Executive Summary

Enjoy the current installment of "weekend reading for financial planners" – this week's edition kicks off with the huge industry news that Envestnet has purchased PortfolioCenter from Schwab, just months after Schwab announced that it was not going to create a full-scale upgraded cloud replacement to its still-popular platform, in what appears to be a tremendous strategic win for Envestnet (given both that Tamarac itself is built on top of PortfolioCenter, and that the acquisition gives Tamarac over 2,000 "new" PortfolioCenter desktop users to cross-sell their Tamarac cloud-based solution to).

Also in the news this week is a study from Cerulli finding that consumers do increasingly show a preference to pay their advisors with ongoing AUM fees or retainer fees... unless they're mostly self-directed, in which case they'd actually prefer to pay commissions on each transaction as needed instead. And there's also a fascinating recap of industry lobbyist spending in financial services, which finds that product manufacturing and distribution firms (e.g., fund companies, insurance and annuity carriers, and broker-dealers) spent more than $15M in lobbying last year, while advisor-centric organizations spent less than $300k... which goes a long way to explaining why the industry manages to keep defeating or watering down each proposed fiduciary rule!

From there, we have several articles on marketing, from tips on how to actually pick a specific niche or otherwise select an ideal target client (from the seemingly endless number of available choices), to why factors like "having at least $500,000 in investable assets" or "is a delegator" may be important "acceptance criteria" to selecting a new client (or not) but should not be part of the description of your ideal client profile (because they don't define needs that you solve that would make you more referrable), and a series of tips on what you must consider when designing a good financial advisor website.

There are also a number of investment articles this week, from two articles that look at how the recent launches of zero-fee mutual funds are not actually attracting significant new asset flows (suggesting that perhaps consumers are either becoming wary of "free" from financial services firms, or simply that index funds have become "cheap enough" that price is no longer going to be the driver it once was), to another that looks at recent criticisms against index funds from regulators wondering if perhaps there are now too many behind-the-scenes conflicts for index fund providers in how they construct and execute their index funds.

We wrap up with three interesting articles, all around the theme of personal productivity and efficiency: the first is a fascinating look at how Aaron Klein of Riskalyze manages his increasingly busy email Inbox (and why despite the near email overload, he views email as his "secret weapon" and not a burden); the second explores the benefits of time-blocking, where entire days are set to one type of task (e.g., client meetings) or another (e.g., internal/staff meetings and prep) to reduce the amount of task- and context-switching that ultimately degrades personal productivity; and the last is a review of the recent book "Atomic Habits" by James Clear, which dives into how to actually change and improve your habits for the better, noting that improving by "just" 1% per day leads to a massive 3,700% improvement in the span of a year, and emphasizing that the key to achieving even massive long-term goals may not be in focusing on the long-term goal itself, but simply trying to establish the small short-term habits that can help you get on the right track... and then let the compounding of that habit carry you the rest of the way!

Enjoy the "light" reading!

Schwab Advisor Services Tosses Its PortfolioCenter Platform To Envestnet (Brooke Southall, RIABiz) - This week, Schwab announced that it has sold its portfolio performance reporting solution PortfolioCenter to Envestnet, for an undisclosed fire-sale sum that was reportedly so little that the price was "immaterial." The sale of PortfolioCenter comes just 5 months after Schwab announced that it was halting a four-year effort to relaunch PortfolioCenter to the cloud back in September, and instead was going to focus on a scaled-back internal solution to be dubbed PortfolioConnect that would be free for Schwab advisors. From Envestnet's perspective, the purchase isn't entirely surprising, though, as Tamarac had built its own reporting engine on top of PortfolioCenter - and thus couldn't risk having Schwab shut it down altogether - and in practice the acquisition brings 2,300 new PortfolioCenter RIA prospects for Envestnet to solicit to switch to its own Tamarac solution (which has 1,000 RIAs as well). In fact, despite fears already emerging from PortfolioCenter users that the sale means the software's inevitable demise, Southall notes that because PortfolioCenter is so integral to Tamarac itself, it's actually more likely to stick around longer in the hands of Envestnet than it might have if Orion or Black Diamond had purchased it. Nonetheless, it's rumored that as soon as Schwab announced it was not going to support a full cloud-based rebuild and transition for existing PortfolioCenter users last September, many have already been leaving for alternatives, and the transition to Tamarac will no doubt put even more PortfolioCenter-using firms into play as they decide if they want their future to be with Envestnet and Tamarac (or not).

Advisory Fees Push Commissions Further Into The Background (Jeff Benjamin, Investment News) - In a recent new report from Cerulli Associates covering more than 8,000 retail investors with at least $250,000 of investable assets, a whopping 61% who want to work with an advisor on an ongoing basis would prefer to pay AUM fees, as contrasted with 22% who want to pay a retainer fee, and only 13% who want to pay via commission (and 4% who prefer hourly). Notably, though, this strong preference for AUM fees was only preferred for those who want to delegate to an advisor in the first place; for those who are self-directed, 56% would rather just pay a commission as needed when buying a product, compared to only 16% who would choose an AUM fee and 14% who would prefer an hourly fee. Similarly, clients who just want one-off advice for a special event also prefer to just pay a transactional commission at the time (48%) over paying an AUM fee (30%) or a retainer fee (17%). In essence, the data suggests that it's not a matter of whether fees are better than commissions (or vice versa), per se, but that more ongoing-advisor-relationship-oriented clients prefer AUM or retainer fees, while those who are more self-directed and only occasionally and "transactionally" want advice as needed would prefer to pay as they go (via either commissions or hourly fees). Though overall, the data does show a rising willingness to pay AUM fees over commissions (with 36% of investors overall preferring AUM fees, up from 27% in 2011), even as alternative fee structures are on the rise as well (with only 10% of investors aware of other fee-only models in 2011, up to 34% in 2018).

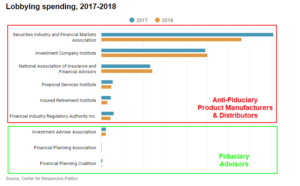

Lobbyist Spending in Financial Services, Product Companies Vs. Advisor Advocates

Again, SIFMA Spent Most Money In Financial Services Industry Lobbying Lawmakers (Mark Schoeff, Investment News) - The latest data is out from the Center for Responsive Politics on lobbying spending in financial services, and it finds that the Securities Industry and Financial Markets Association (SIFMA, which represents wirehouses and other major Wall Street firms) was once again the top spender, with a whopping $6.6M spend. Following close behind was the Investment Company Institute (ICI, which represents the mutual fund industry) at about $5M, and the National Association of Insurance and Financial Advisors (NAIFA, which represents the insurance and annuity industry) at $2.4M, and then the Financial Services Institute (FSI, representing broker-dealers), the Insured Retirement Institute (IRI, representing the annuity industry), and FINRA that each spent roughly $500k. By contrast, the Investment Adviser Association spent less than $250k on lobbying last year, and the Financial Planning Association and Financial Planning Coalition combined spent only $67.5k on lobbying. The significance of these numbers is that, in the midst of major rulemaking proposals on a fiduciary duty in recent years, from the Department of Labor in 2017 to the SEC in 2018, along with numerous state fiduciary proposals, lobbying organizations representing financial services product manufacturers and distributors cumulatively spent nearly $15.5M on lobbying activities, while organizations actually representing fiduciary advice spent less than $300k all together. Which perhaps helps to explain why, despite clear consumer demand and a strong preference from financial advisors themselves, fiduciary rulemaking has been so challenging to get through without being countered or watered down by the product distribution industry.

Five Ways To Pick Your Ideal Target Client (Bob Hanson, Advisor Perspectives) - One of the biggest challenges for advisors to get good results from their marketing efforts is that they don't necessarily have a clear target market identified that they're trying to reach in the first place... which results in broad-based, overly-generalized marketing that rarely manages to generate positive results. The clear "solution" is to pick a clearer target market... except for many advisors, that itself feels like a terrifying choice, with a concern that they might make a long-term commitment to the "wrong" niche or specialization. Accordingly, Hanson provides a series of 5 strategies to choose a clearer target market to be able to implement more targeted and effective marketing, including: 1) if you have several target markets you're considering, just make a list of all of them... and then sketch out a niche marketing plan for each, considering ease of access, fit with the existing practice, size of the market, existing relationships with Centers of Influence, etc., score each of the factors, and choose the target market that gets the highest score; 2) consider your top 3 clients that you'd most like to replicate, write out their key descriptors and characteristics, and then try to draft a mini sample marketing plan to reach more of those ideal clients (just to verify you can create a viable plan to reach more people like them); 3) take a broader view of the top 20% of your clientele (that usually generate 80% of the profits!), and look for commonalities amongst them that could coalesce to become your ideal target client; 4) select some natural market based on your own interests and preferences (e.g., "I naturally get along with ____ kinds of people" or "I like to work with people like myself, which means the following ____"); and 5) try to access someone else's client base (e.g., targeting a particular profession and the association where they're members, or employees at a particular firm, or joint clients of a top CPA firm, etc.).

Why The Difference Between Your Ideal Client Characteristics And Acceptance Criteria Is Important (Stephen Wershing, Client Driven Practice) - If it has one at all, the typical advisory firm's "ideal client profile" is usually something to the effect of, "We're looking for successful corporate executives who are delegators, appreciate the value of advice, and have at least $500,000 to invest." But Wershing suggests that, in practice, this is still an incomplete and ineffective definition of the ideal client because it's still not specific and clear enough for people who might refer you to know exactly who to refer. So what's the alternative? To describe not just the ideal client, per se, but the problem they have, for which you have a unique and ideal solution; thus, for instance, why it's much easier to refer advisors who specialize in women going through divorce or families with college-bound children than just "corporate executives who have at least $500,000 of investable assets." In other words, the advisory industry has a tendency to stress the characteristics that are important to the advisor (e.g., $500,000 of investable assets, client who is a delegator), rather than the characteristics that would be most useful and relevant to the target client themselves (or the person who might refer them). In fact, Wershing suggests that those advisor-specific factors like minimum assets and willingness to delegate really aren't characteristics of the ideal client profile at all, and are really more of "acceptance criteria" that define who in that target market the advisor will accept (once they otherwise fit a clear target client profile). Especially since the person doing the referring may not know if the person is advisor-delegation-oriented or has sufficient investable assets... and risks that they don't even make a referral, rather than take the chance of making a "wrong" referral. The key point, though, is simply to understand that increasing referrals is about making yourself more referrable in order to solve a problem of the client... and you can decide for yourself at a later point whether that client also has the investable assets, delegator mentality, or other key characteristics for you to decide to accept them as well.

10 Must-Haves For Your RIA Website (Jennifer Mastrud, XYPN Advisor Blog) - In the modern world, your website is the gatekeeper between you and your livelihood, the first impression that most prospective clients will have of you (before they ever get around to contacting you to meet in person), which means it's essential to begin the trust-building process from the moment the prospect arrives on your site. Accordingly, Mastrud offers up 10 core "must-haves" to consider when designing your advisor website, including: 1) get a clear and practical URL that people can type and remember, be certain it's a .com (because clients are going to assume it's a .com anyway, so get the one they're anticipating!), and be certain you actually own it and don't have a contractor register on your behalf and own the website in their name instead (you can buy cheaply yourself on sites like GoDaddy or Name.com); 2) people connect with images (not just text), so make sure you have images on your website, and make sure it's images that are relevant to your target clientele (and of good quality, as the quality of the images on your website becomes a reflection of your quality as well); 3) keep it simple and clean and easy to navigate to the core information (i.e., eschew fancy moving graphics and slides for simple navigation that clearly guides readers through what you want them to see); 4) have a well-written bio (as your Bio/Team page will usually be one of your most-viewed pages on your site, because prospects usually want to know who you are before they want to learn about what you do); 5) have a quality headshot, because again prospects want to see you and understand who they're going to be working with, and a low-quality picture of you detracts from your perceived quality and integrity (and having no picture at all undermines the ability of the prospect to make that person-to-person connection in the first place!); 6) be transparent about your fees and pricing, especially if you're marketing that you're a transparent fiduciary in the first place (i.e., you can't say "we value fiduciary transparency, but won't tell you what we cost without making you call us for a meeting first!"); 7) have an easy way for prospects who are interested to schedule an introductory meeting with you, which you can do now by integrating any number of online scheduling apps directly into your website; 8) have a way to capture the contact information for prospects who may not be ready to meet yet, but would at least give you their email address in exchange for something useful to them (i.e., a "lead magnet"); 9) be cognizant of using good SEO practices when setting up your website (or working with an SEO expert to help ensure it's done right); and 10) only after you've done the rest of the site design should you go back and try to do further refinements (e.g., A/B test to see if people are more likely to click on the green or blue version of that Contact button!?).

Who Needs Free? Passive Fund Prices Flatline (Asjylyn Loder, Wall Street Journal) - Notwithstanding the 2018 launch of Fidelity's new zero-fee mutual funds, a recent Morningstar report found that, overall, the price paid for index funds barely budged in 2018, and in some categories, investors actually paid higher average fees. In fact, a separate investor survey from Brown Brothers Harriman found that, for the first time in at least six years, investors rated fund performance equally important as fund fees, suggesting that perhaps fund fees have finally gotten low enough that cost will no longer be the overriding central focus it has been in recent years. In fact, Blackrock's iShares saw record inflows in the 4th quarter of 2018, despite not having any fresh new price cuts (since 8 months prior). Notably, though, the Morningstar report does still show that fees for actively managed funds continue to fall, and transaction costs (i.e., trading commissions at broker-dealers) also continue to fall, coupled with an ever-rising list of ETFs available to trade without any transaction fees at all. Nonetheless, the data suggests that perhaps the passive index fund industry at least has finally gotten "cheap enough" that consumers are now satisfied that the costs are low enough to be a good deal, such that the focus is beginning to shift to other factors instead; after all, the whole point of branding a low-cost solution is that once investors trust that it is low-cost, they tend to stop comparison-price-shopping altogether. Which perhaps helps to explain why not one of Fidelity's new zero-fee funds is among the firm's top 10 most popular this year (as the Fidelity ZERO Total Market Index Fund took in only $290M in January, compared to $5.2B into Fidelity's 500 Index Fund (at a cost of "just" $0.20 per $1,000 invested).

Wall Street Learns That Giving Stuff Away Is Boring (Barry Ritholtz, Bloomberg) - Over the past year, the seemingly inexorable decline of fees and trading costs (dubbed "The Vanguard Effect") finally reached their logical extreme, with a rapid expansion of no-transaction-fee platforms (e.g., Vanguard offering nearly 1,800 ETFs on a no-transaction-fee basis) and even Fidelity's launch of four zero-fee funds. Yet after an 8% decline in fund fees in 2017, the data suggests that over the past year, fund fees have largely stabilized (at least in large-cap passive index funds). In part, this may simply be because other competitors have brought their fees down to Vanguard levels, at least for some of their funds, and that there simply isn't much room left to cut. Yet for most asset managers besides Vanguard, the companies still have to find some way to make money, and Ritholtz suggests that perhaps consumers are simply realizing that "free" isn't really free, and that it may not be worthwhile trying to go all-in on free after all (e.g., "free" trades with poor execution can actually be more costly than just paying a small trading fee for best execution in the first place!). Or stated more simply, perhaps investing costs are getting low enough that consumers have now reached the point that they'd prefer to pay a very low known cost than get investments for "free" but wonder how the firm is making money off them anyway?

The Heat Grows On Indexing (John Rekenthaler, Morningstar) - Earlier this week, the New York Times published an Op-Ed from SEC Commissioner Jackson and law professor Steven Solomon raising concerns about whether all index fund providers are really creating index funds as transparent as investors think. After all, index fund providers can still face their own conflicts of interest, from Morgan Stanley adding Chinese stocks to its MSCI Emerging Markets Index after what was reported to be "business blackmail" from China over being included, to the LIBOR-rigging scandal several years ago (though LIBOR is not an index directly represented in index funds, since it's an "index" of survey data, not an actual index of securities themselves). There's also a rising concern of internally-constructed index funds, where the index is created by the fund company itself, potentially making it less a pure "index" and more an expression of the asset manager about what it believes should be invested in (essentially turning its proprietary "index fund" into an algorithmic active investment selection process). Ultimately, Rekenthaler questions whether these index fund critiques are really as problematic as the authors claim (e.g., LIBOR rigging wasn't actually expressed directly in index funds because LIBOR isn't an index of bond securities, and it's not clear whether asset manager self-indexing creates more outsider influences than any other index fund, especially given how even Morgan Stanley's Emerging Markets index may have been compromised). Nonetheless, Rekenthaler acknowledges that, as more and more dollars pour into index funds, the amount of assets those providers control may increasingly tempt them to sin and eventually become more problematic, and thus Rekenthaler does support the NY Times authors' calls for greater scrutiny of index funds going forward from here. Or as the late John Bogle himself recently put it, "there's no way that the Federal government will stand by while a handful of fund companies gain control of 40% of the U.S. stock market."

How I've Made Email My Secret Weapon (Aaron Klein, Medium) - The nearly overwhelming volume of email that hits our inboxes every day has led to a growing backlash against email, and a proliferation of new tools designed to help keep our inboxes sane. Yet Klein suggests that there's nothing like email to stay connected, both internally to a business and externally to clients and colleagues, and that email is his "secret weapon" for success (and that he still reaches "Inbox Zero" 1 - 3x per week, despite keeping his email address relatively open and accessible). Tips that Klein shares about how he keeps control of his inbox start with "slowing the firehose" coming in, such as: use email for messages, and push articles/newsletters that you read to an RSS reader like Pocket instead (Michael's note: I use Inoreader myself); if you do let a few brands into your email inbox, be selective and make sure they're brands you actually want to hear from; kill/unsubscribe to all the "notifications" you receive from apps and tools that aren't really essential in the first place; be an aggressive unsubscriber to anything that doesn't really fit your reading or email habits. From there, other tips from Klein include: turn off your email notifications (don't worry, you'll still remember you have email to read even if your phone doesn't notify you every 2 minutes!); free yourself from feeling obligated to respond to everything (if random people showed up in your office to ask for your time and attention during your work day, you'd likely say no, and the same should be true for random emails, too!); remember that if you use an email client with good search capabilities (e.g., Gmail), you don't need to file everything into a zillion folders (as it takes more time to file every email away than it does to just search for what you need when you need it with a good search tool!); get a To-Do app and use that as your to-do list instead of your inbox (Klein recommends Asana); set up text macros to be able to quickly respond with common messages using a text expander service (e.g., Klein just types "nocant" and it auto-replaces into the email with his "I'm sorry, I'm not able to help due to prior commitments..." respond; and have an aggressive triage system to sort through your volume of emails in the first place (e.g., sort into "Reply", "Reply with a Macro", "Forward/Delegate", "Process Later", or "Archive/Delete" it); and then have a system for the emails you do have to process later (Unsubscribe/Block, Reply, Forward/Delegate, or Task out for work).

Want To Cut Your Work Hours In Half? Create An A/B Schedule (Andee Love, Fast Company) - Recent research has shown that despite its intuitive appeal, our brains really are not built for multi-tasking, and in fact all of the "context switching" of going from one area of focus to another can drastically cut down on our productivity as our brains have to keep resetting focus and getting (back) up to speed on the new task. At a minimum, this suggests that we should try not setting all of your client meetings clustered on 3 "A" days of the week, and then holding two "B" days for all of your in-office team meetings and prep work multi-tasking, but Love goes so far as to suggest that we should proactively try to block our tasks together to reduce and minimize how much task-switching and context-switching happens at all. For instance, you might divide your tasks and schedule into an "A" and "B" column, and only do A tasks on one day and B tasks on another. In practical terms, this might mean (rather than the typical advisor that switches back and forth every day between internal meetings and prep work, and external meetings with clients). In the extreme, advisors could even block whole weeks at a time for "A" tasks, followed by "B" weeks of recovery (or prep for the next stint of meetings). Notably, once you set your schedule for A and B tasks, it's important to communicate it to clients and colleagues so they understand what to expect as well. Ultimately, though, Love suggests that while it might feel strange at first to limit tasks and access to certain days, ultimately the improvement in productivity is more than worth it, and clients and colleagues may even appreciate the clearer guidance and framework about when they can and should try to access your time.

How To Build Durable And Long-Lasting "Atomic" Habits (Khe Hy, Rad Reads) - Habits can be remarkably sticky once formed, which in the case of bad habits makes them challenging to break, but also creates the opportunity to establish good habits that, once established, repeatedly benefit us as they compound over time. In fact, in his recent book "Atomic Habits," James Clear makes the point that creating habits that result in even just tiny incremental change can have immense compounded benefits - for instance, a habit that makes us just 1% better every day compounds out to over a 3,700% improvement in a year (while getting 1% worse every day compounds to a -97% loss!). Notably, though, most people struggle with this, precisely because they try to focus on the end goal of what they're trying to achieve, and not the habits they need to establish to get there; or stated more simply, "don't aim for consistently heroic efforts, aim for being heroic at consistency" and let the compounding work for you instead. So how do you build good habits? Expanding upon Charles Duhigg's "The Power Of Habit," Clear notes that habit formation follows a cycle of Cue (a trigger to your brain to set off a behavior, such as an alarm ringing or your phone buzzing), Craving (where a certain feeling arises in response to the cue, from the excitement of gambling to the calmness of alcohol), Response (where you engage in the habit to satisfy the craving, e.g., having a drink or checking your phone), and then a Reward (the outcome occurs). Accordingly, you can change your habits by trying to impact any of the four steps, for instance by making it more obvious (better Cue) if it's good, or invisible if it's bad; by making it more attractive (as a Craving) if it's good, or unattractive if it's bad; by making it easier (to engage in the Response) if it's good (or difficult if it's bad); or making it more satisfying (to reinforce the Reward) if it's good, or unsatisfying if it's bad. For example, aim to meditate first thing after waking up or handle financial matters on Saturday mornings (time-based cues), or take medication by putting it next to the faucet or send more thank-you notes by keeping a stack of stationary on your desk (location-based cues), or even create "temptation bundles" for yourself (e.g., if you crave the morning's first cup of coffee, require yourself to do those pushups first and then have the coffee, or plan to do Yoga while watching Netflix, or clean out your inbox while getting a pedicure). You might even try "habit tracking" yourself, either in a journal or with an app, or even just by giving yourself an easy system to track progress; for instance, one broker habit-tracked his requisite cold calls by putting 120 paper clips into a jar, and every time he made a call he moved one paper clip out of the jar to a second one and knew when the first jar was empty he had completed the habit, and it was time to go home for the day!

How To Build Durable And Long-Lasting "Atomic" Habits (Khe Hy, Rad Reads) - Habits can be remarkably sticky once formed, which in the case of bad habits makes them challenging to break, but also creates the opportunity to establish good habits that, once established, repeatedly benefit us as they compound over time. In fact, in his recent book "Atomic Habits," James Clear makes the point that creating habits that result in even just tiny incremental change can have immense compounded benefits - for instance, a habit that makes us just 1% better every day compounds out to over a 3,700% improvement in a year (while getting 1% worse every day compounds to a -97% loss!). Notably, though, most people struggle with this, precisely because they try to focus on the end goal of what they're trying to achieve, and not the habits they need to establish to get there; or stated more simply, "don't aim for consistently heroic efforts, aim for being heroic at consistency" and let the compounding work for you instead. So how do you build good habits? Expanding upon Charles Duhigg's "The Power Of Habit," Clear notes that habit formation follows a cycle of Cue (a trigger to your brain to set off a behavior, such as an alarm ringing or your phone buzzing), Craving (where a certain feeling arises in response to the cue, from the excitement of gambling to the calmness of alcohol), Response (where you engage in the habit to satisfy the craving, e.g., having a drink or checking your phone), and then a Reward (the outcome occurs). Accordingly, you can change your habits by trying to impact any of the four steps, for instance by making it more obvious (better Cue) if it's good, or invisible if it's bad; by making it more attractive (as a Craving) if it's good, or unattractive if it's bad; by making it easier (to engage in the Response) if it's good (or difficult if it's bad); or making it more satisfying (to reinforce the Reward) if it's good, or unsatisfying if it's bad. For example, aim to meditate first thing after waking up or handle financial matters on Saturday mornings (time-based cues), or take medication by putting it next to the faucet or send more thank-you notes by keeping a stack of stationary on your desk (location-based cues), or even create "temptation bundles" for yourself (e.g., if you crave the morning's first cup of coffee, require yourself to do those pushups first and then have the coffee, or plan to do Yoga while watching Netflix, or clean out your inbox while getting a pedicure). You might even try "habit tracking" yourself, either in a journal or with an app, or even just by giving yourself an easy system to track progress; for instance, one broker habit-tracked his requisite cold calls by putting 120 paper clips into a jar, and every time he made a call he moved one paper clip out of the jar to a second one and knew when the first jar was empty he had completed the habit, and it was time to go home for the day!

I hope you enjoyed the reading! Please leave a comment below to share your thoughts, or make a suggestion of any articles you think I should highlight in a future column!

In the meantime, if you're interested in more news and information regarding advisor technology, I'd highly recommend checking out Bill Winterberg's "FPPad" blog on technology for advisors as well.