Executive Summary

As ETFs and indexing makes the raw cost of “owning the market” cheaper and cheaper, the question arises of whether or how advisors can continue to justify an ongoing AUM fee for an investment portfolio. For some, the cost is justified by the alpha or portfolio-related “advisor gamma” value-adds that are provided; for others, the benefit is the inclusion of financial planning services; and for the rest, the benefit may just be to help protect clients from themselves and their self-imposed “behavior gap” on returns.

Yet the reality is that AUM fees are far more relevant for some of these services – like portfolio-related alpha – than others, and in some cases while some AUM fee is justified there is significant pricing pressure (e.g., providing portfolio-related gamma like automated rebalancing, tax-loss harvesting, and asset location). In some cases, the advisor provides so little actual portfolio-related value that the financial planning fee may become unbundled altogether.

Notwithstanding the potential pressure to unbundle, though, a look at the landscape of the financial services industry suggests that, if anything, the trend remains towards AUM fees. The shift towards fee-based revenue has been increasingly adopted by even the largest firms, from wirehouses to Schwab Private Client to Vanguard Personal Advisor Services – often bundled together with comprehensive financial planning services that are either very low cost, or entirely free because their impact on retention rates and increased lifetime client value alone justifies their cost to deliver. Which means in the end, even the declining cost of beta may not be enough to end the AUM fee… though the fact that a huge swath of Americans cannot be served by AUM fees – because they don’t have the assets in the first place – means a wider range of financial-planning-fee-for-service models may be inevitable anyway!

Creating Value In A World Where Beta Is (Nearly) Free – Alpha, Gamma, Financial Planning, Dynamic Beta, and Managing Behavior

Notwithstanding the fact that the cost of indexing and simply “buying beta” is getting cheaper and cheaper with the ongoing rise of Vanguard index funds and various ETFs, advisors have been increasingly adopting an assets-under-management (AUM) style business model that layers the advisor’s investment management fee on top of the portfolio, which raises the fundamental question: what value, exactly, is that advisory fee supposed to be paying for, as the cost of buying “the market” beta moves inexorably towards zero?

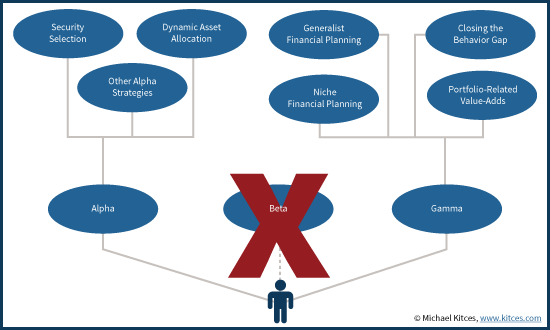

For some advisors, the primary purpose of the investment management fee is an attempt to deliver alpha – adding value to the portfolio above and beyond its core beta exposure, and being paid accordingly. In this context, alpha might be in the form of picking individual securities, selecting third-party managers that add value, or simply trying to better manage risk (which can improve risk-adjusted returns without increasing the raw return itself).

For others, the goal is actually to add advisor “gamma” – value-added advice that enhances the overall (portfolio or other) results, outside of trying to improve the raw investment performance itself. For instance, this might include tax-management strategies like automated rebalancing, tax-loss harvesting (where appropriate) and asset location, or for retired clients the tax-strategic sourcing of withdrawals across various types of retirement accounts and establishing dynamic withdrawal strategies. The more wealth there is in the first place, the more value these gamma strategies can add. For other advisors, their gamma value-add may be financial planning advice that goes far beyond the portfolio, to all the other areas in which clients may need (financial) help, or towards a particular type of niche clientele.

A third, more nuanced category of advisor value-add, might be determining which beta to own and when to dynamically adjust it, in a world where it’s not entirely clear how to allocate amongst “the markets” of various asset classes. For instance, an investor can own the Vanguard Total Market Fund and the Vanguard Total Bond Fund, but how much should be allocated to each? Should the entire stock and bond market allocations be determined by their weightings in global market capitalization? How can that be done for asset classes that don’t really have an effective means to measure market cap (e.g., commodities futures)? And with herding behavior, groupthink, and limitations of leverage and shorting, it’s also not clear if asset classes as a whole are necessarily as efficient as their underlying securities, raising the question of whether tactical asset allocation amongst asset classes may have opportunity (though to some extent this may simply be a sub-category of alpha?).

And in the end, for some advisors the primary portfolio-related value proposition is not to beat the market, enhance returns, or otherwise add to wealth, but simply to help prevent clients from reducing their own wealth due to their own bad behavior – in other words, by aiming to reduce clients’ self-imposed “behavior gap” in returns. While the exact magnitude of the behavior gap is still widely debated, clearly there are at least a subset of investors for whom the behavior gap is a significant negative, and merely closing that gap may actually contribute more “advisor gamma” than anything else to enhance the client’s actual long-term wealth and their ability to achieve their goals!

Broadly speaking, then, the ongoing commoditization of beta through indexing and technology essentially puts advisors at a crossroad regarding their value proposition: to provide alpha (in the form of security or asset class selection), or gamma (in the form of tax and other portfolio/wealth value-adds, or helping clients behaviorally), because there’s no longer any money in getting paid for beta itself.

The Relevance Of AUM Fees To Compensate For The Value Of Financial Advice

Given the crossroads that advisors face in being forced to choose whether they will provide alpha or gamma (or both) to clients, the secondary question arises: is an AUM fee still the appropriate mechanism to charge client for these value propositions? And will the declining cost of beta put pressure on advisory fees overall?

Ultimately, the impact of the declining cost of beta on advisory fees will likely depend on exactly what value propositions the advisor provides in the first place, as some are more or less conducive to AUM pricing, and are more or less exposed to pricing pressure.

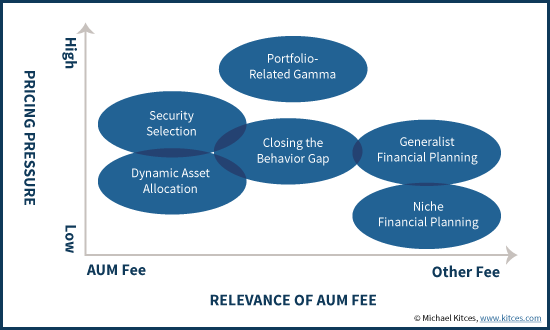

In the context of adding alpha, AUM fees are still arguably a very appropriate mechanism for charging clients; the AUM structure helps to align advisor and client interests, without some of the perverse incentives that arise with performance fees, and still allows for the advisory firm to effectively grow and scale resources. The more the advisory firm manages for the client, the more real-dollar-value that is added to the client if/when the alpha is delivered, so the AUM fee remains a reasonable way to charge for the service.

On the other hand, there is clearly some pricing pressure on alpha – especially as today’s technology tools make it easier to evaluate investment managers and determine whether they’re really living up to their expected alpha, or not. This is especially true for investment managers in the business of security selection, where performance can be clearly and easily measured against a relevant benchmark. Ironically, pricing pressure may be somewhat less on firms that manage tactically across asset classes, if only because it is significantly more difficult to determine the appropriate benchmark to evaluate such “unconstrained” managers in the first place.

On the gamma side, the relevance of an AUM fee varies significantly depending on the type of service being performed. For gamma value-adds that tie directly to the portfolio itself, where the value is implicitly tied to the amount of assets being managed, the AUM fee remains relevant… with the caveat that, because many of these services can and are implemented by technology (whether from advisor rebalancing software or “robo-advisors”), the downward pricing pressure on that AUM fee is very significant.

Where the advisor gamma is in the form of other financial planning advice, not directly related to the portfolio itself, there is arguably little relevance for charging an AUM fee – especially in the context of working with middle-income or younger clientele, where there is little if any portfolio to manage in the first place. Not surprisingly, this is why hourly fees, and more recently monthly retainer fees, have become an increasingly popular business model for serving this clientele (not to mention retainer fees in general for clients who do not have portfolio-centric needs). The good news in this category is that pricing pressure is more limited, due to the fact that financial planning services are not commoditized and its hard for consumers to compare them at all; on the other hand, fees that are paid directly (e.g., by check) tend to be more salient, which itself still creates some significant pricing pressure. The more focused and niche the financial planning business is, though, the less prone advisors will tend to be to pricing pressure, for the simple reason that fees in a highly-targeted niche business have no real point of competitive price comparison in the first place!

In the middle of all of these categories sits the advisor gamma value of “closing the behavior gap”, a service that arguably still fits an AUM fee context – as the benefit of the outcome is directly related to the size of the portfolio that the client doesn’t unwittingly damage with bad behaviors! On the other hand, providing “behavior gap protection” services is inherently challenging to price, for the simple reason that clients can only justify the cost of the fee by first admitting that they are incapable of being successful on their own and that they are their own worst enemy – which, while objectively true for at least some clientele, may not necessarily be something they are willing to admit to themselves!

The Great Unbundling – Will Low-Cost Beta Force Advisors To Reduce Or Unbundle AUM Fees?

In light of the fact that AUM fees are relevant to some services more than others – and in particular, tends to be least relevant for the most “pure” (non-portfolio-centric) financial planning services – the third and final question that arises is: will advisors eventually be forced to significantly reduce, or entirely “unbundle”, their financial planning services from the AUM fee structure?

For advisors who solely offer financial planning services, and do not manage portfolios already, the reality is that such services have unbundled from the AUM fee, as such advisors are already charging hourly fees, monthly or annual retainer fees, or standalone project fees for modular financial plan solutions. After all, if there’s really no portfolio involved, there was never really an AUM fee in the first place.

For those who have previously charged an AUM fee to simply purchase a passive, strategic portfolio – i.e., to just buy beta – and then provide additional services on top, the pressure to unbundle may be more significant, as the price point of beta move towards zero and in the end, all the advisor is really substantively providing are the non-portfolio (and non-AUM-based) financial planning services anyway.

At the other end of the spectrum, advisors whose primary value-add really is some form of alpha-related offering – whether at the security or asset class level – the AUM fee arguably remains as relevant as ever. While the pricing pressure may be on – and some will contend that alpha is increasingly difficult to find in the first place – for better or worse, the pressure will be on delivering alpha to validate the value proposition, not whether an AUM fee is an appropriate way to charge for it. Similarly, advisors – and robo-advisors – who provide portfolio-related gamma, such as automated rebalancing, ongoing tax-loss harvesting, asset location, etc., will likely still charge AUM fees as well, though the pricing pressure for such a potentially-commoditized service may become so severe that the AUM fee is compressed to the point of requiring tremendous scale for any profitability (limiting its value for individual advisors unless they have access to the technology as part of their platform).

The greatest ambiguity, then, will be for advisors who do not offer “just” financial planning gamma or “just” portfolio-related alpha and gamma, but who offer a combination of both for a combined, bundled fee. Arguably, this model is the most popular of all in the current marketplace, as fee-for-financial-planning firms have struggled to scale, and investment-only firms have struggled with being commoditized and the rising pressure to justify their often-not-delivered alpha; by combining both under a single pricing structure and business model, firms effectively “diversify” their value proposition, such that hopefully at least one part or another will be “working” in any particular year.

From this perspective, it’s really not clear whether unbundling will occur anytime soon. In fact, in recent years, the trend has been the exact opposite direction, with the “insourcing” of financial planning as large asset management firms and platforms add financial planning services to their existing AUM-fee structure, from the expansion of Vanguard Personal Advisor Services to the growth of Schwab Private Client. In this context, financial planning fees are either relatively modest (especially given the net worth sometimes involved), or are entirely free simply because the firm recognizes that if financial planning services improve client retention, the increase in lifetime client value justifies the entire cost of the service without charging the client at all. And even the wirehouses have been increasingly shifting towards comprehensive AUM fees in recent years to cover investment management and a broad range of supporting advisory services.

Certainly, this bundling of fees will have a natural limit – if the firm is delivering no alpha (or portfolio-specific gamma) over time, the pressure will be on to unbundle the fee, and charge a (very low if any) AUM fee just for portfolio services (and buying access to beta), with a separate service-appropriate fee for financial planning.

Nonetheless, for the time being, it appears that while financial planning fees may be unbundling from charging AUM for beta – if only because the price of beta is going to zero – the broader trend of unbundling financial planning fees from AUM fees altogether may still be a ways off. In fact, given the challenge of getting clients to cut a check to pay for a service as intangible as financial planning (and the impact of making the fee so salient), firms that can resist unbundling fees will likely do so as long as possible, as the long-term growth rate of the AUM business model may still be more compelling than its retainer-based alternative (at least when serving clients who have assets in the first place). Ironically, the ultimate death knell for the bundled fee structure may not be the difficulty of delivering beta for an AUM fee, but the difficult of delivering alpha for an AUM fee, given that alpha seems to be the next/current (and possibly last?) bastion of the AUM fee in today’s world.

The bottom line, though, is simply this: the declining cost of beta will (and has already) put significant pressure on advisors charging AUM fees while delivering little actual portfolio value-add, and is already driving firms to look at adding other value-add services (e.g., various “advisor gamma” benefits like financial planning) to defend their fee structure. And the reality is that AUM fees limit who can be served in the first place – i.e., working with younger clientele necessitates a different business model like monthly retainers. Nonetheless, for those who do have the net worth to be served by an AUM model – and as long as firms still have some portfolio value-add to provide – a bundled AUM fee may still be the strongest business model for the time being, and the shift of more and more large asset management firms towards bundling AUM and financial planning services seems for the time being to suggest that the trend is not away from the AUM fee, but is still towards it!