Executive Summary

While the debate rages on about whether robo-advisors will ultimately be a threat to human advisors, or whether the solutions that combined technology and humans will be the ultimate victors, the reality is that to view the battle as one of “technology vs human advisors” may be missing the real “threat” of robo-advisors. As technology platforms, their disruptive potential goes far beyond just impacting financial advisors.

For instance, the ability of software tools to re-create index funds – but without the mutual fund or ETF wrapper – creates the potential for today’s robo-advisors to disintermediate much of the existing index fund industry, aided by the tailwind of a benefit under tax code that uniquely favors these new “Indexing 2.0” robo-platforms over current fund-based solutions. Similarly, robo-advisors as “trading” software creates the potential to eliminate many active management middlemen, allowing a wide range of smart beta and rules-based trading algorithms to be implemented and automated directly.

And as the robo-technology trends shift from a direct-to-consumer focus to offer new robo-advisors-for-advisors solutions instead, the new platforms present the threat to today’s existing RIA custodians, who face the potential of a generational shift as new less-investment-centric financial planners adopt simplified robo-advisor investment platforms, and build a business there for the long run… which means in the end, the greatest threat of robo-advisors may not be their competition with human advisors, but the way that human advisors adopt them to disrupt much of the existing FinTech ecosystem!

“Robo” Indexing 2.0 Can Disintermediate Index ETFs And Mutual Funds

The origination of the mutual fund was driven by two primary needs: to facilitate a process where an active investment manager could more efficiently manage a single pool of funds, and to benefit investors with lower transaction costs through the economies of scale of pooled trading. Decades later, the index mutual fund was invented, and while pooling investments for the efficiency of an active manager wasn’t relevant, index mutual funds still benefitted their investors with the lower transaction costs of investing at scale.

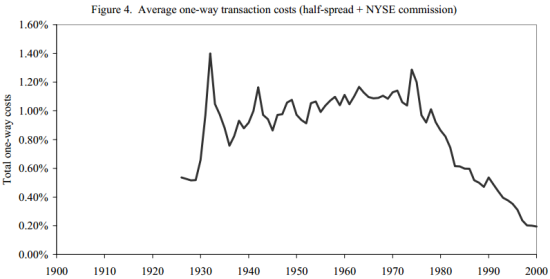

As transaction costs grind inevitably lower and lower, though, the need for pooling funds to lower trading costs is becoming less and less relevant; retail investors can use any number of online trading platforms to execute a trade for less than $10, a nearly 90% drop over the past few decades. Of course, for a large number of investment positions, even $10/trade adds up, but as costs continue to grind lower, there will eventually come a point where there’s virtually no incremental benefit to pooled mutual funds or ETFs at all.

Source: "A Century Of Stock Market Liquidity And Trading Costs" by Charles M. Jones

The significance of this trend is that as transaction costs approach zero, suddenly there’s no reason to own an index ETF or mutual fund at all. Certainly, the investor may still want to own the diversified exposure of the index, but that can be accomplished by simply buying all of the underlying securities directly. In other words, you wouldn’t own the S&P 500 Index Fund, you’d just push a button and software would automate the purchase of each of the 500 stocks in the S&P instead for an equivalent (near-zero) transaction cost.

Of course, it’s necessary to have software to manage that process – but that’s exactly what robo-advisor trading platforms are positioned to do, and in fact Wealthfront has already launched their “Direct Indexing” Wealthfront 500 solution to do just this. Similarly, Motif Investing is capable of building at least “mini” versions of an index, up to 30 securities at a time, through its motifs, at the click of a button.

The significance of these “Indexing 2.0” solutions is that they can disintermediate index ETFs and mutual funds altogether, potentially saving investors an entire layer of middle-man cost. Of course, the robo-advisors themselves will also charge a fee for their service – partially reintroducing that middle man – but the software has the potential to scale to a lower cost than many of today’s index funds with even greater technology-driven economies of scale. And at a minimum, shifting the layer of middle-man costs from today’s mutual fund and ETF complex to the world of software instead would result in a tremendous disruption to the status quo.

An even more notable benefit of Indexing 2.0 beyond just lower costs, though, is the fact that the tax code limits the ability of investors in pooled investment vehicles to enjoy tax deductions for their losses; mutual funds and ETFs cannot pass through net losses, and therefore cannot selectively harvest losses in excess of gains to generate current tax deductions for their investors. However, direct ownership of the underlying stocks of an index can be loss harvested at the security level, creating an indirect tax incentive that favors Indexing 2.0 solutions over today’s existing indexing vehicles. In other words, Indexing 2.0 solutions have an explicitly tax benefit over today’s Indexing 1.0 mutual funds and ETFs, due to the structure of the tax code itself.

Which means in the end, Indexing 2.0 with robo-advisor platforms has the potential to use the benefits of the tax code to entirely disintermediate today’s existing index ETF and mutual fund vehicles, in addition to saving cost for investors by potentially cutting out the ETF and mutual fund middleman (or at least, achieving greater economies of scale for a lower cost).

FinTech Robo-Automation Of Smart Beta And Rules-Based Trading Algorithms?

While robo-advisor Indexing 2.0 platforms threaten to disintermediate the existing index ETF and mutual fund industry, such indexing solutions are not necessarily relevant for the subset of financial advisors that are more inclined towards active management solutions. Even if transaction costs are driven down to zero, pooled investment vehicles remain relevant for active investment managers to operate efficiently (at least with today’s investment and technology infrastructure).

However, the reality is that many active managers actually implement what are fundamentally fairly “passive” strategies, in that they’re not based on ongoing subjective decisions of the manager, but instead operating on a pre-built series of trading algorithms, screens and filters, or other “rules-based” investing systems. And if software can apply a “filter” like “buy all the stocks in the S&P 500” to replicate an index, there’s no reason that software couldn’t apply other filters as well – like tilt the portfolio towards value stocks, or small-cap, or low volatility, or favorable Price/Earnings, Price/Book, Price/Sales, or other Fundamental Indexing-style screens.

In other words, robo-advisor software as a “trading” tool creates the potential for investors (and/or their advisors) to implement and self-automate their own tilts, filters, screens, trading algorithms, and rules-based investment strategies. Popular strategies (e.g., various forms of smart beta?) could be licensed directly through the platform, allowing any investor to have access to the “strategy” of the investment manager, implemented automatically on their behalf. Or alternatively, investors (or their advisors) could create any number of their own investment strategies as well, and then allow the software to automate their implementation.

In the end, this means that robo-advisors as a passive investor tool threaten index ETFs and mutual funds as an Indexing 2.0 solution, but robo-advisors as an active investment and trading tool threatens to disintermediate a wide segment of today’s active investment manager industry as well, from “Smart Beta” funds to hedge fund “algo[rithm]s” to low volatility, DFA-style small-cap and value tilts, and more. And just as with Indexing 2.0 solutions, the robo platforms can benefit by avoiding pooled investment vehicles and allowing investors to own the underlying securities, to obtain more favorable tax loss harvesting treatment as well!

Notably, a small subset of “true” active managers, who conduct some kind of (individual security, macroeconomic, or other) analyses that require their unique intellectual capital, may remain relevant and uniquely suited to a pooled investment vehicle. But by the time all the other types of “active” management strategies are automated, it’s not entirely clear how many managers would be left (and how many would really be any good!).

Robo-Advisors – The Next Generation Of (All-In-One) RIA Custodian Platforms?

A notable factor of how today’s robo-advisors are implementing – whether to deliver automated “active” trading strategies, or indexing 2.0 solutions – is that most have either negotiated their own brokerage, trading, custody, and clearing arrangements, or are even aiming to fulfill at least some/many of these roles by creating their own entities. In essence, (at least some) robo-advisors are creating a “vertically integrated” investment management solution, particularly as a means to keep transaction costs down (and facilitate everything from trading in fractional shares, to netting trades from all investors on the platform to reduce the total amount of shares being bought and sold).

For advisors who already have an existing RIA built around the infrastructure of their existing custodian, there may not be much pressure to change in the near term (except perhaps to use robo-advisors as a segmented solution for “smaller” AUM clientele). However, for newer advisors, the opportunity to build businesses and gather assets on today’s emerging robo-advisor-for-advisors platforms may entirely avoid the need to work with any of the “traditional” RIA custodians like Schwab, Fidelity, TD Ameritrade, Pershing Advisor Solutions, or even “start-up friendly” platforms like SSG. Of course, for many newer advisors, traditional custodians won’t accept them due to advisor asset minimums anyway (SSG being a notable no-advisor-minimum exception); however, an advisor who builds a business on a robo-advisor platform now, and accumulates significant assets over time, may not show any interest in transitioning to a “traditional” custodian in the future, either!

In other words, the longer-term potential threat from today’s robo-advisor platforms is that as the next generation of advisors comes along – focusing more and more on adding value in financial planning and advisor “gamma”, rather than investment management and investment alpha – an emerging generational shift may be underway at the same time. It may not simply be that robo-advisors-for-advisors accept “small” advisors while traditional custodians serve “big” ones; it may also be that robo-advisors serve “younger”(Gen X and Gen Y) advisors while traditional custodians serve ”older” (some Gen X and Baby Boomer) advisors, which does not paint a pretty picture for traditional custodians in another decade whether Baby Boomer advisors finally begin to retire en masse. For instance, with our recent partnership announcement between XY Planning Network and Betterment Institutional, it's possible that many XYPN advisors will grow their AUM as a supplement to their monthly retainer clientele without ever needing a custodian, now or later! And Betterment's recent $60M round of venture capital funding suggests that its backers are seeing the opportunity, too, as Betterment pivots to serve advisors and disrupt custodians.

And notably, the risk of this generational shift in platforms for advisors is not merely an issue for the traditional custodians themselves, but also the technology ecosystem that has built around them. After all, an advisor using a platform like Betterment Institutional or Motif Advisor not only avoids needing a “traditional” custodian, but with the ground-up technology being built, also no longer needs portfolio accounting software like PortfolioCenter or Advent or Orion, no longer needs portfolio reporting tools like Black Diamond, and no longer needs rebalancing software like iRebal, Tamarac, or TRX. And it’s not difficult to imagine an additional layer of the FinTech ecosystem being built around the new robo-advisor platforms themselves, with client portals and practice management dashboards and integrations to advisor CRM and financial planning software being built directly.

Of course, to the extent that today’s robo-advisor solutions may simply represent a more efficient and effective set of technology tools to manage and implement an advisory firm practice – while taking advantage of the natural tax benefits of disintermediating pooled investment vehicles – there is also the potential that some of today’s custodian platforms will step up their own technology to fill the void (although notably, the first player in this space is Charles Schwab with their Schwab Intelligent Portfolios solution, which itself will reportedly use ETFs, rather than aiming to disintermediate them!). In fact, arguably one of the most significant consequences of the robo-advisor trend has been to highlight the relatively poor quality of technology solutions – at least from the perspective of user experience, for both the advisor and the client. But that also means the robo-advisor trend has put new pressure on RIA custodians, and their supporting technology providers, to either step up or risk being left behind altogether by the next generation of advisors.

So what do you think? Are robo-advisors a threat to human advisors, or not? Or is the reality that the true disruptive threat of robo-advisors will be the adoption of their technology to manage portfolios themselves in new and different ways, eliminating the need for traditional mutual funds and ETFs in lieu of direct ownership of securities with more favorable tax treatment? And will the robo-advisors-for-advisors trend mean the next generation of financial planners may simply never need to use today's traditional RIA custodian platforms at all?