (or a Roth conversion followed by a partial recharacterization) is a flexible strategy to ensure that those low tax rate buckets never go to waste!

So what do you think? Do you engage in partial Roth conversion strategies systematically with your clients every year? How do you figure out the amount to convert each year?