Executive Summary

Enjoy the current installment of "weekend reading for financial planners" – this week's edition kicks off with the announcement of the CFP Board's latest public awareness campaign, which will kick off this fall with a series of new ads around the theme of promoting a "more confident today and more secure tomorrow... with a CFP professional," as the public awareness campaign completes its 6th year of spending $10M+/year from its $145 assessment on what is now 82,000+ CFP certificants.

Also in the news this week was an interesting private letter ruling from the IRS that may clear the way for employers to provide "matching" 401(k) contributions, based not on an employee's own contributions to the plan, but their payments for their student loans instead (which might alternatively be framed as employers providing student loan assistance for those employees who are also willing to save towards retirement), and a discussion from SEC Commissioner Clayton about possibly expanding the accessibility to private investments for main street investors (potentially through the use of a financial advisor).

From there, we have several articles about investment trends in the industry, from a look at how more and more mutual fund companies are beginning to automatically convert C-shares to A-shares after 7-10 years (ostensibly in response to the SEC's Share Class Selection Disclosure Initiative earlier this year scrutinizing brokers that used higher-cost share classes when equivalent lower-cost alternatives were available), to the rising concern from Morningstar that not all "Clean" shares are equally clean (and why "bundled", "semi-bundled", and truly "unbundled" categories may be a better descriptor), and the discussion of how advisors are becoming even more proactive in seeking out better cash yields for clients who don't want the low-yield cash sweep options available from most broker-dealers and RIA custodians today.

We also have several marketing-related articles this week, including: why it's important to not just explain to clients the benefit of working with you but also the consequences of not working with you; how to change your seminar evaluation firms to get prospects to book more follow-up appointments; and how when it comes to complex services like financial planning, it's not enough to simply show that the advisor has solutions to solve the client's problems, it's also necessary to engage in a conversation to help clients better define what the problems are that they're really trying to solve for in the first place (which clients sometimes don't realize themselves)!

We wrap up with three interesting articles, all around the theme of our very human struggle to be part of the herd and liked by others, and how it can adversely impact us: the first looks at how many advisors find themselves unhappy in their advisory firms because they build towards the peer pressure of what others are doing (e.g., "grow more!" or "get bigger!") instead of focusing on the goals for the firm that will make them personally happy; the second explores how increasingly collaborative work environments are leading to rising employee overwhelm and burnout because it can be so hard to figure out how to say "no" to co-worker requests (especially when our identity is built around being the go-to person in the office that likes to help people as a "good team player"); and the last provides a powerful reminder that to be a good leader, it's crucial to not always try to be "nice", as the reality is that sometimes team members need hard feedback... instead, focus on being honest, consistent, and rigorous, and then deliver those messages as nicely as you reasonably can.

Enjoy the "light" reading!

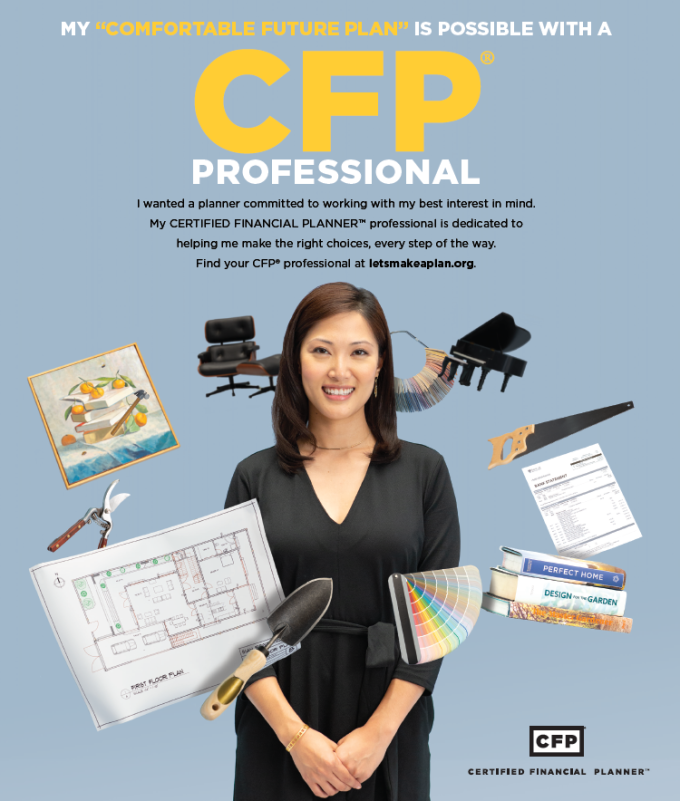

CFP Board To Launch New Round Of Ads To Build Public Awareness Of Designation (Mark Schoeff, Investment News) - This fall, the CFP Board will begin the next stage of its public awareness campaign, now up to $11.7M/year in spending and funded by the $145/certificant annual assessment that was added back in 2011 and has been renewed ever since given the positive results the CFP Board has demonstrated from its efforts (although unaided awareness of the CFP marks dipped in 2017 from a peak in 2016, which spurred the CFP Board to develop a fresh new campaign). The theme of the latest public awareness campaign series is "More confident today and more secure tomorrow" and focuses on achieving that confidence "With a CFP professional," featuring one ad showing a young woman getting a "Comfortable Future Plan" with her CFP professional, and another ad with an older couple seeking a "Comfortable Forever Plan." In addition to simply building awareness of the CFP marks, which will run in both print media and also television channels like CNN, Fox, Bloomberg, and ESPN, the ads will also steer consumers directly to the CFP Board's "Let's Make A Plan" site for finding a CFP professional to work with.

CFP Board To Launch New Round Of Ads To Build Public Awareness Of Designation (Mark Schoeff, Investment News) - This fall, the CFP Board will begin the next stage of its public awareness campaign, now up to $11.7M/year in spending and funded by the $145/certificant annual assessment that was added back in 2011 and has been renewed ever since given the positive results the CFP Board has demonstrated from its efforts (although unaided awareness of the CFP marks dipped in 2017 from a peak in 2016, which spurred the CFP Board to develop a fresh new campaign). The theme of the latest public awareness campaign series is "More confident today and more secure tomorrow" and focuses on achieving that confidence "With a CFP professional," featuring one ad showing a young woman getting a "Comfortable Future Plan" with her CFP professional, and another ad with an older couple seeking a "Comfortable Forever Plan." In addition to simply building awareness of the CFP marks, which will run in both print media and also television channels like CNN, Fox, Bloomberg, and ESPN, the ads will also steer consumers directly to the CFP Board's "Let's Make A Plan" site for finding a CFP professional to work with.

IRS Clears Path For Student Loan Repayment Tied To 401(k) (Madison Alder, Bloomberg Law) - In Private Letter Ruling 201833012, the IRS approved the request of an employer to provide 401(k) "matching" contributions for their workers based not on whether they contributed to their 401(k) plans or not, but whether they made a payment on their existing student loans (of at least 2% of their salary). From a technical perspective, it is notable that the IRS will allow "matching" contributions to 401(k) plans to occur even when the underlying dollars being matched weren't contributed to the 401(k) plan in the first place. From the broader planning perspective, though, the strategy paves the way for employers to support retirement planning for employees that simply can't afford to contribute to a 401(k) plan and pay down their student loan debt. Alternatively, some are even suggesting that employers may position the employee benefit as a form of helping students to pay their student loan debts on a tax-preferenced basis, arguing that the employer is essentially "replacing" the cost of student loan payments for the worker with its contribution to the employer retirement plan. Ultimately, the private letter ruling is specific to only the one company that applied for it, and it's not clear whether or how many other employers will adopt it going forward. But given one recent survey showing 86% of younger workers would commit to their employer for 5 years if the employer helped to pay off their student loans, there is a growing hunger amongst employers to find ways to provide student loan assistance to workers (on a tax-preferenced basis), either through 401(k) plan "matching" initiatives like the one highlighted in PLR 201833012, or legislative proposals like H.R. 795 (the Employer Participation in Student Loan Assistance Act) that would allow employers to provide tax-preferenced student loan payments as a part of their educational assistance programs.

SEC Chairman Wants To Let More Main Street Investors In On Private Deals (Dave Michaels, Wall Street Journal) - This week, SEC Commissioner Clayton announced that the SEC is exploring options that would make it easier for individuals to invest directly in private companies, in recognition of the shrinking interest in fast-growing companies to IPO in the public markets in the first place, and/or at least the tendency for companies to grow larger privately and only show interest in an IPO later as an exit strategy for their private investors and after more of the rapid-growth gains have already been earned (e.g., Uber and Airbnb). And the concern is not merely that main street investors won't have public markets opportunities to participate in private companies that don't IPO until later stages of growth, but that the traditional "accredited investor" rules (with their income and net worth requirements) make it impossible for most individual investors to participate in private offerings even if they wanted to. On the other hand, the complexity and more limited information on private offerings mean they are already a more common source of fraud against small investors. As a result, the SEC is exploring whether main street investors might be given access to private market companies through vehicles that would more easily aggregate individual investors together through vehicles that could consolidate the efforts for the necessary due diligence and make it easier for companies raising capital to certify their investors qualify. Which, notably, may include allowing in investors who don't meet income or wealth thresholds, but have professional licenses or advanced education (e.g., financial advisors)!

Fund Industry Limits C-Share Investing, Cutting 12b-1 Fee Income For Advisors (Jeff Benjamin, Investment News) - Through the end of the year, a growing number of fund companies (including Fidelity, Franklin Templeton, BlackRock, and Putnam) have announced plans to start "automatically" converting C-share mutual funds paying a 1% 12b-1 trail that have been held for 7-10+ years into A-shares that would pay only a 25bps 12b-1 fee instead. Commentators are suggesting that the news is likely related to the SEC's recent "Share Class Selection Disclosure (SCSD) Initiative" earlier this year, which raised concerns that some brokerage firms were inappropriately using higher-cost share classes when equivalent lower-cost share classes were available. And while A-shares are generally more expensive upfront - thanks to the upfront commission load they pay - the fundamental purpose of C shares was not that advisors would earn a higher trail indefinitely; instead, C-shares pay a 1% 12b-1 fee simply because 0.75% of it is meant to be a levelized version of that upfront A share commission. Which means after 7-10 years, once the upfront commission has been earned out over time, the broker "should" only be paid the 0.25% ongoing shareholder servicing fee... and rather than put broker-dealers at risk for failing to do the proper share class conversion, fund companies will now apparently begin to do it automatically. Yet from the broker's perspective, those who were relying on long-standing C-share trails of 1% may suddenly find themselves facing a significant drop in revenue on long-standing clients, raising the question of whether brokers will simply switch clients to an actual advisory account (where ongoing fees are validated by the ongoing services)... or instead simply sell a new C-share fund to replace the existing one and restart their 7-10 year conversion period.

Commission-Free 'Clean Shares' Are Messier Than You Might Think (Christopher Robbins, Financial Advisor) - The concept of "clean shares" emerged during the Department of Labor's fiduciary rulemaking process, as a simplified form of a no-load fund that eschewed both commissions and the 12b-1 trails that often go with them. However, as Morningstar notes, commissions and 12b-1 fees are not the only additional cost layers that are sometimes assessed within a mutual fund's expense ratio and paid out to brokerage platforms, as there are also "sub-Transfer-Agent" (sub-TA) fees, or occasionally simply "shelf space" payments meant to recreate such revenue-sharing. As a result, not all "clean shares" are equally clean, which is leading Morningstar to propose a new classification of mutual fund expense models: bundled, semi-bundled, and unbundled. The "bundled" share classes would include traditional commission loads, 12b-1 and other distribution fees, and related transactional or operational fees. By contrast, "semi-bundled" shares would not have 12b-1 fees or commission loads, but would still include sub-TA or other revenue-sharing arrangements to platform providers. While truly "unbundled" mutual funds would require investors to pay only the fund manager's fees and fund operating expenses, but nothing else related to distribution or implementation (which Morningstar suggests is what most investors and advisors are likely thinking of and expecting when they hear "clean" shares). Notably, even with "unbundled" or semi-bundled mutual funds, advisors and platforms still need to get paid, so such funds won't necessarily result in lower all-in costs for investors. But unbundling, or at least being aware if a fund is truly "clean" and unbundled, does help to clarify other potential conflicts of interest between asset managers and the platforms they're available (or not available) on, and the distinction between unbundled and semi-bundled helps to clarify when and whether a platform may be "double-dipping" on compensation for distributing and holding the fund.

Advisors In A Pickle Over Low-Yielding Cash Sweep Accounts (Jeff Benjamin, Investment News) - As the economy improves and the Fed raises rates, interest rates across the board are trending higher... except in many broker-dealer and RIA custodian money market funds or cash sweep accounts, where the average yield remains around 25bps (compared to a nearly 1.8% yield for the average independent money market fund, and a similar average interest rate for high-yield bank accounts). The issue came to a head this week as Merrill Lynch announced that it was shifting its default cash sweep allocation into a (lower-yielding) affiliated bank and would require their advisors to proactively request for client cash to be held in higher-yielding money markets, although notably some RIA custodians don't even give their advisors an option for a high-yield money market sweep and require the use of their affiliated-bank cash sweep options. In turn, the lack of yield on today's advisor platforms is leading to a rise of technology solutions like MaxMyInterest to provide an alternative way for advisors to help clients maximize their cash yields (by allocating across various high-yield banks), as advisors feel the pressure from clients (and the fiduciary duty) to ensure that client cash is properly managed. Of course, the reality is that in a world where most advisor tech is "free" from broker-dealers and custodians, and ticket charges wind ever lower, many platforms need to earn a substantial spread on client cash in order to generate revenue and profits to execute their business model... but the rising squeeze on cash, including the growing tendency of advisors to move client cash out of the broker-dealer or custodian's cash sweep anyway, raises the question of whether under-paying on cash yields will eventually compel broker-dealers and especially RIA custodians to adopt a more direct model of simply charging advisors basis points for custody and providing competitive cash yields instead.

What's The Risk Of NOT Hiring You? (Stephen Wershing, Client Driven Practice) - Most financial advisors market themselves by talking about the benefits for clients of hiring an advisor. But Wershing points out that to really demonstrate your value and give clients a reason to hire you and work with you, it's also important to communicate the costs of not hiring you... and the adverse consequences that may ensue for clients who choose another advisor (or simply take no action at all). Of course, for clients who have already shown up feeling 'unsettled' and looking for a solution, the pain point is often quite straightforward... not hiring the advisor means not resolving the issue that perturbed the client enough to seek the advisor out in the first place. But for other clients, who may not yet be that motivated to take action and hire the advisor, it's necessary to create that motivating tension by showing or highlighting to them the consequences of not taking action. After all, if there's merely upside to working with the advisor but "no downside" for not working with the advisor, there's no adverse consequence to just deciding not to move forward "right now" and waiting. Of course, what it is that clients lose by not acting will depend on the particular firm and its value proposition... for some, the consequence might be that not diversifying and rebalancing loses the opportunity for more consistent returns and diminished drawdown risk, while for others it might be that not retirement planning could force them to work several more years, or that not doing estate planning could cause needless money to be lost to taxes after death, etc., etc. The fundamental point, though, is simply that it's not enough to show why clients would benefit by hiring you... it's also important to show the consequences if they don't hire you today as well!

How To Double Your Seminar Appointments (Kerry Johnson, Advisor Perspectives) - Seminar marketing has long been a staple for financial advisors looking for prospects, where the advisor provides some form of financial education and then hopes to sign up attendees at the end of the meeting for a follow-up consultation that will hopefully turn them into a client. Yet for most advisors, it's still a struggle to actually get those seminar attendees to book an appointment, given that some are not qualified to do business, while others came only for the free meal or education, and by the time the advisor reaches out for a follow-up a few days later, the attendees have often forgotten much of what was said and/or have lost interest altogether. So what's the alternative? Johnson suggests that the starting point is to recognize that it's crucial to create for attendees a need/reason for themselves about why they should want to book an appointment. Accordingly, on your evaluation form at the end of the seminar, ask retirees to rate for themselves on a scale of 1-5 how concerned they are about the most common fears for retirees (running out of money, volatility, inflation, impact of taxes, and a desire to build a legacy or protect against a catastrophic illness). To emphasize the point, the advisor can also raise these issues during the seminar, and ask attendees to raise their hands for each that is a concern (which makes them more engaged and also increases the likelihood they sign up for an appointment). Bear in mind, though, that the strategy only works if attendees actually complete and turn in their evaluation sheets, which means there may need to be some kind of raffle prize (e.g., a free dinner, and iPad drawing) to incentivize them. But the fundamental point is that when people self-rate their concerns - and remind themselves how concerned they are - they're far more likely to book appointments based on their own self-assessed and self-acknowledged ratings of concern, than just trying to tell them and convince them of the problem yourself.

Clients Don't Buy Solutions They Buy Problem Definitions (Charles Green, Trusted Advisor) - The traditional view of sales is that in the end, people don't buy products, they buy solutions to their problems... for instance, they don't buy a drill-bit but a solution to the need to drill a hole, which is why businesses are guided to package up their "value proposition" not in terms of their features but the benefits they provide and the problems they solve. But the caveat when it comes to more complex services - like financial planning - is that often, consumers don't actually fully understand their own problems in the first place, and what it is they really need to solve. As a result, while it might be appealing to just try to find the best way to explain your value proposition as an advisor and what you do for clients, Green suggests that it's first necessary to engage in a discussion about the problem that the client is trying to solve and affirm it's really the "right" problem in the first place. For instance, the client who wants to figure out if he/she has enough to retire really may just need to find a different and more personally rewarding job (i.e., they don't want to retire from work, they really just want to get away from where they're working now!), and the client who doesn't want to update their estate planning documents may really be having anxiety about the fact that the kids don't know how much they stand to inherit in the first place. The fundamental point is simply that the problems that clients state at the beginning of the first meeting with the advisor are often not the final problems that the advisor ends out solving... so rather than assuming that clients actually want what they're asking for, probe deeper to figure out if that's what they're really worried about in the first place. And of course, helping clients get better insights into their real problems is itself often a highly motivating "breakthrough" that helps to persuade the client to follow-through on working with the advisor, too!

Do Advisors Cave To Peer Pressure? (Carolyn McClanahan, Financial Planning) - While "peer pressure" and the desire to fit in is something most often associated with the days of high school, the reality is that human beings are social animals and a feeling of pressure to conform and do what everyone else is doing remains ever present. The issue often crops up with clients, who may be seeking an advisor to get them the returns their co-worker is getting (as revealed during a talk at the water cooler!), or those who have trouble getting control of their spending out of a desire to keep up with the spending of their (potentially more affluent) friends and neighbors, or those who suddenly want to change their retirement plans to match what a "more successful" colleague is doing. And McClanahan notes that the phenomenon of peer pressure is equally present amongst financial advisors as well, from those who adopt the mindset that they "must grow" because it seems like everyone else is growing (rather than adopt the lifestyle practice that would make them happy), or that the advisory firm must be a certain size ("larger"!) in order to be perceived as credible and of good quality. Yet the reality is that advisors can and do run successful practices and businesses with a wide range of sizes, growth rates, and business models. Which means, as with avoiding peer pressure in high school and portfolios and retirement, it's crucial to focus on your goals of what you actually want to achieve as an advisor... not just try to conform to the peer pressure of adopting the goals that other advisors may be pursuing.

You Could Be Too Much Of A Team Player (Sue Shellenbarger, Wall Street Journal) - The trend of modern workplaces is towards ever more teamwork and collaboration, with one study estimating that many white-collar employees now spend a whopping 85% of their time collaborating with multiple teams of co-workers between meetings, emails, conference calls, and more. Yet in new research on the trend, it turns out that workers are also reporting feeling more overwhelmed than ever by all the teamwork, especially by those who are most inclined towards helping others or have the highest need to be perceived favorably by others... who now struggle to figure out how to draw boundaries and stop being so engaged before they burn out altogether. In other words, for those employees who have "identity drivers" of being know as helpers, good team players, or the "office MVP," there's no clear way to ever put the brakes on an ever-mounting workload in an ultra-collaborative team-based environment (especially since those who are known to always say "yes" to offering help will just find even more requests and demands for their help as collaboration increases!). Of course, the irony is that many people like to help others precisely because it feels good to help others; nonetheless, with no way to draw the line on when those requests end, burnout is becoming increasingly difficult to avoid. So what's the alternative? The point isn't necessarily that collaboration is bad, but to at least recognize that certain employees may need help in understanding that sometimes it's OK to say "no" and not answer and respond to every email or request for help, and that some may need assistance in prioritizing their tasks to make sure that the most essential work is still being done as needed (despite the requests of co-workers to collaborate on a never-ending stream of other non-essential tasks).

Leaders, Stop Being So Nice All The Time (Claire Lew, Signal v. Noise) - It's natural for human beings to want to be liked by others, but unfortunately, when it comes to those in positions of leadership, it's not always feasible to be nice and be a good leader. At the most basic level, this is simply because sometimes team members really do need some tough feedback to correct a problem behavior, and at least polite disagreement about a strategy or tactic can often foster discussions that lead to even better solutions. But the greater challenge is that for those who self-perception is to "The Nice Guy" (or gal) in the company, it becomes almost impossible to give critical feedback and engage in the important disagreements that can and do happen from time to time. Because while it's nice to be nice, when it becomes more important to remain popular and "liked" instead of being fair (which includes being direct on those who need to hear hard feedback), leaders can lose sight of their real purpose as a leader, which is to guide a team to accomplish a specific purpose or mission (not just to be well-liked by them along the way). Even worse, for some leaders who become too focused on "being nice," it can too easily become "a dangerously convenient rationalization to avoid hard decisions, uncomfortable conversations, or controversial actions." Or stated more simply, if you allow yourself to care too much about being nice, it's the equivalent of saying, "the needs of my team as a whole don't matter as much as their perception of me as an individual." Instead, Lew suggests the better path is to be honest, rigorous, and consistent (though as the famous book Crucial Conversations illustrates, you can still be nice about those hard conversations, too!).

Leaders, Stop Being So Nice All The Time (Claire Lew, Signal v. Noise) - It's natural for human beings to want to be liked by others, but unfortunately, when it comes to those in positions of leadership, it's not always feasible to be nice and be a good leader. At the most basic level, this is simply because sometimes team members really do need some tough feedback to correct a problem behavior, and at least polite disagreement about a strategy or tactic can often foster discussions that lead to even better solutions. But the greater challenge is that for those who self-perception is to "The Nice Guy" (or gal) in the company, it becomes almost impossible to give critical feedback and engage in the important disagreements that can and do happen from time to time. Because while it's nice to be nice, when it becomes more important to remain popular and "liked" instead of being fair (which includes being direct on those who need to hear hard feedback), leaders can lose sight of their real purpose as a leader, which is to guide a team to accomplish a specific purpose or mission (not just to be well-liked by them along the way). Even worse, for some leaders who become too focused on "being nice," it can too easily become "a dangerously convenient rationalization to avoid hard decisions, uncomfortable conversations, or controversial actions." Or stated more simply, if you allow yourself to care too much about being nice, it's the equivalent of saying, "the needs of my team as a whole don't matter as much as their perception of me as an individual." Instead, Lew suggests the better path is to be honest, rigorous, and consistent (though as the famous book Crucial Conversations illustrates, you can still be nice about those hard conversations, too!).

I hope you enjoyed the reading! Please leave a comment below to share your thoughts, or make a suggestion of any articles you think I should highlight in a future column!

In the meantime, if you're interested in more news and information regarding advisor technology, I'd highly recommend checking out Bill Winterberg's "FPPad" blog on technology for advisors as well.