Executive Summary

In recent years, an increasing number of practice management consultants have begun to “sound the alarm” on the dangers of having an aging, retiree-centric client base in a financial planning firm. As the logic goes, retired clients are depleting their portfolios with ongoing withdrawals, and more and more will pass away as the years go by, so a planning firm with aging clients is akin to a rapidly depreciating asset.

However, a deeper look at the numbers reveals that these drawdowns in client assets may be overstated, at least in the coming decade. After all, the reality is that at a 4% safe withdrawal rate, a balanced portfolio should still be able to grow for years to come, and there’s actually a 96% chance that clients will still have all of their nominal principal left even after 30 years! Similarly, while the mortality rate is higher as clients age, the reality is that out of 100 client couples aged 65, the statistics suggest that 90% of them will still be around in 15 years!

Of course, the caveat to working with retirees is that, compared to accumulator clients, the mere fact that they’re spending and not saving with ongoing contributions is still a headwind, and obviously even the modest attrition rate for early retirees is still higher than what it would be for younger clients. Nonetheless, these statistics suggest that firms simply worried about retaining value in the coming years should perhaps focus less on catering to the next generation to reduce the average age of clients (especially if those clients can't be served profitably by the firm in the first place!), and more on simply retaining the current generation, especially by building relationships with both members of a couple to increase the likelihood of retaining a surviving widow. While the demographics of an aging client base will eventually be more of a challenge, the real impact is still many, many years away, and simply focusing on retaining widows (or not) of the current generation may matter most of all in the coming years!

How Much Do Clients Withdrawal In Retirement, Really?

For an advisory firm that’s built around the assets-under-management business model, clearly having clients who are retired and taking withdrawals from their asset base is a concerning headwind to growth and sustainability. Yet the reality is that relative to the asset base itself – and the prospective growth of markets – ongoing retirement withdrawals are not likely to deplete assets significantly. In fact, the withdrawals may not deplete assets at all for years to come.

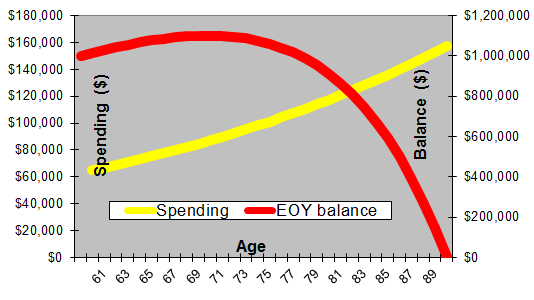

The reason that retirement withdrawals are not all that destructive is the simple fact that in the early stages of retirement, withdrawals relative to total assets tends to be rather modest. For instance, the chart below shows how rising spending (yellow line) impacts a retirement account balance (red line) over time, assuming an 8% growth rate on a balanced portfolio, and an initial withdrawal rate of 6.6% that rises each subsequent year for inflation (i.e., $66,000 withdrawal in year 1 on a $1,000,000 portfolio, and the $66,000 withdrawal amount is increased in each subsequent year for inflation).

As the results reveal – and as evidenced by the simple fact that withdrawals start at a rate (6.6%) that is less than the growth rate (8%) – on average a retiree at age 60 doesn’t actually begin to deplete the account balance at all until almost half way through retirement! It’s only by the client’s mid-70s that the account balance even begins to decline, and several more years after that before it dips below where it started, and only then finally experiencing the rapid spenddown in the later years.

Of course, the caveat to the chart above is that portfolios that average 8% don’t necessarily earn it every year, and not every retired client dies “promptly” on their 90th birthday - some unexpectedly live longer. As a result, even assuming an average growth rate of 8% on a balanced portfolio, clients are not recommended to spend the 6.6% initial withdrawal rate that “works” based on the above straight-line projection. Instead, the standard “safe withdrawal rate” is actually 4%, to defend against such unfavorable sequences, unexpectedly longevity, etc.

Yet in turn, it’s important to bear in mind that when balanced portfolios average 8% and the withdrawal rate starts at only 4%, in the overwhelming majority of scenarios, clients will simply outearn their spending level – sometimes quite dramatically – and wealth is more likely to compound upwards than spend down at all. In fact, as Bengen’s original safe withdrawal rate research showed, in 96% of historical scenarios a 4% withdrawal rate approach finishes with at least as much nominal principal at the end of 30 years that it started with; in the median outcome, clients following a 4% safe withdrawal rate approach actually more-than-quadruple their wealth over their retirement time horizon!

Which means that ultimately, there is actually very little danger that ongoing retirement withdrawals will really totally deplete a retiree’s asset base, and even if it does, it’s not likely to happen until the very last years at the end of retirement as clients move into their 80s and beyond. (Notably, while some consultants caution about the impact once clients reach age 70 ½ and begin required minimum distributions from traditional IRAs, the reality is that if clients don’t actually need to spend the money, an RMD is simply a transfer from an IRA to a taxable account that doesn’t necessary change the available assets to manage, beyond perhaps the portion attributable to income taxes that may be payable from the investment assets!)

The "Surprising" Survival Rate Of Married Couples

Another classic concern of the AUM model with retirees is that as they age, clients will ultimately pass away, and most firms struggle greatly to retain assets (one study estimates that advisors will lose as much as 90% of the assets that pass to the next generation).

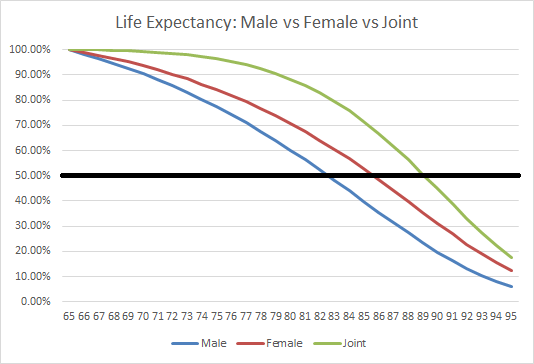

Yet again, a critical look at mortality statistics suggests that this client attrition through death is more likely to be a decades-distant challenge than a near-term one. For instance, the chart below shows the survival rate for males, females, and couples, based on the Social Security Administration’s mortality tables.

As the results reveal, while the mortality rate does rise as retirees move into their 60s and 70s, the joint life expectancy – i.e., the probability that at least one member of the couple remains alive – remains extremely modest in the first half of retirement. It takes 15 years – from age 65 to age 80 – for just the first 10% of client couples to pass away, at a rate of less than 1% per year. Only as the couple really enters into their 80s does the joint mortality rate begin to accelerate, where 25% of couples have passed away by age 85, and only at age 90 does the joint survival line finally even move below the 50% threshold!

And of course, some criticize that the Social Security mortality tables are unrealistically conservative for financial planners in the first place, as clients of planners tend to be more affluent with better life expectancies than the broad population assumption from Social Security. And some suggest the Social Security tables fail to sufficiently adjust to anticipate what appears to be a continued trend towards medical improvements that may further enhance life expectancies between now and when today’s baby boomers actually do reach their 80s and beyond. Which means in practice for financial planners, client survival rates may even be slightly better than the chart above!

Losing A Tailwind Is Still A Headwind

While the asset losses due to retirees taking withdrawals and eventually passing away may not be an avalanche of outflows anytime soon – given that the very oldest baby boomers are “only” in their late 60s and the youngest are only just turning 50 this year – the reality is that relative to businesses that were built on the basis of working with accumulators, the fact that clients aren’t adding assets is a lost tailwind that will no longer aid the growth of business revenues (in addition to the fact that clients tend to have more conservative portfolios at retirement that reduces the portfolio’s contribution to the growth rate). So while the actual headwind of client withdrawals and attrition may be modest, the “net” headwind of shifting from net savers to net spenders and reducing the anticipated portfolio growth rate is a bit more dramatic.

Nonetheless, the results here suggest that ongoing retirement withdrawals (at a ‘mere’ 4% withdrawal rate) and attrition from clients passing away (given even today’s mortality rates) is not likely to hit baby-boomer-centric advisory firms any time soon; the greatest impact doesn’t really begin until clients approach their 80s, which is a decade away for even the oldest boomers and not until the 2030s(!) and beyond for most! And of course, that assumes that medical advances don’t push out client life expectancies even further (which would both reduce client attrition from death and also likely lead clients to moderate their spending further in anticipation of longer life).

In turn, these statistics suggest that advisors should be cautious about how aggressively they adjust their business strategies to account for an aging client base. For instance, while much has been made of the importance of building relationships with the children of clients in an effort to retain assets, these statistics suggest it may be far more important to simply focus on establishing a relationship with the prospective surviving spouse of a couple, rather than their children. This is especially true given that asset/client retention for most advisors is also poor with widows (and the odds of one spouse dying and leaving assets to the survivor is far higher than both passing away and leaving assets to children). In addition, the irony is that dissipating assets to the next generation could even result in unprofitable clients that the firm wouldn’t want to retain anyway (for instance, a retired couple with $1,000,000 in assets may turn into three $333,333 son-and-daughter clients at the next generation, tripling the required work and turning one profitable client into three unprofitable ones!).

Similarly, advisors who are selling a practice should be cautious not to discount the value of the practice too much “just” because it has a large base of retiring/baby-baby boomer clients. While it is crucial to recognize that most clients will be in net outflow and not contributing – which does impact the growth trajectory of the firm and therefore the valuation – the reality is that the bulk of spending outflows and attrition due to death is still 15-20+ years out, given a typical 20%-25% discount rate used in the valuation of advisory firm cash flows, changes in the assumptions for asset retention that far out have almost no impact anyway. For instance, a projection of losing a whopping $1,000,000 of revenue in 20 years due to client withdrawals/deaths would only reduce the price of the business by a mere $11,500 in today's dollars at a 25% discount rate!

The bottom line is that while building an AUM-based practice around retirees is likely to grow more slowly than a similar business built around accumulators – due to the more conservative portfolios, the lack of ongoing contributions, the shift to spending withdrawals, and the ever-greater risk of client attrition due to death as the years advance – the reality is that the impact on most planning firms is likely to be modest in the coming decade. Though the trend will eventually accelerate in the 2020s and especially the 2030s, that point is far enough out that in the near term, planners might be better focused on simply retaining and growing new (retired) clients, and building relationships with spouses to ensure that the couple together remains a client for the decades to come. While building a practice with younger clients who are still in the accumulation phase and adding assets can ultimately benefit the firm’s long-term growth and value – and clearly a client with $X who is still a net accumulator is more valuable as a client than one with the same assets who is retired and withdrawing – pursuing such clients may be best suited for those firms that are truly seeking to serve those clients profitably, or are deeply concerned about the valuation of the business 10-20 years out, and not necessarily those who wish to wind down or sell their practice in the near term anyway.