Executive Summary

As an advisory business gets started, the focal point is typically on just getting the first few paying clients in the door – the key aspect being paying clients. Simply put, it’s all about just trying to generate some revenue, and the key indicator for measuring the advisory firm is pretty straightforward: how much revenue is there.

However, as the advisory practice begins to grow, the picture gets more complex. Soon there are a range of different clients, paying varying fees for what may be a varying services. The cost to operate the business begins to rise as well, with investments into anything/everything from technology to staff. Suddenly, just look at how much money is coming in the door is no longer enough; just because there’s revenue doesn’t mean there’s profits, and there are too many clients to just keep it all straight in your head.

Accordingly, as a financial advisory practice grows, it becomes increasingly important measure and track more information about the business, so it can be managed as a business. As the saying goes, “if you can’t measure it, you can’t manage it.” Building a financial dashboard of “Key Performance Indicators”, KPIs, for financial advisors, that track key metrics of the business, its growth, and its clientele, can give you the information you need to make better practice management decisions. It's not necessarily about harnessing the "big data" insights of an entire industry, but simply the "small data" opportunities of better understanding your own business!

KPIs About The Financial Health Of Your Business

The first key step in understanding an advisory firm beyond just its revenue (or its AUM as a proxy for revenue) is to look at the costs to generate that revenue, and the profits that remain after a reasonable allocation of costs.

In benchmarking advisory firms, expenses are usually broken down into two broad categories: direct expenses, and overhead expenses. Direct expenses represent the cost to acquire and directly service clients; in other words, the cost of the financial advisors who work directly with clients. Overhead expenses includes… everything else, from operations and administrative (and for larger firms, management) staff, to office space, to the various technology and software tools the firm uses.

Once broken out accordingly, the advisory firm can then begin to evaluate its key performance indicator for the health of the business: profit margins. The gross profit margin is the profitability of the firm after accounting for direct expenses; the net profit margin of the firm is what remains after accounting for all (i.e., overhead) expenses (also often referred to as the ‘operating profit margin’). According to practice management guru Mark Tibergien in his excellent book "How To Value, Buy, Or Sell A Financial Advisory Practice", a typical rule of thumb for advisory firms is 40/40/20 – 40% of revenue to direct expenses (resulting in a 60% gross profit margin), and 40% to overhead expenses, resulting in a 20% net profit margin, as shown below (larger firms tend to be closer to 40/35/25).

Once broken out accordingly, the advisory firm can then begin to evaluate its key performance indicator for the health of the business: profit margins. The gross profit margin is the profitability of the firm after accounting for direct expenses; the net profit margin of the firm is what remains after accounting for all (i.e., overhead) expenses (also often referred to as the ‘operating profit margin’). According to practice management guru Mark Tibergien in his excellent book "How To Value, Buy, Or Sell A Financial Advisory Practice", a typical rule of thumb for advisory firms is 40/40/20 – 40% of revenue to direct expenses (resulting in a 60% gross profit margin), and 40% to overhead expenses, resulting in a 20% net profit margin, as shown below (larger firms tend to be closer to 40/35/25).

| Revenue | $1,000,000 | 100% |

| Minus Direct Expenses | $400,000 | 40% |

| Equals Gross Profit | $600,000 | 60% |

| Minus Overhead Expenses | $400,000 | 40% |

| Equals Operating Profit | $200,000 | 20% |

For solo advisors, allocate a “direct expense” estimate to account for the cost it would take to hire another advisor to do the owner’s job; this is crucial to understanding whether the advisory firm is actually profitable as a business with a net profit margin after the owner’s compensation, or if the reality is simply that the value of the business is the owner’s ability to pay their own salary-equivalent but with no actual profits left over. By contrast, larger firms may wish to examine the revenue per advisor across each advisory team in the practice to understand which teams are responsible for the most revenue and/or profits.

KPIs For The Growth Of Your Business

Of course, it’s one thing to understand the profit margins of the advisory firm in the current year; it’s another to look at how those numbers change over time as the firm grows. Accordingly, when it comes to growth, there are two more key performance indicators: growth rate, and retention rate. After all, for a firm to grow, it matters not only what comes in, but also how much revenue is retained!

Growth for an advisory firm in turn can be broken down into two categories: new revenue from new clients, and new revenue from existing clients (e.g., clients who hire you for more services, buy additional products, add AUM to their managed account, etc.). For a firm that’s generating more revenue overall, this helps to clarify where it’s coming from – is the firm primarily adding more clients, or primarily generating more revenue from existing clients? Notably, firms that are paid on an AUM basis may also wish to separate out new revenue from market performance (growth) that increases AUM, versus new revenue that comes from clients actually contributing net new dollars. This distinction is especially important to understand the potential impact of a bear market on the revenue of the firm; for instance, if most new revenue is because clients are adding assets, the firm can potentially grow through a bear market, while if most revenue growth is just from portfolio growth, then revenue is at significant risk of decline if the market declines as well.

In addition to looking at new revenue coming in, it’s also important to understand how much revenue is being retained from year to year. Key metrics in this category include the percentage of revenue that is recurring in the first place (e.g.,ongoing trails, AUM, or retainer fees, versus one-time planning fees, hourly fees, or upfront commissions), and the percentage of clients that are retained each year. AUM firms may wish to delve into this even further, looking at the percentage of clients retained versus lost, the percentage of assets retained versus lost, and the percentage of assets that flowed out even though the clients were retained (e.g., due to retirees taking withdrawals or paying taxes). Of course, looking at typical turnover of clients also provides some indication of the average tenure of clients with the firm (as businesses that turn over clients at a higher rate will have lower retention rates).

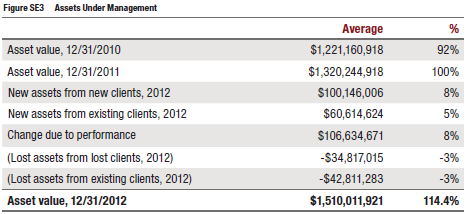

For example, the chart below shows a version of how these numbers trended for the average “super ensemble” (more than $1B of AUM) firms in the latest Moss Adams/Investment News Benchmarking Study. The results show that the typical large firm grew new assets by 12% (of which 7.5% was new clients and 4.5% was existing clients), but also lost approximately 6% of assets in outflows (half from losing clients, half due to withdrawals from existing clients), resulting in a net asset growth (‘organic’ growth) of approximately 6%; by contrast, market performance alone contributed about 8%, which means more than half the firm’s growth rate was still being driven by market returns!

KPIs For The Clients In Your Advisory Practice

In addition to looking at the firm’s overall profitability, and the trends in its growth rate, it’s also important to look at the revenues and profitability of individual clients across the firm.

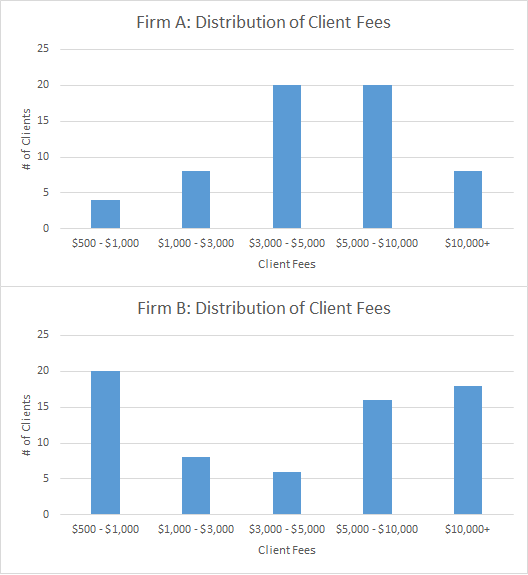

The starting point is to simply look at the average revenue per client. How much, on average, does each client pay to the firm (determined by simply dividing the number of clients into the total revenue of the firm). And what is the distribution of revenue paid from each client? For instance, the chart below illustrates two different advisory firms, which each generate a healthy average revenue/client of $5,750. However Firm A has the bulk of its clients right in the midst of its sweet spot around its average, while Firm B essentially has a “barbell” practice, with a large segment of wealthy clientele balancing out (and effectively subsidizing) a large base of small (likely unprofitable) clients.

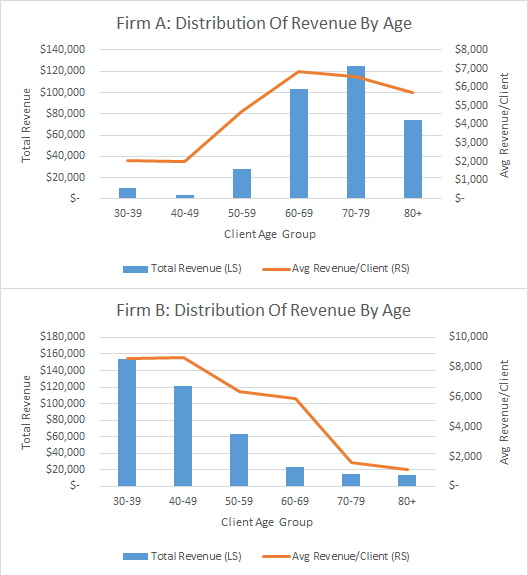

In addition to looking at the overall distribution of client fees, firms should also tracking client revenue by age, which can provide important insight into potential client revenue loss (or not!) due to retirement withdrawals or even attrition due to death.

For instance, the data below recharacterizes the same firms A and B from above, but delineates total revenue and average revenue/client by age. From the above data, it appeared as though Firm A was the ‘healthiest’ with a large core of clients paying consistent fees, while Firm B was far more scattered with a ‘barbell’ distribution of low-revenue clients being subsidized by high-revenue clients. However, when categorized by age, the data reveals that while Firm A may be a firm consistently working with retirees, Firm B may actually be far healthier in the long run, as the higher income clients are almost exclusively at the young end of the spectrum and the lower revenue clients are all much older ‘legacy’ clients of the firm who will slowly attrition away.

In another 10 years, 80% of Firm A’s revenue will be concentrated with clients in their 70s and 80s with a high withdrawal/death/attrition rate, while almost 2/3rds of Firm B’s revenue will still be from clients who haven’t even retired yet and are still saving and adding to the portfolio, and the majority of Firm B’s low-revenue clients may be gone entirely at that point! To say the least, viewing client revenue by age reveals significant and meaningful differences in the long-term health of the businesses!

Ideally, a firm should also have metrics to track how much time is spent on behalf of each client by the advisor and various staff (or at least track how much activity occurs on behalf of each client to estimate the time spent ). By assigning a ‘cost’ to the value of the time for each staff member and the advisor, the firm can then make an estimate of revenue/hour for various clients, and the profitability of each client.

Benchmarking, Strategic Goals, And Management By Measurement

Ultimately, the goal of this exercise is to recognize that potential problems can’t be managed, and strategic goals can’t be set, until there’s a mechanism to measure and monitor the financial health of the firm, its growth, and its clients in the first place. Simply put, as the saying goes, “if you can’t measure it, you can’t manage it.”

Accordingly, for firms that have never gone through the exercise, try building your own “financial dashboard” for your own advisory practice (the process of doing so may also highlight some areas where you could better manage and track the data in your practice!), including these key performance indicators (KPIs):

Firm Metrics

- Gross Revenue

- Direct Expenses (including reasonable salary for owner’s compensation!)

- Overhead Expenses

- Gross Profit Margin

- Net/Operating Profit MarginGrowth

- New amount/percentage of revenue from new clients

- New amount/percentage revenue from existing clients

- %age of revenue that’s recurring

- Client retention rate

- Revenue (or asset) retention rateClients

- Average revenue/client

- Distribution of revenue/client

- Distribution (and average) of client age

- Distribution of revenue (or revenue/client) by client age

- Client revenue/hour and profit/client

Once the metrics have been tabulated the first time, they can be updated (at least annually, but ideally even more frequently) for the firm, providing perspective on how these key performance indicators for the business are changing over time. In turn, the data can then be compared to industry benchmarking surveys to identify potential problems (e.g., high gross margins but low operating margins suggest the firm has too much overhead), to identify the overall profitability of the firm and its capacity of its profit margin to absorb a challenging business environment, to determine whether the firm is still growing at a healthy pace (which is crucial to create growth opportunities for staff), and to review whether services or fees need to be adjusted for particular clients whose revenue or profitability may be out of whack. From the planning perspective, firms may wish to focus on improving particular metrics from one year to the next, or hold partners accountable for improving a particular metric as a part of their responsibilities to the firm.

The bottom line, though, is simply this: the only way to effective manage a business based on the data is to have the data in the first place. If you’re not measuring the key performance indicators of the financial health of your advisory firm, there’s no way you can be aware – not to mention try to fix – any problems that become apparent. Fortunately, though, the data of a financial planning firm is not "so" complex as to make it an impossible big data challenge; instead, it's simply about harnessing the "small data" already in your CRM, portfolio management, and other software! So in the coming months, as client meetings slow down for the summer, try compiling your own practice management dashboard of key performance indicators, and begin to get some better perspective on where your practice stands, beyond just the sheer amount of gross revenue (or AUM) coming in the door!

So what do you think? Do these Key Performance Indicators (KPIs) seem relevant to you? Are there any missing from the list that you think are relevant? What KPIs are on the financial dashboard for your practice? What do you use to regularly monitor and track the health of your business?

Also important in the mix is Client Acquisition Costs. i.e. how much does it really “cost” you to acquire each clients.

Maria,

In concept I agree measuring Client Acquisition Costs is crucial.

In practice, though, I find it far harder, because most firms spend very little dollars on marketing (typical advisor benchmarking surveys peg it at no more than 1% – 2% of revenues), but spend a lot of time trying to market themselves and network. As a result, it’s almost impossible to effectively measure Client Acquisition Cost without a good measure of the personal time spent on marketing activities… which, unfortunately, most advisors don’t track in the first place. :/ Though if they do, indeed this can be assigned a dollar value to give a reasonable estimate of Client Acquisition Costs.

– Michael

Michael,

I agree that in order to measure CAC, you need to track other important business data — business data that most FAs are not easily willing to track. Those are the numbers that really run a business. And when selling a business, those are the numbers people are going to ask for… so as FAs get nearer to 50 years old, those numbers will mean more to them.

While tracking portfolio performance, client goals, etc. are thing an FA does easily and willingly, tracking their own business, as is planning for their business growth, is a horse of a very different color.

Part of the problem with FAs not tracking CAC is that it’s not an exact science, but more of an art. FAs prefer, IMO, to have an exact equation to plug into. (CAC or sometimes called CAV – Client Acquisition Value.)

Working with FAs to determine what their numbers are, including their “hourly” rate really is, well, — I’d be better off telling them that I’d like to pull one of their teeth 🙂 And do feel like I’m doing it, very often! It also seems to take “months” before the revelation of how those numbers work for them kicks in.

Every FA and industry can come up with “some number”. The thing that stops people is that they don’t have an ideal client (they take on anyone who breaths, no matter what the costs) and that makes it harder to determine a number because the range is so wide. Also, the number is not always exact (as most financial business owners prefer) but may end up more as an average. You also need to have an idea (or guess at) the length of time a client will stay with you.

How could anyone run a business is they don’t know what the cost of acquiring a new client is?

I find that the problem with survey’s that measure “marketing”, is that most business owners don’t take into account all the time they really spend “marketing” which could include networking, referrals, being on boards of organizations, speaking, etc. etc. They do a lot for “free” but don’t consider that it’s really costing them to do this “free marketing, networking, speaking, etc.” So IMO, I really don’t believe survey’s when it comes to marketing. Especially in the FA industry where many FAs are really running “jobs” vs. businesses.

I talk to lots of FAs who tell me they get all their clients through referrals (for example) and often it’s from a referral from a person they’ve recently marketed to or who heard them at an event!

Yes, for CAC you do need to know what your “real” hourly rate is, what the hourly rates are of your staff

Interestingly enough I have a few “practice” management books for FAs on my shelf. I just looked in their index and don’t see anything regarding CAC/CAV.

But gladly, I did find 2 good articles on the subject online, just to get folks thinking about CAC!

http://www.fipath4advisors.com/blog/2014/client-acquisition-costs-%E2%80%93-what-to-know-and-what-to-do!.aspx#.U4zrf7ROX3g

http://blog.blueleaf.com/the-silent-advisor-killer-cost-of-customer-acquisition/

http://en.wikipedia.org/wiki/Customer_acquisition_cost

Michael..it will be interesting to find out the metrics used by online platforms or even robo advisors. Because they usually are able to measure the cost of client acquisition since they use online marketing channels which are measurable. Also like saas platforms if they work on subscription model, they should be able to arrive at metrics like Life Time Customer Value, attrition and retention rates forecasts for each product or service that they introduce clients for subscription over a period of time. Of course, it will start from freemium to premium models. Have you in your experience found whether financial services firms which are offering their services predominantly online are using similar metrics like tech firms which offer their services on subscription basis? Say a comparison between wealth front or learn vest with drop box or whatever. This could help understand the deluge of money pouring into the space. Probably there is a case that 7 or 10 years down the line they might be profitable? At least a couple of them?

Great sharing !!

Michael,

Any suggestions on non-financial KPIs? If I were looking to buy a firm, or even just look objectively at my own firm, I would also want to know the health of the client base. Are they receiving regular contact, are they satisfied with the value/fee ratio or are they on the cusp of leaving the firm. I’m not sure how you would measure these things, but it seems that there must be more to a successful firm than just profitability.

On a related note one of my personal KPIs is days off work. If firm A & firm B have the same profit margin, but one firm owner works half as many days as the other this is a huge difference.

Your thoughts?

Michael, Do you have sample spreadsheets we can incorporate in our own practice you’d be willing to share?